|

市場調査レポート

商品コード

1773239

海洋掘削廃棄物管理の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Offshore Drilling Waste Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 海洋掘削廃棄物管理の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月27日

発行: Global Market Insights Inc.

ページ情報: 英文 128 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

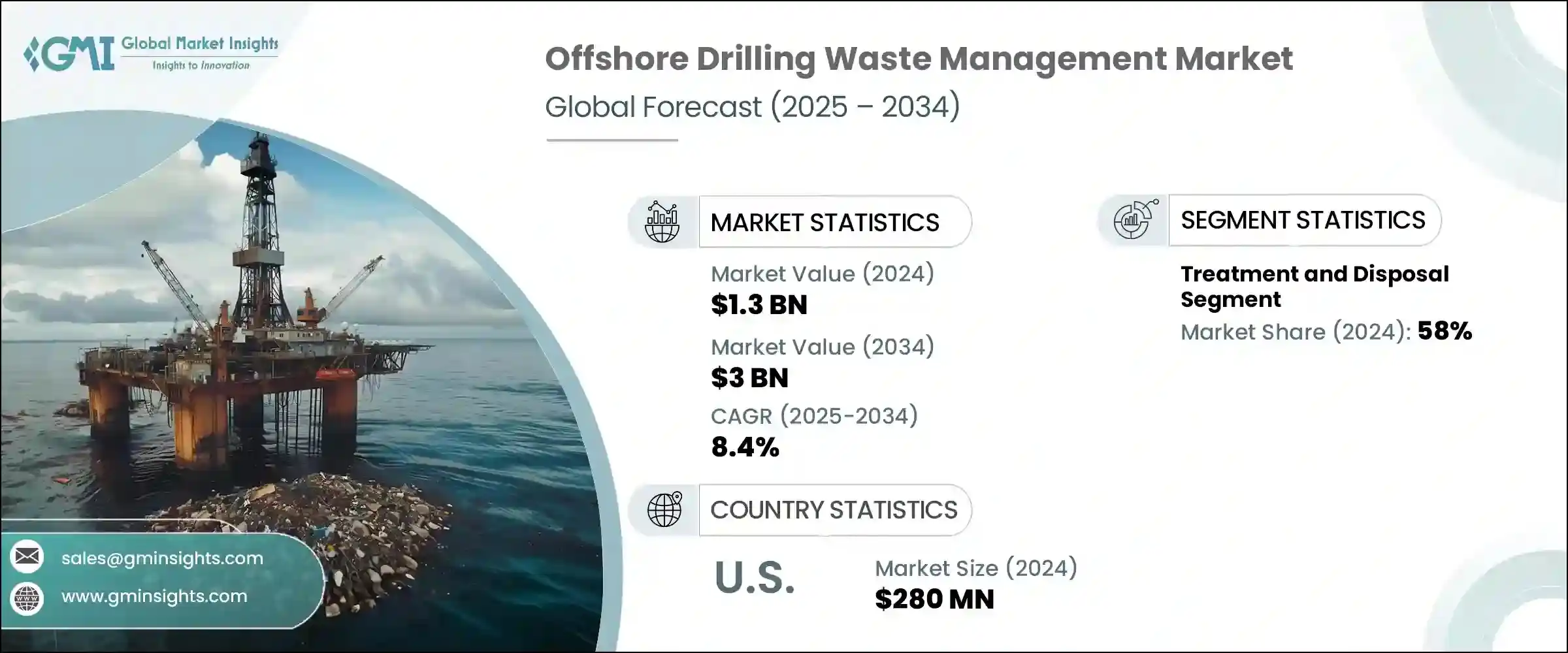

海洋掘削廃棄物管理の世界市場規模は、2024年に13億米ドルとなり、CAGR 8.4%で成長し、2034年には30億米ドルに達すると予測されています。

この市場の拡大は、特に環境への影響が大きな懸念事項となっている海洋掘削地帯で、厳しい環境規制の導入が進んでいることが大きな要因となっています。探鉱活動が深海や超深海の場所へとシフトし続けているため、掘削廃棄物の量と複雑さも増加しており、より高度で準拠性の高い廃棄物管理ソリューションが求められています。この成長は、石油・ガス業界における持続可能性の重視の高まりによってさらに後押しされており、事業者は生産効率を維持しながら環境フットプリントを削減する必要に迫られています。

海洋掘削では、掘削泥水、掘削くず、生産水など、さまざまな廃棄物の流れが発生するが、これらはすべて、環境汚染を防ぐために適切な封じ込め、治療、処分が必要です。これに対応するため、企業は海洋環境でこれらのマテリアルを処理するために特別に設計された技術に多額の投資を行っています。これには、クローズドループシステムや、特に生態学的に影響を受けやすいオフショア海域でのゼロ排出作業をサポートするソリューションが含まれます。複数の地域の規制機関がコンプライアンス対策を強化しているため、掘削会社は高度な廃棄物処理方法を採用し、より高い環境基準を維持することを余儀なくされています。その結果、海洋廃棄物管理サービスに対する需要は急増し、責任ある持続可能な操業に向けた業界全体のシフトを反映しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 13億米ドル |

| 予測金額 | 30億米ドル |

| CAGR | 8.4% |

同市場では、効率の向上、排出ガスの削減、海洋汚染の最小化に焦点を当てた技術革新も顕著に進んでいます。事業者は、最適なパフォーマンスとコンプライアンスを確保するために、リアルタイムのデータ追跡と自動化を提供する統合廃棄物管理システムを導入する傾向が強まっています。これらのデジタルソリューションは、廃棄物の組成と治療結果に関する洞察を提供し、迅速な意思決定とコスト管理の改善を可能にします。これらの技術の統合は、業務を合理化し、手作業による監督への依存を減らすことで、廃棄物管理業務を変革しています。

主要なサービスセグメントのうち、処理・廃棄は2024年の市場で最大のシェアを占め、全体の収益の約58%を占めています。このセグメントには、熱処理、化学的中和、固形化、生物学的処理など、幅広い処理方法が含まれます。環境に優しく、低排出ガス処理ソリューションへの嗜好の高まりは、従来の手法から脱却し、長期的な環境負債の削減に重点を置く企業によって、サービス提供の形を変えつつあります。海洋事業者は特に、廃棄物を現場で処理できる原位置処理オプションに傾倒しており、大規模な輸送の必要性を削減し、環境リスクを最小限に抑えています。

米国の市場は大きな勢いを見せており、海洋掘削廃棄物管理分野の市場規模は2022年に2億3,000万米ドル、2023年に2億5,000万米ドル、2024年に2億8,000万米ドルと評価されています。この成長には、厳格な環境政策の施行、海洋掘削プロジェクトの拡大、持続可能性への業界全体の関心の高まりなど、さまざまな要因が絡み合っています。掘削強度の増加による廃棄物発生量の増加は、高度な廃棄物処理・封じ込めソリューションの需要拡大につながりました。規制当局が監視を強化し、技術基準を精緻化する中、事業者は既存のシステムをアップグレードし、より安全で効果的な廃棄物処理方法を採用する必要に迫られています。

市場情勢の競合情勢は、多国籍企業と地域企業によって形成されています。2024年には、上位5社(Baker Hughes、Halliburton、Weatherford、SLB、TWMA)が合わせて世界市場シェアの30%以上を占めています。これらの企業は、包括的なサービスポートフォリオ、世界な操業能力、技術革新の組み合わせによってその地位を固めてきました。廃棄物の封じ込めから処理、輸送、最終処分まで、エンドツーエンドの廃棄物管理ソリューションを提供する能力により、複雑なオフショアプロジェクトに対応する上で際立った強みを発揮しています。大手企業に加え、定評のある地域企業やニッチな地元サービスプロバイダーのネットワークが競争力を高め、技術や業務のベストプラクティスの継続的な進歩を促しています。

主要企業は戦略的に、効率性とコンプライアンスを強化するために、サービスの統合とデジタルトランスフォーメーションを優先しています。単一のサービス傘下で完全な廃棄物管理エコシステムを提供することで、オフショア顧客のベンダー調整を簡素化すると同時に、パフォーマンスを最適化し、運用コストを削減しています。また、これらの企業は、廃棄物処理プロセスのトレーサビリティを改善し、プロジェクトのライフサイクル全体にわたってより良い意思決定を推進するために、リアルタイムのモニタリングシステムとデータ分析を採用しています。市場が進化するにつれ、こうしたイノベーションは競争力を維持し、規制や持続可能性への期待の高まりに応えるために不可欠なものとなると思われます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的取り組み

- 競合ベンチマーキング

- 戦略ダッシュボード

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:サービス別、2021年~2034年

- 主要動向

- ソリッドコントロール

- 封じ込めと取り扱い

- 処理と廃棄

- その他

第6章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- ラテンアメリカ

- ブラジル

- アルゼンチン

第7章 企業プロファイル

- Augean

- Baker Hughes Company

- CLEAN HARBORS, Inc.

- Derrick Corporation

- Geminor

- GN Solids Control

- Halliburton

- Imdex Limited

- Newpark Drilling Fluids LLC

- NOV

- Ridgeline Canada Inc.

- Secure Energy Services

- SELECT WATER SOLUTIONS

- SLB

- Soli-Bond, Inc.

- TWMA

- Weatherford

The Global Offshore Drilling Waste Management Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 3 billion by 2034. The expansion of this market is largely driven by the growing implementation of stringent environmental regulations, particularly in offshore drilling zones where environmental impact is a significant concern. As exploration activities continue to shift toward deepwater and ultra-deepwater locations, the volume and complexity of drilling waste are also rising, demanding more advanced and compliant waste management solutions. This growth is further supported by the increasing emphasis on sustainability within the oil and gas industry, with operators under pressure to reduce their environmental footprint while maintaining production efficiency.

Offshore drilling generates a variety of waste streams, including drilling fluids, drill cuttings, and produced water, all of which require proper containment, treatment, and disposal to prevent environmental contamination. In response, companies are investing heavily in technologies specifically designed to handle these materials in offshore environments. This includes solutions that support closed-loop systems and zero-discharge operations, especially in ecologically sensitive offshore areas. Regulatory agencies across multiple regions are reinforcing compliance measures, compelling drilling companies to adopt advanced waste handling practices and maintain higher environmental standards. As a result, the demand for offshore waste management services has surged, reflecting a broader industry shift toward responsible and sustainable operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $3 Billion |

| CAGR | 8.4% |

The market has also seen notable advancements in technology, with innovations focused on improving efficiency, reducing emissions, and minimizing marine pollution. Operators are increasingly implementing integrated waste management systems that offer real-time data tracking and automation to ensure optimal performance and compliance. These digital solutions provide insights into waste composition and treatment outcomes, enabling quicker decision-making and improved cost control. The integration of these technologies is transforming waste management practices by streamlining operations and reducing reliance on manual oversight.

Among the key service segments, treatment and disposal accounted for the largest share of the market in 2024, commanding approximately 58% of the overall revenue. This segment includes a wide array of treatment methods such as thermal processing, chemical neutralization, solidification, and biological treatment. The growing preference for eco-friendly and low-emission treatment solutions is reshaping service offerings, with companies moving away from conventional practices and focusing on reducing long-term environmental liabilities. Offshore operators are particularly inclined toward in-situ treatment options that allow waste to be processed on-site, cutting down the need for extensive transport and minimizing environmental risk.

The market in the United States has shown significant momentum, with the offshore drilling waste management sector valued at USD 230 million in 2022, USD 250 million in 2023, and USD 280 million in 2024. This growth is fueled by a combination of factors, including the enforcement of rigorous environmental policies, expansion in offshore drilling projects, and a growing industry-wide focus on sustainability. The rise in waste generation due to increased drilling intensity has led to greater demand for advanced waste processing and containment solutions. With regulatory authorities stepping up oversight and refining technical standards, operators are being pushed to upgrade existing systems and adopt safer, more effective methods for waste handling.

The competitive landscape of the offshore drilling waste management market is shaped by a mix of multinational corporations and regional players. In 2024, the top five companies- Baker Hughes, Halliburton, Weatherford, SLB, and TWMA-together held over 30% of the global market share. These companies have cemented their positions through a combination of comprehensive service portfolios, global operational capabilities, and technological innovation. Their ability to deliver end-to-end waste management solutions-from waste containment to treatment, transportation, and final disposal-gives them a distinct edge in servicing complex offshore projects. Alongside the major players, a network of established regional firms and niche local service providers adds to the competitive intensity, encouraging continuous advancements in technology and operational best practices.

Strategically, leading companies are prioritizing service integration and digital transformation to enhance efficiency and compliance. By offering complete waste management ecosystems under a single service umbrella, they are simplifying vendor coordination for offshore clients while optimizing performance and reducing operational costs. These players are also adopting real-time monitoring systems and data analytics to improve the traceability of waste handling processes and drive better decision-making across project lifecycles. As the market evolves, such innovations are likely to become essential for maintaining competitiveness and meeting rising regulatory and sustainability expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic initiative

- 4.4 Competitive benchmarking

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Service, 2021 - 2034, (USD Billion)

- 5.1 Key trends

- 5.2 Solid control

- 5.3 Containment & handling

- 5.4 Treatment & disposal

- 5.5 Others

Chapter 6 Market Size and Forecast, By Region, 2021 - 2034, (USD Billion)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 France

- 6.3.3 UK

- 6.3.4 Spain

- 6.3.5 Italy

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 Australia

- 6.4.5 South Korea

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 South Africa

- 6.5.3 UAE

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Argentina

Chapter 7 Company Profiles

- 7.1 Augean

- 7.2 Baker Hughes Company

- 7.3 CLEAN HARBORS, Inc.

- 7.4 Derrick Corporation

- 7.5 Geminor

- 7.6 GN Solids Control

- 7.7 Halliburton

- 7.8 Imdex Limited

- 7.9 Newpark Drilling Fluids LLC

- 7.10 NOV

- 7.11 Ridgeline Canada Inc.

- 7.12 Secure Energy Services

- 7.13 SELECT WATER SOLUTIONS

- 7.14 SLB

- 7.15 Soli-Bond, Inc.

- 7.16 TWMA

- 7.17 Weatherford