|

市場調査レポート

商品コード

1871311

骨空隙充填材市場の機会、成長要因、業界動向分析、2025年~2034年の予測Bone Void Fillers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 骨空隙充填材市場の機会、成長要因、業界動向分析、2025年~2034年の予測 |

|

出版日: 2025年10月29日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

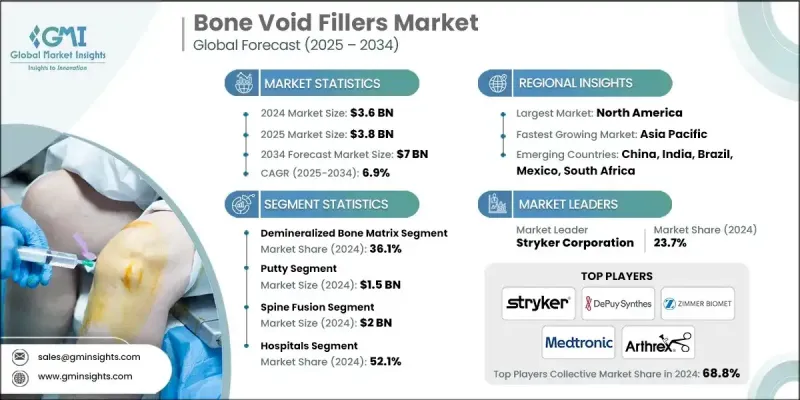

世界の骨空隙充填材市場は、2024年に36億米ドルと評価され、2034年までにCAGR6.9%で成長し、70億米ドルに達すると予測されています。

この市場拡大は、整形外科手術や外傷手術の件数増加、ならびに骨折や骨粗鬆症などの骨関連疾患の有病率上昇に支えられています。主要な動向として、従来の自家移植や同種移植から、リン酸カルシウム、バイオアクティブガラス、複合スキャフォールドなどの合成・生体活性骨空隙充填材への移行が挙げられます。これらの代替品は、予測可能な吸収率、低い感染リスク、優れた生体適合性を提供するため、広範な臨床使用に理想的です。注射可能な骨空隙充填材の需要も増加しています。これらは低侵襲手術を可能にし、手術時間を短縮し、患者の回復を促進するためです。世界的な平均寿命の延伸、都市化、変性性骨疾患や外傷関連損傷の発生率増加が、特に先進国と新興国双方において、市場のさらなる成長を牽引しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025年~2034年 |

| 開始時価値 | 36億米ドル |

| 予測金額 | 70億米ドル |

| CAGR | 6.9% |

脱灰骨マトリックス(DBM)セグメントは、2024年に36.1%のシェアを占め、2025年から2034年にかけてCAGR 6.1%で成長すると予測されています。DBMは、高い骨誘導能、生体適合性、臨床応用における汎用性から高く評価されています。加工された同種移植骨由来のDBMは、コラーゲン、骨形成タンパク質、成長因子などの主要な有機成分を保持しており、これらが新たな骨形成と効果的な移植片の統合を促進します。パテ、ペースト、ゲル、ストリップなど複数の投与形態で提供されるため、整形外科、外傷、脊椎固定術において外科医に柔軟性を提供します。

パテセグメントは2024年に15億米ドルの市場規模を記録し、2034年までCAGR7.2%で拡大が見込まれます。外科医がパテを好む理由は、その粘着性と成形性に優れ、不規則または複雑な骨欠損部への精密な充填を可能とする点にあります。優れた操作性と適応性により、脊椎固定術、頭蓋顔面再建術、整形外科的外傷、歯科手術への応用が理想的です。

北米の骨空隙充填材市場は2024年に48.9%のシェアを占めました。同地域は先進的な医療インフラ、高い手術件数、低侵襲ソリューションや革新的な骨移植代替材を提供する主要企業の存在といった利点を有しています。生体活性型・注射可能な充填材の早期導入に加え、研究開発および臨床試験への多大な投資が、北米のこの分野における主導的地位を強化しています。

世界の骨空隙充填材市場で事業を展開する主要企業には、アーチレックス、バイオベンタス、メドライン、メドトロニック、アビリックス、ストライカー、バクスター・インターナショナル、デピュイ・シンセシス(ジョンソン・エンド・ジョンソン)、ボーンサポート、アキュメッド、ジマー・バイオメットなどが挙げられます。骨空隙充填材市場の企業は、戦略的取り組みを通じて存在感を高めています。優れた骨誘導能、吸収率、生体適合性を備えた先進的な生体材料を導入するため、研究開発への投資を進めております。病院、外科センター、流通業者との提携や協力関係は、市場へのリーチ拡大と革新的な製品の採用促進に寄与しております。技術力の強化と生産規模の拡大には、合併や買収が活用されております。また、信頼性向上のため、規制当局の承認、製品認証、臨床試験にも注力しております。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 骨疾患および損傷の発生率の増加

- 高齢人口の増加

- 外科手術技術の進歩

- 増加する整形外科手術

- 業界の潜在的リスク&課題

- 骨疾患に関連する高コスト

- 厳格な規制環境

- 市場機会

- 低侵襲・注射可能なソリューションへの移行

- 生体活性および抗生物質放出型フィラーの進歩

- 促進要因

- 成長可能性分析

- 技術情勢

- 現在の技術動向

- 新興技術

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- 将来の市場動向

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携および協力関係

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:材料タイプ別、2021年~2034年

- 主要動向

- 脱灰骨マトリックス

- 硫酸カルシウム

- コラーゲンマトリックス

- リン酸三カルシウム/リン酸カルシウム系

- その他の材料タイプ

第6章 市場推計・予測:形態別、2021年~2034年

- 主要動向

- ゲル

- 顆粒

- ペースト/注射剤

- パテ

- その他の形態

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 脊椎固定術

- 骨折

- 関節再建

- 歯科/頭蓋顎顔面外科(CMF)

- その他の用途

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 専門クリニック

- 外来手術センター

- その他の最終用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Abyrx

- Acumed

- Arthrex

- Baxter International

- Bioventus

- Bonesupport

- DePuy Synthes(Johnson &Johnson)

- Medline

- Medtronic

- Stryker

- Zimmer Biomet