レーザー加工装置の市場機会、成長促進要因、産業動向分析と2025年~2034年予測

Laser Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 155 Pages

- 納期

- 2~3営業日

- 商品コード

- 1844384

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

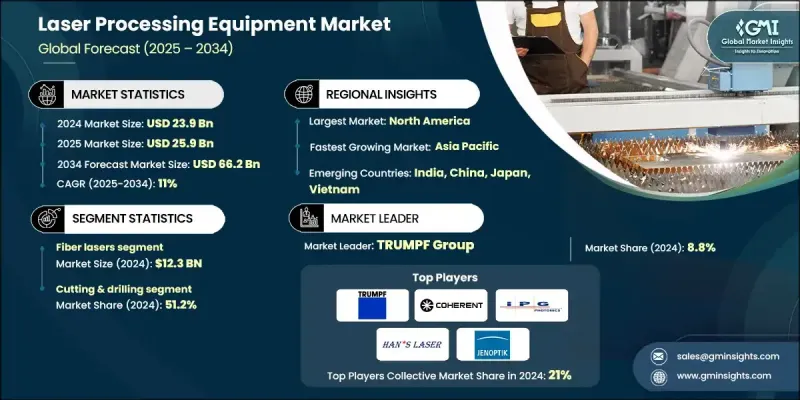

世界のレーザー加工装置市場は、2024年に239億米ドルと評価され、CAGR 11%で成長し、2034年には662億米ドルに達すると予測されています。

AI、IoT、フルスケールの自動化を含むインダストリー4.0イノベーションの急速な統合は、産業製造業を再構築し、高度なレーザ加工ソリューションの採用を加速しています。ファイバーレーザは、そのエネルギー効率、運用コストの削減、厳しい環境下での高い信頼性により、勢いを増し続けています。レーザベースの積層造形技術の利用の増加は、産業界がより迅速なプロトタイピングとより大きな設計の柔軟性を求めているため、市場成長をさらに促進しています。超高速・高出力レーザは、精度とカスタマイズが不可欠な航空宇宙や医療などの重要分野でも不可欠になっています。持続可能な製造方法に対する需要の高まりとともに、精度に対する期待の高まりが継続的な研究開発を促進しています。業界の拡大は、マイクロマシニング、彫刻、穴あけ、構造切断など、精密な非接触加工から恩恵を受ける拡張可能なアプリケーションによって支えられています。こうした使用事例の進化は、有利なコスト・パフォーマンス比や産業基盤の拡大と相まって、今後も世界市場のダイナミクスを形成していくと思われます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 239億米ドル |

| 予測金額 | 662億米ドル |

| CAGR | 11% |

ファイバレーザカテゴリセグメントは、優れたエネルギー変換効率と低メンテナンス要件によって、2024年に123億米ドルを生み出しました。ファイバーレーザの安定したビーム品質は、詳細な加工を可能にします。エネルギー消費の削減は運用コストの削減につながり、ファイバーレーザはコスト意識の高い産業界に好まれる選択肢となっています。その最小限の材料廃棄出力と精度に焦点を当てた性能は、世界の製造現場で導入されつつあるより厳格な生産および持続可能性基準に適合しています。ファイバーレーザの信頼性と寿命の継続的な改善は、その採用率をさらに高めています。

切断と穴あけセグメントは、2024年に51.2%のシェアを占め、複雑な成形と精密な材料除去のニーズがその原動力となっています。レーザー加工は、材料の無駄を最小限に抑え、リーン生産モデルをサポートし、コスト効率を改善することが認められています。金属、プラスチック、セラミック、複合材料のマテリアルハンドリングにおけるその適応性により、レーザー加工は複数の業種にまたがる重要なツールとなっています。自動車組立ラインから医療機器製造に至るまで、複雑な加工を正確に行う能力により、レーザー切断と穴あけは現代の産業ワークフローにおける標準工程として確固たる地位を築いています。

米国のレーザー加工装置市場は65%を占め、2024年には35億米ドルを生み出します。同国のイノベーションに焦点を当てたエコシステムは、高度な製造インフラと相まって、製品開発と普及を支え続けています。航空宇宙、エレクトロニクス、自動車、ヘルスケアなど多様な産業が、次世代レーザー技術への一貫した投資を促進しています。国内における強力な研究開発イニシアティブと、世界的な製造業のリーダーの存在が、この地域における日本の優位性をさらに強化しています。

世界のレーザー加工装置市場を形成している著名企業には、IPG Photonics、TRUMPF、Hans Group、Control Micro Systems、Vermont、Newport、Coherent、Rofin-Sinar Technologies、Lumibird、Universal Laser Systems、Eurolaser、Laser Systems、Concept Laser、Jenoptik、Hgtechなどがあります。レーザー加工装置市場の企業は、技術革新、効率性、分野別ソリューションに注力することで、グローバルな足跡を強化しています。多くの企業が研究開発に多額の投資を行い、精密産業向けのコンパクトで高出力なレーザシステムを開発しています。カスタマイズとモジュール化された装置設計により、メーカーは医療、航空宇宙、エレクトロニクス分野のニッチアプリケーションに対応しています。OEMや産業用オートメーションプロバイダーとの戦略的提携により、その技術範囲は拡大しています。また、持続可能な製造業に対する需要の高まりに対応するため、環境に優しいオペレーションを重視しながら生産能力を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- レーザー技術の進歩

- 高品質・精密製造の需要の高まり

- 積層造形(3Dプリンティング)の採用増加

- 業界の潜在的リスク&課題

- 初期投資額が高め

- 運用コストの増加

- 機会

- (EV)とバッテリー製造

- 半導体およびマイクロエレクトロニクス製造

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 技術タイプ別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- 貿易統計(HSコード:84561000)

- 主要輸入国

- 主要輸出国

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:技術種別、2021-2034

- 主要動向

- ファイバーレーザー

- 二酸化炭素

- ソリッドステート

- その他

第6章 市場推計・予測:プロセスタイプ別、2021-2034

- 主要動向

- 切断と穴あけ

- 溶接

- マーキングと彫刻

- パンチング&マイクロマシニング

- その他

第7章 市場推計・予測:材質別、2021-2034

- 主要動向

- 鋼鉄

- アルミニウム

- 銅

- プラスチックとポリマー

- セラミックス

- その他(ガラス、複合材料、半導体など)

第8章 市場推計・予測:機能タイプ別、2021-2034

- 主要動向

- 半自動

- 自動

第9章 市場推計・予測:統合レベル別、2021-2034

- 主要動向

- スタンドアロンシステム

- 統合生産ライン

- モジュラーシステム

- ポータブル/デスクトップユニット

第10章 市場推計・予測:レーザー光源の種類別、2021-2034

- 主要動向

- ダイオードレーザー

- ディスクレーザー

- エキシマレーザー

- その他(超高速レーザー、ツリウム)

第11章 市場推計・予測:冷却機構別、2021-2034

- 主要動向

- 空冷式

- 水冷式

- ハイブリッド冷却

第12章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 自動車

- 金属および加工

- エレクトロニクス

- エネルギーと電力

- その他

第13章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第14章 企業プロファイル

- Coherent

- Concept Laser

- Control Micro Systems

- Eurolaser

- Hans Group

- Hgtech

- IPG Photonics

- Jenoptik

- Laser Systems

- Lumibird

- Newport

- Rofin-Sinar Technologies

- TRUMPF

- Universal Laser Systems

- Vermont

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 155 Pages

- 納期

- 2~3営業日