|

市場調査レポート

商品コード

1801891

スマート電気メーターの市場機会、成長促進要因、産業動向分析、2025~2034年予測Smart Electric Meter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| スマート電気メーターの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年08月11日

発行: Global Market Insights Inc.

ページ情報: 英文 145 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

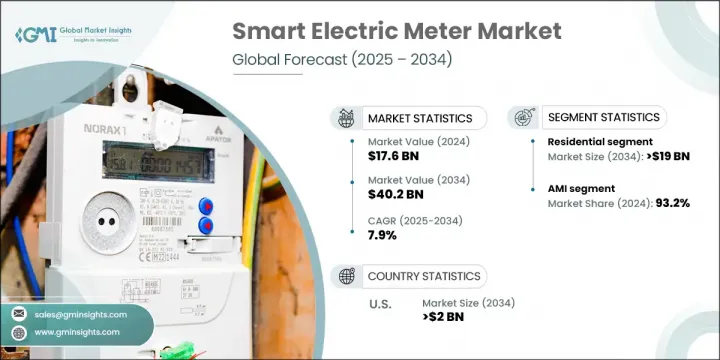

世界のスマート電気メーター市場は、2024年には176億米ドルとなり、CAGR 7.9%で成長し、2034年には402億米ドルに達すると推定されています。

この成長は、先進グリッド技術への世界の投資の増加によって大きく後押しされています。各国が時代遅れの電力インフラの近代化に取り組み、停電を減らし、再生可能エネルギーの統合をサポートする中で、スマートメーターはこうした最新システムの中核的なコンポーネントになりつつあります。これらのメーターは、電力会社にきめ細かな消費データを提供し、グリッドの効率を最適化し、サービス上の問題をリアルタイムで特定し、全体的な運営費を削減するのに役立ちます。

IoT、無線技術、データ分析における絶え間ない技術革新は、スマートメーターの価格と性能を向上させています。消費者は現在、エネルギー使用に関するリアルタイム洞察から恩恵を受け、より良い需要管理、エネルギーコストの削減、グリッド・バランシングのサポート強化につながっています。スマートメーターは、ホームオートメーションやデマンドレスポンスプラットフォームとともに採用され、現代のエネルギーエコシステムにおける役割をさらに高めています。二酸化炭素排出量の削減が急務となる中、これらの機器は効率的な配電を可能にし、よりクリーンなエネルギーを促進する上で重要な役割を果たすようになっています。財政的インセンティブ、施策的義務付け、電力会社主導の展開により、世界各地域で導入が加速し続けており、市場全体の情勢を強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 176億米ドル |

| 予測金額 | 402億米ドル |

| CAGR | 7.9% |

住宅部門は、個人住宅や集合住宅におけるスマートメーター需要の高まりにより、2034年までに190億米ドルに達します。エネルギー効率、太陽エネルギー統合、正確な請求への重点の高まりが、このセグメント拡大の主要因です。太陽光発電の設置が特に住宅スペースで増加するにつれ、スマートメーターはエネルギーモニタリングの合理化に役立ち、ユーザーはデータに基づいた消費決定を行えるようになります。電力会社も、顧客とのコミュニケーションを強化し、近隣地域全体で高まる持続可能性の目標に対応するため、スマートメーターの設置を増やしています。

技術的には、市場は高度計測インフラ(AMI)と自動検針(AMR)に分かれます。AMIセグメントは2024年に93.2%のシェアを占め、双方向通信、リアルタイムデータ伝送、公益事業管理システムとのシームレスな統合を提供できることから、引き続きリードしています。AMRが効率を改善し人的ミスを減らす一方で、AMIはエネルギーネットワークの完全なデジタル変革を可能にし、エネルギーフローの制御を強化します。

米国スマート電気メーター市場は2034年までに20億米ドルに達すると予想され、増加する再生可能エネルギーの投入を管理するために最新のグリッドシステムを必要とする、進化する規制によって支えられています。世界で最も洗練された経済諸国の一つである米国は、世界貿易において主要な役割を果たしており、このことはこれらのメーターのようなスマートグリッド技術の開発と展開にも影響を与えています。特に電気自動車の普及や再生可能エネルギーの統合が進む州では、安定した電力供給を求める動きが、より広範なメーター設置を後押ししています。

世界のスマート電気メーター市場を積極的に形成している主要企業には、Siemens、ランディス+ギア、Schneider Electric、Honeywellインターナショナル、イトロンなどがあります。スマート電気メーター産業の主要企業は、公益事業者との提携やスマートグリッドプロジェクトを通じて、地理的な範囲の拡大に注力しています。企業は、競合を維持するためにAI、エッジコンピューティング、IoT機能を統合し、メーターの精度、接続性、機能性を高めるための研究開発に多額の投資を行っています。また、地域のコンプライアンスやグリッドインフラとの相互運用性のためのカスタマイズも優先事項の中核となっています。イトロンやSchneider Electricのような参入企業は、リアルタイムのモニタリングとデジタルグリッド管理の需要に応えるため、AMIベースソリューションを優先しています。戦略的買収、政府機関との長期契約、再生可能エネルギー展開への参加は、市場参入企業の地位をさらに強化しています。さらに、企業は公益事業者と最終消費者の信頼を築くため、サイバーセキュリティとデータプライバシーを重視しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- 規制情勢

- 輸出入貿易分析

- 地域別価格動向分析(米ドル/単位)

- 産業への影響要因

- 促進要因

- 産業の潜在的リスク・課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

- 新たな機会と動向

- デジタル化とIoTの統合

- 新興市場への浸透

- 投資分析と将来展望

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

- 戦略的取り組み

- 競合ベンチマーキングの描写

- 戦略ダッシュボード

- イノベーションと技術の情勢

第5章 市場規模・予測:用途別、2021~2034年

- 主要動向

- 住宅

- 一戸建て

- 複数世帯住宅

- 商用

- 教育

- ヘルスケア

- 小売

- 物流・輸送

- オフィス

- ホスピタリティ

- その他

- 公益事業

第6章 市場規模・予測:技術別、2021~2034年

- 主要動向

- AMI

- RF

- PLC

- セルラー

- AMR

第7章 市場規模・予測:相別、2021~2034年

- 主要動向

- 単相

- 三相

第8章 市場規模・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スウェーデン

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

第9章 企業プロファイル

- ABB

- Aclara Technologies LLC

- Advanced Electronics Company(AEC)

- Apator SA

- Circutor

- Cisco Systems, Inc.

- CyanConnode

- Enel Spa.

- General Electric

- Honeywell International Inc.

- Iskraemeco Group

- Itron Inc.

- Kamstrup

- Landis+Gyr

- Larsen & Toubro Limited

- Mitsubishi Electric Corporation

- Osaki Electric Co., Ltd.

- Schneider Electric

- Sensus

- Siemens

- Toshiba

- Trinity Energy Systems

The Global Smart Electric Meter Market was valued at USD 17.6 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 40.2 billion by 2034. This growth is largely propelled by increasing global investments in advanced grid technologies. As nations work to modernize outdated power infrastructure, reduce blackouts, and support renewable integration, smart meters are becoming a core component of these modern systems. These meters provide utilities with granular consumption data that helps optimize grid efficiency, identify service issues in real time, and lower overall operating expenses.

Continuous innovation in IoT, wireless technology, and data analytics is improving the affordability and performance of smart meters. Consumers now benefit from real-time insights into energy usage, leading to better demand management, reduced energy costs, and greater support for grid balancing. Smart meters are also being adopted alongside home automation and demand-response platforms, further increasing their role in modern energy ecosystems. As the urgency to cut carbon emissions grows, these devices are becoming instrumental in enabling efficient power distribution and promoting cleaner energy. Financial incentives, policy mandates, and utility-driven rollouts continue to accelerate adoption across global regions, reinforcing the overall smart electric meter market landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.6 Billion |

| Forecast Value | $40.2 Billion |

| CAGR | 7.9% |

The residential sector will reach USD 19 billion by 2034, driven by the rising demand for smart meters in individual homes and multifamily dwellings. Increasing emphasis on energy efficiency, solar energy integration, and accurate billing are major factors behind this segment's expansion. As solar PV installations rise, particularly in residential spaces, smart meters help streamline energy monitoring and allow users to make data-driven consumption decisions. Utilities are also increasingly installing smart meters to enhance communication with customers and meet growing sustainability goals across neighborhoods.

Technologically, the market is split into advanced metering infrastructure (AMI) and automatic meter reading (AMR). The AMI segment held a 93.2% share in 2024 and continues to lead due to its ability to provide two-way communication, real-time data transmission, and seamless integration with utility management systems. While AMR improves efficiency and reduces human error, AMI enables full digital transformation of energy networks and enhances control over energy flows.

United States Smart Electric Meter Market will reach USD 2 billion by 2034, supported by evolving regulations that require modern grid systems to manage growing renewable energy inputs. With one of the world's most sophisticated economies, the US plays a major role in global trade, which also influences the development and deployment of smart grid technologies like these meters. The push for stable power delivery, especially in states with rising electric vehicle adoption and renewable integration, is driving broader meter installations.

Key players actively shaping the Global Smart Electric Meter Market include Siemens, Landis + Gyr, Schneider Electric, Honeywell International, and Itron. Leading companies in the smart electric meter industry are focusing on expanding their geographic reach through partnerships with utility providers and smart grid projects. Firms are investing heavily in R&D to enhance the accuracy, connectivity, and functionality of their meters, integrating AI, edge computing, and IoT capabilities to stay competitive. Customization for regional compliance and interoperability with grid infrastructure is also a core priority. Players like Itron and Schneider Electric are prioritizing AMI-based solutions to cater to demand for real-time monitoring and digital grid management. Strategic acquisitions, long-term contracts with government bodies, and participation in renewable energy rollouts are further strengthening market positions. Additionally, businesses are emphasizing cybersecurity and data privacy to build trust among utilities and end consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Import/Export trade analysis

- 3.4 Price trend analysis, by region (USD/Unit)

- 3.5 Industry impact forces

- 3.5.1 Growth drivers

- 3.5.2 Industry pitfalls & challenges

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.8.6 Environmental factors

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & '000 Units)

- 5.1 Key trends

- 5.2 Residential

- 5.2.1 Single family

- 5.2.2 Multi family

- 5.3 Commercial

- 5.3.1 Education

- 5.3.2 Healthcare

- 5.3.3 Retail

- 5.3.4 Logistics & transportation

- 5.3.5 Offices

- 5.3.6 Hospitality

- 5.3.7 Others

- 5.3.8 Utility

Chapter 6 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million & '000 Units)

- 6.1 Key trends

- 6.2 AMI

- 6.2.1 RF

- 6.2.2 PLC

- 6.2.3 Cellular

- 6.3 AMR

Chapter 7 Market Size and Forecast, By Phase, 2021 - 2034 (USD Million & '000 Units)

- 7.1 Key trends

- 7.2 Single

- 7.3 Three

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & '000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Sweden

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 South Africa

- 8.5.4 Egypt

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Mexico

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Aclara Technologies LLC

- 9.3 Advanced Electronics Company (AEC)

- 9.4 Apator SA

- 9.5 Circutor

- 9.6 Cisco Systems, Inc.

- 9.7 CyanConnode

- 9.8 Enel Spa.

- 9.9 General Electric

- 9.10 Honeywell International Inc.

- 9.11 Iskraemeco Group

- 9.12 Itron Inc.

- 9.13 Kamstrup

- 9.14 Landis + Gyr

- 9.15 Larsen & Toubro Limited

- 9.16 Mitsubishi Electric Corporation

- 9.17 Osaki Electric Co., Ltd.

- 9.18 Schneider Electric

- 9.19 Sensus

- 9.20 Siemens

- 9.21 Toshiba

- 9.22 Trinity Energy Systems