|

市場調査レポート

商品コード

1740965

構造心臓デバイスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Structural Heart Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 構造心臓デバイスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月25日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

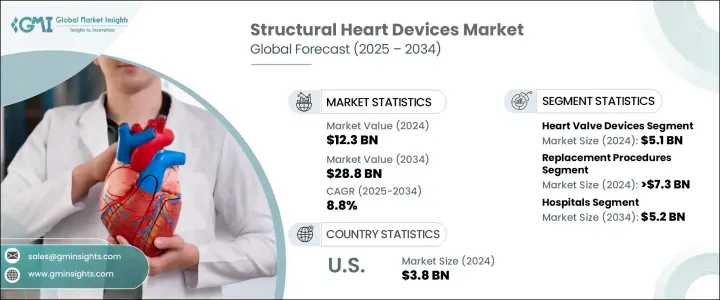

世界の構造心臓デバイス市場は、2024年に123億米ドルと評価され、CAGR 8.8%で成長し、2034年には288億米ドルに達すると推定されています。

この一貫した成長は、心血管疾患の罹患率の増加、ヘルスケアサービスへのアクセス拡大、低侵襲治療技術の広範な採用によって促進されています。世界的に高齢化が進むにつれ、高血圧や糖尿病などの慢性的な健康状態が蔓延し、心臓の構造的障害と診断される患者数の増加に直接的に寄与しています。特に、弁関連の問題、先天性心疾患、心臓の構造に影響を及ぼす疾患が頻発するようになり、高度な治療ソリューションに対する需要が高まっています。さらに、認知度の向上、早期診断、技術の進歩により、心臓血管分野の患者ケアは大きく変化しています。

2023年には、世界市場は113億米ドルに達し、上昇軌道を反映しています。製品タイプの中では、心臓弁装置が2024年に最も高い収益を上げ、51億米ドルと評価されました。この成長は、開心術の必要性を最小限に抑えながら適切な心臓弁機能を回復させるよう設計された、最新の耐久性のあるデバイスの使用が増加していることに起因しています。その他の主な製品分野には、環状形成リング、オクルーダー、送達システム、構造的介入を可能にする様々な支援技術などがあります。これらのツールの安全性と有効性を高める技術革新が進むにつれて、臨床医は個々の患者のニーズに合わせて治療をカスタマイズするための選択肢を増やしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 123億米ドル |

| 予測金額 | 288億米ドル |

| CAGR | 8.8% |

心筋症や弁膜症などの心臓の構造的疾患は、迅速かつ効率的な管理を必要とするため、機器の性能や手技の技術的強化が重視されています。低侵襲的アプローチの開発は、特に回復時間と入院期間を短縮する経カテーテル弁置換術のような手技に大きな変革をもたらしました。これらの方法がより洗練されるにつれて、患者の転帰は改善され、合併症は減少しており、ヘルスケアシステム全体でより多くの採用が推進されています。最先端の素材、リアルタイムの画像処理機能、より人間工学に基づいた設計の統合も、複雑なインターベンション中の医師の精度を高め、より良い治療結果を可能にしています。

手技の観点からは、市場は修理手技と交換手技に区分されます。2024年には、置換術がセグメントを支配し、73億米ドル以上の売上を占める。置換術への嗜好の高まりは、精度の向上と手技リスクの軽減を提供する非外科的手技やロボット支援手技の進歩に起因しています。このような改良は、患者の長期的な耐久性と生活の質の向上を優先する治療への治療パラダイムのシフトを支えています。置換術はまた、その有効性を検証する臨床研究や実世界のデータからも恩恵を受け、ヘルスケア提供者の間でより広範な使用が奨励されています。

最終用途では、2024年に病院が構造心臓デバイスの最大の消費者に浮上し、予測期間終了までに52億米ドルを生み出すと予測されています。病院は熟練した人材、最新の心臓病ユニット、診断能力を備えており、大量の心臓血管処置を扱うことができます。構造的な心臓治療の複雑化に伴い、病院は最先端のツールやシステムを用いて包括的な治療を提供する上で中心的な役割を果たし続けています。また、病院は紹介や術後ケアの主要拠点でもあり、市場での地位をさらに強化しています。

米国は2024年に38億米ドルの市場収益を占め、2025年から2034年にかけてCAGR 7.7%で成長すると予想されています。同国の優位性は、高度なヘルスケアインフラ、斬新な医療技術の早期導入、構造的介入に対する有利な償還政策に大きく支えられています。特に高齢者における心臓弁膜症患者の増加が、侵襲性の低い弁置換療法への需要を高めています。加えて、主要市場プレイヤーの存在感が強く、デバイス設計や手技ワークフローにおける技術革新が進んでいることも、引き続き国内市場の成長を後押ししています。

世界の構造心臓デバイス市場は競争が激しいのが特徴で、大手5社が市場シェア全体の約75%を占めています。これらの大手企業は、製品性能を向上させ、複雑なインターベンションを簡素化するための研究開発に継続的に投資しています。リアルタイムの視覚化の強化から手術ワークフローの合理化まで、メーカーは治療結果を最適化し臨床生産性を高める直感的で効率的、かつ患者に優しいソリューションで医師をサポートすることに注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 心血管疾患の負担増大

- 技術的進歩

- 有利な償還シナリオ

- 低侵襲手術への関心の高まり

- 業界の潜在的リスク&課題

- 厳格な規制政策

- 潜在的な合併症および有害事象

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 償還シナリオ

- 価格分析、 2024

- テクノロジーの情勢

- 将来の市場動向

- ポーター分析

- GAP分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 心臓弁デバイス

- 外科用心臓弁

- 経カテーテル心臓弁

- 環状形成リング

- 閉塞器具および送達システム

- その他の製品

第6章 市場推計・予測:手順別、2021-2034

- 主要動向

- 交換手順

- 外科的大動脈弁置換術(SAVR)

- 経カテーテル大動脈弁置換術(TAVR)

- 経カテーテル僧帽弁置換術(TMVR)

- その他の交換手順

- 修理手順

- 左心耳閉鎖(LAAC)

- 経カテーテル僧帽弁修復術(TMVr)

- 経カテーテル三尖弁修復術(TTVr)

- 弁形成術

- その他の修理手順

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

- 心臓カテーテル検査室

- その他の用途

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott

- AtriCure

- BIOMERICS

- Boston Scientific

- BRAILE

- CryoLife

- Edwards

- JENAVALVE

- LEPU MEDICAL

- LivaNova

- Medtronic

- NUMED

The Global Structural Heart Devices Market was valued at USD 12.3 billion in 2024 and is estimated to grow at a CAGR of 8.8% to reach USD 28.8 billion by 2034. This consistent growth is fueled by the increasing incidence of cardiovascular diseases, expanding access to healthcare services, and the widespread adoption of minimally invasive treatment techniques. As aging populations rise globally, chronic health conditions such as hypertension and diabetes become more prevalent, directly contributing to the increasing number of patients diagnosed with structural heart disorders. In particular, valve-related issues, congenital heart defects, and conditions impacting the heart's structure are becoming more frequent, intensifying the demand for advanced treatment solutions. Moreover, greater awareness, early diagnosis, and technological advances have significantly transformed patient care in the cardiovascular segment.

In 2023, the global market stood at USD 11.3 billion, reflecting its upward trajectory. Among the product types, heart valve devices generated the highest revenue in 2024, valued at USD 5.1 billion. This growth can be attributed to the increasing use of modern, durable devices designed to restore proper heart valve function while minimizing the need for open-heart surgery. Other key product segments include annuloplasty rings, occluders, and delivery systems, along with various supportive technologies that enable structural interventions. As innovation continues to enhance the safety and effectiveness of these tools, clinicians have more options for customizing treatment to individual patient needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.3 Billion |

| Forecast Value | $28.8 Billion |

| CAGR | 8.8% |

Structural heart conditions such as cardiomyopathies and valve diseases demand immediate and efficient management, which has led to a strong emphasis on technological enhancements in device performance and procedural techniques. The development of minimally invasive approaches has had a transformative effect, especially with procedures such as transcatheter valve replacements that reduce recovery time and hospital stays. As these methods become more refined, patient outcomes are improving and complications are decreasing, driving greater adoption across healthcare systems. The integration of cutting-edge materials, real-time imaging capabilities, and more ergonomic designs have also elevated physician accuracy during complex interventions, allowing for better therapeutic results.

From a procedural standpoint, the market is segmented into repair and replacement procedures. Replacement procedures dominated the segment in 2024, accounting for more than USD 7.3 billion in revenue. The increasing preference for replacement methods stems from ongoing advances in non-surgical and robotic-assisted techniques that offer enhanced precision and reduced procedural risks. These improvements have supported a shift in treatment paradigms toward therapies that prioritize long-term durability and improved quality of life for patients. Replacement procedures also benefit from clinical studies and real-world data that validate their effectiveness, encouraging broader use among healthcare providers.

In terms of end use, hospitals emerged as the largest consumers of structural heart devices in 2024 and are projected to generate USD 5.2 billion by the end of the forecast period. Hospitals are well-equipped with skilled personnel, modern cardiac units, and diagnostic capabilities, enabling them to handle high volumes of cardiovascular procedures. With the increasing complexity of structural heart treatments, hospitals continue to play a central role in delivering comprehensive care using state-of-the-art tools and systems. They are also the primary hubs for referrals and post-surgical care, further strengthening their position in the market.

The United States accounted for USD 3.8 billion in market revenue in 2024 and is expected to grow at a CAGR of 7.7% between 2025 and 2034. The country's dominance is largely supported by its advanced healthcare infrastructure, early adoption of novel medical technologies, and favorable reimbursement policies for structural interventions. Rising cases of heart valve disorders, especially among older adults, are increasing the demand for less invasive valve replacement therapies. Additionally, the strong presence of key market players and ongoing innovation in device design and procedural workflows continue to drive market growth across the country.

The global structural heart devices market is characterized by high competition, with five major companies holding approximately 75% of the total market share. These leading firms are continuously investing in research and development to improve product performance and simplify complex interventions. From enhancing real-time visualization to streamlining surgical workflows, manufacturers are focused on supporting physicians with intuitive, efficient, and patient-friendly solutions that optimize outcomes and boost clinical productivity.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing burden of cardiovascular diseases

- 3.2.1.2 Technological advancements

- 3.2.1.3 Favorable reimbursement scenario

- 3.2.1.4 Rising preference for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory policies

- 3.2.2.2 Potential complications and adverse events

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Reimbursement scenario

- 3.7 Pricing analysis, 2024

- 3.8 Technology landscape

- 3.9 Future market trends

- 3.10 Porter's analysis

- 3.11 GAP analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Company market share analysis

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Heart valve devices

- 5.2.1 Surgical heart valves

- 5.2.2 Transcatheter heart valves

- 5.3 Annuloplasty rings

- 5.4 Occluders and delivery systems

- 5.5 Other products

Chapter 6 Market Estimates and Forecast, By Procedure, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Replacement procedures

- 6.2.1 Surgical aortic valve replacement (SAVR)

- 6.2.2 Transcatheter aortic valve replacement (TAVR)

- 6.2.3 Transcatheter mitral valve replacement (TMVR)

- 6.2.4 Other replacement procedures

- 6.3 Repair procedures

- 6.3.1 Left atrial appendage closure (LAAC)

- 6.3.2 Transcatheter mitral valve repair (TMVr)

- 6.3.3 Transcatheter tricuspid valve repair (TTVr)

- 6.3.4 Valvuloplasty

- 6.3.5 Other repair procedures

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Cardiac catheterization labs

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 AtriCure

- 9.3 BIOMERICS

- 9.4 Boston Scientific

- 9.5 BRAILE

- 9.6 CryoLife

- 9.7 Edwards

- 9.8 JENAVALVE

- 9.9 LEPU MEDICAL

- 9.10 LivaNova

- 9.11 Medtronic

- 9.12 NUMED