|

市場調査レポート

商品コード

1858973

床暖房の市場機会、成長促進要因、産業動向分析、2025~2034年予測Underfloor Heating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 床暖房の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年10月08日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

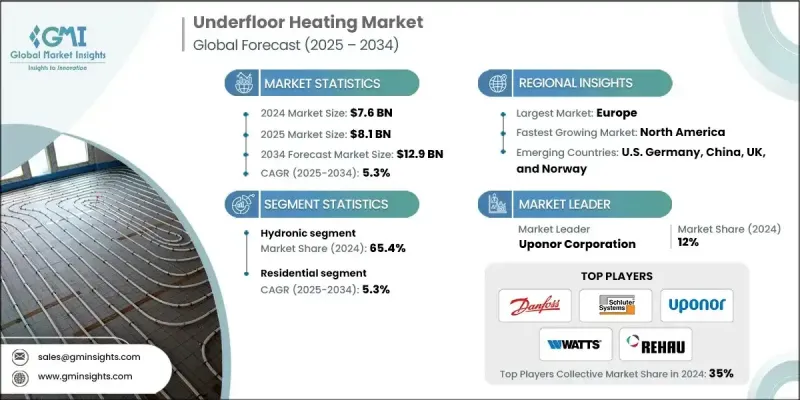

床暖房の世界市場規模は、2024年に76億米ドルとなり、CAGR 5.3%で成長し、2034年には129億米ドルに達すると予測されています。

信頼性が高くエネルギー効率の高い室内暖房システムに対する需要の高まりと相まって、二酸化炭素排出量の削減が重視されるようになり、さまざまな地域で普及が進んでいます。消費者も産業界も同様に、快適性と環境基準への適合の両方を提供する持続可能な代替暖房にシフトしています。床暖房ソリューションは、エネルギー効率を改善し、再生可能エネルギー源とシームレスに統合することで、化石燃料への依存を低減します。寒冷化やエネルギー規制の強化に直面する中、電気輻射式や水熱式などの高度な暖房システムへの需要が高まっています。これらのシステムは、省エネ目標に貢献しながら、均一な暖かさを提供します。均一な温度制御と運用コスト削減の動向とともに、住宅・商業部門全体で環境に優しい技術を求める動きが広がっており、床暖房製品の採用が加速しています。都市化の進展、インフラの近代化、スマートで低メンテナンスの暖房オプションの魅力の高まりは、世界各地域で引き続き市場の見通しを高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 76億米ドル |

| 予測金額 | 129億米ドル |

| CAGR | 5.3% |

ハイドロニック床暖房分野は、商業用および住宅用アプリケーションにおける高度で効率的な暖房ソリューションに対する需要の高まりにより、2024年に50億米ドルを創出しました。グリーンビルディングの拡大や持続可能な建設プロジェクトの増加が、製品需要の押し上げに重要な役割を果たしています。特に発展途上地域における継続的な人口増加とスマートシティの台頭が相まって、長期的な業界拡大が見込まれています。

住宅分野は2024年に60.4%のシェアを占め、2034年までのCAGRは5.3%で成長します。この成長の主因は、最新の住宅技術や省エネソリューションへの消費者シフトの高まりです。長期的な節約、メンテナンスコストの削減、快適性の向上に対する意識の高まりが、住宅所有者の床暖房システムの採用を加速させています。安定した暖房と室内空気の質の向上が魅力で、新築とリフォームの両方で住宅への採用がさらに進んでいます。

米国の床暖房市場は77.9%のシェアを占め、2024年には15億米ドルを生み出します。北米は、改築活動の増加、建築基準法の進化、エネルギー効率の高い生活水準への注目の高まりにより、強力な市場地位を維持すると予想されます。人口密度の上昇やエネルギー指令の強化に加え、厳しい冬の条件が床暖房技術の採用に拍車をかけています。インフラの近代化や生活水準の向上と相まって、高度な快適性ソリューションへの嗜好が高まっていることが、米国市場の拡大を支えています。

床暖房市場の競合情勢を形成している主要企業は、nVent、Uponor Corporation、Warmboard, Inc.、Warmup、Schluter Systems、REHAU、ThermaRay、Watts、HEATCOM CORPORATION、Gaia Climate Solutions、Amuheat、Danfoss、Polypipe、Robert Bosch、H2O Heating、ETHERMA Elektrowarme GmbH、Resideo Technologies、Hunt Commercial、Thermogroup、Hemstedt、Thermo-Floor UK Limited、Therma-HEXX Corporationなどです。床暖房世界市場におけるプレゼンスを強化するため、大手企業は技術革新、持続可能性、地域拡大に注力しています。多くの企業が研究開発に投資し、システム効率の向上、スマート暖房制御の導入、再生可能電源と互換性のある低エネルギーソリューションの開発に取り組んでいます。建設会社や不動産開発業者とのパートナーシップは、新しい住宅や商業プロジェクトでの早期採用を後押ししています。また、各社は製品ラインを拡大し、古い建物にも対応するモジュール式や改修に適したソリューションを提供しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 原材料の入手可能性と調達分析

- バリューチェーンに影響を与える主な要因

- ディスラプション

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

- 床暖房システムのコスト構造分析

- 新たな機会と動向

- IoT技術によるデジタルトランスフォーメーション

- 新興市場への普及

- 投資分析と将来展望

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 戦略的取り組み

- 主なパートナーシップ

- 主なM&A活動

- 製品イノベーションと発売

- 市場拡大戦略

- 競合ベンチマーキング

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:技術別、2021-2034

- 主要動向

- 電気式

- ハイドロニック

第6章 市場規模・予測施設別、2021-2034

- 主要動向

- 新築ビル

- レトロフィット

第7章 市場規模・予測:用途別、2021-2034

- 主要動向

- 住宅用

- シングルファミリー

- 集合住宅

- 商業用

- 教育

- ヘルスケア

- 小売り

- 物流・運輸

- オフィス

- ホスピタリティ

- その他

- 産業用

第8章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- フィンランド

- ノルウェー

- スウェーデン

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- メキシコ

第9章 企業プロファイル

- Amuheat

- Danfoss

- ETHERMA Elektrowarme GmbH

- Gaia Climate Solutions

- H2O Heating

- HEATCOM CORPORATION

- Hemstedt

- Hunt Commercial

- nVent

- Polypipe

- REHAU

- Resideo Technologies

- Robert Bosch

- Schluter Systems

- Therma-HEXX Corporation

- ThermaRay

- Thermo-Floor UK Limited

- Thermogroup

- Uponor Corporation

- Warmboard, Inc.

- Warmup

- Watts