|

|

市場調査レポート

商品コード

1535013

世界のベーカリーおよびシリアル業界における機会:2024年Opportunities in the Global Bakery & Cereals Sector 2024 |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界のベーカリーおよびシリアル業界における機会:2024年 |

|

出版日: 2024年05月30日

発行: GlobalData

ページ情報: 英文 189 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

世界のベーカリーおよびシリアルの市場規模は、2023年に6,822億米ドルとなりました。同市場はCAGR4.4%で拡大し、2028年には8,443億米ドルに達すると予測されています。2023年には、パンおよびロールが金額ベースで最大のカテゴリーとなり、シェアは39.7%、次いでケーキ、ペストリー・スイートパイのシェアが22.8%でした。この部門はGrupo Bimboが金額シェアで3.5%を占め、Mondelez Internationalが3.1%で続きました。ハイパーマーケットとスーパーマーケットは、2023年における世界のベーカリーおよびシリアル部門の主要流通チャネルであり、金額シェアは35.6%、次いで食品・飲料専門店の34%でした。2023年に最も使用された包装材料は軟包装で、80.1%のシェアを占め、硬質プラスチックが14.1%のシェアでこれに続きました。

当レポートでは、世界のベーカリーおよびシリアル市場について調査し、市場の概要とともに、2018年から28年にかけてのベーカリーおよびシリアルセクターの消費変化の概要、地域別動向、競合環境とブランドシェアなどを提供しています。

目次

- エグゼクティブサマリー

- セクター概要

- 世界の概要

- アメリカの概要

- アジア太平洋の概要

- 東欧の概要

- 中東・アフリカの概要

- 西欧の概要

- ベーカリーおよびシリアル:世界の課題

- 食品価値シェアパターンの変化

- 食品産業全体における価値シェアの変化、2023年~2028年

- 価値シェアの変化の理由

- 消費レベルの変化:南北アメリカ、2018年~2028年

- 消費レベルの変化:アジア太平洋、2018年~2028年

- 消費レベルの変化:東欧、2018年~2028年

- 消費レベルの変化:中東・アフリカ、2018年~2028年

- 消費レベルの変化:西欧、2018年~2028年

- 地域別に潜在力の高い国

- 調査手法-潜在力の高い国の特定

- 見通し

- 健康とウェルネス分析

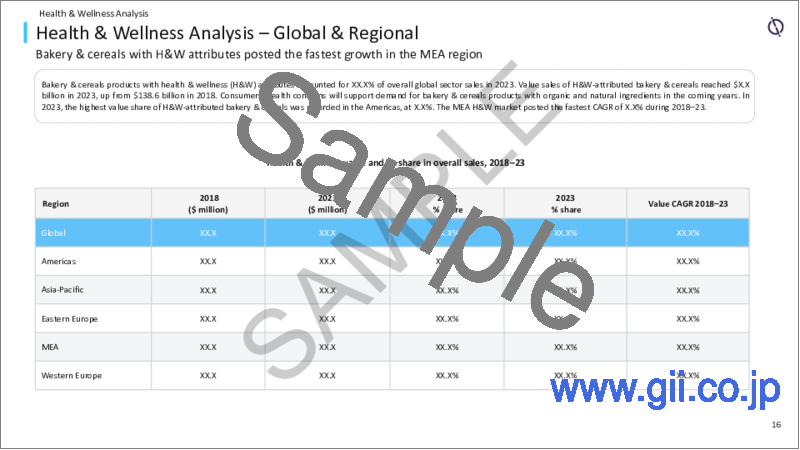

- 健康とウェルネス分析- 世界と地域

- 競合環境

- 価値別トップ企業- 世界

- 主要企業とブランドのシェア分析- 世界

- 地域別主要企業・ブランドシェア分析

- 競合情勢-市場分析

- 主要ブランド- ベーキング材料

- 主要ブランド- ベーキングミックス

- 主要ブランド- パン・ロール

- 主要ブランド- 朝食用シリアル

- 主要ブランド- ケーキ、ペストリー、スイートパイ

- 主要ブランド- シリアルバー

- 主要ブランド- クッキー(甘いビスケット)

- 主要ブランド- 生地製品

- 主要ブランド- エナジーバー

- 主要ブランド- モーニンググッズ

- 主要ブランド- セイボリービスケット

- プライベートブランドの市場シェア

- 地域別プライベートブランドのシェア分析

- プライベートブランドのカテゴリー別シェア分析

- 主要流通チャネル

- 主要流通チャネルのシェア- 世界および地域レベル

- 主要包装形態

- 主要パック素材とパックタイプ別の成長分析

- 閉鎖タイプと主な外部タイプ別成長分析

- 業界指標を選択

- 世界特許出願

- 世界求人分析

- 世界の取引

- 付録

- 定義

- GlobalDataについて

The global bakery & cereals sector was valued at $682.2 billion in 2023 and is projected to reach $844.3 billion in 2028, at a CAGR of 4.4%. In 2023, bread & rolls was the largest category in terms of value, with a share of 39.7%, followed by cakes, pastries & sweet pies with a share of 22.8%. The sector was led by Grupo Bimbo, which held a value share of 3.5%, followed by Mondelez International with a 3.1%. Hypermarkets & supermarkets was the leading distribution channel in the global bakery & cereals sector in 2023, with a value share of 35.6%, followed by food & drinks specialists with 34%. Flexible packaging was the most used pack material in 2023, accounting for a share of 80.1%, distantly followed by rigid plastics with a 14.1% share.

Scope

This report brings together multiple data sources to provide a comprehensive overview of the global bakery & cereals sector, analyzing data from 108 countries. It includes analysis of the following -

- Sector overview: Provides an overview of the current sector scenarios in terms of ingredients, manufacturer claims, labeling, and packaging. The analysis also provides a regional overview across five regions-Asia-Pacific, Middle East and Africa (MEA), the Americas, Western Europe, and Eastern Europe-highlighting sector size, growth drivers, the latest developments, and future challenges for each region.

- Change in consumption: Provides an overview of consumption changes in the bakery & cereals sector over 2018- 28 at global and regional levels.

- High-potential countries: Provides risk- reward analysis of the top high-potential countries in each region based on market assessment, economic development, governance indicators, sociodemographic factors, and technological infrastructure.

- Country and regional analysis: Provides a deep-dive analysis of 10 high-potential countries covering value growth during 2023- 28 and key trends. It also includes regional analysis covering the future outlook for each region.

- Competitive environment and brand shares: Provides an overview of the leading companies and brands at global and regional levels. Market shares of brands and private labels in each region are also detailed.

- Key distribution channels: Provides an analysis of the leading distribution channels in the global bakery & cereals sector in 2023. It covers hypermarkets & supermarkets, convenience stores, food & drinks specialists, e-retailers, cash & carries & warehouse clubs, "dollar stores", variety stores & general merchandise retailers, department stores, vending machines, drug stores & pharmacies, and other retail channels.

- Packaging analysis*: The report provides percentage share (in 2023) and growth rate analysis (during 2018- 28) for various pack materials, pack types, closures, and primary outer types based on volume sales of bakery & cereals.

Reasons to Buy

- Manufacturers and retailers seek latest information on how the market is evolving to formulate their sales and marketing strategies. There is also demand for authentic market data with a high level of detail. This report has been created to provide its readers with up-to-date information and analysis to uncover emerging opportunities of growth within the bakery and cereals sector.

- The report provides a detailed analysis of the countries in the region, covering the key challenges, competitive landscape and demographic analysis, that can help companies gain insight into the country specific nuances.

- The analysts have also placed a significant emphasis on the key trends that drive consumer choice and the future opportunities that can be explored in the region, than can help companies in revenue expansion.

- To gain competitive intelligence about leading brands in the sector in the region with information about their market share and growth rates.

Table of Contents

Table of Contents

- Executive Summary

- Sector Overview

- Global Overview

- Americas Overview

- Asia-Pacific Overview

- Eastern Europe Overview

- MEA Overview

- Western Europe Overview

- Bakery & cereals: Global Challenges

- Shift in Food Value Share Patterns

- Change in Value Share in the Overall Food Industry, 2023-28

- Reasons for Shift in Value Share

- Change in Consumption Levels: Americas, 2018-28

- Change in Consumption Levels: Asia-Pacific, 2018-28

- Change in Consumption Levels: Eastern Europe, 2018-28

- Change in Consumption Levels: MEA, 2018-28

- Change in Consumption Levels: Western Europe, 2018-28

- Identifying High-Potential Countries by Region

- Identifying High-Potential Countries by Region

- Methodology - Identifying High-Potential Countries

- Country Deep Dive

- High-Potential Country Analysis

- Outlook

- Health & Wellness Analysis

- Health & Wellness Analysis - Global & Regional

- Competitive Environment

- Leading Companies by Value - Global

- Leading Companies and Brands Share Analysis - Global

- Leading Companies and Brands Share Analysis by Region

- Competitive Landscape - Market Analysis

- Key Brands - Baking Ingredients

- Key Brands - Baking Mixes

- Key Brands - Bread & Rolls

- Key Brands - Breakfast Cereals

- Key Brands - Cakes, Pastries & Sweet Pies

- Key Brands - Cereal Bars

- Key Brands - Cookies (Sweet Biscuits)

- Key Brands - Dough Products

- Key Brands - Energy Bars

- Key Brands - Morning Goods

- Key Brands - Savory Biscuits

- Market Share of Private Labels

- Private Labels' Share Analysis by Region

- Private Labels' Share Analysis by Category

- Key Distribution Channels

- Share of Key Distribution Channels - Global and Regional Level

- Key Packaging Formats

- Growth Analysis by Key Pack Material and Pack Type

- Growth Analysis by Closure Type and Primary Outer Type

- Select Industry Metrics

- Global Patent Filings

- Global Job Analytics

- Global Deals

- Appendix

- Definitions

- About GlobalData