|

市場調査レポート

商品コード

1928978

溶接機器および消耗品の市場機会、成長要因、業界動向分析、ならびに2026年から2035年までの予測Welding Equipment and Consumables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 溶接機器および消耗品の市場機会、成長要因、業界動向分析、ならびに2026年から2035年までの予測 |

|

出版日: 2026年01月14日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

概要

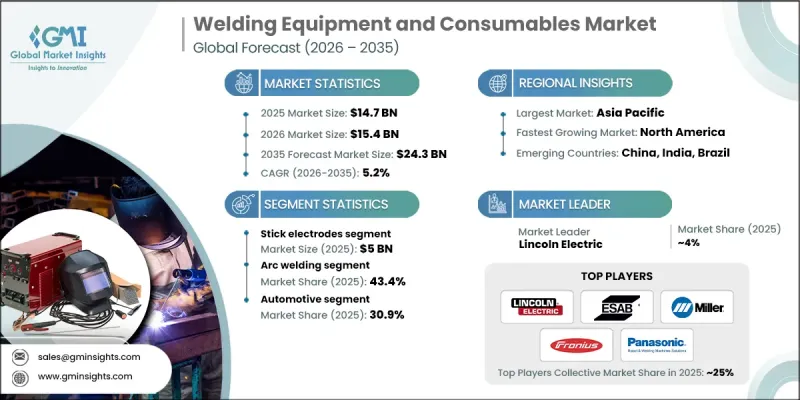

世界の溶接機器および消耗品市場は、2025年に147億米ドルと評価され、2035年までにCAGR5.2%で成長し、243億米ドルに達すると予測されています。

この業界の拡大は、信頼性と高強度を備えた溶接ソリューションを必要とする急速な都市化と大規模なインフラ開発によって推進されています。現代のインフラプロジェクトでは、橋梁、鉄道、高速道路、産業施設における耐久性と構造的完全性を確保するため、高度な溶接技術が求められています。建設分野を超えて、持続可能な建築手法への移行により、効率性を向上させ環境への影響を最小限に抑える革新的な溶接技術の必要性が高まっています。公共部門と民間部門の双方によるインフラ投資が、持続的な成長機会を生み出しています。同時に、自動車・輸送産業では電気自動車や軽量素材の採用により変革が進んでおり、新たな合金や複合材に対応可能な特殊溶接機器・消耗品への需要をさらに促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 147億米ドル |

| 予測金額 | 243億米ドル |

| CAGR | 5.2% |

棒状電極セグメントは2025年に50億米ドルを占め、2035年までCAGR4.6%で成長すると予測されています。これらの電極は、コスト効率の良さ、汎用性、屋外や過酷な環境下でも確実に機能する能力により人気を保っており、建設、修理、メンテナンス用途において不可欠な存在です。その頑丈な設計により、風雨や極端な温度環境下など、他の消耗品が故障する可能性のある環境でも、溶接作業を効率的に行うことが可能です。また、スティック電極は幅広い金属や合金との互換性を備えており、多様なプロジェクトにおいて一貫した溶接品質を提供します。

アーク溶接セグメントは2025年に43.4%のシェアを占めました。アーク溶接の適応性と効率性は、自動車、建設、重工業など高品質な溶接を必要とする産業において中核的な役割を果たしています。シールドメタルアーク溶接(SMAW)、ガスメタルアーク溶接(GMAW)、サブマージドアーク溶接(SAW)などの技術は、様々な金属や合金において耐久性と精密性を兼ね備えた溶接を実現するために広く採用されています。

米国溶接機器・消耗品市場は2025年に27億米ドルの規模を記録し、2026年から2035年にかけてCAGR5.7%で拡大が見込まれています。米国市場は強固な産業基盤と高度に発達した製造業セクターを背景に、自動車・航空宇宙・エネルギー産業における自動化・ロボット溶接システムの普及が精密機器の需要を牽引しています。厳しい安全基準と品質基準を満たすことへの注力が、先進的な産業プロセスを支える最先端の溶接技術と消耗品への投資を加速させております。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- インフラ整備と工業化

- 自動車・輸送分野の拡大

- 溶接プロセスにおける技術的進歩

- 課題と困難

- 初期投資および維持管理コストの高さ

- 熟練労働力の不足

- 機会

- 自動化とインダストリー4.0の導入

- 再生可能エネルギー分野における需要の拡大

- 促進要因

- 成長可能性分析

- 今後の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 規制情勢

- 北米

- 米国:消費者製品安全委員会(CPSC)連邦規則集(CFR)第16編第1512部

- カナダ:国際標準化機構(ISO)4210

- 欧州

- ドイツ:ドイツ規格協会(DIN)欧州規格(EN)ISO 4210

- 英国:欧州規格(EN)ISO 4210/英国適合性評価(UKCA)

- フランス:欧州規格(EN)ISO 4210

- アジア太平洋地域

- 中国:国家標準(GB)3565

- インド:インド規格(IS)10613

- 日本:日本工業規格(JIS)D 9110

- ラテンアメリカ

- ブラジル:ブラジル技術規格協会(ABNT)ブラジル規格(NBR)ISO 4210

- メキシコ:国際標準化機構(ISO)4210

- 中東・アフリカ

- 南アフリカ:南アフリカ国家規格(SANS)311

- サウジアラビア:サウジアラビア規格・計量・品質機構(SASO)湾岸標準化機構(GSO)ISO 4210

- 北米

- 貿易統計(HSコード-8501)

- 主要輸入国

- 主要輸出国

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:タイプ別、2022-2035

- 棒状電極

- 単線

- フラックス巻線

- ソーイングワイヤー

- その他(棒状電極、シールドガスなど)

第6章 市場推計・予測:技術別、2022-2035

- アーク溶接

- 抵抗溶接

- 酸素燃料溶接

- 固体状態溶接

- その他(電子ビームなど)

第7章 市場推計・予測:用途別、2022-2035

- 自動車

- 建築・建設

- 船舶

- 航空宇宙・防衛

- 石油・ガス

- その他(金属、鉱業など)

第8章 市場推計・予測:流通チャネル別、2022-2035

- 直接販売

- 間接

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第10章 企業プロファイル

- Ador Welding Ltd.

- Air Liquide Welding

- Arcon Welding Equipment

- Bohler Welding

- Denyo Co., Ltd.

- ESAB

- Fronius International GmbH

- Hyundai Welding Co., Ltd.

- Illinois Tool Works Inc.(ITW)

- Jasic Technology Co., Ltd.

- Kemppi Oy

- Lincoln Electric

- Miller Electric

- Panasonic Welding Systems

- Tianjin Golden Bridge Welding Materials Group