|

|

市場調査レポート

商品コード

1570903

難聴疾患治療市場、機会、成長促進要因、産業動向分析と予測、2024年~2032年Hearing Loss Disease Treatment Market, Opportunity, Growth Drivers, Industry Trend Analysis and Forecast, 2024-2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 難聴疾患治療市場、機会、成長促進要因、産業動向分析と予測、2024年~2032年 |

|

出版日: 2024年08月07日

発行: Global Market Insights Inc.

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

世界の難聴疾患治療市場は、難聴の有病率の増加、認知度の向上、政府の支援策に牽引され、2024年から2032年にかけてCAGR 5.4%で成長します。

世界人口の高齢化に伴い、聴覚障害の発生率が上昇し、補聴器、人工内耳、薬などの治療オプションに対する需要が高まっています。公衆衛生キャンペーンは、早期診断や利用可能な治療法についての認識を高める一方、政府はアクセシビリティを向上させるための政策や資金援助を実施しており、今後数年間で市場規模をさらに拡大させるでしょう。

難聴疾患治療産業は、治療タイプ、症状、最終用途、地域によって区分されます。

機器分野は、補聴器、人工内耳、骨固定聴力システムの普及に後押しされ、2023年に97億米ドルを計上しました。これらの補聴器は、さまざまな程度の聴覚障害に効果的なソリューションを提供し、高い人気を集めています。ワイヤレス接続や音響増幅などの継続的な技術進歩がユーザー体験を向上させ、需要を促進しています。さらに、政府支援や保険適用によるアクセシビリティの向上が、機器セグメントの成長をさらに押し上げ、市場における優位性を確固たるものにしています。

感音性難聴分野は、その高い有病率と効果的な治療の必要性から、2032年までに125億米ドルを獲得します。感音性難聴は、内耳や聴覚神経の損傷によって引き起こされることが多く、高齢化や大きな騒音にさらされる人に多く見られます。人工内耳や補聴器などの先進的な治療法がこの症状の管理に広く用いられており、市場の成長を牽引しています。治療法に関する調査の増加も、このセグメントの主導的地位を支えています。

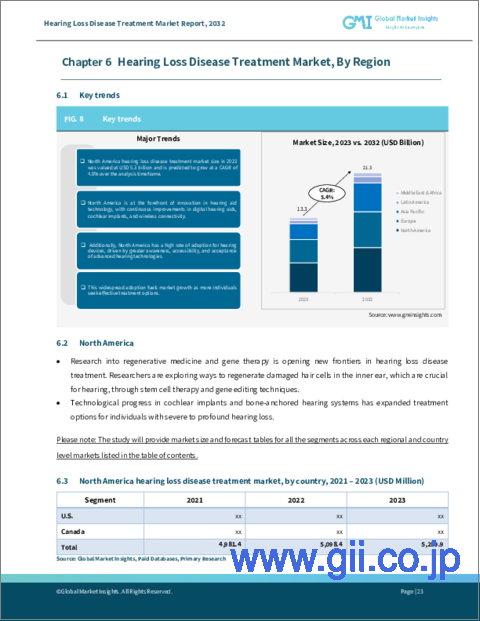

2023年、北米の難聴疾患治療市場は53億米ドルを記録し、2032年までのCAGRは4.8%に達する見込みです。この地域の高度なヘルスケアインフラ、難聴の高い有病率、革新的な治療技術の早期導入が拍車をかけています。人口の高齢化と啓蒙活動の広がりは、補聴器、人工内耳、その他の治療法の需要をさらに押し上げます。さらに、政府の強力な支援と有利な償還政策も市場の成長に寄与しています。堅調な研究イニシアティブと高いヘルスケア支出を誇る米国は、この地域支配に大きく貢献しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 末梢動脈疾患(PAD)の有病率の増加

- 難聴の有病率の上昇

- 技術の進歩

- 認知度と診断の向上

- 政府の支援イニシアティブ

- 業界の潜在的リスク&課題

- 機器や治療費の高騰

- 難聴に関する知識の不足

- 促進要因

- 成長可能性分析

- 技術展望

- 今後の市場動向

- 規制状況

- 製品パイプライン分析

- 償還シナリオ

- ポーター分析

- PESTEL分析

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:治療タイプ別、2021年~2032年

- 主要動向

- デバイス

- 補聴器

- BTE(耳かけ型)

- RITE/RIC(外耳道レシーバー)

- CIC/IIC(超小型耳あな型/インビジブル耳あな型)

- ITE(耳あな型)

- ITC(小型耳あな型)

- 人工内耳

- 片耳インプラント

- 両耳インプラント

- 骨性補聴器(BAHA)

- MEI

- 補聴器

- 薬剤

- ステロイド

- 抗ウイルス薬

- 血管拡張薬

- その他の薬剤

第6章 市場推計・予測:疾患別、2021年~2032年

- 主要動向

- 感音性難聴

- 伝音性難聴

- 混合性難聴

第7章 市場予測:用途別市場推計・予測:エンドユーザー別、2021年~2032年

- 主要動向

- 病院

- 耳科クリニック

- 外来手術センター

第8章 市場推計・予測:地域別、2021年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東とアフリカ

第9章 企業プロファイル

- Bayer

- Cochlear Ltd

- Demant A/S

- Eargo, Inc

- GlaxoSmithKline

- GN Store Nord A/S

- Pfizer

- Sonova Holding AG

- Starkey

- WS Audiology

The Global Hearing Loss Disease Treatment Market will grow at a 5.4% CAGR between 2024 and 2032, driven by the increasing prevalence of hearing loss, greater awareness, and supportive government initiatives. As the global population ages, the incidence of hearing impairments is rising, creating higher demand for treatment options such as hearing aids, cochlear implants, and medications. Public health campaigns are raising awareness about early diagnosis and available treatments, while governments are implementing policies and funding initiatives to improve accessibility, further expanding the market size in the coming years.

The hearing loss disease treatment industry is divided based on treatment type, condition, end-use, and region.

The devices segment accumulated USD 9.7 billion in 2023, fueled by the widespread adoption of hearing aids, cochlear implants, and bone-anchored hearing systems. These devices offer effective solutions for various degrees of hearing impairment, making them highly sought-after. Continuous technological advancements, including wireless connectivity and sound amplification, enhance the user experience, driving demand. Additionally, increasing accessibility through government support and insurance coverage has further boosted the growth of the devices segment, solidifying its dominance in the market.

The sensorineural hearing loss segment will capture USD 12.5 billion by 2032 due to its high prevalence and the need for effective treatments. Sensorineural hearing loss, often caused by damage to the inner ear or auditory nerves, is more common among aging populations and individuals exposed to loud noise. Advanced therapies such as cochlear implants and hearing aids are widely used to manage this condition, driving market growth. Increasing research into treatment options also supports the segment's leading position.

In 2023, the North America hearing loss disease treatment market recorded USD 5.3 billion and will reach a 4.8% CAGR through 2032, spurred by the region's advanced healthcare infrastructure, high prevalence of hearing loss, and early adoption of innovative treatment technologies. The aging population and widespread awareness campaigns further boost demand for hearing aids, cochlear implants, and other therapies. Additionally, strong government support and favorable reimbursement policies contribute to market growth. The United States, with its robust research initiatives and high healthcare spending, is a significant contributor to this regional dominance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of peripheral artery disease (PAD)

- 3.2.1.2 Rising prevalence of hearing loss

- 3.2.1.3 Technological advancements

- 3.2.1.4 Increased awareness and diagnosis

- 3.2.1.5 Supportive government initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices and treatment

- 3.2.2.2 Lack of knowledge regarding hearing loss

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Future market trends

- 3.6 Regulatory landscape

- 3.7 Product pipeline analysis

- 3.8 Reimbursement scenario

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Gap analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2032 ($ Mn)

- 5.1 Key trends

- 5.2 Devices

- 5.2.1 Hearing aids

- 5.2.1.1 Behind-the-ear (BTE)

- 5.2.1.2 Receiver in the ear/receiver in canal (RITE/RIC)

- 5.2.1.3 Completely-in-the-canal/invisible-in-canal (CIC/IIC)

- 5.2.1.4 In-the-ear (ITE)

- 5.2.1.5 In-the-canal (ITC)

- 5.2.2 Cochlear implants

- 5.2.2.1 Unilateral implants

- 5.2.2.2 Bilateral implants

- 5.2.3 Bone-anchored hearing aids (BAHA)

- 5.2.4 MEI

- 5.2.1 Hearing aids

- 5.3 Drugs

- 5.3.1 Systemic steroids

- 5.3.2 Antiviral medication

- 5.3.3 Vasodilators

- 5.3.4 Other drugs

Chapter 6 Market Estimates and Forecast, By Condition, 2021 - 2032 ($ Mn)

- 6.1 Key trends

- 6.2 Sensorineural hearing loss

- 6.3 Conductive hearing loss

- 6.4 Mixed hearing loss

Chapter 7 Market Estimates and Forecast, By End-Use, 2021 - 2032 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Otology clinics

- 7.4 Ambulatory surgical centers

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2032 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Bayer

- 9.2 Cochlear Ltd

- 9.3 Demant A/S

- 9.4 Eargo, Inc

- 9.5 GlaxoSmithKline

- 9.6 GN Store Nord A/S

- 9.7 Pfizer

- 9.8 Sonova Holding AG

- 9.9 Starkey

- 9.10 WS Audiology