|

市場調査レポート

商品コード

1928973

自律移動ロボット市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Autonomous Mobile Robots (AMR) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 自律移動ロボット市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月14日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

概要

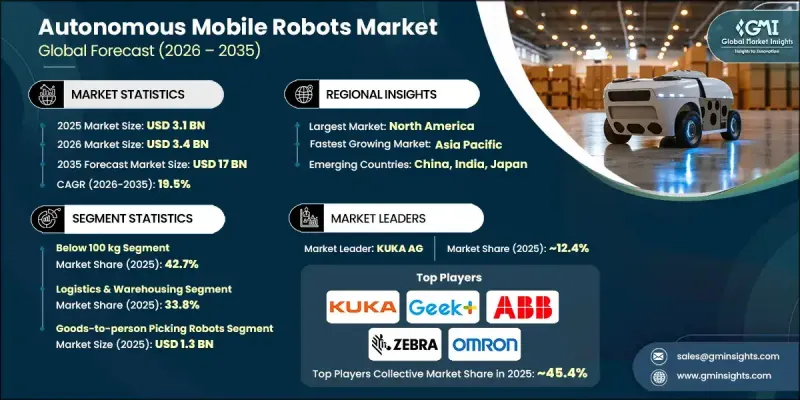

世界の自律移動ロボット(AMR)市場は、2025年に31億米ドルと評価され、2035年までにCAGR 19.5%で成長し、170億米ドルに達すると予測されています。

この市場成長は、物流、製造、医療、サービス指向環境における自動化の需要増加を反映しています。組織は職場の安全性向上、業務効率の強化、人的労働への依存度低減を目的として、自律移動ロボットの導入を拡大しています。自動化イニシアチブの拡大と業務の複雑化が進む中、インテリジェントなロボットソリューションへの需要は引き続き高まっています。荷役能力の進歩により、ロボットはより大きな積載量を管理できるようになり、作業サイクルを短縮し、施設全体のワークフロー効率を向上させています。人工知能(AI)と機械学習は現在、自律システムの核心的な構成要素となっており、適応型ナビゲーション、リアルタイム意思決定、高度なデータ処理を可能にしています。これらの機能により、ロボットは動的な環境下で効果的に機能すると同時に、精度と信頼性を向上させることができます。デジタルトランスフォーメーションが世界的に加速する中、自律移動ロボットは複数の産業にわたる現代的な業務戦略の不可欠な要素となりつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 31億米ドル |

| 予測金額 | 170億米ドル |

| CAGR | 19.5% |

2025年には、100kg未満のペイロードカテゴリーが42.7%のシェアを占めました。このセグメントのロボットは軽量作業向けに設計されており、エネルギー効率、精密なナビゲーション、コンパクトなフォームファクターに最適化されています。メーカーは、このペイロード範囲内の多様な運用要件を満たすため、バッテリー寿命の延長、正確な動作制御、安全なペイロード処理、コスト効率の高い拡張性を重視しています。

電子機器・半導体セグメントは、2026年から2035年にかけてCAGR20.8%で成長すると予測されています。この成長は、自動化ニーズの高まり、製造精度向上への要求、生産サイクルの高速化、厳格な品質基準によって支えられています。継続的な技術革新、柔軟な生産能力、研究開発への持続的な投資は、この分野に参入するメーカーにとって依然として重要です。

北米自律移動ロボット(AMR)市場は2025年に33.5%のシェアを占めました。地域的な成長は、先進的製造技術の採用、自動化物流ソリューションへの需要増加、人件費の上昇、ロボット技術革新への強力な投資によって牽引されています。スマート製造技術と柔軟な自動化システムの統合は、同地域における市場リーダーシップを強化し続けています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- エコシステム分析

- 業界への影響要因

- 促進要因

- 電子商取引と倉庫自動化の成長

- 医療・製薬分野における自律移動ロボットの拡大

- 農業および食品加工分野における自律移動ロボット(AMR)の導入

- 産業および物流業務における安全性・効率性の向上

- ホスピタリティ業界における自律移動ロボット(AMR)の応用拡大

- 課題と困難

- 自律移動ロボットに関連する高コスト

- 自律移動ロボット技術(AMR)の統合と導入における課題

- 市場機会

- ラストマイル配送における拡大

- スマート工場との統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 新興ビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 消費者心理分析

- 特許および知的財産分析

- 地政学的・貿易動向

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 市場集中度分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオ比較

- 製品ラインの広さ

- 技術

- イノベーション

- 地理的プレゼンス比較

- 世界展開分析

- サービスネットワークのカバー率

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー企業

- 課題者

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績比較

- 主な発展, 2021-2024

- 合併・買収

- 提携および共同事業

- 技術的進歩

- 拡大と投資戦略

- サステナビリティへの取り組み

- デジタルトランスフォーメーションの取り組み

- 新興/スタートアップ競合の動向

第5章 市場推計・予測:コンポーネント別、2022-2035

- ハードウェア

- ソフトウェア・サービス

第6章 市場推計・予測:タイプ別、2022-2035

- 商品搬送型ピッキングロボット

- 自律走行フォークリフト

- 自律型在庫管理ロボット

- 無人航空機

第7章 市場推計・予測:積載量別、2022-2035

- 100 kg未満

- 100kg~500kg

- 500kg超

第8章 市場推計・予測:ナビゲーション技術別、2022-2035

- レーザー/ライダー

- ビジョンガイダンス

- その他

第9章 市場推計・予測:電池タイプ別、2022-2035

- 鉛蓄電池

- リチウムイオン電池

- ニッケル系電池

- その他

第10章 市場推計・予測:用途別、2022-2035

- 選別

- 交通機関

- 組立

- 在庫管理

- その他

第11章 市場推計・予測:最終用途産業別、2022-2035

- 物流・倉庫業

- 小売り

- 自動車

- 電子機器・半導体

- 医薬品・ヘルスケア

- 食品・飲料

- 航空宇宙・防衛

- ホスピタリティ

- その他

第12章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第13章 企業プロファイル

- 世界の主要企業

- ABB Ltd.

- KUKA AG

- Omron Corporation

- Zebra Technologies Corp.

- 地域別主要企業

- 北米

- Aethon, Inc.

- Vecna Robotics

- ForwardX Robotics

- Mobile Industrial Robots

- アジア太平洋地域

- Geekplus Technology Co., Ltd.

- YUJIN ROBOT Co., Ltd.

- Honda Motor Co., Ltd.

- 欧州

- Fanuc

- GreyOrange

- Locus Robotics

- Murata Machinery, Ltd.

- 北米

- ニッチプレイヤー/ディスラプター

- Balyo

- Boston Dynamics

- Onward Robotics

- Seegrid

- Teradyne Inc.

- JBT