|

市場調査レポート

商品コード

1871314

生分解性ポリマー市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測Biodegradable Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 生分解性ポリマー市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年10月29日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

概要

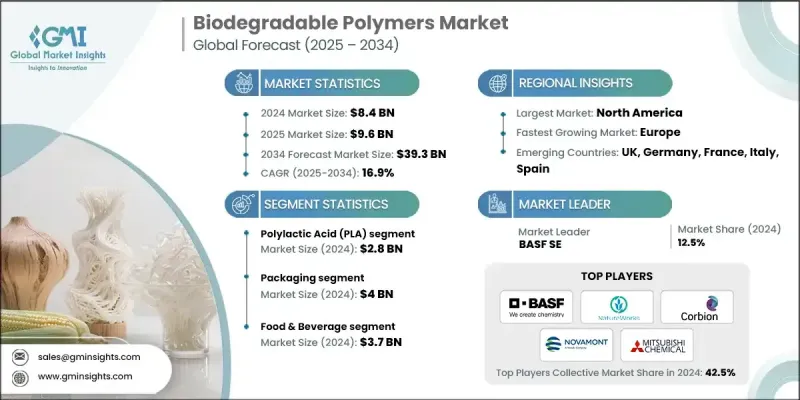

世界の生分解性ポリマー市場は、2024年に84億米ドルと評価され、2034年までにCAGR16.9%で成長し、393億米ドルに達すると予測されています。

生分解性ポリマーとは、微生物、熱、湿気、好気性条件に曝されることで、水、二酸化炭素、バイオマスへと自然に分解される材料です。環境中で数世紀にわたって残存する従来のプラスチックとは異なり、これらのポリマーは再生可能資源由来または合成的に製造された持続可能な代替品を提供します。環境意識の高まりとプラスチック汚染に対する規制強化が、様々な産業分野での採用を促進しています。世界各国の政府は使い捨てプラスチックの使用制限を課し、企業が環境に優しい選択肢へ移行するよう促しています。持続可能な包装材、農業用フィルム、使い捨て製品に対する消費者需要の高まりが、さらなる成長を加速させています。技術進歩により、生分解性ポリマーの性能、加工性、耐久性が向上しています。現在の調査は、強度、柔軟性、熱安定性を向上させつつ、自然分解性を維持するための化学構造の最適化に焦点を当てています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025-2034 |

| 開始時価値 | 84億米ドル |

| 予測金額 | 393億米ドル |

| CAGR | 16.9% |

ポリ乳酸(PLA)は、包装、使い捨て製品、および医療用途での応用により、2024年に28億米ドルの市場規模を占めました。産業規模での堆肥化が可能であり、既存の製造設備との統合が容易であることから、持続可能なソリューションを追求する企業から高い支持を得ています。ポリヒドロキシアルカノエート(PHA)は、優れた生分解性と汎用性により、医療機器および特殊プラスチック市場で注目を集めています。

包装セグメントは、生分解性ポリマーの応用拡大により、2024年に40億米ドルの規模を生み出しました。食品、飲料、小売セクターの企業は、規制要件と消費者の期待に応えるため、従来のプラスチックをPLA、澱粉系フィルム、セルロース製品に置き換える動きを加速させています。このセグメントは、大量使用と目に見える持続可能性のメリットを兼ね備えており、生分解性ポリマー導入において最も商業的に進んだ分野となっています。

米国における生分解性ポリマー市場は、2024年に21億米ドルの規模に達しました。北米地域は、企業と消費者が環境に優しいソリューションを優先する姿勢を継続し、引き続き主導的な立場を維持しております。連邦および州レベルの政策、ならびにプラスチック汚染に対する認識の高まりが、包装、農業、消費財分野における生分解性素材の統合を促進しております。ポリマー科学の進歩によりコスト効率と性能が向上し、環境負荷低減を目指す産業にとって生分解性ポリマーは魅力的な選択肢となっております。これにより北米は、持続可能なポリマーソリューションの革新と広範な採用における中核地域としての地位を確立しております。

世界の生分解性ポリマー市場における主要企業には、BASF SE、ネイチャーワークスLLC、ノバモントS.p.A.、コービオンN.V.、三菱ケミカルグループ、カネカ株式会社、バイオーム・バイオプラスチックス・リミテッド、FKuR Kunststoff GmbH、ブラスケムS.A.、キングファ・サイエンティフィック・アンド・テクノロジー株式会社、バイオオンS.p.A.、プランティック・テクノロジーズ・リミテッド、ジェノマティカ社、マンゴー・マテリアルズ社、フルサイクル・バイオプラスチックス社、RWDCインダストリーズ社、バイオプラスチックス原料連合などが参画しております。&Tech. Co., Ltd.、Bio On S.p.A.、Plantic Technologies Limited、Genomatica Inc.、Mango Materials Inc.、Full Cycle Bioplastics Inc.、RWDC Industries Pte Ltd.、Bioplastics Feedstock Alliance、CJ CheilJedang Corporationなどが挙げられます。生分解性ポリマー市場における各社は、複数の戦略的アプローチを通じて存在感を強化しております。強度、熱安定性、生分解性を向上させた新たなポリマー配合の開発に向け、研究開発に多額の投資を行っております。包装、消費財、農業関連企業との戦略的提携や協業により、市場範囲の拡大とカスタマイズされたソリューションの開発を実現しております。技術力の統合と生産規模の拡大を目的とした合併・買収も推進されております。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 生産技術の進歩

- 包装業界における需要の増加

- 医療および農業分野における利用の増加

- 環境に配慮した製品に対する消費者の嗜好

- 業界の潜在的リスク&課題

- 高い生産コスト

- 性能上の制約

- 市場機会

- 医療・農業分野における拡大

- 技術革新

- 循環型経済モデルの開発

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- ポリマーの種類別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:ポリマータイプ別、2021-2034

- 主要動向

- ポリ乳酸(PLA)

- ポリヒドロキシアルカノエート(PHA)

- ポリブチレンサクシネート(PBS)

- ポリカプロラクトン(PCL)

- 澱粉系ポリマー

- セルロース誘導体

- 新興タイプ

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 包装

- 農業分野

- 医療・ヘルスケア

- 繊維・繊維製品

- 消費財

- その他の用途

第7章 市場推計・予測:最終用途産業別、2021-2034

- 主要動向

- 食品・飲料

- 農業・園芸

- 医療・ヘルスケア

- 自動車

- 電子機器・民生品

- 繊維・アパレル

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- BASF SE

- NatureWorks LLC

- Novamont S.p.A

- Corbion N.V.

- Mitsubishi Chemical Group

- Kaneka Corporation

- Biome Bioplastics Limited

- FKuR Kunststoff GmbH

- Braskem S.A.

- Kingfa Sci. &Tech.Co.,Ltd.

- Bio On S.p.A.

- Plantic Technologies Limited

- Genomatica Inc.

- Mango Materials Inc.

- Full Cycle Bioplastics Inc.

- RWDC Industries Pte Ltd.

- Bioplastics Feedstock Alliance

- CJ CheilJedang Corporation