|

市場調査レポート

商品コード

1844376

サブマージアーク炉の市場機会、成長促進要因、産業動向分析、2025~2034年予測Submerged Arc Furnace Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| サブマージアーク炉の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年09月25日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

概要

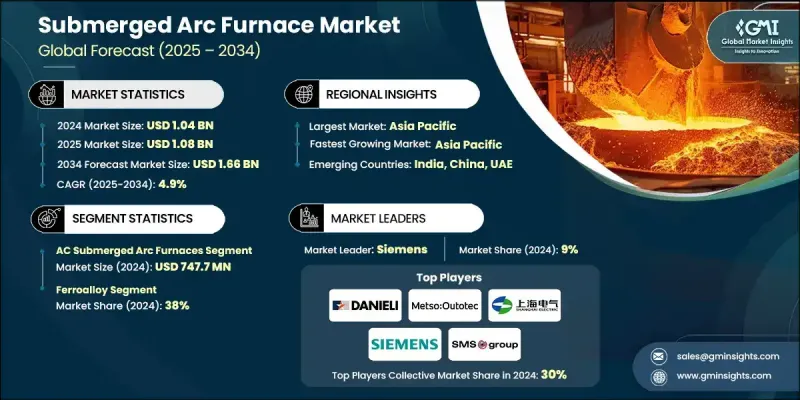

世界のサブマージアーク炉市場は2024年に10億4,000万米ドルと評価され、CAGR 4.9%で成長し、2034年には16億6,000万米ドルに達すると推定されています。

サブマージアーク炉の需要急増は、鉄鋼、合金鉄、シリコン金属生産の世界的な上昇と密接に結びついています。新興国市場で工業化と都市開拓が加速するにつれ、高品位鉄鋼製品へのニーズは激化の一途をたどっています。サブマージド・アーク炉は鉄鋼製造の中心的役割を果たし、特に製鋼工程で重要なインプットとなる合金鉄の生産で重要な役割を果たします。インフラ整備、自動車製造、建設セクターの拡大が、このニーズをさらに高めています。さらに、再生可能エネルギーの推進は、ソーラーパネルや電子機器に使用される金属ケイ素の需要拡大に拍車をかけています。金属ケイ素の生産はエネルギー集約型であるため、最新のSAF設計は効率と生産性の向上に不可欠です。炉技術の革新と相俟って、多方面にわたる用途の増加が市場の上昇軌道に拍車をかけています。鉄鋼とシリコンは世界経済の基盤材料であり続けるため、サブマージアーク炉の採用は拡大し続け、世界中の製造業にとって重要な技術投資となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 10億4,000万米ドル |

| 予測金額 | 16億6,000万米ドル |

| CAGR | 4.9% |

ACサブマージアーク炉セグメントは、2024年に7億4,770万米ドルを生み出し、2034年までCAGR 5.1%で成長すると予測されます。ACサブマージド・アーク炉は、そのコスト効率、成熟した技術基盤、産業現場での使いやすさからトップの座を維持しています。AC-SAFシステムは、操作の信頼性と高温プロセスへの適合性により、シリコンメタルや合金鉄の生産によく選ばれています。AC-SAFシステムは、資本コストを管理しながら安定した結果を提供するため、大規模な工業用として非常に魅力的です。

合金鉄用途セグメントは2024年に38%のシェアを占め、2025年から2034年にかけてCAGR 5%で成長すると予測されています。サブマージアーク炉の全用途の中でも、合金鉄製造が依然として需要の支配的な原動力となっています。フェロシリコン、フェロクロム、フェロマンガンなどの特殊合金は鉄鋼生産に不可欠であり、SAFだけが確実に提供できる一貫した高熱環境を必要とします。高品質な鋼材の生産と冶金精度の必要性は、世界市場全体でこのアプリケーションの需要を押し上げ続けています。

米国のサブマージアーク炉市場は2024年に76%のシェアを占め、2億880万米ドルを生み出しました。同国の主導的地位は、強固な鉄鋼・金属生産基盤に支えられており、設備のアップグレードや技術改善への投資が拡大しています。SAFは、インフラ、輸送、製造などの基幹産業で使用される重要金属の生産に広く導入されています。生産量とエネルギー効率の向上を目指した近代化努力が、SAFの採用拡大にさらに貢献しています。

世界のサブマージアーク炉市場を形成する主要企業には、Shanghai Electric、Outotec Oyj、Tenova、Xi'an Abundance Electric Technology、SMS Group、Thermtronix、Paul Wurth、Thyssenkrupp Industrial、Electrotherm、Siemens、Hatch、Metso Outotec、Primetals Technologies、Danieli、Doshi Technologiesなどがあります。これらの企業は、世界中の主要な工業炉の用途における技術革新と技術統合をリードし続けています。サブマージアーク炉分野の企業は、足跡を維持・拡大するため、エネルギー効率、炉の自動化、デジタル監視を強化する研究開発を優先しています。技術的なアップグレードは、ダウンタイムを最小化し、装置の寿命を延ばすと同時に、高温性能を最適化することに重点を置いています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 鉄鋼、合金鉄、シリコン金属の需要増加

- 環境の持続可能性と規制

- 業界の潜在的リスク&課題

- 高い資本コストと運用コスト

- エネルギー依存と供給リスク

- 機会

- 技術の進歩とデジタル統合

- 高純度金属の需要増加

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品タイプ別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- 貿易統計

- 主要輸入国

- 主要輸出国

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 直流サブマージアーク炉

- ACサブマージアーク炉

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- フェロアロイ

- シリコンメタル

- 溶融アルミナ

- 炭化カルシウム

- 黄リン

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- Danieli

- Doshi Technologies

- Electrotherm

- Hatch

- Metso Outotec

- Outotec Oyj

- Paul Wurth

- Primetals Technologies

- Shanghai Electric

- Siemens

- SMS Group

- Tenova

- Thermtronix

- Thyssenkrupp Industrial

- Xi’an Abundance Electric Technology