電磁鋼板用コーティング市場のビジネスチャンス、成長要因、業界動向分析、および2026年~2035年の予測

Electrical Steel Coatings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 160 Pages

- 納期

- 2~3営業日

- 商品コード

- 2038377

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

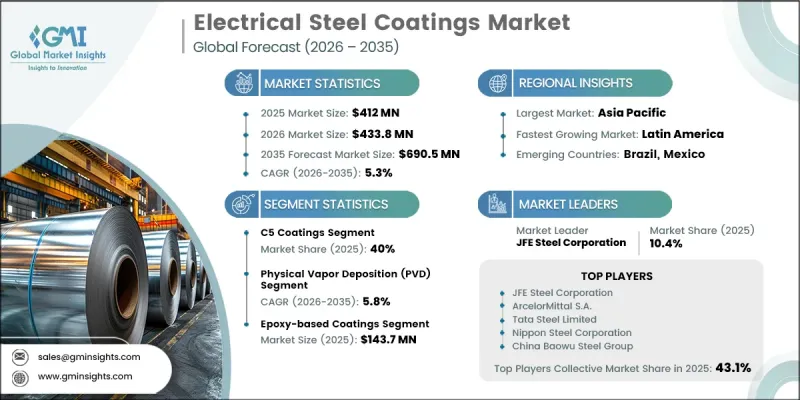

世界の電磁鋼板用コーティング市場は、2025年に4億1,200万米ドルと評価され、CAGR 5.3%で成長し、2035年までに6億9,050万米ドルに達すると予測されています。

この市場は、世界の電化への動き、持続可能性の目標、およびコーティング技術の継続的な進歩に支えられ、急速に進化しています。自動車の電化、再生可能エネルギーシステム、および産業機械からの需要の増加により、効率を高め、エネルギー損失を低減する高性能な電磁鋼板用コーティングの必要性がさらに高まっています。メーカー各社は、より厳格な環境基準や持続可能性への取り組みに対応するため、クロムフリーやホルムアルデヒドフリーの配合を含む、環境基準に適合したソリューションをますます優先しています。技術の進歩により生産手法は再構築されており、コスト効率の高さから無電解めっきが引き続き広く使用されている一方、高精度・高性能な用途では物理気相成長法(PVD)や化学気相成長法(CVD)の採用が進んでいます。材料の革新も加速しており、絶縁耐力と手頃な価格を理由にエポキシおよびポリエステル系コーティングが主流となっている一方で、クロム系ソリューションへの需要は引き続き減少しています。セラミック系、酸化マグネシウム、およびハイブリッドコーティングシステムにおける新たな開発により、耐久性、熱安定性、および環境性能が向上しています。鋼材の種類という観点では、結晶粒配向電磁鋼板(GOES)はその優れた磁気効率により変圧器用途において依然として不可欠ですが、非結晶粒配向電磁鋼板(NOES)は、特に電動モビリティ分野において、電気モーター用途で急速に普及しています。変圧器が依然として需要の大部分を占めていますが、電動機、特にEVの駆動システムが最も急成長しているセグメントとして台頭しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時点の市場規模 | 4億1,200万米ドル |

| 予測額 | 6億9,050万米ドル |

| CAGR | 5.3% |

C5コーティングセグメントは2025年に40%のシェアを占め、2035年までCAGR5.7%で成長すると予測されています。C3やC5などのコーティング分類は、モーターや変圧器の絶縁およびパンチ加工性要件において、依然として広く採用されています。C5AやC5ASなどの高度なバリエーションは、付着防止性能の向上とコーティング厚の低減を実現し、電気システムの運用効率向上に貢献しています。電動モビリティや小型電気機器への移行が進む中、次世代アプリケーションで使用される超薄型コーティングソリューションへの需要が大幅に高まっています。

結晶粒配向電磁鋼板(GOES)セグメントは、2025年に2億4,310万米ドルを占め、2026年から2035年にかけてCAGR 5.3%で成長すると予想されています。GOESは、他の鋼種と比較して優れた磁気特性と低いコア損失を持つため、変圧器用途において引き続き重要な役割を果たしています。対照的に、非結晶配向電磁鋼板(NOES)は、その均一な磁気特性と動的用途への適性から、EVシステムを含む電気モーターでの採用が拡大しています。

北米の電気鋼板コーティング市場は、2026年から2035年にかけてCAGR6%で成長すると予測されています。同地域の成長は、進行中の送電網近代化の取り組み、再生可能エネルギーインフラへの投資拡大、および電気自動車の普及拡大によって牽引されています。高度な変圧器や電動機に対する強い需要が市場の拡大をさらに後押ししている一方、環境規制の強化により、環境に優しいコーティング技術への移行が加速しています。継続的な技術革新と、確立されたメーカーの存在が、地域の市場発展をさらに支えると予想されます。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- コーティングの種類別

- 将来の市場動向

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許動向

- 貿易統計(HSコード)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境配慮型イニシアチブ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ(MEA)

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- パートナーシップおよび提携

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:コーティング種別、2022-2035

- C5コーティング

- C6コーティング

- C4コーティング

- C3コーティング

- C2コーティング

- その他のコーティング

第6章 市場推計・予測:コーティング技術別、2022-2035

- 物理気相成長(PVD)

- 化学気相成長(CVD)

- 無電解めっき

第7章 市場推計・予測:材料組成別、2022-2035

- エポキシ系塗料

- クロム含有塗料

- ポリエステル系塗料

- クロムフリー塗料

- フェノール系塗料

- ホルムアルデヒドフリー塗料

- MgO系塗料

- その他の材料タイプ

第8章 市場推計・予測:電磁鋼板の種類別、2022-2035

- 結晶粒配向電磁鋼板(GOES)

- 非結晶粒配向電磁鋼板(NOES)

- ケイ素鋼

第9章 市場推計・予測:用途別、2022-2035

- 変圧器

- 電動機

- 発電機

- インダクタ

- その他の用途

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第11章 企業プロファイル

- JFE Steel Corporation

- ArcelorMittal S.A.

- Tata Steel Limited

- Nippon Steel Corporation

- China Baowu Steel Group

- POSCO Holdings Inc.

- Voestalpine AG

- Axalta Coating Systems

- Dorf Ketal Chemicals

- Chemetall GmbH(BASF)

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 160 Pages

- 納期

- 2~3営業日