|

市場調査レポート

商品コード

1716706

オプトエレクトロニクス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Optoelectronics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| オプトエレクトロニクス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月17日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

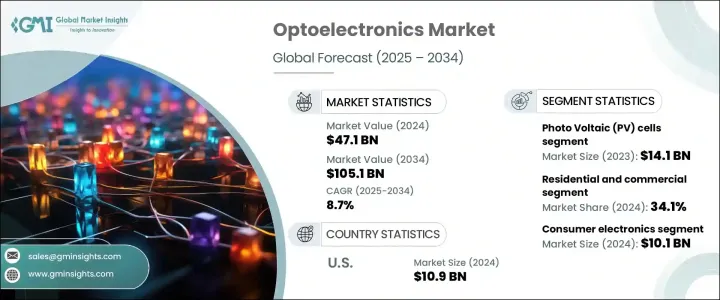

オプトエレクトロニクスの世界市場は、2024年に471億米ドルを生み出し、2025年から2034年にかけてCAGR 8.7%で成長すると予測されています。

エネルギー効率の高いソリューションに対する需要の高まりが、消費電力が少なく性能が向上した電子システムを産業界が積極的に求めるようになり、市場の成長を促進しています。発光ダイオード(LED)、レーザーダイオード、光電池などのオプトエレクトロニクスデバイスは、コスト効率が高く環境に優しいソリューションを提供できることから、広く採用されるようになっています。持続可能性への注目の高まりとエネルギーコスト削減の必要性が相まって、さまざまな分野でこれらの技術の採用がさらに加速しています。産業界がより環境に優しい代替エネルギーへと移行するにつれ、オプトエレクトロニクスは先進的な照明システム、通信技術、画像処理アプリケーションに不可欠な要素となりつつあります。

さらに、光ファイバーネットワーク、インテリジェントディスプレイシステム、自律走行車技術の利用拡大により、現代インフラにおけるオプトエレクトロニクスの範囲が拡大しています。センサー技術の進歩は、モノのインターネット(IoT)や人工知能(AI)ソリューションの統合と相まって、オプトエレクトロニクスシステムの機能性と効率性を高めています。また、世界各国の政府は、有利な政策や財政的インセンティブを通じて再生可能エネルギーの導入を推進しており、これが太陽電池や太陽エネルギーソリューションの需要をさらに押し上げ、市場全体の成長を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 471億米ドル |

| 予測金額 | 1,051億米ドル |

| CAGR | 8.7% |

オプトエレクトロニクス市場は、光電池(PV)セル、オプトカプラ、イメージセンサ、LED、その他の技術などタイプ別に区分されます。光電池セグメントは、2023年に141億米ドルを生み出し、主に再生可能エネルギー重視の高まりと太陽電池技術の進歩が原動力となっています。ペロブスカイト太陽電池、バイフェイシャルモジュール、高効率シリコンPVデバイスなどの主な技術革新は、これらのシステムの費用対効果とエネルギー変換能力を高めています。また、住宅、商業、工業分野での太陽エネルギー導入を奨励する政府の取り組みも、この分野の成長に寄与しています。持続可能なエネルギー慣行への移行が進んでいることから、PV技術の採用はさらに進むと予想され、世界のエネルギー転換の重要な要素となっています。

最終用途では、オプトエレクトロニクス市場は住宅、商業、産業分野にサービスを提供しています。住宅および商業セグメントは、2023年に市場シェアの34.1%を占め、スマートホーム技術、エネルギー効率の高い照明ソリューション、先進的ディスプレイシステムの需要増が原動力となっています。インテリジェント照明、セキュリティシステム、太陽エネルギーソリューションなどの用途でLED、画像センサー、光電池の人気が高まっていることが、このセグメントの成長を後押ししています。消費者は、エネルギー効率を高め、ホームオートメーションシステム全体を改善するためにこれらの技術を採用する傾向が強まっており、市場拡大にさらに貢献しています。

2024年の米国のオプトエレクトロニクス市場規模は109億米ドルで、研究開発への多額の投資と強力な半導体インフラに支えられた力強い成長となっています。自律走行車、ヘルスケアイメージング、光ファイバ通信ネットワークなどの分野でオプトエレクトロニクスデバイスの利用が増加していることが、この地域の技術革新と市場拡大を促進しています。大手技術プレイヤの存在と半導体技術の継続的な進歩が米国のオプトエレクトロニクス産業の成長見通しを高めており、世界市場への主要貢献国として位置付けられています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- エネルギー効率の高いソリューションに対する需要の高まり

- コンシューマーエレクトロニクスでの用途拡大

- 自動車用オプトエレクトロニクスの進歩

- 高速光通信の成長

- ヘルスケアおよびバイオメディカルアプリケーションの進歩

- 業界の潜在的リスク&課題

- 高い製造コスト

- 複雑な集積化と小型化の問題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 光起電力(PV)セル

- オプトカプラ

- イメージセンサー

- 発光ダイオード(LED)

- その他

第6章 市場推計・予測:出力タイプ別、2021年~2034年

- 主要動向

- アナログ

- デジタル

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅および商業

- 産業

第8章 市場推計・予測、産業別、2021年~2034年

- 主要動向

- 自動車

- 航空宇宙・防衛

- コンシューマーエレクトロニクス

- 情報技術

- ヘルスケア

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Avago Technologies

- Broadcom Inc.

- Cree Inc.

- Hamamatsu Photonics

- Kyocera Corporation

- LG Innotek

- Lumileds

- Luminit

- Nichia Corporation

- ON Semiconductor

- Osram Licht AG

- Panasonic Corporation

- Renesas Electronics

- Rohm Semiconductor

- Samsung Electronics

- Sharp Corporation

- Sony Corporation

- STMicroelectronics

- Texas Instruments

- Toshiba Corporation

The Global Optoelectronics Market generated USD 47.1 billion in 2024 and is projected to grow at a CAGR of 8.7% from 2025 to 2034. The increasing demand for energy-efficient solutions is driving the growth of the market as industries actively seek electronic systems with lower power consumption and improved performance. Optoelectronic devices, such as light-emitting diodes (LEDs), laser diodes, and photovoltaic cells, are gaining widespread adoption due to their ability to deliver cost-effective and eco-friendly solutions. The rising focus on sustainability, combined with the need to reduce energy costs, is further accelerating the adoption of these technologies across various sectors. As industries transition toward greener energy alternatives, optoelectronics is becoming an integral part of advanced lighting systems, communication technologies, and imaging applications.

Additionally, the growing use of fiber-optic networks, intelligent display systems, and autonomous vehicle technologies is expanding the scope of optoelectronics in modern infrastructure. Advancements in sensor technologies, combined with the integration of the Internet of Things (IoT) and artificial intelligence (AI) solutions, are enhancing the functionality and efficiency of optoelectronic systems. Governments worldwide are also promoting renewable energy adoption through favorable policies and financial incentives, which are further driving the demand for photovoltaic cells and solar energy solutions, thereby boosting the market's overall growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $47.1 Billion |

| Forecast Value | $105.1 Billion |

| CAGR | 8.7% |

The optoelectronics market is segmented by type, including photovoltaic (PV) cells, optocouplers, image sensors, LEDs, and other technologies. The photovoltaic cells segment generated USD 14.1 billion in 2023, primarily driven by the growing emphasis on renewable energy and advancements in solar technology. Key innovations such as perovskite solar cells, bifacial modules, and high-efficiency silicon PV devices are increasing the cost-effectiveness and energy conversion capabilities of these systems. Government initiatives that encourage solar energy adoption across residential, commercial, and industrial sectors are also contributing to the growth of this segment. The ongoing shift toward sustainable energy practices is expected to drive further adoption of PV technologies, making them a critical component of the global energy transition.

In terms of end-use applications, the optoelectronics market serves residential, commercial, and industrial sectors. The residential and commercial segment accounted for 34.1% of the market share in 2023, driven by increasing demand for smart home technologies, energy-efficient lighting solutions, and advanced display systems. The rising popularity of LEDs, image sensors, and photovoltaic cells in applications such as intelligent lighting, security systems, and solar energy solutions is fueling growth in this segment. Consumers are increasingly adopting these technologies to enhance energy efficiency and improve overall home automation systems, further contributing to market expansion.

The U.S. optoelectronics market was valued at USD 10.9 billion in 2024, with robust growth supported by significant investments in research and development and a strong semiconductor infrastructure. The increasing use of optoelectronic devices in sectors such as autonomous vehicles, healthcare imaging, and fiber-optic communication networks is driving innovation and market expansion across the region. The presence of leading technology players, along with ongoing advancements in semiconductor technologies, is enhancing the growth prospects for the U.S. optoelectronics industry, positioning it as a key contributor to the global market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for energy-efficient solutions

- 3.6.1.2 Expanding applications in consumer electronics

- 3.6.1.3 Advancements in automotive optoelectronics

- 3.6.1.4 Growth in high-speed optical communication

- 3.6.1.5 Advancements in healthcare and biomedical applications

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High manufacturing costs

- 3.6.2.2 Complex integration and miniaturization issues

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Photo Voltaic (PV) cells

- 5.3 Optocouplers

- 5.4 Image sensors

- 5.5 Light Emitting Diodes (LED)

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Output Type, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Analog

- 6.3 Digital

Chapter 7 Market Estimates & Forecast, End Use, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Residential and commercial

- 7.3 Industrial

Chapter 8 Market Estimates & Forecast, Industry, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Aerospace and defense

- 8.4 Consumer electronics

- 8.5 Information technology

- 8.6 Healthcare

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Avago Technologies

- 10.2 Broadcom Inc.

- 10.3 Cree Inc.

- 10.4 Hamamatsu Photonics

- 10.5 Kyocera Corporation

- 10.6 LG Innotek

- 10.7 Lumileds

- 10.8 Luminit

- 10.9 Nichia Corporation

- 10.10 ON Semiconductor

- 10.11 Osram Licht AG

- 10.12 Panasonic Corporation

- 10.13 Renesas Electronics

- 10.14 Rohm Semiconductor

- 10.15 Samsung Electronics

- 10.16 Sharp Corporation

- 10.17 Sony Corporation

- 10.18 STMicroelectronics

- 10.19 Texas Instruments

- 10.20 Toshiba Corporation