|

市場調査レポート

商品コード

1849915

生分解性ポリマー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Bio-degradable Polymers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 生分解性ポリマー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月30日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

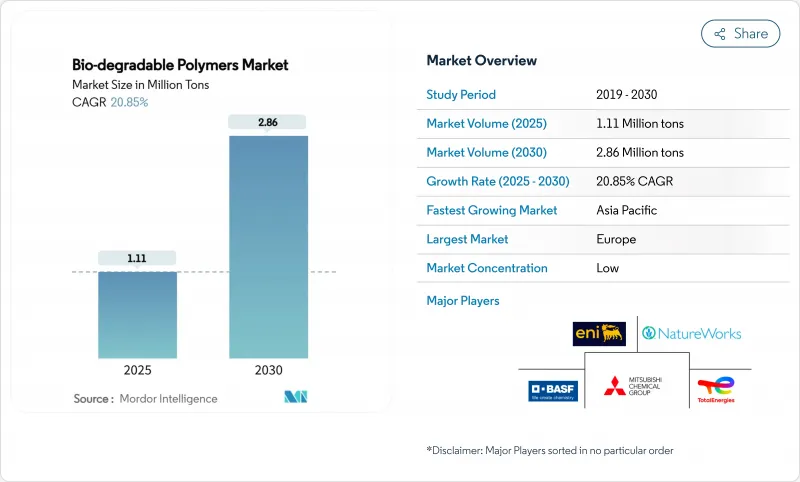

生分解性ポリマー市場規模は2025年に111万トンと推定され、2030年には286万トンに達すると予測され、予測期間(2025-2030年)のCAGRは20.85%です。

規制圧力の高まり、企業の持続可能性目標の拡大、微生物生産技術の急速な進歩により、需要は高性能・低炭素材料へと向かっています。欧州は依然として地域最大の消費国であるが、アジア太平洋は産業のスケールアップと支援的な法規制により最も急速に進歩しています。現在、製品革新の中心は海洋分解性グレードとコスト効率の高いPHAであり、石油化学メジャー、特殊バイオプラスチック企業、新興企業が同時に生産能力と研究開発に投資しているため、競合は激化しています。

世界の生分解性ポリマー市場の動向と洞察

使い捨てプラスチックに対する政府の規制

世界的な規則制定が材料の流れを再編成しています。2024年に最終決定される欧州連合(EU)の包装・包装廃棄物規制は、域内で販売されるすべての包装にリサイクル可能であることを義務付けるとともに、段階的な廃棄物削減目標を設定し、コンバーターを即座にコンポスタブルまたはリサイクル可能な認定グレードに誘導します。2024年4月に導入される英国のプラスチック入りウェットティッシュの禁止は、衛生製品の機会をさらに拡大します。香港の2024年のストローやEPS容器などの使い捨て品目の禁止は、アジアにおける同様の勢いを示しています。これらの措置が相まって、新規ポリマー工場の投資回収期間が短縮され、オフテイク契約が促進され、川下ブランドの採用が促進されています。

持続可能な包装への需要の高まり

ブランドオーナーは現在、持続可能性をコンプライアンス(法令遵守)ではなく、成長の原動力として扱っています。高級食品・飲料メーカーは、PLA、PHA、および使用後の排出量を削減するコート紙構造にシフトしています。ポーツマス大学の研究所の証拠によれば、PLAは従来のPPに比べて、海水と太陽光の暴露下でマイクロプラスチックの排出が9倍少なく、海洋に関心のある消費者の間でブランドの評判が向上しています。リサイクル可能な設計ガイドラインとeコマースの拡大が、フィルム、トレイ、硬質容器の大量需要を生み出しています。

高い生産コスト

設備の償却、特殊原料、控えめな工場規模により、平均販売価格は汎用PEやPPを上回っています。2025年のダニマー・サイエンティフィック社の破産申請は、技術リーダーにとっても収益性の逆風であることを浮き彫りにしています。生産能力の増強とプロセスの強化がコスト削減の原動力になっているとはいえ、多くのコンバーターは大衆市場向けパッケージング・セグメントへの参入をためらっています。

セグメント分析

デンプンベースのグレードは、豊富な原料、既存のブローフィルムや熱成形ラインとの互換性により、生分解性ポリマー市場シェアの41.05%を占めています。PLAは硬質包装と医療機器において確固たる地位を維持しています。PHAの生分解性ポリマー市場規模はCAGR 23.49%で成長すると予測され、その急速な海洋分解プロファイルと微生物発酵収率の向上が後押ししています。PBSやPBATのようなポリエステル系は、クリンプフィルムや衛生用バックシートでシェアを伸ばしており、セルロース系はコーティングや紙コップに使用されています。

コスト・パリティはまだ達成されていないです。スターチブレンドは、農業補助金や配合の簡素化を享受しているが、PHA開発者は、炭素回収クレジットや利益率の高い医療用販売から利益を得ています。ブレンドシステムへの収束が予見され、バランスの取れたコスト・パフォーマンスが実現するかもしれないです。

地域分析

欧州の39.19%のリーダーシップは、政策の明確化と消費者のエコ意識に起因します。2024年に最終決定されたEU規制は、リサイクル可能または堆肥化可能な包装を義務付けており、フィンランドにあるフォータムのCO2-ポリマー・プラントのような画期的なプロジェクトは、炭素回収がバイオベース生産とどのように統合されるかを示しています。

アジア太平洋はCAGR 29.44%で最も急成長している地域です。中国は、国家的なプラスチック禁止期限を守り、農業用フィルムを供給するために、PHAとPBATプラントを増強しています。日本は海洋ブイ用途にジスルフィド結合を組み込んだ海洋分解性PBSを革新。

北米では技術革新と企業の自主目標を両立。ダウとニュー・エナジー・ブルー社との契約では、トウモロコシの茎葉を使用してPE資産用のバイオエチレンを製造し、低炭素ドロップインの道を開きます。南米と中東はまだ発展途上であるが、野焼きを減らすための生分解性マルチに関心を示しています。産業用堆肥化施設の不足は、当面の普及を抑制しているが、長期的なインフラ整備の機会を示唆しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 使い捨てプラスチックの使用に対する政府の規制

- 持続可能で環境に優しい包装への需要の高まり

- ヘルスケア業界における生分解性プラスチックの採用増加

- 農業における生分解性フィルムの使用急増

- 生分解性ポリマーの製造プロセスにおける技術革新の進展とその収率向上

- 市場抑制要因

- 従来のプラスチックに比べて生産コストが高め

- 自動車の消費を制限する機械性能の限界

- 産業用堆肥化施設の不足

- バリューチェーン分析

- 規制の見通し

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- タイプ別

- デンプン系プラスチック

- ポリ乳酸(PLA)

- ポリヒドロキシアルカン酸(PHA)

- ポリエステル(PBS、PBAT、PCL)

- セルロース誘導体

- 原料別

- サトウキビとテンサイ

- トウモロコシおよびその他のデンプン作物

- セルロースと木質バイオマス

- 廃棄植物油脂

- 藻類および微生物バイオマス

- エンドユーザー業界別

- パッケージ

- 消費財

- テキスタイル

- 農業

- ヘルスケア

- その他(自動車、建設など)

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- BASF

- Biome Bioplastics

- BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- Braskem

- CJ CheilJedang Corp

- Danimer Scientific

- DuPont

- Evonik Industries AG

- FKuR

- GENECIS

- Mitsubishi Chemical Group Corporation

- NatureWorks LLC

- Eni S.p.A.(Novamont)

- Plantic

- PTT MCC Biochem Co., Ltd.

- BEWI

- TEIJIN LIMITED

- TORAY INDUSTRIES, INC.

- TotalEnergies(Total Corbion)

- Zhejiang Hisun Biomaterials Co., Ltd.