|

市場調査レポート

商品コード

1716471

ユーティリティスケール高電圧変圧器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Utility Scale High Voltage Power Transformer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ユーティリティスケール高電圧変圧器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月27日

発行: Global Market Insights Inc.

ページ情報: 英文 131 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

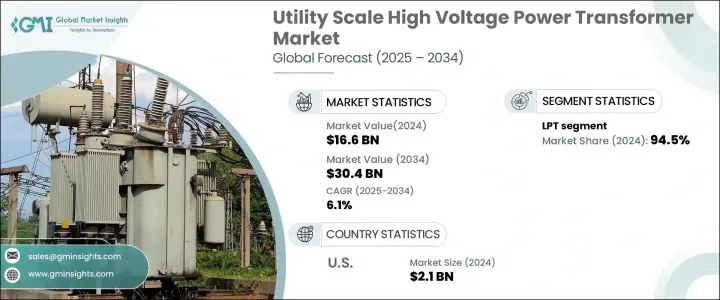

世界のユーティリティスケール高電圧変圧器市場は、2024年に166億米ドルと評価され、2025年から2034年にかけてCAGR 6.1%で拡大すると予測されています。

同市場は、変圧器材料の技術進歩、絶縁システムの改善、スマートグリッド技術の統合によって力強い成長を遂げています。これらの技術革新により、高圧変圧器の効率、信頼性、寿命が向上し、現代のエネルギー・インフラにとって重要な部品となっています。さらに、風力発電や太陽光発電を含む再生可能エネルギー発電の導入が増加しているため、高圧変圧器の需要が大幅に増加しています。高圧変圧器は、再生可能エネルギー発電で発電した電力を長距離送電し、既存の送電網システムとの互換性を確保するために不可欠です。

世界中でエネルギー転換と脱炭素化がますます推進されているため、送電網のアップグレードに多額の投資が行われています。政府と電力事業者は、信頼性と効率を向上させるため、送電網内のエネルギーの流れを自動化することに注力しています。このような送電網の近代化が進むにつれて、油浸変圧器の需要が高まっています。油浸入変圧器は電圧変動に対応するのに適しており、現代の送電網システムにおける拡張可能なアプリケーションに最適です。さらに、最近の動向により、エネルギー損失を最小限に抑える高度な冷却システムを備えた油浸変圧器が開発されています。これらの変圧器は、発電所、送電網、屋外工業地帯での使用がますます好まれるようになっており、予測期間中の需要増加に寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 166億米ドル |

| 予測金額 | 304億米ドル |

| CAGR | 6.1% |

大型電源変圧器(LPT)セグメントは2024年に94.5%のシェアを占め、市場を独占しました。この傾向は、工業化の進展と老朽化した送電網の近代化がLPT定格のユーティリティ規模高圧変圧器の需要を煽るため、今後も続くと予想されます。送電網の近代化は、送電網の回復力を強化し、より高い負荷に対応できる容量を増やすことを目的としており、LPTはエネルギー配電網の安定性を維持するために不可欠なものとなっています。さらに、送電網の近代化と再生可能エネルギーの統合を促進する政府の支援政策が、LPT市場を世界的にさらに強化しています。

米国では、公益事業規模の高圧変圧器市場は2024年に21億米ドルを生み出しました。エネルギー効率を促進する政府の強力な取り組みとスマートグリッド技術への投資が、公益事業用途の高度変圧器需要を促進しています。電力網における再生可能エネルギー源の割合増加に対応するため、エネルギー・インフラの近代化に重点を置く同国は、高圧変圧器市場の継続的拡大に有利な環境を作り出しています。電力会社が送電網の信頼性と効率の向上に努めていることから、技術的に先進的な変圧器に対する需要は、今後数年間で一貫した成長が見込まれます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:冷却材別、2021年~2034年

- 主要動向

- 乾式

- 油浸式

第6章 市場規模・予測:定格別、2021年~2034年

- 主要動向

- SPT(60 MVA以下)

- LPT(60 MVA超)

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- Bharat Bijlee

- Bharat Heavy Electricals

- CG Power &Industrial Solutions

- DAIHEN Corporation

- General Electric

- HD HYUNDAI ELECTRIC

- Hitachi Energy

- Hyosung Heavy Industries

- JSHP Transformer

- Kirloskar Electric Company

- LS ELECTRIC

- Siemens Energy

- Toshiba Energy Systems &Solutions

- WEG

The Global Utility Scale High Voltage Power Transformer Market was valued at USD 16.6 billion in 2024 and is projected to expand at a CAGR of 6.1% between 2025 and 2034. The market is witnessing robust growth driven by technological advancements in transformer materials, improved insulation systems, and the integration of smart grid technologies. These innovations enhance the efficiency, reliability, and lifespan of high-voltage transformers, making them critical components for modern energy infrastructure. Additionally, the rising adoption of renewable energy sources, including wind and solar power, has significantly increased the demand for high-voltage transformers, which are essential for transmitting electricity generated from renewable sources over long distances and ensuring compatibility with existing grid systems.

The increasing push for energy transition and decarbonization across the globe is driving significant investments in power grid upgrades. Governments and utility providers are focusing on automating energy flow within grids to improve reliability and efficiency. This ongoing modernization of power grids is boosting the demand for oil-immersed transformers, which are well-suited to handle voltage fluctuations and are ideal for scalable applications in contemporary grid systems. Furthermore, recent developments have led to the creation of oil-immersed transformers equipped with advanced cooling systems that minimize energy losses. These transformers are increasingly preferred for use in power plants, transmission networks, and outdoor industrial areas, contributing to their rising demand during the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.6 Billion |

| Forecast Value | $30.4 Billion |

| CAGR | 6.1% |

The large power transformer (LPT) segment dominated the market with a 94.5% share in 2024, a trend that is expected to continue as growing industrialization and the modernization of aging power grids fuel demand for LPT-rated utility-scale high voltage transformers. The modernization efforts aim to enhance grid resilience and increase the capacity to accommodate higher loads, making LPTs indispensable for maintaining stability in energy distribution networks. Additionally, supportive government policies promoting grid modernization and renewable energy integration are further strengthening the market for LPTs globally.

In the United States, the utility-scale high voltage power transformer market generated USD 2.1 billion in 2024. Strong government initiatives promoting energy efficiency and investment in smart grid technology are driving the demand for advanced transformers in utility applications. The country's emphasis on modernizing energy infrastructure to handle the increasing share of renewable energy sources in the power grid is creating a favorable environment for the continued expansion of the high voltage transformer market. With utilities striving to enhance grid reliability and efficiency, the demand for technologically advanced transformers is expected to witness consistent growth in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Cooling, 2021 – 2034 (USD Million, ‘000 Units)

- 5.1 Key trends

- 5.2 Dry type

- 5.3 Oil immersed

Chapter 6 Market Size and Forecast, By Rating, 2021 – 2034 (USD Million, ‘000 Units)

- 6.1 Key trends

- 6.2 SPT (≤ 60 MVA)

- 6.3 LPT (> 60 MVA)

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, ‘000 Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.3.5 Russia

- 7.3.6 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Bharat Bijlee

- 8.2 Bharat Heavy Electricals

- 8.3 CG Power & Industrial Solutions

- 8.4 DAIHEN Corporation

- 8.5 General Electric

- 8.6 HD HYUNDAI ELECTRIC

- 8.7 Hitachi Energy

- 8.8 Hyosung Heavy Industries

- 8.9 JSHP Transformer

- 8.10 Kirloskar Electric Company

- 8.11 LS ELECTRIC

- 8.12 Siemens Energy

- 8.13 Toshiba Energy Systems & Solutions

- 8.14 WEG