ポリ袋市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測

Polybags Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 250 Pages

- 納期

- 2~3営業日

- 商品コード

- 1959617

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

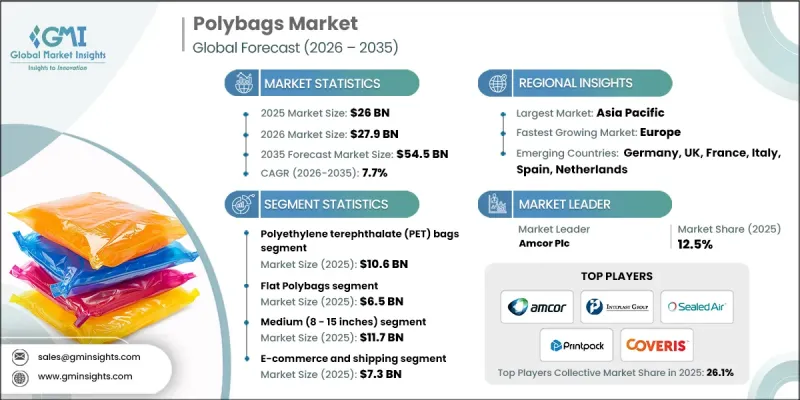

世界のポリ袋市場は2025年に260億米ドルと評価され、2035年までにCAGR 7.7%で成長し、545億米ドルに達すると予測されております。

ポリ袋は主にポリエチレン製で、家庭から産業まで幅広く使用される多用途で柔軟な包装ソリューションです。商品の保管、輸送、保護に活用され、軽量で耐久性があり、コスト効率に優れる特性から高い人気を博しています。透明タイプとカラータイプがあり、LDPE(低密度ポリエチレン)、HDPE(高密度ポリエチレン)、LLDPE(線状低密度ポリエチレン)などのポリマーを用いて製造されます。強度、厚み、柔軟性は素材の品質によって決定されます。高度な押出成形およびブロー成形技術が製造工程の主流であり、紫外線耐性、印刷品質、機械耐久性を向上させるための添加剤が添加されることが一般的です。これらの技術基準により、均一な性能と信頼性が確保されています。ポリ袋は食品、消費財、衣類の包装に使用され、湿気、塵、物理的損傷に対するバリア機能を提供します。その低コスト、利便性、幅広い適用性が、世界の市場拡大を継続的に牽引しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 260億米ドル |

| 予測金額 | 545億米ドル |

| CAGR | 7.7% |

ポリエチレンテレフタレート(PET)袋セグメントは、2025年に106億米ドルを占めました。高い引張強度、透明性、伸縮・収縮への耐性で知られるPET袋は、耐久性と視覚的に魅力的な包装を必要とする産業で好まれています。特に小売業や食品業界において、冷蔵・冷凍食品などの用途で人気があります。その他のポリ袋の種類には、複合材料、ラミネート、生分解性プラスチック、あるいは特定産業の性能要件を満たすために設計された特殊フィルムなどが含まれます。

中型ポリ袋(8~15インチ)は2025年に117億米ドルの市場規模を記録し、最大のシェアを占めました。バランスの取れたサイズは、消費財、書類、衣類、食品の包装に最適です。中程度の寸法は取り扱いの利便性を保ちつつ十分な容量を提供するため、小売後の流通、物流、電子商取引用途に特に適しています。

米国ポリ袋市場は2025年に59億米ドルに達しました。小売、電子商取引、食品包装分野の堅調な成長に加え、使い捨てプラスチック削減を目的とした規制が需要を牽引しています。持続可能性への取り組みにより、特に二次・三次包装において、リサイクル可能、再利用可能、バイオベースのポリ袋への移行が進んでいます。物流や衣料品包装における高い消費量は国内需要を強化する一方、州レベルでのプラスチック袋禁止や課税は、メーカーに堆肥化可能で環境に優しい代替品の開発を促しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 包装業界からの需要増加

- 電子商取引と物流の拡大

- 製造コストおよび材料コストの低さ

- 業界の潜在的リスク&課題

- リサイクルインフラの制約

- 原材料価格の変動性

- 市場機会

- 生分解性ポリ袋の開発

- 製造における技術的進歩

- カスタマイズとブランディングへの需要

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 素材別

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許状況

- 貿易統計(HSコード)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントへの配慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:材料別、2022-2035

- ポリエチレン(PE)袋

- ポリプロピレン(PP)袋

- ポリエチレンテレフタレート(PET)袋

- その他

第6章 市場推計・予測:製品別、2022-2035

- 平型ポリ袋

- ガセット付きポリ袋

- ジップロック式ポリ袋

- ウィケット付きポリ袋

- ポリメーラー

- バブルメール袋

- その他のポリ袋

第7章 市場推計・予測:サイズ別、2022-2035

- 小型(8インチ未満)

- 中型(8~15インチ)

- 大型(15インチ以上)

第8章 市場推計・予測:用途別、2022-2035

- 小売および包装

- 小型(8インチ未満)

- 中型(8~15インチ)

- 大型(15インチ以上)

- 食品包装

- 小型(8インチ未満)

- 中型(8~15インチ)

- 大型(15インチ以上)

- 医療・ヘルスケア

- 小型(8インチ未満)

- 中型(8~15インチ)

- 大型(15インチ以上)

- 工業・製造

- 小型(8インチ未満)

- 中型(8~15インチ)

- 大型(15インチ以上)

- 農業

- 小型(8インチ未満)

- 中型(8~15インチ)

- 大型(15インチ以上)

- 電子商取引と配送

- 小型(8インチ未満)

- 中型(8~15インチ)

- 大型(15インチ以上)

- その他

- 小型(8インチ未満)

- 中型(8~15インチ)

- 大型(15インチ以上)

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- Amcor Plc

- Sealed Air Corporation

- Novolex

- Coveris AG

- Inteplast Group

- Huhtamaki Group

- Printpack, Inc.

- Winpak Ltd.

- A-Pac Manufacturing Co., Inc.

- Arihant Packers

- PPC Flex

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 250 Pages

- 納期

- 2~3営業日