自動車用TICサービス市場の機会、成長要因、業界動向分析、および2026年~2035年の予測

Automotive TIC Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 290 Pages

- 納期

- 2~3営業日

- 商品コード

- 2045713

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

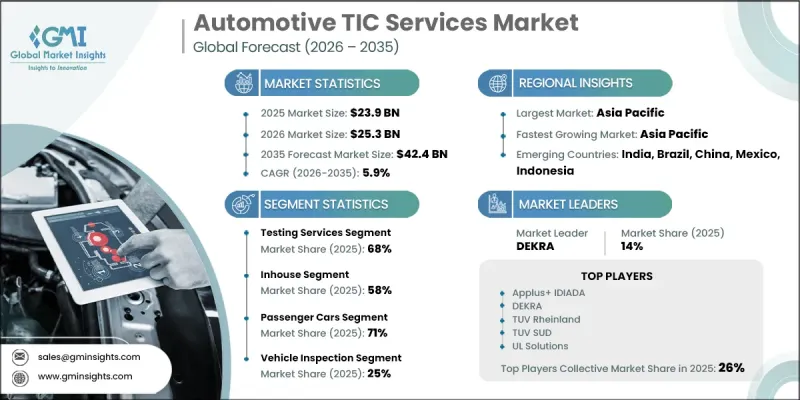

世界の自動車用TICサービス市場は、2025年に239億米ドルと評価され、CAGR5.9%で成長し、2035年までに424億米ドルに達すると推定されています。

規制当局が車両の安全性、排出ガス規制、サイバーセキュリティ要件に関するより厳格な基準を引き続き施行していることから、市場は拡大しており、試験、検査、認証サービスへの依存度が高まっています。自動車製造とサプライチェーンの世界の化は、複数の地域にわたる標準化されたコンプライアンスフレームワークの必要性をさらに高めています。電動モビリティの急速な進展は、特にバッテリー性能、熱効率、充電システムなどのセグメントにおいて、専門的な検証能力への需要を強めています。同時に、車両への高度ソフトウェアシステムの統合が進むにつれ、産業の焦点は、コネクテッド技術やインテリジェント技術に対する継続的な検証プロセスへと移行しています。このセグメントにおけるデジタルトランスフォーメーションも調査手法に影響を与えており、高度シミュレーションツールによって効率が向上し、開発期間が短縮されています。さらに、商用車両の運営事業者は、運用上の信頼性を高め、コンプライアンスを確保し、パフォーマンスを最適化するためにTICサービスをますます活用しており、自動車エコシステム全体における持続的な市場成長に寄与しています。

| 市場の範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026~2035年 |

| 開始時の市場規模 | 239億米ドル |

| 予測額 | 424億米ドル |

| CAGR | 5.9% |

試験サービス部門は2025年に68%のシェアを占め、2026~2035年にかけてCAGR5.4%で成長すると予想されています。これらのサービスは、安全、性能、排出ガスに関する要件への準拠を確保するため、制御環境と実稼働環境の両方において、車両システム、コンポーネント、完成ユニットの評価に重点を置いています。その範囲には、規制当局の承認を支援し、製品の信頼性を維持するために設計された複数の検証プロセスが含まれます。

社内セグメントは2025年に58%のシェアを占め、2035年までCAGR 4.9%で成長すると予測されています。社内のTIC(試験・検査・認証)能力により、自動車メーカーはテストと認証のワークフローを完全に管理できるようになり、その結果、実行の迅速化、データセキュリティの向上、社内開発プロセスとの整合性の向上が図られます。しかし、こうした能力を維持するには、高度インフラ、技術的専門知識、継続的なシステムアップグレードへの多額の投資が必要となるため、一貫した試験ニーズを持つ大規模メーカーにとってより現実的な選択肢となります。

米国の自動車用TICサービス市場は2025年に51億米ドルに達し、2026~2035年にかけてCAGR 6.3%で成長すると予想されています。市場の成長は、安全性、排出ガス規制への適合、高度な車両検証要件を重視する強力な規制環境によって支えられています。電気自動車の安全基準への注目が高まり、コンプライアンスの枠組みが進化していることから、全米における包括的なTICサービスへの需要はさらに強まっています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 産業洞察

- 産業エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 厳格な規制遵守

- 自動車産業の世界の化

- 車両性能検査への需要の高まり

- 品質保証に対する消費者の需要

- 産業の潜在的リスク・課題

- 高度TIC機器の高コスト

- 複雑な規制環境

- 市場機会

- 新興市場の成長機会

- 電気自動車と自動運転車の開発

- 商用車用TICサービスの拡大

- TICサービスへの先端技術の統合

- 促進要因

- 成長ポテンシャル分析

- 技術とイノベーションの展望

- 最新技術動向

- 新規技術

- 価格分析

- 過去の価格動向分析

- 参入企業タイプ別価格戦略(プレミアムバリューコストプラス)

- 規制情勢

- 北米

- 米国道路交通安全局

- 環境保護庁

- 欧州

- 欧州の委員会

- 国連欧州の経済委員会

- アジア太平洋

- 工業情報化部

- 道路運輸・高速道路省

- ラテンアメリカ

- 国立陸上運輸庁

- インフラ通信・運輸省

- 中東・アフリカ

- サウジアラビア規格・計量・品質機構

- 強制規格に関する国家規制機関

- 北米

- ポーターの分析

- PESTLE分析

- コスト内訳分析

- 特許分析

- AIと生成AIが市場に与える影響

- AIによる既存ビジネスモデルの変革

- セグメントによる生成AIのユースケースと導入ロードマップ

- リスク、制約、規制上の考慮事項

- 持続可能性と環境面

- サステイナブル取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントへの配慮

- 予測前提条件とシナリオ分析

- ベースケース:CAGRを牽引する主要なマクロ経済と産業変数

- 楽観的シナリオ:マクロ経済と産業における追い風

- 悲観シナリオ:マクロ経済の減速または産業の逆風

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 北米

- 欧州

- アジア太平洋

- LATAM

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併・買収

- パートナーシップ・提携

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推定・予測:サービス別、2022~2035年

- 試験サービス

- 検査サービス

- 認証サービス

- その他

第6章 市場推定・予測:ソーシング別、2022~2035年

- 社内

- 外部委託

第7章 市場推定・予測:車両別、2022~2035年

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- LCV

- MCV

- HCV

第8章 市場推定・予測:用途別、2022~2035年

- 自動車検査

- 排出ガス検査

- 部品検査

- テレマティクス

- ADAS

- 型認定検査

- 燃料、流体と潤滑油

- 電気システムと部品

- その他

第9章 市場推定・予測:地域別、2022~2035年

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧

- ロシア

- ポーランド

- ルーマニア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- ベトナム

- インドネシア

- フィリピン

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 世界企業

- Bureau Veritas

- DEKRA

- Eurofins Scientific

- Element Materials Technology

- Intertek

- SGS

- TUV Rheinland

- TUV SUD

- UL Solutions

- 地域企業

- Applus+IDIADA

- Automotive Research Association of India

- CATARC

- China Automotive Technology and Research Center

- Japan Automobile Research Institute

- Korea Testing Laboratory

- SOCOTEC

- TUV NORD

- 新興企業

- ALS

- CSA

- MISTRAS

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 290 Pages

- 納期

- 2~3営業日