|

|

市場調査レポート

商品コード

1913290

血友病治療市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Hemophilia Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 血友病治療市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月24日

発行: Global Market Insights Inc.

ページ情報: 英文 163 Pages

納期: 2~3営業日

|

概要

世界の血友病治療市場は、2025年に152億米ドルと評価され、2035年までにCAGR 6.1%で成長し、272億米ドルに達すると予測されています。

本市場は、血友病AおよびBの罹患率上昇、予防的治療アプローチの広範な受容、先進的治療イノベーションの導入加速により拡大を続けております。血友病治療は、凝固因子の欠乏によって引き起こされる出血性疾患の管理に焦点を当て、安定した凝固機能の維持と出血リスクの最小化を図ります。また、事後対応型治療よりも予防を優先する長期疾患管理モデルへの移行も市場成長を牽引しています。治療の持続性、投与精度の向上、患者利便性の継続的な改善により、治療遵守率と治療成果が向上しています。日常生活の質の向上と長期合併症の軽減への関心の高まりが、先進国・新興国を問わずヘルスケアシステム全体での需要をさらに強化しています。加えて、治療負担を軽減しつつ持続的な治療効果を提供する革新技術が、治療法の選好を再構築し、世界の市場成長の勢いを後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 152億米ドル |

| 予測金額 | 272億米ドル |

| CAGR | 6.1% |

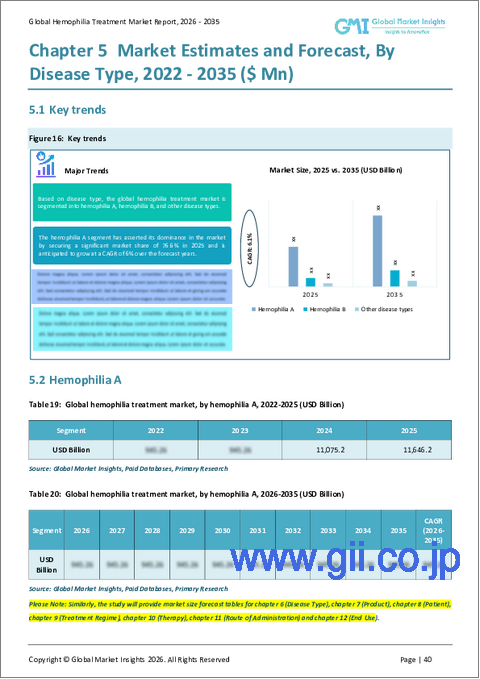

血友病Aセグメントは2025年に76.6%のシェアを占め、2034年までCAGR6%で成長すると予測されています。このセグメントは、世界的に有病率が著しく高く、凝固因子欠乏症に対処する先進的な治療ソリューションに対する需要が大幅に生じていることから、主導的な地位を維持しています。大規模な患者基盤は、確立された治療法と新興治療法の強力な普及を引き続き支え、このセグメントにおける持続的な収益成長に寄与しています。

組換え凝固因子製剤セグメントは2025年に71億米ドルの市場規模を記録し、2035年までCAGR6.2%で成長すると予測されます。これらの治療法は、安定した供給信頼性、強化された安全基準、治療成果の向上により、広く支持され続けています。製品の持続期間延長と投与頻度低減に焦点を当てた継続的な技術革新が、その強固な市場地位をさらに強化しています。

北米の血友病治療市場は、先進的なヘルスケアインフラ、高い診断率、新規治療法の早期導入、強力な償還制度に支えられ、2025年に44.2%のシェアを占めました。同地域はまた、広範な臨床研究活動と確立された患者支援エコシステムの恩恵も受けています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 血友病および出血性疾患の有病率増加

- 予防的・個別化治療への移行

- 非因子療法および遺伝子治療の進展

- 新興市場におけるアクセスと診断の改善

- 業界の潜在的リスク&課題

- 高コストと手頃な価格への障壁

- 複雑な規制および製造要件

- 市場機会

- 遺伝子治療および根治的アプローチの拡大

- デジタルヘルス統合と在宅ケア

- 促進要因

- 成長可能性分析

- 技術動向

- 現在の技術動向

- 新興技術

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 将来の市場動向

- パイプライン分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携および協力関係

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:疾患タイプ別、2022-2035

- 血友病A

- 重症

- 中等度

- 軽度

- 血友病B

- 重症

- 中等度

- 軽度

- その他の疾患タイプ

第6章 市場推計・予測:製品別、2022-2035

- 組換え凝固因子製剤

- 第VIII因子

- 第IX因子

- 血漿由来凝固因子製剤

- 第VIII因子

- 第IX因子

- 半減期延長製品

- 第VIII因子

- 第IX因子

- デスモプレシン

- 抗線溶剤

- 遺伝子治療製品

- その他の製品

第7章 市場推計・予測患者別、2022-2035

- 小児

- 0~4歳

- 5~13歳

- 14~18歳

- 成人用

- 19~44歳

- 45歳以上

第8章 市場推計・予測:治療レジメン別、2022-2035

- 予防投与

- オンデマンド

第9章 市場推計・予測:治療法別、2022-2035

- 因子補充療法

- 非因子補充療法

第10章 市場推計・予測:投与経路別、2022-2035

- 注射剤

- 点鼻薬

- 経口

第11章 市場推計・予測:最終用途別、2022-2035

- 病院

- 診療所

- 血友病治療センター

- その他のエンドユーザー

第12章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第13章 企業プロファイル

- Bayer Healthcare

- Biogen

- BioMarin Pharmaceutical

- Biotest

- CSL Behring

- Ferring

- Genentech

- Kedrion

- Novo Nordisk

- Octapharma

- Pfizer

- Sanofi

- Swedish Orphan Biovitrum

- Takeda Pharmaceutical