|

市場調査レポート

商品コード

1750544

水管式化学ボイラーの市場機会、成長促進要因、産業動向分析、2025~2034年予測Water Tube Chemical Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 水管式化学ボイラーの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年05月15日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

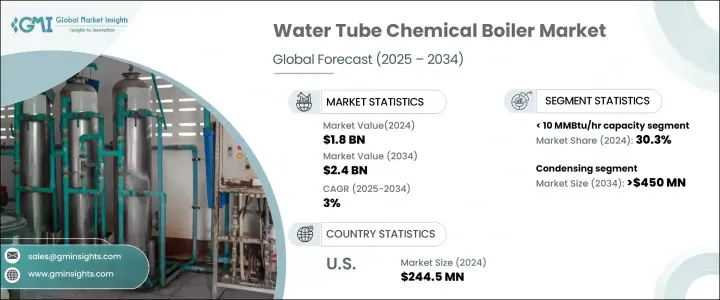

世界の水管式化学ボイラー市場は、2024年に18億米ドルと評価され、CAGR 3%で成長し、2034年には24億米ドルに達すると推定されています。

急速な都市化と工業の発展を目の当たりにしている主要地域は、エネルギー・インフラへの投資の増加と相まって、業界の前向きな見通しをさらに後押しすると思われます。

化学産業向けの水管式化学ボイラーは、水管技術を採用しています。このシステムでは、燃料の燃焼によって外部で加熱された管の中を水が循環します。エネルギー効率を重視する環境規制の強化や、既存のボイラー・ユニットのアップグレードが、市場の成長を後押しします。効率的な暖房技術が重視され、これらのボイラーにスマート・ソリューションを統合することで、製品採用が促進される見込みです。メーカーは、接続性と自動化機能を組み込み、予知保全と運用信頼性をサポートしています。産業界が持続可能性とスマート技術の両方に重点を置く中、水管式化学ボイラーは、将来対応可能なインフラにとって不可欠な存在であり続けると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 18億米ドル |

| 予測金額 | 24億米ドル |

| CAGR | 3% |

10-25 MMBTU/hrボイラー分野は、その拡張性と要求の厳しい産業環境で安定した性能を発揮する能力が主な要因となって、2034年までCAGR 3%で成長すると予想されます。エネルギー効率の高い技術への投資の増加と、デジタル統合への強力な後押しが相まって、市場の拡大を後押ししています。インテリジェントな制御システムを統合することで、ボイラーの運用が再定義され、エネルギーの浪費を抑えながら、リアルタイムのニーズへの適応性が高まっています。現代の性能基準を満たす、持続可能で応答性の高い暖房ソリューションが注目されています。

水管式化学ボイラー市場の非凝縮型セグメントは、温室効果ガス排出量の削減と優れたエネルギー効率により、2034年までCAGR 2.5%で成長すると予想されます。この業界の軌道は、産業プロセスにおけるデジタル化と自動化の採用の高まり、特に高度な制御システムの統合によってプラスの影響を受けています。さらに、化学セクターでは中小企業の開発と拡大が進行中であり、コスト効率重視の傾向が顕著であるため、製品の普及が進むものと思われます。

米国水管式化学ボイラー2024年の市場規模は2億4,450万米ドルで、技術革新、産業ニーズの進化、エネルギー効率目標が原動力となっています。二酸化炭素排出量削減への関心の高まりとともに、よりクリーンなエネルギー・ソリューションへの需要の高まりが、高効率水管ボイラーへのシフトを促しています。これらのシステムは、産業界がより厳しい排出規制を遵守しながら業務の近代化を目指す中で、支持を集めています。産業インフラの継続的な改善と、部門を超えた脱炭素化の推進が、採用の新たな道を開いています。

クリーバー・ブルックス、ミウラ・アメリカ、サーモダイン・ボイラー、レンテック・ボイラー・システムズ、ボッシュ・インダストリーケッセル、バブコック・アンド・ウィルコックス、フォーブス・マーシャル、アルファ・ラバル、コクラン、ブライアン・スチーム、ヴィースマン、クレイトン・インダストリーズ、アリストン・ホールディング、BMグリーンテック、ハースト・ボイラー&ウェルディング、ビクトリー・エナジー・オペレーションズ、バブコック・ワンソン、サーマックスなどの大手メーカーは、市場で確固たる地位を維持するため、複数の戦略を駆使しています。これには、高効率ボイラー・システムを開発するための研究開発能力の拡大、戦略的協力関係の構築、スマート制御技術への投資などが含まれます。また、よりクリーンな燃焼技術を採用し、エンドユーザーの特定の要件を満たすカスタマイズされたソリューションを提供することで、多くの企業が持続可能性に注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的ダッシュボード

- 戦略的取り組み

- 企業の市場シェア分析

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:容量別、2021-2034

- 主要動向

- 10 MMBTU/時未満

- 10~25 MMBTU/時

- 25~50 MMBTU/時

- 50~75 MMBTU/時

- 75~100 MMBTU/時

- 100~175 MMBTU/時

- 175~250 MMBTU/時

- 250 MMBTU/時以上

第6章 市場規模・予測:技術別、2021-2034

- 主要動向

- 凝縮

- 不凝縮

第7章 市場規模・予測:燃料別、2021-2034

- 主要動向

- 天然ガス

- 油

- 石炭

- その他

第8章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- フランス

- 英国

- ポーランド

- イタリア

- スペイン

- オーストリア

- ドイツ

- スウェーデン

- ロシア

- アジア太平洋地域

- 中国

- インド

- フィリピン

- 日本

- 韓国

- オーストラリア

- インドネシア

- 中東・アフリカ

- サウジアラビア

- イラン

- アラブ首長国連邦

- ナイジェリア

- 南アフリカ

- ラテンアメリカ

- ブラジル

- チリ

- アルゼンチン

第9章 企業プロファイル

- Alfa Laval

- Ariston Holding

- Babcock and Wilcox

- Babcock Wanson

- BM GreenTech

- Bosch Industriekessel

- Bryan Steam

- Clayton Industries

- Cleaver-Brooks

- Cochran

- Forbes Marshall

- Hurst Boiler &Welding

- Miura America

- Rentech Boiler Systems

- Thermax

- Thermodyne Boilers

- Victory Energy Operations

- Viessmann

The Global Water Tube Chemical Boiler Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 3% to reach USD 2.4 billion by 2034, bolstered by the increasing adoption of cleaner energy units and significant advancements in boiler systems aimed at reducing emissions and enhancing efficiency. Key regions witnessing rapid urbanization and industrial growth, coupled with rising investments in energy infrastructure, will further support the industry's positive outlook.

Water tube chemical boilers, tailored for the chemical industry, employ water-tube technology. In this setup, water circulates through tubes heated externally by fuel combustion. Heightened environmental regulations, emphasizing energy efficiency, and upgrades to existing boiler units, are set to drive market growth. There's a pronounced emphasis on efficient heating technologies and integrating smart solutions in these boilers is expected to boost product adoption. Manufacturers embedded connectivity and automation features to support predictive maintenance and operational reliability. With industries placing greater emphasis on both sustainability and smart technology, water tube chemical boilers are expected to remain essential to future-ready infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $2.4 Billion |

| CAGR | 3% |

The 10 - 25 MMBTU/hr boiler segment is expected to grow at a CAGR of 3% through 2034, driven largely by its scalability and ability to deliver consistent performance in demanding industrial settings. Increasing investments in energy-efficient technologies, combined with a strong push toward digital integration, are reinforcing the market's expansion. Integrating intelligent control systems has redefined boiler operations, making them more adaptable to real-time needs while reducing energy wastage. The focus is on sustainable and responsive heating solutions that meet modern performance benchmarks.

The non-condensing segment in the water tube chemical boiler market is expected to grow at a CAGR of 2.5% through 2034, due to their reduced GHG emissions and superior energy efficiency. The industry's trajectory is positively influenced by the rising adoption of digitalization and automation in industrial processes, especially with the integration of advanced control systems. Furthermore, the ongoing development and expansion of small and medium-sized enterprises in the chemical sector, coupled with a pronounced emphasis on cost efficiency, are set to amplify product penetration.

United States Water Tube Chemical Boiler Market was valued at USD 244.5 million in 2024, driven by technological innovation, evolving industry needs, and energy efficiency goals. Rising demand for cleaner energy solutions, alongside an increased focus on reducing carbon footprints, is encouraging the shift toward high-efficiency water tube boilers. These systems are gaining traction as industries seek to modernize their operations while adhering to stricter emission regulations. Continued upgrades in industrial infrastructure and the push toward decarbonization across sectors have opened up new avenues for adoption.

To maintain a strong position in the market, leading manufacturers such as Cleaver-Brooks, Miura America, Thermodyne Boilers, Rentech Boiler Systems, Bosch Industriekessel, Babcock and Wilcox, Forbes Marshall, Alfa Laval, Cochran, Bryan Steam, Viessmann, Clayton Industries, Ariston Holding, BM GreenTech, Hurst Boiler & Welding, Victory Energy Operations, Babcock Wanson, and Thermax are leveraging multiple strategies. These include expanding R&D capabilities to develop high-efficiency boiler systems, forming strategic collaborations, and investing in smart control technologies. Many firms are also focusing on sustainability by adopting cleaner combustion technologies and offering customized solutions to meet the specific requirements of end-users.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Strategic initiatives

- 4.4 Company market share analysis, 2024

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 - 2034 (USD Million, MMBTU/hr & Units)

- 5.1 Key trends

- 5.2 < 10 MMBTU/hr

- 5.3 10 - 25 MMBTU/hr

- 5.4 25 - 50 MMBTU/hr

- 5.5 50 - 75 MMBTU/hr

- 5.6 75 - 100 MMBTU/hr

- 5.7 100 - 175 MMBTU/hr

- 5.8 175 - 250 MMBTU/hr

- 5.9 > 250 MMBTU/hr

Chapter 6 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million, MMBTU/hr & Units)

- 6.1 Key trends

- 6.2 Condensing

- 6.3 Non-condensing

Chapter 7 Market Size and Forecast, By Fuel, 2021 - 2034 (USD Million, MMBTU/hr & Units)

- 7.1 Key trends

- 7.2 Natural gas

- 7.3 Oil

- 7.4 Coal

- 7.5 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, MMBTU/hr & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 France

- 8.3.2 UK

- 8.3.3 Poland

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Austria

- 8.3.7 Germany

- 8.3.8 Sweden

- 8.3.9 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Philippines

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.4.6 Australia

- 8.4.7 Indonesia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 Iran

- 8.5.3 UAE

- 8.5.4 Nigeria

- 8.5.5 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Chile

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 Alfa Laval

- 9.2 Ariston Holding

- 9.3 Babcock and Wilcox

- 9.4 Babcock Wanson

- 9.5 BM GreenTech

- 9.6 Bosch Industriekessel

- 9.7 Bryan Steam

- 9.8 Clayton Industries

- 9.9 Cleaver-Brooks

- 9.10 Cochran

- 9.11 Forbes Marshall

- 9.12 Hurst Boiler & Welding

- 9.13 Miura America

- 9.14 Rentech Boiler Systems

- 9.15 Thermax

- 9.16 Thermodyne Boilers

- 9.17 Victory Energy Operations

- 9.18 Viessmann