|

市場調査レポート

商品コード

1716687

IVHM(統合型車両ヘルスマネジメント)の市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Integrated Vehicle Health Management (IVHM) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| IVHM(統合型車両ヘルスマネジメント)の市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月04日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

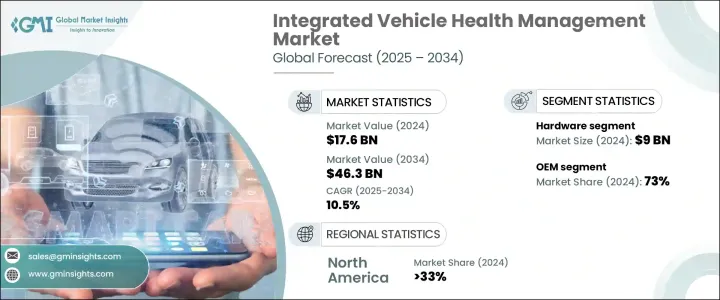

世界のIVHM(統合型車両ヘルスマネジメント)市場の2024年の市場規模は176億米ドルで、2025年から2034年にかけてCAGR 10.5%で成長すると予測されています。

この市場拡大の背景には、電気自動車(EV)の急速な普及、コネクテッドカーの台頭、最新の自動車における予知保全のニーズの高まりがあります。自動車技術の高度化に伴い、メーカーや車両運行会社は、性能の向上、寿命の延長、ダウンタイムの削減を実現するため、リアルタイムの車両ヘルスモニタリングに注力しています。IVHMシステムは現在、リアルタイム診断、予測分析、プロアクティブ・メンテナンス・ソリューションを提供する、自動車エコシステムの重要な構成要素となっています。

自動車メーカーは、先進的なIVHM技術を統合することで、車両の効率を高め、故障を最小限に抑え、全体的な安全性を向上させています。自動車産業が電動化へとシフトする中、バッテリーの健全性監視ソリューションの需要が急増しています。電気自動車やハイブリッド車では、ドライブトレイン、バッテリー電圧、充電システムなどの重要なコンポーネントを継続的に追跡する必要があります。自動車エレクトロニクスの複雑化は、自律走行技術の台頭と相まって、高度なIVHMソリューションの必要性をさらに高めています。自動車メーカー、車両管理者、サービスプロバイダーは、AIを活用した分析とクラウドベースのプラットフォームを活用して、事前予防的なメンテナンスを確実に行い、運用リスクを最小限に抑えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 176億米ドル |

| 予測金額 | 463億米ドル |

| CAGR | 10.5% |

IVHM市場はハードウェア、ソフトウェア、サービスに分類され、ハードウェアが優位を占める。2024年の市場シェアはハードウェアが50%を占め、90億米ドルを創出します。センサーは、エンジン温度、タイヤ空気圧、バッテリーの健全性など、車両の主要パラメーターを監視する上で極めて重要な役割を果たします。これらの部品はリアルタイムの診断を可能にし、重要なシステムが最適に機能することを保証します。自動車産業の進歩に伴い、EVや自律走行車向けに設計された特殊なハードウェアの需要は増加の一途をたどっています。

市場セグメンテーションには販売チャネルも含まれ、相手先商標製品メーカー(OEM)が大きなシェアを占めています。2024年には、OEMがIVHMシステムを製造時に車両に組み込むため、市場の73%を支配しています。このシームレスな統合により、車両は当初から高度な診断、テレマティクス、継続的モニタリング機能の恩恵を受けることができます。OEMはイノベーションの最前線に立ち続け、電気自動車やコネクテッドカーの所有者の進化するニーズに対応しています。EVセグメントでは予知保全とバッテリーの健全性管理が極めて重要になっており、メーカーは最先端のIVHMソリューションに多額の投資を行っています。

米国のIVHM(統合型車両ヘルスマネジメント)(IVHM)市場は、2024年に32億米ドルを生み出し、33%のシェアを占める。同国は自動車および航空宇宙分野で強い存在感を示しており、IVHM技術の需要を牽引しています。自動車の安全性、排出ガス、メンテナンスに関連する政府規制が強化され、導入がさらに加速しています。さらに、民間車両運行会社や防衛機関は、業務効率を高めるために予知保全を優先しています。米国市場では、データ主導の車両ヘルスマネジメントシステムへと急速にシフトしており、運輸業界全体で最適な性能、コンプライアンス、コスト削減を実現しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- プラットフォームプロバイダー

- ソフトウェア・プロバイダ

- サービスプロバイダー

- 流通チャネル

- 最終用途

- 利益率分析

- テクノロジーとイノベーションの展望

- 特許分析

- 主要ニュースと取り組み

- コスト内訳分析

- 規制状況

- 影響要因

- 促進要因

- 予知保全に対する需要の高まり

- EVとコネクテッドカーの需要増加

- 車両の複雑化

- IoTとAIの技術的進歩

- 規制要件と安全基準

- 業界の潜在的リスク&課題

- データ・セキュリティとプライバシーに関する懸念

- レガシーシステムとの統合の複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- センサー

- 電子制御ユニット(ECU)

- データ収集システム

- 通信モジュール

- テレマティクス制御ユニット(TCU)

- 車載診断(OBD)ポート

- ソフトウェア

- 診断ソフトウェア

- 診断ソフトウェア

- データ管理ソフトウェア

- ユーザーインターフェース(UI)ソフトウェア

- サービス

- 設置および統合サービス

- 保守・修理サービス

- コンサルティングサービス

第6章 市場推計・予測:チャネル別、2021年~2034年

- 主要動向

- OEM

- サービスセンター

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 診断

- 予後診断

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 民間・防衛航空

- 自動車

- 船舶

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Acellent Technologies

- Aptiv

- Boeing

- Caterpillar

- Cummins

- General Electric

- Honeywell

- IBM

- Intangles Lab

- Iotasmart

- Lockheed Martin

- Michelin

- North Atlantic Industries

- OnStar

- Robert Bosch GmbH

- Rockwell Collins

- Rolls Royce

- Sibros Technologies Inc

- TATA Elxsi

- ZF Friedrichshafen

The Global Integrated Vehicle Health Management Market was valued at USD 17.6 billion in 2024 and is expected to grow at a CAGR of 10.5% between 2025 and 2034. This expansion is fueled by the rapid adoption of electric vehicles (EVs), the rise of connected cars, and the increasing need for predictive maintenance in modern automobiles. As automotive technologies become more sophisticated, manufacturers and fleet operators are focusing on real-time vehicle health monitoring to enhance performance, extend lifespan, and reduce downtime. IVHM systems are now a critical component of the automotive ecosystem, offering real-time diagnostics, predictive analytics, and proactive maintenance solutions.

Automakers are integrating advanced IVHM technologies to enhance vehicle efficiency, minimize breakdowns, and improve overall safety. With the automotive industry shifting toward electrification, the demand for battery health monitoring solutions has surged. Electric and hybrid vehicles require continuous tracking of vital components like drivetrains, battery voltage, and charging systems. The growing complexity of automotive electronics, coupled with the rise of autonomous driving technologies, further amplifies the need for sophisticated IVHM solutions. Automakers, fleet managers, and service providers are leveraging AI-powered analytics and cloud-based platforms to ensure proactive maintenance and minimize operational risks.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.6 Billion |

| Forecast Value | $46.3 Billion |

| CAGR | 10.5% |

The IVHM market is categorized into hardware, software, and services, with hardware dominating the landscape. In 2024, hardware accounted for a 50% market share, generating USD 9 billion. Sensors play a pivotal role in monitoring key vehicle parameters, including engine temperature, tire pressure, and battery health. These components enable real-time diagnostics, ensuring that critical systems function optimally. As the automotive industry advances, demand for specialized hardware designed for EVs and autonomous vehicles continues to rise.

Market segmentation also includes distribution channels, with original equipment manufacturers (OEMs) holding a significant share. In 2024, OEMs controlled 73% of the market as they integrated IVHM systems into vehicles during manufacturing. This seamless incorporation allows vehicles to benefit from advanced diagnostics, telematics, and continuous monitoring capabilities from the outset. OEMs remain at the forefront of innovation, addressing the evolving needs of electric and connected vehicle owners. With predictive maintenance and battery health management becoming crucial in the EV segment, manufacturers are investing heavily in cutting-edge IVHM solutions.

The U.S. Integrated Vehicle Health Management (IVHM) Market generated USD 3.2 billion in 2024, accounting for a 33% share. The country's strong presence in the automotive and aerospace sectors drives demand for IVHM technologies. Stricter government regulations related to vehicle safety, emissions, and maintenance further accelerate adoption. Additionally, commercial fleet operators and defense agencies are prioritizing predictive maintenance to enhance operational efficiency. The U.S. market is witnessing a rapid shift toward data-driven vehicle health management systems, ensuring optimal performance, compliance, and cost savings across the transportation industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Platform provider

- 3.2.2 Software provider

- 3.2.3 Service provider

- 3.2.4 Distribution channel

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Cost breakdown analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Growing demand for predictive maintenance

- 3.9.1.2 Increase in demand for EVs and connected vehicle

- 3.9.1.3 Increasing vehicle complexity

- 3.9.1.4 Technological advancements in IoT and AI

- 3.9.1.5 Regulatory requirements and safety standards

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Data security and privacy concerns

- 3.9.2.2 Complexity of integration with legacy systems

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensors

- 5.2.2 Electronic Control Units (ECUs)

- 5.2.3 Data acquisition systems

- 5.2.4 Communication modules

- 5.2.5 Telematics Control Units (TCUs)

- 5.2.6 On-board diagnostics (OBD) ports

- 5.3 Software

- 5.3.1 Diagnostics software

- 5.3.2 Prognostic software

- 5.3.3 Data management software

- 5.3.4 User Interface (UI) software

- 5.4 Service

- 5.4.1 Installation and integration services

- 5.4.2 Maintenance and repair services

- 5.4.3 Consulting services

Chapter 6 Market Estimates & Forecast, By Channel, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 OEM

- 6.3 Service center

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Diagnostics

- 7.3 Prognostics

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Commercial & defense aviation

- 8.3 Automotive

- 8.4 Marine

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Acellent Technologies

- 10.2 Aptiv

- 10.3 Boeing

- 10.4 Caterpillar

- 10.5 Cummins

- 10.6 General Electric

- 10.7 Honeywell

- 10.8 IBM

- 10.9 Intangles Lab

- 10.10 Iotasmart

- 10.11 Lockheed Martin

- 10.12 Michelin

- 10.13 North Atlantic Industries

- 10.14 OnStar

- 10.15 Robert Bosch GmbH

- 10.16 Rockwell Collins

- 10.17 Rolls Royce

- 10.18 Sibros Technologies Inc

- 10.19 TATA Elxsi

- 10.20 ZF Friedrichshafen