|

市場調査レポート

商品コード

1913450

自律型農業機械市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Autonomous Farm Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 自律型農業機械市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月16日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

概要

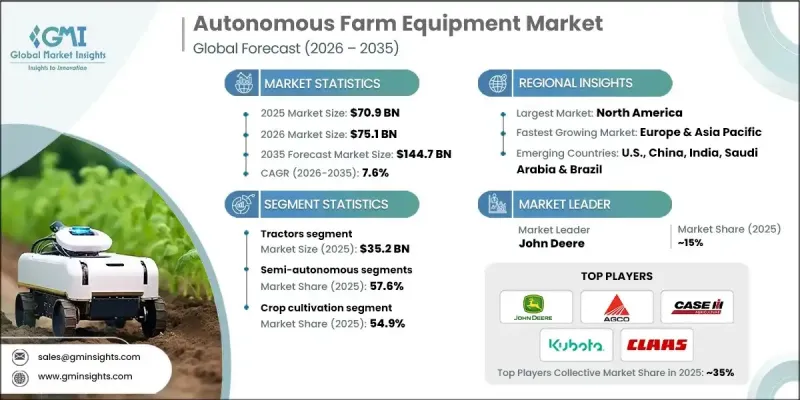

世界の自律型農業機械市場は、2025年に709億米ドルと評価され、2035年までにCAGR 7.6%で成長し、1,447億米ドルに達すると予測されています。

この分野の成長は、精密農業技術の普及拡大によって推進されています。これらの手法により、農家は投入資材の使用を最適化し、資源の浪費を最小限に抑え、作物の生産量を最大化することが可能となります。トラクター、収穫機、ドローンなどの自律型機械により、農家は最も効果的な時期に投入物を施用でき、収益性を向上させながら環境への影響を低減できます。AI、IoT、ロボティクス、マシンビジョンの融合は農業に革命をもたらし、作物のモニタリング、土壌評価、最小限の人為的介入による自動収穫といった高度な作業を可能にしています。5Gやクラウドプラットフォームを含む先進的な通信ネットワークにより、リアルタイム監視と遠隔操作が可能となり、効率性と普及がさらに促進されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 709億米ドル |

| 予測金額 | 1,447億米ドル |

| CAGR | 7.6% |

トラクターセグメントは2025年に352億米ドルを占め、2026年から2035年にかけてCAGR7.4%で成長すると予測されています。トラクターは農業の重要な作業に不可欠であり、AI、GPSナビゲーション、IoT接続の統合により、高効率な半自律型または完全自律型の機械へと進化しています。労働力不足と運用コストの上昇が需要を牽引しており、これらのトラクターは手作業への依存度を低減すると同時に、精度と生産性を向上させます。

半自律型機器セグメントは57.6%のシェアを占め、2026年から2035年にかけてCAGR7.1%で成長すると予測されています。この機器は自動化と人的監視のバランスを提供し、自動操舵や精密制御などの機能を備えつつ、農家が運用上の柔軟性を維持できるようにします。このハイブリッドアプローチは、投資コストや技術的複雑さに関する懸念に対応し、自動化システムの円滑な導入を可能にするとともに、反復作業の効率化を実現します。

米国の自律型農業機器市場は、2025年に185億米ドルと評価され、2026年から2035年にかけてCAGR8.5%で成長すると予測されています。大規模農場と技術的に進んだ農業セクターが自律型ソリューションの導入を推進しています。既存メーカーと新興企業の双方によるAI、ロボティクス、IoTへの多額の投資が導入を加速させております。スマート農業技術と持続可能な実践に対する政府の優遇措置が、市場のさらなる拡大を促進しております。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 精密農業の導入拡大

- 技術的進歩

- 政府の施策と補助金

- 労働力不足とコスト上昇

- 業界の潜在的リスク&課題

- 高い初期投資とコスト障壁

- 接続性とインフラの制約

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 規制情勢

- 規格およびコンプライアンス要件

- 地域別規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:製品別、2022-2035

- トラクター

- 収穫機

- プランター

- 噴霧器

- 無人航空機(UAV)

- その他(耕うん機、灌漑設備)

第6章 市場推計・予測:技術別、2022-2035

- ガイダンスおよびナビゲーションシステム

- センサー技術

- 人工知能(AI)および機械学習

- ロボティクスと自動化

- 接続性と通信システム

第7章 市場推計・予測:事業別、2022-2035

- 完全自律型

- 準自律型

第8章 市場推計・予測:出力別、2022-2035

- 30馬力未満

- 31~100馬力

- 100馬力超

第9章 市場推計・予測:用途別、2022-2035

- 作物栽培

- 園芸・苗木

- 酪農・畜産管理

- 林業および木材管理

第10章 市場推計・予測:流通チャネル別、2022-2035

- 直接販売

- 間接販売

第11章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- インドネシア

- マレーシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第12章 企業プロファイル

- AGCO Corporation

- Agrobot

- Autonomous Solutions Inc.

- Case IH

- Claas

- Dot Technology Corp

- DroneDeploy

- Fendt

- Harvest Automation

- John Deere

- Kinze Manufacturing

- Kubota Corporation

- New Holland Agriculture

- Precision Planting

- Raven Industries