|

市場調査レポート

商品コード

1833677

建設機械の市場機会、成長促進要因、産業動向分析、2025~2034年予測Construction Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 建設機械の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年09月08日

発行: Global Market Insights Inc.

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

概要

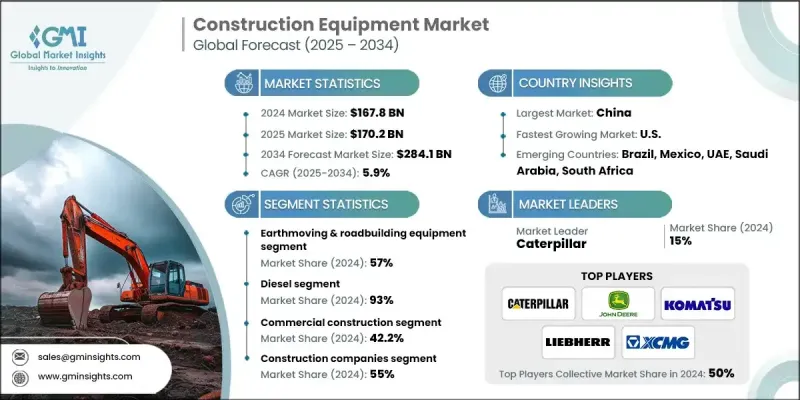

建設機械の世界市場規模は、2024年に1,678億米ドルとなり、CAGR 5.9%で成長し、2034年には2,841億米ドルに達すると予測されています。

成長の原動力は、インフラ開発と都市化の進展です。各国政府は、経済成長を後押しし接続性を向上させるため、道路、橋、空港、鉄道などのインフラに多額の投資を行っています。このような建設の増加により高度な機械が求められ、建設機械の需要が増加しています。AIやIoTなどの技術的進歩を製造機器に統合することで、生産性と安全性が向上し、これらの機器は製造企業にとってより魅力的なものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 1,678億米ドル |

| 予測金額 | 2,841億米ドル |

| CAGR | 5.9% |

民間投資と不動産開発の増加も市場成長に影響を与えると思われます。産業が拡大し、新しい産業が出現するにつれて、小売業、工業、建設工事のニーズが高まる。これにより、掘削機やフォークリフトからクレーンやブルドーザーに至るまで、建設機械の需要が増加します。農業と鉱業における工業化へのシフトは重要であり、これらの産業は効率的であるために特殊な機器を必要とします。

土木・道路建設機械セグメントは2024年に57%のシェアを占め、2025年から2034年にかけてCAGR 5%で成長すると予測されています。このセグメントには、バックホー、掘削機、ローダー、コンパクターなどの機械が含まれ、世界各国政府による公共インフラへの投資の増加や道路開発プロジェクトの迅速な実行により、成長が加速する見通しです。効率的な道路輸送システムと農村部や過疎地域へのより良い接続性に対する需要の急増は、建設機械セクター全体における土木・道路建設機械の優位性を確固たるものにしています。

燃料の種類別では、ディーゼルエンジン搭載機器分野が2024年に93%のシェアを占め、2025年から2034年にかけてCAGR 5%で成長すると予測されています。大手メーカーは、ディーゼル車両にスマート技術を搭載し、性能の向上、ダウンタイムの短縮、燃費の改善を図っています。GPS統合、診断、センサーベースのモニタリングを特徴とする高度なテレマティクス・ソリューションは、モバイル・ネットワークを介してリアルタイムで運転データを収集・送信するために導入されています。これらの技術革新は、機器の使用状況、予知保全、性能の最適化に関する洞察を提供し、オペレーターが現場の生産性を最大化しながら機械の寿命を延ばすのに役立っています。

アジア太平洋建設機械市場は2024年に45.7%のシェアを占める。この地域の拡大は、通信とインフラストラクチャー分野の一貫したアップグレードに支えられています。通信タワーの建設や光ファイバーの普及がクレーンやその他の吊り具の需要を押し上げています。さらに、レンタルモデルは、特に高性能でメンテナンスの少ない機械で、この地域全体で人気を集めています。建設業者は、古い機械を購入するよりも最新の機器をレンタルすることを選ぶようになっており、運用コストを最小限に抑え、建設現場での効率性を高めています。

建設機械業界で事業を展開する主要企業には、テレックス、コマツ、CNHインダストリアル、キャタピラー、XCMG、日立建機、リーヘル、ボルボ、斗山、ディア・アンド・カンパニー、三一などがあります。建設機械主要メーカーは、イノベーション、持続可能性、デジタルトランスフォーメーションを重視し、グローバルな足跡を強化しています。その多くは、テレマティクス、IoT、自動化技術を統合して、機器の性能、安全性、遠隔操作性を高めています。各社は、強化される排ガス規制に対応し、環境に配慮した建設需要に応えるため、ハイブリッドおよび電気製品ラインを拡大しています。テクノロジー企業との戦略的パートナーシップは、スマートな建設慣行をサポートする次世代機械を可能にしています。さらに企業は、アフターマーケット・サービス、部品供給チェーン、グローバル・ディーラー・ネットワークを強化し、顧客体験とサポートを向上させています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- グローバル

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 都市化とインフラ開発

- スマートシティと公共事業への政府投資の増加

- 技術の進歩(自動化、テレマティクス、IoT)

- 電気自動車とハイブリッド車への移行建設機械

- レンタル・リースブーム

- 業界の潜在的リスク&課題

- 高い資本コストと維持費

- 原材料価格の変動

- 熟練オペレーターの不足

- 規制および排出ガス規制の遵守要件

- レンタルや中古機器との激しい競合

- 市場機会

- 電気自動車・ハイブリッド車の導入加速

- 自律建設オペレーションとAI統合

- 精密建設技術とGPSガイダンス

- 機器サービス(EaaS)ビジネスモデル

- レガシー機器の改造・アップグレード市場

- 促進要因

- 成長可能性分析

- 主要な市場動向と混乱

- 将来の市場動向

- 規制情勢

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許分析

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 生産統計

- 生産拠点

- 輸入と輸出

- 主要輸入国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 土木・道路建設機械

- バックホー

- 掘削機

- ローダ

- 圧縮装置

- その他

- マテリアルハンドリングとクレーン

- 保管および取り扱い設備

- エンジニアリングシステム

- 産業用トラック

- バルクマテリアルハンドリング機器

- コンクリート機器

- コンクリートポンプ

- クラッシャー

- トランジットミキサー

- アスファルト舗装機

- バッチングプラント

第6章 市場推計・予測:推進力別、2021-2034

- 主要動向

- ディーゼル

- CNG/LNG

- 電気

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 住宅建設

- 商業建設

- 産業建設

- 鉱業と採石業

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 建設会社

- 鉱山事業者

- レンタル会社

- 政府および地方自治体

- 産業ユーザー

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- グローバルプレーヤー

- Caterpillar

- Komatsu

- John Deere

- Volvo

- Liebherr

- Hitachi

- JCB

- Sany

- Regional Champions

- Case

- New Holland

- Doosan

- Hyundai

- XCMG

- Zoomlion

- Terex

- Manitou

- Wacker Neuson

- 新興プレーヤーとサービスプロバイダー

- United Rentals

- Ashtead Group/Sunbelt Rentals

- H&E Equipment Services

- Home Depot Tool Rental

- Built Robotics

- SafeAI

- Trimble

- Topcon