|

市場調査レポート

商品コード

1716588

データセンターロボティクス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Data Center Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| データセンターロボティクス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月31日

発行: Global Market Insights Inc.

ページ情報: 英文 154 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

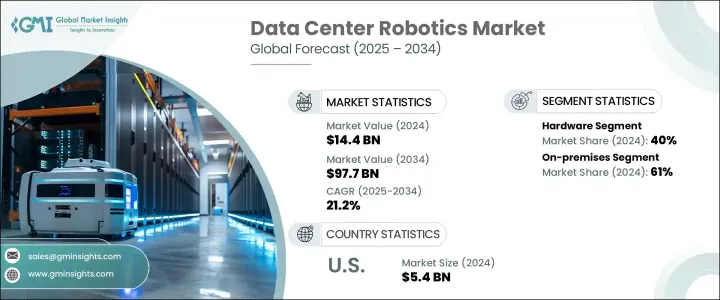

世界のデータセンターロボティクス市場は、2024年に144億米ドルの評価額を記録し、データセンターにおける自動化ニーズの高まりを背景に、2025年から2034年にかけてCAGR 21.2%で成長すると予測されています。

ロボット工学の需要は、生産性の向上、人的労働力の削減、運用効率の強化の必要性によって促進されています。サーバー・メンテナンス、ケーブル管理、環境モニタリングなどの重要な作業を自動化することで、ロボットは人的ミスを最小限に抑え、ダウンタイムを削減し、最小限の監視でよりスムーズで効率的な運用を可能にしています。

データセンターの数と規模が拡大し続ける中、特にハイパースケールやエッジ施設の台頭により、ロボティクスの役割はますます重要になっています。これらの自動化システムは、機器の取り扱い、サーバーの監視、冷却の最適化など、処理する必要のある膨大なタスクを管理するために不可欠です。これらのプロセスを自動化することで、ダウンタイムやアイドル時間を最小限に抑え、データ需要が高まる中で生産性を向上させることができます。より効率的でスケーラブルなロボット・ソリューションに対するニーズの拡大は、データセンターへの依存度の高まりと、その複雑なインフラを維持する必要性を反映しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 144億米ドル |

| 予測金額 | 977億米ドル |

| CAGR | 21.2% |

市場はハードウェア、ソフトウェア、サービスに区分され、現在ハードウェアが市場をリードしており、2024年にはシェアの約40%を占める。このセグメントは今後も力強い成長を続け、CAGR 19.5%以上で拡大すると予想されます。自律移動ロボット(AMR)やロボットアームなどの自動化技術は、徐々に手作業に取って代わりつつあり、より迅速で正確なメンテナンスや機器の取り扱いを可能にしています。

データセンターロボティクスは導入モデルによっても分類され、市場はオンプレミス型とクラウド型に分かれます。2024年時点では、オンプレミス型が市場の61%を占め、大半のシェアを占めています。このセグメントは2034年までCAGR 20.5%以上で成長すると予想されます。オンプレミスの導入は、ロボットシステムの制御性を高め、パフォーマンスを向上させ、外部ネットワークへの依存を減らし、待ち時間を最小化し、サーバー監視や自動化などのタスクへの迅速な対応を可能にするなど、大きな利点があります。

ロボットの種類別では、運用の自動化やシステムの信頼性向上において重要な役割を果たすサービスロボットが優位を占めています。これらのロボットは、データセンターの全体的なパフォーマンスを向上させるため、暖房、冷房、セキュリティパトロールなどの監視作業にますます活用されるようになっています。また、サービス・ロボットは遠隔管理も可能なため、ITスタッフは離れた場所から運用を監視することができ、運用効率をさらに高めることができます。

北米では、米国が同地域の市場シェアの93%を占め、市場をリードしています。米国はハイテクハブとして成長を牽引し続けており、大手企業はサーバーインフラの保守とエネルギー消費の最適化のためにロボティクスに投資しています。ハイパフォーマンス・コンピューティング、AI、クラウド運用の需要が高まる中、データセンターロボティクスは、信頼性の高い効率的な運用を確保するための重要な要素になりつつあります。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 部品サプライヤー

- メーカー

- システムインテグレーター

- テクノロジープロバイダー

- 最終用途

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- 自動化需要の高まり

- データセンター拡張の増加

- クラウドコンピューティングとAIワークロードの増加

- セキュリティ強化のニーズの高まり

- 業界の潜在的リスク&課題

- 高い初期投資コスト

- 既存インフラとの複雑な統合

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- センサー

- アクチュエーター

- モーター

- ビジョンシステム

- AIプロセッサー

- その他

- ソフトウェア

- サービス

第6章 市場推計・予測:ロボット別、2021年~2034年

- 主要動向

- 協働ロボット

- 産業用ロボット

- サービスロボット

- その他

第7章 市場推計・予測:展開モデル別、2021年~2034年

- 主要動向

- オンプレミス

- クラウドベース

第8章 市場推計・予測:企業規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- BFSI

- コロケーション

- エネルギー

- 政府機関

- ヘルスケア

- 製造業

- IT・通信

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- 365 Data Centers

- ABB

- Amazon Web Services

- Boston Dynamics

- China Telecom

- Cisco Systems

- ConnectWise

- Digital Realty

- Equinix

- Fanuc

- Hewlett Packard Enterprise Development

- Huawei Technologies

- IBM

- Microsoft Corporation

- NTT Communications

- Rockwell Automation

- Siemens

- SoftBank Robotics

- Verizon

The Global Data Center Robotics Market, with a valuation of USD 14.4 billion in 2024, is expected to grow at a CAGR of 21.2% from 2025 to 2034, driven by the increasing need for automation in data centers. The demand for robotics is being fueled by the necessity for improved productivity, reduced human labor, and enhanced operational efficiency. By automating essential tasks such as server maintenance, cable management, and environmental monitoring, robotics are minimizing human errors and reducing downtime, enabling smoother, more efficient operations with minimal supervision.

As data centers continue to grow in number and scale, particularly with the rise of hyperscale and edge facilities, the role of robotics becomes increasingly vital. These automated systems are essential for managing the vast array of tasks that need to be handled, including equipment handling, server supervision, and cooling optimization. The automation of these processes helps to minimize downtime and idle time, improving productivity in the face of rising data demands. This expanding need for more efficient and scalable robotic solutions reflects the growing reliance on data centers and the need to maintain their complex infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.4 Billion |

| Forecast Value | $97.7 Billion |

| CAGR | 21.2% |

The market is segmented into hardware, software, and services, with hardware currently leading the market, accounting for approximately 40% of the share in 2024. This segment is expected to continue its strong growth, expanding at a CAGR of over 19.5%. Automation technologies such as autonomous mobile robots (AMRs) and robotic arms are gradually replacing manual labor, enabling faster, more accurate maintenance and equipment handling.

Data center robotics are also categorized based on deployment model, with the market divided between on-premises and cloud-based models. In 2024, the on-premises segment holds the majority share, representing 61% of the market. This segment is expected to grow at a CAGR of more than 20.5% through 2034. On-premises deployment offers significant advantages, including greater control over robotic systems, which helps improve performance and reduces reliance on external networks, minimizing latency and enabling quicker responses for tasks like server monitoring and automation.

Within the robot type segment, service robots are poised to dominate, thanks to their pivotal role in automating operations and improving system reliability. These robots are increasingly utilized for monitoring tasks such as heating, cooling, and security patrols, enhancing the overall performance of data centers. Service robots also provide remote management, allowing IT staff to oversee operations from a distance, which further boosts operational efficiency.

In North America, the U.S. leads the market with a substantial 93% market share in the region. The U.S. continues to drive growth through its tech hubs, with major corporations investing in robotics to maintain server infrastructure and optimize energy consumption. As demand for high-performance computing, AI, and cloud operations grows, data center robotics are becoming a critical part of ensuring reliable, efficient operations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component suppliers

- 3.2.2 Manufacturers

- 3.2.3 System integrators

- 3.2.4 Technology providers

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising demand for automation

- 3.8.1.2 Increasing data center expansion

- 3.8.1.3 Growth in cloud computing and AI workloads

- 3.8.1.4 Growing need for enhanced security

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High initial investment costs

- 3.8.2.2 Complex integration with existing infrastructure

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensor

- 5.2.2 Actuator

- 5.2.3 Motors

- 5.2.4 Vision systems

- 5.2.5 AI processors

- 5.2.6 Others

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Robot, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Collaborative robots

- 6.3 Industrial robots

- 6.4 Service robots

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 On-premises

- 7.3 Cloud-based

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 Colocation

- 9.4 Energy

- 9.5 Government

- 9.6 Healthcare

- 9.7 Manufacturing

- 9.8 IT & telecom

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 365 Data Centers

- 11.2 ABB

- 11.3 Amazon Web Services

- 11.4 Boston Dynamics

- 11.5 China Telecom

- 11.6 Cisco Systems

- 11.7 ConnectWise

- 11.8 Digital Realty

- 11.9 Equinix

- 11.10 Fanuc

- 11.11 Google

- 11.12 Hewlett Packard Enterprise Development

- 11.13 Huawei Technologies

- 11.14 IBM

- 11.15 Microsoft Corporation

- 11.16 NTT Communications

- 11.17 Rockwell Automation

- 11.18 Siemens

- 11.19 SoftBank Robotics

- 11.20 Verizon