|

市場調査レポート

商品コード

1766316

ユーティリティ配電盤の市場機会、成長促進要因、業界動向分析、2025~2034年予測Utility Distribution Panel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ユーティリティ配電盤の市場機会、成長促進要因、業界動向分析、2025~2034年予測 |

|

出版日: 2025年06月05日

発行: Global Market Insights Inc.

ページ情報: 英文 255 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

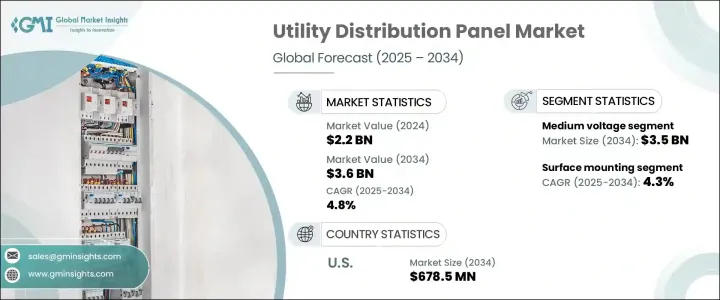

ユーティリティ配電盤の世界市場規模は、2024年に22億米ドルとなり、CAGR4.8%で成長し、2034年までには36億米ドルに達すると予測されています。

この成長の主な要因は、エネルギー需要の変化、継続的なインフラ開発、送電網の安全性と信頼性の向上に対するニーズの高まりです。先進経済諸国と新興経済諸国の両方で、都市中心部が拡大し続け、産業活動が活発化するにつれて、近代的でインテリジェントな配電フレームワークへの需要が一貫して伸びています。これらのシステムにデジタル機能を統合することで、より効率的なエネルギー管理が可能になるだけでなく、監視、制御、性能最適化も向上します。

技術革新は、従来の配電盤を再構築する上で重要な力となっています。制御機能の強化、リアルタイムのモニタリング機能、さまざまなアプリケーション環境へのシステムの適応性などが、市場で好まれるようになっています。再生可能エネルギー発電への依存度が高まるにつれ、分散型発電の変動性と複雑性を管理するために、ユーティリティ配電盤は進化する必要があります。これらのシステムは、複数の電源からのエネルギーフローをサポートするために、より高い柔軟性と容易な再構成を提供することが期待されています。このダイナミックな市場シナリオは、機能的ニーズと規制ニーズの両方に対応する高度にカスタマイズ可能でスケーラブルなソリューションの開発をメーカーに促しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 22億米ドル |

| 予測金額 | 36億米ドル |

| CAGR | 4.8% |

同市場はまた、エネルギー効率の義務化と安全基準の進化にも影響を受けています。メーカーは、高性能と信頼性に対する顧客の期待に応えつつ、国際的なプロトコルに合わせる必要に迫られています。その結果、リアルタイムの診断、予知保全、強化された電力品質管理を確実にするために、スマート機能とIoT(モノのインターネット)統合を組み込むことが重視されるようになっています。さらに、工業団地、住宅、商業施設など、幅広いエンドユーザーに合わせたスケーラブルなソリューションを提供できることが、競争上の差別化要因になりつつあります。

また、さまざまな部門に配備される配電盤のタイプやサイズにも顕著な変化が起きています。中電圧セグメントは2024年に最大の市場シェアを占め、2034年には35億米ドルに達するまで大きく成長すると予測されています。このセグメントは主に、大規模な産業施設、エネルギー集約型の製造工場、ユーティリティグレードの変電所での用途に好まれています。システムのダウンタイムを最小限に抑えつつ、高い電力負荷に対応するため、システムの信頼性と耐久性を強化する動きが強まっています。高圧パネルは、システムの安定性を高め、運用リスクを低減し、最新のオートメーションシステムとシームレスに統合できるように設計されています。

取り付け形態はユーティリティ配電盤分野での購買決定を左右する重要な要素です。2024年の市場シェアは表面実装型が51%を占め、2034年までのCAGRは4.3%と予測されています。表面実装パネルは、その設置の容易さ、アクセスのしやすさ、全体的な実用性から、産業環境で好まれることが多いです。これらのパネルは、厳しい使用条件に耐える堅牢で耐久性のある設置が要求される、需要の高い環境に適しています。一方、フラッシュマウントパネルは、美観とスペースの有効活用が最優先される商業・住宅分野で人気を集めています。インテリアに溶け込み、合理的な外観を維持できることから、特に新築のスマートビルや高級不動産プロジェクトでの需要が高まっています。

米国は、ユーティリティ配電盤業界全体で一貫して力強い成長を示しています。2022年の市場規模は4億1,000万米ドルで、2023年には4億3,880万米ドルに増加し、2024年には4億6,680万米ドルにさらに増加しました。今後、米国市場は2034年までに6億7,850万米ドルに成長すると予測されています。この増加傾向は、インフラの近代化に向けた多額の投資、スマートグリッド技術の幅広い採用、エネルギー効率目標の達成に向けた国家の確固としたコミットメントによるものです。デジタルトランスフォーメーションと老朽化した送電網コンポーネントの更新に重点を置いた継続的な取り組みが、将来の拡大に向けた肥沃な土壌を形成しています。北米は、堅牢な電力網と先進技術の導入に支えられ、北米地域市場の成長に最も貢献している国です。

業界競争は激化しており、メーカーは技術革新、製品の多様化、高成長地域への進出を通じて市場シェアの確保に努めています。市場はますます細分化されていますが、2024年の世界シェアは上位5社合計で35%を超えています。これらの大手企業は世界的に確固たる地位を確立しており、複数の垂直市場にわたってイノベーションを推進し続けています。これらの企業の製品は、幅広い製品ポートフォリオ、顧客中心のカスタマイズオプション、配電エコシステム全体のデジタル変革への明確なコミットメントによって区別されることが多いです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク・課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 競合情勢

- 企業の市場シェア分析

- 戦略的取り組み

- 競合ベンチマーキング

- 戦略的ダッシュボード

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:電圧別、2021年~2034年

- 主要動向

- 低電圧

- 中電圧

第6章 市場規模・予測:取り付け別、2021年~2034年

- 主要動向

- フラッシュマウント

- 表面実装

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

第8章 企業プロファイル

- ABB

- Ags

- alfanar Group

- Arranger Electric Co., Ltd

- CSE Solutions Pvt. Ltd.

- Eaton

- EAMFCO

- ESL POWER SYSTEMS, INC.

- General Electric

- Hager Group

- INDUSTRIAL ELECTRIC MFG

- Larsen &Toubro Limited

- Legrand

- Meba Electric Co., Ltd

- NHP

- Norelco

- Paneltronics

- R Baker

- Schneider Electric

- Siemens

- Symbiotic Systems

The Global Utility Distribution Panel Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 3.6 billion by 2034. This growth is largely driven by shifting energy demands, continuous infrastructure development, and an increasing need for enhanced grid safety and dependability. As urban centers continue to expand and industrial activity intensifies across both developed and emerging economies, the demand for modern, intelligent power distribution frameworks has witnessed consistent growth. The integration of digital capabilities into these systems not only supports more efficient energy management but also improves monitoring, control, and performance optimization.

Technological innovation has been a key force in reshaping traditional utility distribution panels. Enhanced control features, real-time monitoring capabilities, and the adaptability of these systems to different application environments are gaining market preference. As reliance on renewable energy sources grows, utility distribution panels must evolve to manage the variability and complexity of distributed power generation. These systems are expected to offer greater flexibility and easy reconfiguration to support energy flow from multiple sources. This dynamic market scenario is encouraging manufacturers to develop highly customizable and scalable solutions that address both functional and regulatory needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 billion |

| Forecast Value | $3.6 billion |

| CAGR | 4.8% |

The market is also being influenced by tightening energy efficiency mandates and evolving safety standards. Manufacturers are under pressure to align with international protocols while meeting customer expectations for high performance and reliability. As a result, there is a growing emphasis on incorporating smart features and internet-of-things (IoT) integration to ensure real-time diagnostics, predictive maintenance, and enhanced power quality management. Additionally, the ability to provide scalable solutions tailored to a wide range of end users-such as industrial complexes, residential buildings, and commercial establishments-is becoming a competitive differentiator.

A notable shift is also occurring in the type and size of distribution panels deployed across various sectors. The medium voltage segment accounted for the largest market share in 2024 and is projected to grow significantly to reach USD 3.5 billion by 2034. This segment is primarily favored for applications in large industrial facilities, energy-intensive manufacturing plants, and utility-grade substations. There is an increasing push to reinforce the reliability and durability of these systems to cope with high power loads while minimizing system downtime. Medium voltage panels are being engineered to enhance system stability, reduce operational risk, and provide seamless integration with modern automation systems.

Mounting configuration is another critical factor shaping purchasing decisions in the utility distribution panel space. The surface mounting segment dominated the market in 2024, holding 51% of the overall share, and is projected to register a CAGR of 4.3% through 2034. Surface-mounted panels are often preferred in industrial settings due to their ease of installation, accessibility, and overall practicality. These panels are well-suited for high-demand environments that require rugged and durable installations capable of withstanding challenging operating conditions. Meanwhile, flush-mounted panels are gaining popularity in commercial and residential sectors, where aesthetics and space utilization are top priorities. Their ability to blend with interiors and maintain a streamlined appearance is boosting demand, particularly in newly constructed smart buildings and high-end real estate projects.

The United States has consistently demonstrated strong growth across the utility distribution panel industry. The market was valued at USD 410 million in 2022, rose to USD 438.8 million in 2023, and further increased to USD 466.8 million in 2024. Looking ahead, the US market is forecasted to grow to USD 678.5 million by 2034. This upward trend is attributed to significant investments in modernizing infrastructure, broader adoption of smart grid technologies, and a firm national commitment to achieving energy efficiency targets. Ongoing initiatives focused on digital transformation and the renewal of aging grid components are creating fertile ground for future expansion. The country remains the largest contributor to regional market growth in North America, bolstered by a robust utility network and advanced technology adoption.

Industry competition is intensifying, with manufacturers striving to secure market share through innovation, product diversification, and expansion into high-growth regions. While the market is becoming increasingly fragmented, the top five players collectively accounted for over 35% of the global share in 2024. These leaders have established a solid global presence and continue to drive innovation across multiple verticals. Their offerings are often distinguished by wide-ranging product portfolios, customer-centric customization options, and a clear commitment to digital transformation across power distribution ecosystems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Competitive landscape

- 4.2 Company market share analysis, 2024

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Low voltage

- 5.3 Medium voltage

Chapter 6 Market Size and Forecast, By Mounting, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Flush mounting

- 6.3 Surface mounting

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Russia

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 South Africa

- 7.5.5 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Mexico

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Ags

- 8.3 alfanar Group

- 8.4 Arranger Electric Co., Ltd

- 8.5 CSE Solutions Pvt. Ltd.

- 8.6 Eaton

- 8.7 EAMFCO

- 8.8 ESL POWER SYSTEMS, INC.

- 8.9 General Electric

- 8.10 Hager Group

- 8.11 INDUSTRIAL ELECTRIC MFG

- 8.12 Larsen & Toubro Limited

- 8.13 Legrand

- 8.14 Meba Electric Co., Ltd

- 8.15 NHP

- 8.16 Norelco

- 8.17 Paneltronics

- 8.18 R Baker

- 8.19 Schneider Electric

- 8.20 Siemens

- 8.21 Symbiotic Systems