|

市場調査レポート

商品コード

1741026

プライム発電機の市場機会と促進要因、産業動向分析、2025年~2034年予測Prime Power Generators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| プライム発電機の市場機会と促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月24日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

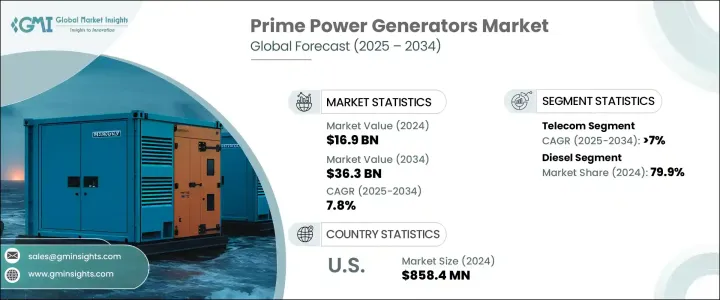

世界のプライム発電機市場は、2024年には169億米ドルとなり、CAGR 7.8%で成長し、2034年には363億米ドルに達すると推定されています。

この顕著な成長軌道は、特に安定した送電網へのアクセスが制限されていたり、安定していなかったりする地域において、中断のない信頼できる電力供給に対する需要が世界中で高まっていることに起因しています。世界のインフラが進化し、都市化が進むにつれて、産業界も政府も同様に、事業継続性を確保する発電ソリューションへの投資を優先しています。プライム発電機は、建設や製造からデータセンターや通信に至るまで、さまざまな用途で安定したエネルギーの流れを維持するために不可欠なものとなっています。デジタルトランスフォーメーションへのシフトと常時接続への依存度の高まりにより、電力の信頼性は利便性から必要性へと変化しています。

太陽光発電や風力発電の設置には、電力変動を管理し安定供給を確保するための堅牢なバックアップ・システムが必要となるため、再生可能エネルギーの導入急増もこの勢いに拍車をかけています。新興経済諸国では、急速な工業化とインフラ開発により、連続運転が可能な発電機に対する需要が高まっています。アジア、アフリカ、ラテンアメリカの国々では、新しい建設プロジェクトや製造施設が、特にオフグリッドや低グリッド安定地域において、信頼性の高いオンサイト電源を持つことに大きな重点を置いています。プライム発電機は、コスト効率、導入の容易さ、拡張性により、様々な産業および商業領域で好まれるソリューションとなっています。これらのシステムは、停電時だけでなく、送電網のインフラが不足している、あるいは未整備の一次電源としても重要なサポートを提供します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 169億米ドル |

| 予測金額 | 363億米ドル |

| CAGR | 7.8% |

農村部電化イニシアチブへの投資の増加により、十分なサービスを受けていない地域への電力アクセスがさらに拡大し、信頼性の高い発電機システムのニーズが高まっています。洪水、地震、ハリケーン、山火事などの自然災害は、危機時に緊急サービスや重要なインフラに電力を供給できるポータブルで堅牢な発電機ユニットの重要性を強調し続けています。また、ヘルスケア、運輸、緊急対応など、ダウンタイムが許されないミッションクリティカルな分野での採用も増加しています。さらに、データセンターや通信インフラの世界の普及に伴い、シームレスな運用をサポートし、データの損失やサービスの中断を防ぐ高信頼性の電源システムが求められています。

電気通信産業は、依然としてプライム発電機市場の重要な成長要因です。電気通信専用の発電機セグメントは、2034年までCAGR 7%で拡大すると予測されています。モバイルユーザー数が飛躍的に増加し、データ消費量が前例のないレベルに達しているため、通信事業者は積極的にインフラを拡張しています。このような成長には、電力不安定が一般的な問題である地方、遠隔地、災害の多い地域でタワーやネットワークの運用を支える安定した電力供給が必要です。プライム発電機は、このようなニーズに対応し、通信サービスの継続的なアップタイムを確保する上で不可欠な存在となっています。

燃料タイプ別に見ると、ディーゼル発電機が世界市場を独占し、2024年には79.9%のシェアを占める。ディーゼル発電機が市場をリードしている主な理由は、その実証済みの信頼性、高い燃料効率、特に物流が課題となっている地域での手頃な価格です。ディーゼル発電機は、堅牢性、メンテナンスの容易さ、多様な環境条件下での性能で知られ、オフグリッドや産業用アプリケーションの最有力選択肢となっています。幅広い使用環境に対応するため、短期間の配備にも長期間の電力ニーズにも理想的です。

北米では、プライム発電機市場は2034年までCAGR 6%で成長すると予測されています。この地域では、ハリケーン、山火事、冬の嵐などの異常気象に対する脆弱性が高まっており、住宅、商業、工業の各分野で信頼性の高いバックアップ電源ソリューションに対する需要が高まっています。継続的なインフラの近代化とエネルギー回復力への投資は、市場成長に影響を与える重要な要因です。プライム発電機は、ヘルスケア、交通機関、緊急対応システムなどの必要不可欠なサービスにおいて、業務の継続性を確保する上で極めて重要な役割を果たしています。

世界のプライム発電機市場を形成している主要企業には、Siemens Energy、Generac Power Systems、YANMAR HOLDINGS、Rolls-Royce、Caterpillar、Ashok Leyland、Cummins、Wartsila、三菱重工業、Briggs &Stratton、Scania、Kirloskar、Atlas Copco、Volvo Penta、PR INDUSTRIAL、Mahindra POWEROL、Deere &Company、Rehlko、Rapid Power Generation、HIMOINSAなどがあります。これらの企業は、多様な市場ニーズに対応するため、ハイブリッド・ユニットや燃料フレキシブル・ユニットで製品ポートフォリオを積極的に拡大しています。戦略的提携、合併、買収により、より広範な市場への参入と技術革新が可能になっています。さらに、デジタル・モニタリング、予知保全、排ガス適合技術への投資は、メーカーがパワフルで効率的、かつ適応性のある発電機ソリューションを提供しながら、世界の持続可能性目標に沿うことを支援しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:出力別、2021-2034

- 主要動向

- 50kVA以下

- 50kVA~125kVA以上

- 125kVA~200kVA以上

- 200kVA~330kVA以上

- 330kVA~750kVA以上

- 750kVA以上

第6章 市場規模・予測:燃料別、2021-2034

- 主要動向

- ディーゼル

- ガス

第7章 市場規模・予測:用途別、2021-2034

- 主要動向

- 通信

- ホスピタリティ

- 石油・ガス

- 鉱業

- 工事

- 農業

- 産業

- その他

第8章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ロシア

- 英国

- ドイツ

- フランス

- スペイン

- オーストリア

- イタリア

- アジア太平洋地域

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- インドネシア

- マレーシア

- タイ

- ベトナム

- フィリピン

- ミャンマー

- バングラデシュ

- 中東

- サウジアラビア

- アラブ首長国連邦

- カタール

- トルコ

- イラン

- オマーン

- アフリカ

- エジプト

- ナイジェリア

- アルジェリア

- 南アフリカ

- アンゴラ

- ケニア

- モザンビーク

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- チリ

第9章 企業プロファイル

- Ashok Leyland

- Atlas Copco

- Briggs &Stratton

- Caterpillar

- Cummins

- Deere &Company

- Generac Power Systems

- HIMOINSA

- Kirloskar

- Mahindra POWEROL

- Mitsubishi Heavy Industries

- PR INDUSTRIAL

- Rapid Power Generation

- Rehlko

- Rolls-Royce

- Scania

- Siemens Energy

- Volvo Penta

- Wartsila

- YANMAR HOLDINGS

The Global Prime Power Generators Market was valued at USD 16.9 billion in 2024 and is estimated to grow at a CAGR of 7.8% to reach USD 36.3 billion by 2034. This remarkable growth trajectory is driven by the increasing demand for uninterrupted and dependable electricity supply across the globe, particularly in regions where access to a stable power grid remains limited or inconsistent. As global infrastructure evolves and urbanization intensifies, industries and governments alike are prioritizing investments in power generation solutions that ensure operational continuity. Prime power generators have become indispensable in maintaining consistent energy flow in various applications ranging from construction and manufacturing to data centers and telecommunications. With the shift toward digital transformation and heightened reliance on always-on connectivity, power reliability has transitioned from a convenience to a necessity.

The surge in renewable energy adoption is also contributing to the momentum, as solar and wind installations require robust backup systems to manage power fluctuations and ensure consistent supply. In emerging economies, rapid industrialization and infrastructure development are generating increased demand for continuous-duty power generators. New construction projects and manufacturing facilities in countries across Asia, Africa, and Latin America are placing significant emphasis on having a reliable, on-site power source, especially in off-grid or low-grid-stability regions. Cost-efficiency, ease of deployment, and scalability make prime power generators a preferred solution across various industrial and commercial domains. These systems offer critical support not just during blackouts but as primary power sources where grid infrastructure is lacking or underdeveloped.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.9 Billion |

| Forecast Value | $36.3 Billion |

| CAGR | 7.8% |

Rising investments in rural electrification initiatives are further expanding electricity access to underserved areas, boosting the need for dependable generator systems. Natural disasters such as floods, earthquakes, hurricanes, and wildfires continue to underline the importance of portable and rugged generator units capable of powering emergency services and critical infrastructure during crises. The market is also seeing increased adoption in mission-critical sectors like healthcare, transportation, and emergency response-industries that require zero tolerance for downtime. Additionally, the global proliferation of data centers and telecom infrastructure demands high-reliability power systems to support seamless operations and prevent data loss or service interruptions.

The telecom industry remains a significant growth driver in the prime power generators market. The segment dedicated to telecom-specific generators is anticipated to expand at a CAGR of 7% through 2034. With mobile user bases growing exponentially and data consumption reaching unprecedented levels, telecom providers are aggressively scaling their infrastructure. This growth requires a consistent power supply to support tower and network operations in rural, remote, or disaster-prone regions where power instability is a common issue. Prime power generators are proving essential in meeting these needs, ensuring continuous uptime for communication services.

When segmented by fuel type, diesel generators dominate the global market, holding a 79.9% share in 2024. Their market leadership is largely due to their proven reliability, high fuel efficiency, and affordability, particularly in regions with challenging logistics. Diesel-powered generators are known for their robustness, ease of maintenance, and ability to perform under diverse environmental conditions, making them the top choice for off-grid and industrial applications. Their compatibility with a wide range of operating environments makes them ideal for both short-term deployments and long-duration power needs.

In North America, the prime power generators market is forecasted to grow at a CAGR of 6% through 2034. The region's increasing vulnerability to extreme weather events-including hurricanes, wildfires, and winter storms-is amplifying the demand for reliable backup power solutions across residential, commercial, and industrial segments. Ongoing infrastructure modernization and investment in energy resilience are key factors influencing market growth. Prime power generators are playing a pivotal role in ensuring operational continuity across essential services such as healthcare, transportation, and emergency response systems.

Leading players shaping the global prime power generators landscape include Siemens Energy, Generac Power Systems, YANMAR HOLDINGS, Rolls-Royce, Caterpillar, Ashok Leyland, Cummins, Wartsila, Mitsubishi Heavy Industries, Briggs & Stratton, Scania, Kirloskar, Atlas Copco, Volvo Penta, PR INDUSTRIAL, Mahindra POWEROL, Deere & Company, Rehlko, Rapid Power Generation, and HIMOINSA. These companies are actively expanding their product portfolios with hybrid and fuel-flexible units to meet diverse market needs. Strategic collaborations, mergers, and acquisitions are enabling broader market reach and innovation. Additionally, investments in digital monitoring, predictive maintenance, and emission-compliant technologies are helping manufacturers align with global sustainability goals while delivering powerful, efficient, and adaptive generator solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Rating, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 330 kVA

- 5.6 > 330 kVA - 750 kVA

- 5.7 > 750 kVA

Chapter 6 Market Size and Forecast, By Fuel, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Gas

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Telecom

- 7.3 Hospitality

- 7.4 Oil & gas

- 7.5 Mining

- 7.6 Construction

- 7.7 Agriculture

- 7.8 Industries

- 7.9 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Russia

- 8.3.2 UK

- 8.3.3 Germany

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Austria

- 8.3.7 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.4.6 Indonesia

- 8.4.7 Malaysia

- 8.4.8 Thailand

- 8.4.9 Vietnam

- 8.4.10 Philippines

- 8.4.11 Myanmar

- 8.4.12 Bangladesh

- 8.5 Middle East

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Turkey

- 8.5.5 Iran

- 8.5.6 Oman

- 8.6 Africa

- 8.6.1 Egypt

- 8.6.2 Nigeria

- 8.6.3 Algeria

- 8.6.4 South Africa

- 8.6.5 Angola

- 8.6.6 Kenya

- 8.6.7 Mozambique

- 8.7 Latin America

- 8.7.1 Brazil

- 8.7.2 Mexico

- 8.7.3 Argentina

- 8.7.4 Chile

Chapter 9 Company Profiles

- 9.1 Ashok Leyland

- 9.2 Atlas Copco

- 9.3 Briggs & Stratton

- 9.4 Caterpillar

- 9.5 Cummins

- 9.6 Deere & Company

- 9.7 Generac Power Systems

- 9.8 HIMOINSA

- 9.9 Kirloskar

- 9.10 Mahindra POWEROL

- 9.11 Mitsubishi Heavy Industries

- 9.12 PR INDUSTRIAL

- 9.13 Rapid Power Generation

- 9.14 Rehlko

- 9.15 Rolls-Royce

- 9.16 Scania

- 9.17 Siemens Energy

- 9.18 Volvo Penta

- 9.19 Wartsilä

- 9.20 YANMAR HOLDINGS