|

市場調査レポート

商品コード

1773257

掘削廃棄物管理の封じ込め・取り扱いの市場機会、成長促進要因、産業動向分析、2025~2034年予測Containment and Handling Drilling Waste Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 掘削廃棄物管理の封じ込め・取り扱いの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年06月25日

発行: Global Market Insights Inc.

ページ情報: 英文 134 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

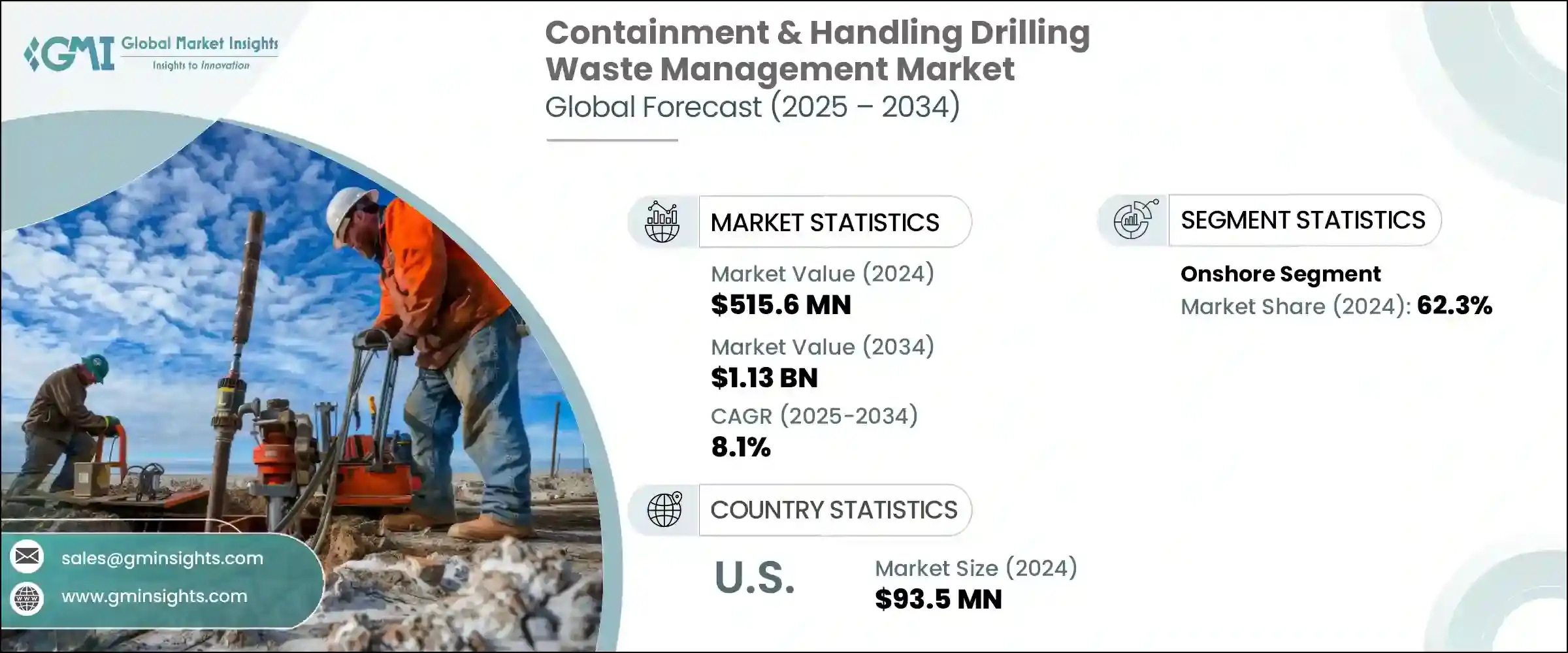

掘削廃棄物管理の封じ込め・取り扱いの世界市場は、2024年には5億1,560万米ドルと評価され、CAGR 8.1%で成長し、2034年には11億3,000万米ドルに達すると推定されています。

掘削廃棄物の処理に関する環境規制がますます厳しくなっていることが、市場成長を形成する主な力となっています。世界各国の政府は、掘削泥水、掘削くず、関連汚染物質の管理、封じ込め、最終処分に関して、生態系への害を最小限に抑えるため、より厳しい政策を実施しています。このような規制枠組みの強化により、企業はより高度な廃棄物処理ソリューションの採用を余儀なくされています。

さらに、現場での廃棄物処理の改善と、従来の油性または合成泥水に比べて有害廃棄物の発生が少ない水性掘削泥水へのシフトが、市場力学に影響を及ぼしています。しかし、一部の油性掘削廃棄物は依然として環境当局によって有害廃棄物に分類されており、より複雑でコストのかかる廃棄処理が要求されています。このような環境面での監視の高まりが、技術革新の急増に拍車をかけ、業界全体で大きな投資を引き寄せています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 5億1,560万米ドル |

| 予測金額 | 11億3,000万米ドル |

| CAGR | 8.1% |

企業は、規制当局の要求を満たすだけでなく、それを上回る高度な技術やよりスマートなソリューションの開発に意欲を燃やしています。こうした動きは、AI主導の分析、リアルタイムのモニタリング、自動報告システムといった最先端のツールの採用を後押ししています。投資家は、持続可能な実践に長期的な価値があることを認識しており、環境コンプライアンスと業務効率を優先する企業に資本を誘導しています。その結果、この業界では、研究開発の加速化、戦略的パートナーシップの構築、製品ポートフォリオの拡充が進んでおり、ビジネスの成長をサポートしながら進化する環境課題に対処できるよう設計されています。

2024年には、オンショア事業部門が62.3%のシェアを占め、さまざまな新興経済国での水圧破砕の展開拡大に牽引されます。このような大量の掘削活動により、大量のドリルくず、逆流液、生産水が発生します。これらの水はすべて、下流での処理や廃棄の前に、現場での安全な封じ込めソリューションが必要となります。資源が豊富な地域で掘削が強化されるにつれ、拡張性があり、法令に準拠した廃棄物処理システムに対する需要が急増しています。オペレーターは、環境コンプライアンスと操業効率基準の両方に適合させるため、封じ込め装置と現場固有のインフラへの投資を優先しています。

米国の2024年の市場規模は9,350万米ドルとなりました。米国とカナダは、特に排出物、水の安全性、土地利用をめぐる厳しい連邦および地域の環境規制による圧力の高まりに直面し続けています。頁岩(けつがん)の多い地層での掘削活動の活発化と相まって、この規制環境は、高度な封じ込め技術と持続可能な廃棄物処理枠組みへのシフトを加速させています。この地域では、生産量を維持しながら生態系リスクを低減することに重点を置いているため、掘削廃棄物管理慣行の世界標準を形成する上で北米の役割はさらに強固なものとなっています。

この市場で積極的に事業を展開している企業には、Baker Hughes、Schlumberger、Clean Harbors、Halliburton、GN Solids Control、Newpark Resources、TWMA、Derrick Equipment Company、Secure Energy Services、Imdex、Ridgeline Canada、Soli-Bond、Select Water Solutions、Weatherford、Augean、NOVなどがあります。市場での地位を固めるため、大手企業は、規制上の要求に合わせた高度な現場廃棄物処理や封じ込めシステムなど、技術力の拡大に注力しています。

これらの企業は、生態系への影響を低減する、より安全で効率的な処理ソリューションを開発することで、進化する環境基準への準拠を優先しています。戦略的パートナーシップや買収は、サービス提供や地理的範囲を広げるために一般的です。多くの企業は、特に粘性物質や有害物質のような困難な廃棄物の流れを取り扱う製品イノベーションを強化するために、RandDに投資しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク・課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- 技術・イノベーションの情勢

第5章 市場規模・予測:用途別、2021~2034年

- 主要動向

- オンショア

- オフショア

第6章 市場規模・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- ラテンアメリカ

- ブラジル

- アルゼンチン

第7章 企業プロファイル

- Augean

- Baker Hughes

- Clean Harbors

- Derrick Equipment Company

- Geminor

- GN Solids Control

- Halliburton

- Imdex

- Newpark Resources

- NOV

- Ridgeline Canada

- Schlumberger

- Secure Energy Services

- Select Water Solutions

- Soli-Bond

- TWMA

- Weatherford

The Global Containment and Handling Drilling Waste Management Market was valued at USD 515.6 million in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 1.13 billion by 2034. Increasingly stringent environmental regulations around the disposal of drilling waste are a primary force shaping market growth. Governments worldwide are enforcing tougher policies on the management, containment, and final disposal of drilling muds, cuttings, and related pollutants to minimize ecological harm. This tightening regulatory framework is compelling companies to adopt more advanced waste-handling solutions.

Additionally, improvements in on-site waste treatment and a shift toward water-based drilling fluids, which produce less hazardous waste compared to traditional oil-based or synthetic muds, are influencing market dynamics. However, some oil-based drilling waste remains classified as hazardous by environmental authorities, leading to more complex and costly disposal requirements. This increasing environmental scrutiny is fueling a surge in innovation and attracting significant investment across industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $515.6 Million |

| Forecast Value | $1.13 Billion |

| CAGR | 8.1% |

Companies are motivated to develop advanced technologies and smarter solutions that not only meet but exceed regulatory demands. This push is encouraging the adoption of cutting-edge tools such as AI-driven analytics, real-time monitoring, and automated reporting systems. Investors recognize the long-term value in sustainable practices, directing capital toward firms that prioritize environmental compliance and operational efficiency. As a result, the industry is witnessing accelerated research and development efforts, strategic partnerships, and expanded product portfolios designed to address evolving environmental challenges while supporting business growth.

In 2024, the onshore operations segment captured a 62.3% share, driven by the expanding footprint of hydraulic fracturing across various emerging economies. These high-volume drilling activities result in significant amounts of drill cuttings, flowback fluids, and produced water-all of which require secure on-site containment solutions before any downstream processing or disposal. As drilling intensifies in resource-rich territories, the demand for scalable and compliant waste-handling systems is rising sharply. Operators are prioritizing investments in containment equipment and site-specific infrastructure to align with both environmental compliance and operational efficiency standards.

United States Containment and Handling Drilling Waste Management Market was valued at USD 93.5 million in 2024. The U.S. and Canada continue to face mounting pressure from rigorous federal and regional environmental regulations, particularly around emissions, water safety, and land use. Combined with heightened drilling activity in shale-rich formations, this regulatory environment has accelerated the shift toward advanced containment technologies and sustainable waste-handling frameworks. The region's focus on reducing ecological risks while maintaining production output further solidifies North America's role in shaping global standards for drilling waste management practices.

Companies actively operating in this market include Baker Hughes, Schlumberger, Clean Harbors, Halliburton, GN Solids Control, Newpark Resources, TWMA, Derrick Equipment Company, Secure Energy Services, Imdex, Ridgeline Canada, Soli-Bond, Select Water Solutions, Weatherford, Augean, and NOV. To solidify their market position, leading players focus on expanding technological capabilities, including advanced on-site waste treatment and containment systems tailored to regulatory demands.

They prioritize compliance with evolving environmental standards by developing safer, more efficient handling solutions that reduce ecological impact. Strategic partnerships and acquisitions are common to broaden service offerings and geographic reach. Many companies invest in RandD to enhance product innovation, particularly around handling challenging waste streams like viscous or hazardous materials.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Market estimates and forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls and challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation and technology landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Onshore

- 5.3 Offshore

Chapter 6 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 France

- 6.3.3 UK

- 6.3.4 Spain

- 6.3.5 Italy

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 Australia

- 6.4.5 South Korea

- 6.5 Middle East and Africa

- 6.5.1 Saudi Arabia

- 6.5.2 South Africa

- 6.5.3 UAE

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Argentina

Chapter 7 Company Profiles

- 7.1 Augean

- 7.2 Baker Hughes

- 7.3 Clean Harbors

- 7.4 Derrick Equipment Company

- 7.5 Geminor

- 7.6 GN Solids Control

- 7.7 Halliburton

- 7.8 Imdex

- 7.9 Newpark Resources

- 7.10 NOV

- 7.11 Ridgeline Canada

- 7.12 Schlumberger

- 7.13 Secure Energy Services

- 7.14 Select Water Solutions

- 7.15 Soli-Bond

- 7.16 TWMA

- 7.17 Weatherford