|

市場調査レポート

商品コード

1716721

バタフライバルブ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Butterfly Valve Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| バタフライバルブ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月21日

発行: Global Market Insights Inc.

ページ情報: 英文 225 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

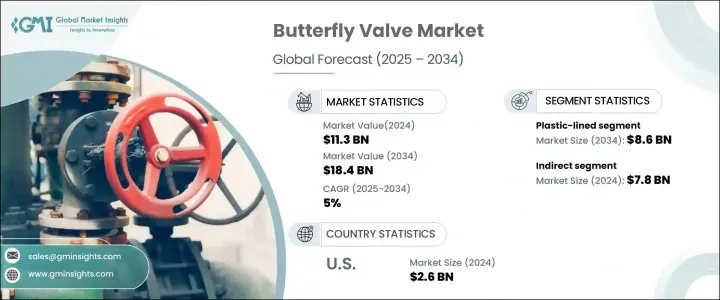

バタフライバルブの世界市場は、2024年に113億米ドルを生み出し、2025年から2034年にかけてCAGR 5%で成長すると予測されています。

この成長の主な要因は、石油・ガス、発電、水処理などの産業における産業オートメーションの急速な進歩です。産業界が業務効率の向上と人的介入の最小化をますます重視するようになるにつれ、自動化され遠隔操作されるバルブの需要は増加の一途をたどっています。バタフライバルブは、その軽量設計、費用対効果、迅速な操作で知られ、スマートな流量制御システムに適した選択肢となりつつあります。その汎用性と信頼性により、様々な産業用途に不可欠な存在となり、スムーズで効率的なプロセスを実現しています。

上下水道管理インフラの改善に対する世界の注目が高まっていることも、バタフライバルブの需要を促進している大きな要因です。特に開発途上地域では、水消費に対する懸念の高まりや廃水管理に関する政府の厳しい規制に対応するため、水処理プラントの建設が急増しています。産業界や自治体が高度な水管理システムに投資する中、バタフライバルブは大量の水を効率的に処理し、最小限のメンテナンスで済むことから、理想的なソリューションとして浮上しています。バタフライバルブは耐久性に優れ、費用対効果に優れているため、大規模な用途に適しており、水処理施設の長期的な運用効率を保証します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 113億米ドル |

| 予測金額 | 184億米ドル |

| CAGR | 5% |

バタフライバルブ市場は、ライニングタイプ別にプラスチックライニング、金属ライニング、ゴムライニングに区分されます。プラスチックライニングのセグメントは、腐食や化学薬品に対する優れた耐性を原動力に、2024年に51億米ドルを生み出しました。これらのバルブは、耐久性、低メンテナンス要件、攻撃的な流体を扱う際の優れた性能により、化学処理や医薬品などの産業で非常に好まれています。機器の寿命を延ばすために耐腐食性のソリューションを採用する産業が増える中、プラスチックライニングのバタフライバルブは引き続き強い需要を目の当たりにしています。

販売チャネルの面では、市場は直接販売と間接販売に分けられます。間接販売分野は2024年に78億米ドルとなり、2034年までCAGR 4.8%で成長すると予想されています。直接販売チャネルの成長にもかかわらず、多くのメーカーは製品の販売促進や流通を代理店、卸売業者、小売業者などの間接的なネットワークに依存しています。特に、信頼できる関係や確立されたサプライチェーンが販売を促進し、製品を確実に入手するために不可欠な産業分野では、こうした仲介業者は市場参入を拡大する上で重要な役割を果たしています。

米国のバタフライバルブ市場は2024年に26億米ドルに達し、2025年から2034年にかけてCAGR 5.5%で成長すると予測されています。特に石油・ガス、水管理、発電などの産業における強固なインフラと高度な製造能力により、米国は北米市場の主要プレーヤーとして位置づけられています。さらに、厳しい環境規制と工業プロセスにおける自動化レベルの向上が、同地域における高度なバタフライバルブの需要を引き続き牽引しています。米国の産業界が規制遵守と業務効率を満たすために革新的な技術を導入していることから、バタフライバルブ市場は今後数年間で安定した成長を遂げると思われます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- 小売業者

- 影響要因

- 促進要因

- 産業オートメーションへの需要の高まり

- 上下水道処理施設の拡大

- 石油・ガスおよび化学処理への投資の増加

- 業界の潜在的リスク&課題

- 原材料価格の変動

- 代替流量制御技術の利用可能性

- 促進要因

- 成長可能性分析

- 原材料分析

- 規制状況

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:ライニングタイプ別、2021年~2034年

- 主要動向

- ゴムライニング

- プラスチックライニング

- 金属ライニング

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 炭素鋼

- ステンレス鋼

- 鉄

- その他

第7章 市場推計・予測:取付タイプ別、2021年~2034年

- 主要動向

- ウエハー

- セミラグ

- ラグ

- ダブルフランジ

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 上下水道

- 石油・ガス

- エネルギー・電力

- 医薬品

- 化学

- その他

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接

- 間接流通

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- UAE

- 南アフリカ

第11章 企業プロファイル

- Alfa Laval

- AVK Group

- Bray International

- Crane

- Curtiss-Wright

- DeZURIK

- Emerson Electric

- Flowserve

- Grundfos

- Honeywell International

- Neles

- SPX FLOW

- Velan

- Weir Group

- Xylem

The Global Butterfly Valve Market generated USD 11.3 billion in 2024 and is projected to grow at a CAGR of 5% between 2025 and 2034. This growth is primarily driven by rapid advancements in industrial automation across industries such as oil & gas, power generation, and water treatment. As industries increasingly emphasize enhancing operational efficiency and minimizing human intervention, the demand for automated and remotely controlled valves continues to rise. Butterfly valves, known for their lightweight design, cost-effectiveness, and quick operation, are becoming the preferred choice for smart flow control systems. Their versatility and reliability make them indispensable in various industrial applications, ensuring smooth and efficient processes.

The increasing global focus on improving water and wastewater management infrastructure is another significant factor fueling the demand for butterfly valves. Developing regions, in particular, are experiencing a surge in the construction of water treatment plants to address growing concerns over water consumption and stringent government regulations on wastewater management. As industries and municipalities invest in advanced water management systems, butterfly valves emerge as the ideal solution due to their ability to handle large water volumes efficiently and with minimal maintenance. Their durability and cost-effectiveness make them a reliable choice for large-scale applications, ensuring long-term operational efficiency in water treatment facilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.3 Billion |

| Forecast Value | $18.4 Billion |

| CAGR | 5% |

The butterfly valve market is segmented by lining type into plastic-lined, metal-lined, and rubber-lined valves. The plastic-lined segment generated USD 5.1 billion in 2024, driven by its superior resistance to corrosion and chemicals. These valves are highly preferred in industries such as chemical processing and pharmaceuticals due to their durability, low maintenance requirements, and excellent performance in handling aggressive fluids. As industries increasingly adopt corrosion-resistant solutions to prolong the lifespan of their equipment, plastic-lined butterfly valves continue to witness strong demand.

In terms of distribution channels, the market is divided into direct and indirect sales. The indirect segment, valued at USD 7.8 billion in 2024, is expected to grow at a CAGR of 4.8% through 2034. Despite the growth of direct distribution channels, many manufacturers still rely on indirect networks, including agents, wholesalers, and retailers, to promote and distribute their products. These intermediaries play a critical role in expanding market reach, particularly in industrial sectors where trusted relationships and established supply chains are essential for driving sales and ensuring product availability.

The U.S. butterfly valve market reached USD 2.6 billion in 2024 and is projected to grow at a CAGR of 5.5% between 2025 and 2034. The country's robust infrastructure and advanced manufacturing capabilities, especially in industries such as oil and gas, water management, and power generation, position the U.S. as a key player in the North American market. Additionally, stringent environmental regulations and increasing levels of automation in industrial processes continue to drive the demand for advanced butterfly valves in the region. As industries in the U.S. adopt innovative technologies to meet regulatory compliance and operational efficiency, the butterfly valve market is poised for steady growth in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for industrial automation

- 3.2.1.2 Expansion of water and wastewater treatment facilities

- 3.2.1.3 Rising investments in oil & gas and chemical processing

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Fluctuating raw material prices

- 3.2.2.2 Availability of alternative flow control technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Raw Material analysis

- 3.5 Regulatory landscape

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Lining Type, 2021-2034 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Rubber lined

- 5.3 Plastic lined

- 5.4 Metal lined

Chapter 6 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Carbon steel

- 6.3 Stainless steel

- 6.4 Iron

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Mounting Type, 2021-2034 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Wafer

- 7.3 Semi lug

- 7.4 Lug

- 7.5 Double flanges

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Water and wastewater

- 8.3 Oil and gas

- 8.4 Energy and power

- 8.5 Pharmaceuticals

- 8.6 Chemicals

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Million Units)

- 9.1 Key Trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021 – 2034, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 Alfa Laval

- 11.2 AVK Group

- 11.3 Bray International

- 11.4 Crane

- 11.5 Curtiss-Wright

- 11.6 DeZURIK

- 11.7 Emerson Electric

- 11.8 Flowserve

- 11.9 Grundfos

- 11.10 Honeywell International

- 11.11 Neles

- 11.12 SPX FLOW

- 11.13 Velan

- 11.14 Weir Group

- 11.15 Xylem