スマート電力メーター:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Smart Electricity Meter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1640689

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

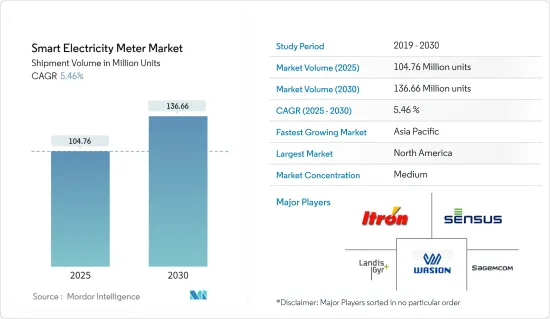

スマート電力メーターの市場規模は、出荷台数ベースで2025年の1億476万台から2030年には1億3,666万台に拡大し、予測期間(2025~2030年)のCAGRは5.46%と予測されます。

スマートメーターの導入により、ホーム・エネルギー管理システム(HEMS)やビル・エネルギー管理システム(BEMS)の導入が可能になり、個々の家庭やビル全体の電力使用量が可視化されます。

主なハイライト

- 経済活動の活発化によりエネルギー消費量が増加し、世界の電力網が限界に達しているため、世界的にエネルギー効率がますます重視されるようになっています。BPによると、2021年の世界の発電量は28,466テラワット時でした。

- デジタル化によってエネルギー効率化対策はさらに加速し、近代化しています。そのため、供給を動的に最適化し、太陽光発電などの再生可能エネルギーによる大量の電力供給を促進できるスマートグリッドの導入が世界的に増加しています。

- 最近のCOVID-19の世界の流行と全国的な封鎖は、スマートメーターの世界の展開全体に影響を与えました。COVID-19の世界的大流行により、世界各地でロックダウンが発生し、業界全体でいくつかの業務が停止しました。その結果、スマートメーターの出荷と設置にも影響が出ました。

- しかし、COVID-19規制が徐々に緩和されつつあるため、スマートメーターの設置台数は長期的には増加すると予想されます。多くの先進地域では、エネルギー供給会社の多くが、スマートメーターへのアップグレードを顧客に促しています。スマートメーターは、人との直接的なやりとりを最小限に抑え、省エネの動機付けや簡単な請求書支払い、遠隔検針、請求・回収効率の向上、技術的・商業的な総損失の削減、電力盗難の抑制など、バリューチェーン全体にわたっていくつかのメリットを提供するからです。

- 家電製品、オフィス機器、その他のプラグ負荷は、主要モードでない間、住宅・商業施設全体の電力の15%~20%近くを消費しています。このエネルギーの大半は、(使用していない間も)低電力モードで動作しているときに消費されます。消費者は、このようなシナリオを追跡するために、スマート・エネルギー管理システムを導入する傾向が強まっています。

スマート電力メーター市場の動向

住宅セグメントが大幅な成長を記録へ

- スマート電力計は、消費者が消費するエネルギーを計測するため、住宅部門で重要な役割を果たします。スマートグリッドへの投資の増加と、新興経済諸国における再生可能電源の既存グリッドへの統合率の急上昇は、スマート電力メーター市場の成長をサポートすると予想されます。

- メーターは電力消費量を測定し、これを中央ユーティリティ・システムに伝達します。世界的に、住宅部門におけるこれらの機器の設置は、ピーク時のエネルギー節約に傾倒する消費者の増加により、CO2排出量の削減に役立っています。

- 住宅建設活動の増加や、設置メーターの80%以上をスマート化することを目指すEUの20-20-20政策のような政府の指令により、スマート電力メーター市場の成長見通しは確実なものとなっています。

- さらに、消費者が独立型エネルギー発電システムに移行するにつれて、スマートグリッドの相互作用能力がますます重要になります。屋上太陽光発電システムや小型風力タービンは現在広く普及しており、多くの家庭や企業にとって費用対効果の高いものとなっています。スマートメーターの設置は、こうしたミニ発電システムすべてを効率的にグリッドに接続し、配電・計測プロセス全体を効果的かつ効率的にするのに役立つと思われます。

- さらに、都市化が進み、都市型ライフスタイルを重視する傾向が強まったことで、無駄を省くために電気、照明、エネルギーの自動制御を行うスマートホーム技術やデバイスの導入が拡大しました。したがって、世界的に家庭でのスマートホームデバイスや技術の採用が増加しており、住宅セグメントにおけるスマートメーターの成長がさらに促進されると予想されます。

米国が大きな市場シェアを占める

- 自動検針ソリューション市場は米国で成熟期を迎えており、成長が鈍化しています。さらに、米国のInstitute for Electric Innovationによると、米国では2021年までに1億1,500万台のスマートメーターが設置されるといいます。

- 第一世代メーターの買い替えと、(より高い機能と改良された技術を備えた)高度なメーター・インフラへの移行が、今後のスマート電力メーター市場を牽引すると予想されます。

- 米国中の電力会社は、エネルギーグリッドの健全性を監視し、停電発生時に電気サービスをより迅速に復旧させ、分散型エネルギー資源(DER)を統合し、エネルギーサービスとソリューションを顧客に提供するために、スマートメーターのデータを活用しています。さらに、米国の電力会社は、エネルギーグリッドを強化するために多額の投資を行っています。

- さらに、この地域のベンダーは、顧客エンゲージメント・ツールやその他のインセンティブ戦略などの追加ツールと組み合わせることで、スマート電力メーターの潜在能力を活用しており、市場におけるスマート電力メーターの採用を促進すると予想されます。例えば、ボルチモア・ガス・アンド・エレクトリックは、スマート電力メーターが設置されるたびに、顧客をスマート・エネルギー報奨プログラムに登録しています。顧客は、フィードバックやピーク時のリベートインセンティブを受け、エネルギーコストの削減に貢献します。

- 同様に、米国のパシフィック・ガス・アンド・エレクトリック社は、AMIをターゲットとした住宅改修プログラムにより、ターゲットとした住宅で3.5倍のエネルギー節約を実現したと報告しています。さらに、スマート電力メーターとデータ分析などの技術との統合は、この地域で調査された市場の成長をさらに促進すると予想されます。

スマート電力計産業の概要

スマート電力計市場は中程度の競争状態にあり、複数の大手企業で構成されています。大小多数のプレーヤーが存在するため、市場は適度に断片化されています。これらの企業は、戦略的イノベーションと共同イニシアティブを活用して市場シェアを拡大し、収益性を高めています。また、同市場で事業を展開する企業は、自社の製品力を強化するため、企業向けネットワーク機器技術に取り組む新興企業を買収しています。

2022年10月、アンドラ・プラデシュ州の電力公社は、スマート電力メーター・プロジェクトを展開するための素晴らしいアップを発表しました。連邦政府は、スマートメーター国家計画(SMNP)の下、インド全土で約25兆個の従来型メーターをスマートメーターに交換することを決定しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- 主要地域における政府の支援的規制

- スマートシティ展開の増加

- 市場抑制要因

- 高コストとセキュリティへの懸念

- スマートメーターとの統合の難しさ

第6章 市場セグメンテーション

- エンドユーザー別

- 住宅

- 商業

- 産業

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- スペイン

- ドイツ

- イタリア

- フランス

- トルコ

- 北欧

- ベネルクス

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- 韓国

- 東南アジア(マレーシア、シンガポール、タイ、その他)

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- コロンビア

- チリ

- その他ラテンアメリカ

- 中東・アフリカ

- GCC

- 南アフリカ

- エジプト

- その他のアフリカ

- その他中東

- 北米

第7章 競合情勢

- 企業プロファイル

- Landis+gyr Group AG

- Wasion Group Holdings

- Elster Group GMBH(Honeywell International Inc.)

- Jiangsu Linyang Energy Co. Ltd

- Sagemcom SAS

- Ningbo Sanxing Electric Co. Ltd

- Kamstrup A/S

- Hexing Electric Company Ltd

- Itron Inc.

- Holley Technology Ltd

- Nanjing Xinlian Electronics Co. Ltd

- Sensus USA Inc.(Xylem Inc)

- Shenzhen Hemei Group Co. Ltd

第8章 投資分析

第9章 市場の将来

目次

The Smart Electricity Meter Market size in terms of shipment volume is expected to grow from 104.76 million units in 2025 to 136.66 million units by 2030, at a CAGR of 5.46% during the forecast period (2025-2030).

Smart meters deployment enabled the implementation of a Home Energy Management System (HEMS) or Building Energy Management System (BEMS) that allows visualization of the electric power usage in individual homes or entire buildings.

Key Highlights

- Energy efficiency is increasingly becoming the primary focus globally, owing to the increasing economic activities, which led to high energy consumption rates and pushed global electricity grids to their limits. The global electricity generation in 2021 stood at 28,466 Terawatt-hours, according to BP.

- Digitization has been further accelerating and modernizing energy efficiency measures due to which the deployment of smart grids has been increasing globally, as they are capable of dynamically optimizing supply and fostering supply of large amounts of electricity from renewable energy sources, such as solar power.

- The recent COVID -19 outbreak and nationwide lockdown across the globe impacted the overall rollout of Smart meters globally. The global COVID -19 pandemic resulted in lockdowns in various parts of the world, which halted several operations across industries. As a result, the shipments and installations of smart meters were also affected.

- However, as the COVID-19 regulations are slowly being eased, the number of smart meters being installed is also expected to witness an increase in the long term. In many developed regions, most energy suppliers have been motivating their customers to upgrade to smart meters as it minimizes direct human interaction and offers several other benefits across the entire value chain, such as incentivizing energy conservation and facilitating easy bill payments, remote meter reading, improving billing and collection efficiency, reducing aggregate technical and commercial losses, and curbing power theft, among others.

- Consumer electronics, office equipment, and other plug loads consume nearly 15% to 20% of the total residential and commercial electricity while not in the primary mode. Most of this energy is consumed when they operate in low-power modes (even while they are not in use). Consumers are increasingly tending to install a smart energy management system to track such scenarios.

Smart Electricity Meter Market Trends

Residential Segment to Register Significant Growing

- Smart electric meter plays a significant role in the residential sector, as this meter measures the energy consumed by the consumers. The increasing smart grid investments and the surge in the rate of integration of renewable sources of power generation to the existing grids in developed economies are expected to support the growth of the smart electricity meter market.

- The meter measures the electricity consumption and communicates this to the central utility system. Globally, installations of these devices in the residential sector help in the reduction of CO2 emissions, owing to the increased consumer's inclination toward peak time savings of energy.

- The increasing residential construction activities and government mandates, like the EU 20-20-20 policy aiming to convert over 80% of the installed meter base to a smart one, have ensured growth prospects for the smart electricity meters market.

- Furthermore, as consumers move toward stand-alone energy generation systems, the interactive capacity of the Smart Grid will become more and more important. Rooftop solar electric systems and small wind turbines are now widely available and have become cost-effective for many homeowners and businesses. Installations of smart meters will help to effectively connect all these mini-power generating systems to the grid to help the overall power distribution and measurement process be effective and more efficient.

- Moreover, increasing urbanization and the increasing inclination toward the focus on developing urban lifestyles led to the expansion of deployment of smart home technologies and devices, which involves automatic control of electricity, light, and energy to avoid wastage. Hence, the increasing adoption of smart home devices and technologies across the homes globally is further expected to foster the growth in smart meters in the residential segment.

United States to Hold Significant Market Share

- The automatic meter reading solutions market has been reaching maturity in the United States, resulting in sluggish growth. Furthermore, according to the Institute for Electric Innovation in the United States, 115 million smart meters have been installed in the US by 2021.

- The replacement of first-generation meters and the shift to advanced metering infrastructure (with higher capabilities and improved technology) are expected to drive the smart electricity meters market in the future.

- Electric companies across the United States are leveraging smart meter data to monitor the health of the energy grid, restore electric service more quickly when outages occur, integrate distributed energy resources (DERs), and deliver energy services and solutions to customers. Furthermore, electricity companies in the United States are making significant investments to enhance the energy grid.

- Moreover, vendors in the region leveraging smart electric meters' potential by pairing them with additional tools, such as customer engagement tools and other incentive strategies, are expected to drive the adoption of smart electric meters in the market. For instance, Baltimore Gas and Electric enrolls its customers into its smart energy rewards program whenever the Smart electricity meter is installed. Customers receive feedback, peak time rebate incentives, and help reduce energy costs.

- Similarly, Pacific Gas & Electric, in the United States, reported AMI targeting a home retrofit program that delivers 3.5 times more energy savings in the targeted homes. Additionally, the integration of smart electric meters with technologies, such as data analytics, is expected to further foster the growth of the market studied in the region.

Smart Electricity Meter Industry Overview

The smart electricity meters market is moderately competitive and consists of several major players. The market is moderately fragmented, owing to the presence of many small and large players. These companies are leveraging strategic innovations and collaborative initiatives to increase their market share and increase their profitability. The companies operating in the market are also acquiring start-ups working on enterprise network equipment technologies to strengthen their product capabilities.

In October 2022, the power utilities of Andhra Pradesh announced a great up for rolling out a smart electricity meter project. The Union government decided to replace around 25 crore conventional meters with smart meters across India under the Smart Meter National Programme (SMNP).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Supportive Government Regulations in Key Regions

- 5.1.2 Rise in Smart City Deployment

- 5.2 Market Restraints

- 5.2.1 High Costs and Security Concerns

- 5.2.2 Integration Difficulties with Smart Meters

6 MARKET SEGMENTATION

- 6.1 By End-user

- 6.1.1 Residential

- 6.1.2 Commercial

- 6.1.3 Industrial

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Spain

- 6.2.2.3 Germany

- 6.2.2.4 Italy

- 6.2.2.5 France

- 6.2.2.6 Turkey

- 6.2.2.7 Nordics

- 6.2.2.8 Benelux

- 6.2.2.9 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 Australia and New Zealand

- 6.2.3.5 South Korea

- 6.2.3.6 Southeast Asia (Malaysia, Singapore, Thailand and Others)

- 6.2.3.7 Rest of Asia-Pacific

- 6.2.4 Latin America

- 6.2.4.1 Brazil

- 6.2.4.2 Mexico

- 6.2.4.3 Columbia

- 6.2.4.4 Chile

- 6.2.4.5 Rest of Latin America

- 6.2.5 Middle East & Africa

- 6.2.5.1 GCC

- 6.2.5.2 South Africa

- 6.2.5.3 Egypt

- 6.2.5.4 Rest of Africa

- 6.2.5.5 Rest of Middle East

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Landis+gyr Group AG

- 7.1.2 Wasion Group Holdings

- 7.1.3 Elster Group GMBH (Honeywell International Inc.)

- 7.1.4 Jiangsu Linyang Energy Co. Ltd

- 7.1.5 Sagemcom SAS

- 7.1.6 Ningbo Sanxing Electric Co. Ltd

- 7.1.7 Kamstrup A/S

- 7.1.8 Hexing Electric Company Ltd

- 7.1.9 Itron Inc.

- 7.1.10 Holley Technology Ltd

- 7.1.11 Nanjing Xinlian Electronics Co. Ltd

- 7.1.12 Sensus USA Inc. (Xylem Inc)

- 7.1.13 Shenzhen Hemei Group Co. Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日