|

市場調査レポート

商品コード

1755334

自動車用音声認識市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)Automotive Voice Recognition Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用音声認識市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年) |

|

出版日: 2025年05月21日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

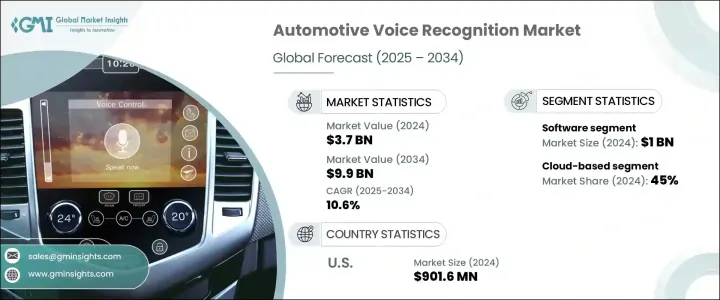

世界の自動車用音声認識市場は、2024年には37億米ドルと評価され、CAGR 10.6%で成長し、2034年には99億米ドルに達すると予測されています。

これらのシステムはドライバーの注意散漫を減らし、路上での安全遵守を向上させます。より多くの自動車メーカーがコネクテッドカーの提供に努める中、音声認識技術に対する需要は高まり続けています。これらのシステムをグーグル・アシスタントやアレクサといった人気のデジタル・アシスタントと統合することで、大きな魅力と機能性が加わり、ユーザーはインフォテインメントや空調設定、さらには車両診断など、自動車のさまざまな機能をコントロールできるようになります。

5Gとクラウド・コンピューティング技術の成長は、より高度な音声認識機能に対する需要をさらに押し上げています。5Gの低遅延と高帯域幅を利用したリアルタイムの音声処理により、自動車の音声アシスタントは即座に応答できるようになり、より豊かなユーザー体験が可能になりました。これらの進歩は、自動車に新たな機能やサービスを提供し、デジタルインターフェースを強化し、機能を拡張します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025~2034年 |

| 当初の市場規模 | 37億米ドル |

| 市場規模予測 | 99億米ドル |

| CAGR | 10.6% |

ソフトウェア分野の2024年の市場規模は10億米ドルでした。このセグメントの重要性は、音声認識システム、特に音声テキスト化、自然言語処理、コマンド処理などの分野におけるソフトウェアの中核的な役割にあります。AIと機械学習によって強化されたソフトウェア開発は、システムの精度とパーソナライゼーションの継続的な改善を可能にし、これらのシステムを様々な言語、ドライバーの嗜好、車両プラットフォームへの適応性を高めます。

クラウドベースのセグメントは2024年に45%のシェアを占めました。クラウドベースのシステムは、物理的な車両リコールなしで音声認識プログラムのシームレスなアップデートを可能にし、技術の最新性と競争力を維持します。また、これらのシステムは、他のデジタルアシスタントやスマートデバイスと統合することができ、複数のプラットフォームでより接続された体験をユーザーに提供します。クラウドシステムはリアルタイムの学習をサポートし、国際的な運用が可能で、自動車用音声認識市場における拡張性と汎用性を高めています。

米国の自動車用音声認識市場は2024年に9億160万米ドルに達します。米国は、高度な音声認識システムと統合された高級車やハイエンド車の採用でリードしています。米国の消費者は、個人の安全性と利便性に大きな価値を置いており、こうしたシステムの需要をさらに促進しています。さらに、自動車市場が確立され発展している米国は、コネクテッドカー技術に多額の投資を続けており、同国が音声認識分野の主要プレーヤーであり続けることを確実にしています。

自動車用音声認識世界市場の主要プレーヤーには、アイシン精機、アリババ・グループ、アマゾン、百度、ボッシュ、セレンス、コンチネンタル、グーグル、ハーマンインターナショナル、マイクロソフトなどが含まれます。競争力を維持するため、自動車用音声認識市場の各社は人工知能と機械学習を組み込んだ高度なソフトウェアの開発にますます注力しており、より優れた音声コマンド認識とよりパーソナライズされたユーザー体験を可能にしています。また、音声認識システムをデジタル・アシスタントやその他の車載テクノロジーと統合しようとするため、自動車メーカーやハイテク大手との提携も一般的な戦略となりつつあります。企業は、リアルタイム処理の限界を押し広げ、待ち時間を短縮し、音声制御システムの機能を向上させるために、研究開発に多額の投資を行っています。

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 自動車メーカー

- ティア1サプライヤー

- 音声AI/ソフトウェアプロバイダー

- クラウドインフラストラクチャプロバイダー

- ハードウェアプロバイダー

- 最終用途

- 利益率分析

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 音声認識の統計データ

- 採用率

- 使用パターン

- 顧客の好み

- コスト内訳分析

- 価格動向

- 地域別

- ハードウェア別

- 影響要因

- 促進要因

- コネクテッドカーの需要増加

- 車載インフォテインメントに対する消費者の嗜好

- クラウドコンピューティングと5Gの成長

- 強化された促進要因安全規制

- 業界の潜在的リスクと課題

- 高い導入コスト

- レガシーシステムとの複雑な統合

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニング・マトリックス

- 戦略的展望マトリックス

第5章 市場の推定・予測:コンポーネント別(2021~2034年)

- 主要動向

- ハードウェア

- マイク

- 電子制御ユニット(ECU)

- インフォテインメントヘッドユニット(HMI)

- 接続ハードウェア

- その他

- ソフトウェア

- 自動音声認識(ASR)

- 自然言語理解(NLU)

- テキスト音声変換(TTS)

- 音声アシスタントプラットフォーム(カスタム/サードパーティ)

- その他

- サービス

- OTAアップデート(無線経由)

- サードパーティアプリの統合

- 多言語サポートサービス

- その他

第6章 市場の推定・予測:展開方式別(2021~2034年)

- 主要動向

- 埋め込み型

- クラウドベース

- ハイブリッド

第7章 市場の推定・予測:車両別(2021~2034年)

- 主要動向

- 内燃機関車(ICE)

- 電気自動車(EV)

第8章 市場の推定・予測:用途別(2021~2034年)

- 主要動向

- ナビゲーション

- 温度調整

- インフォテインメント

- 車両管理

- 安全機能

- その他

第9章 市場の推定・予測:販売チャネル別(2021~2034年)

- 主要動向

- OEM

- アフターマーケット

第10章 市場の推定・予測:地域別(2021~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Aisin Seiki

- Alibaba Group

- Amazon

- Baidu Inc.

- Bosch

- Cerence

- Continental

- Emagine

- Harman International

- iNAGO

- Kardome

- Microsoft

- Nextgen Technologies

- Nissan

- Qualcomm Technologies

- Sensory

- SoundHound

- Speak With Me

- Visteon

The Global Automotive Voice Recognition Market was valued at USD 3.7 billion in 2024 and is estimated to grow at a CAGR of 10.6% to reach USD 9.9 billion by 2034, driven by the rapid adoption of advanced voice-controlled systems as more vehicles incorporate smart technology designed to enhance driving safety and convenience. These systems reduce driver distractions, improving safety compliance on the road. As more automakers strive to offer connected vehicles, the demand for voice recognition technology continues to rise. Integrating these systems with popular digital assistants, such as Google Assistant and Alexa, adds significant appeal and functionality, enabling users to control various car features, such as infotainment, climate settings, and even vehicle diagnostics.

The growth of 5G and cloud computing technologies has further propelled the demand for more sophisticated voice recognition capabilities. With real-time audio processing powered by 5G's low latency and high bandwidth, voice assistants in cars can now respond instantly, enabling a richer user experience. These advancements provide cars with new features and services, enhancing their digital interfaces and expanding their functions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $9.9 Billion |

| CAGR | 10.6% |

The software segment was valued at USD 1 billion in 2024. This segment's importance lies in the core role of software in voice recognition systems, particularly in areas like speech-to-text, natural language processing, and command processing. Software development, enhanced by AI and machine learning, allows for continuous improvements in system accuracy and personalization, making these systems more adaptable to various languages, driver preferences, and vehicle platforms.

The cloud-based segment held a 45% share in 2024. Cloud-based systems enable seamless updates to voice recognition programs without the need for physical vehicle recalls, ensuring that the technology remains up-to-date and competitive. These systems can also integrate with other digital assistants and smart devices, offering users a more connected experience across multiple platforms. Cloud systems support real-time learning and can operate globally, boosting their scalability and versatility in the automotive voice recognition market.

United States Automotive Voice Recognition Market reached USD 901.6 million in 2024. The U.S. leads in adopting luxury and high-end vehicles integrated with advanced voice recognition systems. Consumers in the U.S. place significant value on personal safety and convenience, further driving demand for these systems. Moreover, with an established and well-developed automotive market, the U.S. continues to make substantial investments in connected car technology, ensuring that the country remains a leading player in the voice recognition space.

Key players in the Global Automotive Voice Recognition Market include Aisin Seiki, Alibaba Group, Amazon, Baidu, Bosch, Cerence, Continental, Google, Harman International, and Microsoft. To maintain a competitive edge, companies in the automotive voice recognition market are increasingly focusing on developing advanced software that incorporates artificial intelligence and machine learning, allowing for better voice command recognition and more personalized user experiences. Partnerships with automakers and tech giants are also becoming a common strategy, as companies look to integrate their voice recognition systems with digital assistants and other in-car technologies. Companies are investing heavily in research and development to push the boundaries of real-time processing, reducing latency and improving the functionality of voice-controlled systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Automotive manufacturers

- 3.2.2 Tier 1 suppliers

- 3.2.3 Voice AI/software providers

- 3.2.4 Cloud infrastructure providers

- 3.2.5 Hardware providers

- 3.2.6 End use

- 3.3 Profit margin analysis

- 3.4 Patent analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Voice recognition statistics

- 3.7.1 Adoption rates

- 3.7.2 Usage patterns

- 3.7.3 Customer preferences

- 3.8 Cost breakdown analysis

- 3.9 Price trend

- 3.9.1 Region

- 3.9.2 Hardware

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing demand for connected cars

- 3.10.1.2 Consumer preference for in-car infotainment

- 3.10.1.3 Growth in cloud computing and 5G

- 3.10.1.4 Enhanced driver safety regulations

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High implementation costs

- 3.10.2.2 Complex integration with legacy systems

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Microphones

- 5.2.2 Electronic control units (ECUs)

- 5.2.3 Infotainment head unit / (HMI)

- 5.2.4 Connectivity hardware

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Automatic speech recognition (ASR)

- 5.3.2 Natural language understanding (NLU)

- 5.3.3 Text-to-speech (TTS)

- 5.3.4 Voice assistant platforms (custom or third-party)

- 5.3.5 Others

- 5.4 Services

- 5.4.1 OTA updates (Over-the-Air)

- 5.4.2 Third-party app integrations

- 5.4.3 Multilingual support services

- 5.4.4 Others

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Embedded

- 6.3 Cloud-based

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Navigation

- 8.3 Climate control

- 8.4 Infotainment

- 8.5 Vehicle management

- 8.6 Safety features

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aisin Seiki

- 11.2 Alibaba Group

- 11.3 Amazon

- 11.4 Baidu Inc.

- 11.5 Bosch

- 11.6 Cerence

- 11.7 Continental

- 11.8 Emagine

- 11.9 Google

- 11.10 Harman International

- 11.11 iNAGO

- 11.12 Kardome

- 11.13 Microsoft

- 11.14 Nextgen Technologies

- 11.15 Nissan

- 11.16 Qualcomm Technologies

- 11.17 Sensory

- 11.18 SoundHound

- 11.19 Speak With Me

- 11.20 Visteon