|

|

市場調査レポート

商品コード

1383296

アクリルの成長機会Growth Opportunities in Acrylics |

||||||

|

|

|||||||

|

|||||||

| アクリルの成長機会 |

|

出版日: 2023年10月24日

発行: Frost & Sullivan

ページ情報: 英文 173 Pages

納期: 即日から翌営業日

|

- 全表示

- 概要

- 目次

持続可能性の要件を満たす革新的なアプローチが、研究開発イニシアチブを大幅に推進

アクリルは非常に汎用性の高い材料群であり、コーティング、接着剤、シーラント、エラストマー、高吸水性ポリマー(SAP)、ポリメチルメタクリレート(PMMA)、テキスタイル、添加剤、インク、水処理用薬品、建設用薬品、洗剤、化粧品、紙製品などの最終製品の原材料として幅広く応用されています。輸送、消費財、工業、医療、製紙・包装など、複数の最終産業がこれらの製品を採用しています。様々な最終用途産業の成長が、2023年から2029年にかけてアクリルモノマー・樹脂の市場を牽引すると予想されます。

アクリル酸、アクリロニトリル、アクリル酸エチル、アクリル酸ブチル、メタクリル酸メチル、アクリルアミド、アクリル酸2-エチルヘキシルは、アクリルの世界市場に関する調査の対象となる7つの主要なアクリルモノマータイプです。最終用途ごとに、地域の数量消費と地域の収益予測を、モノマータイプ別の収益・数量予測とともに考察しています。また、世界レベルでの主要なアクリルモノマー・樹脂メーカーの市場シェアも調査しています。

アクリルモノマー・原材料サプライヤー、ならびにアクリル樹脂サプライヤーは、持続可能なプロセスや最終製品の開発を支援するバイオベースのモノマー、原材料、樹脂など、持続可能性の要件を満たす製品に対する最終消費者の需要が増加していることを目の当たりにしています。

アクリル樹脂メーカーは、革新的な製品ポートフォリオを迅速に開発するため、あるいは新しい地域に参入して競合優位性を獲得するために、戦略的買収を行う必要があります。中国、インド、東南アジア、ラテンアメリカは、アクリル樹脂とアクリル製品の消費拡大を支える大規模で急成長中の最終用途産業により、今後7年間で高い成長が見込まれる市場です。

世界のアクリル樹脂メーカーにとって、アクリルモノマーやその他の原材料の入手において優位な足場を得るためには、長期的な安定供給、原材料の品質、競争力のある原材料価格の維持という点で、垂直統合が不可欠となります。したがってM&Aは、有機的戦略とは別に、バリューチェーン全体の利害関係者が垂直統合を迅速に達成するために採用すべき無機的戦略です。最終用途産業によるアクリル樹脂の消費増加と、バイオベース・高機能製品の開発が、5~7年後の市場成長に寄与すると予想されます。

目次

戦略的インペラティブ

- なぜ成長が難しくなっているのか?

- The Strategic Imperative 8(TM)

- アクリル業界に対する主要な戦略的インペラティブの影響

- 成長機会がGrowth Pipeline Engine(TM)を促進

成長機会分析

- 分析範囲

- セグメンテーション

- アクリル:樹脂、製品アプリケーション、関連モノマータイプのマッピング

- 地理的範囲

- 成長指標

- バリューチェーン

- バリューチェーン分析

- 成長促進要因

- 成長抑制要因

- 予測の前提条件

- 収益・数量予測

- 収益予測、モノマータイプ別

- 数量予測、モノマータイプ別

- 収益予測、樹脂アプリケーション別

- 数量予測、樹脂アプリケーション別

- 収益・数量予測分析

- 収益予測、地域別

- 数量予測、地域別

- 収益・数量分析、地域別

- 平均価格予測

- 価格動向と予測

- 価格動向と予測分析

- 競合環境

- 主要な競合企業(モノマー・樹脂サプライヤー)

- 主要な競合企業(樹脂の最終用途産業)

- 収益シェア、モノマータイプ別

- 収益シェア分析、モノマータイプ別

- 収益シェア、樹脂タイプ別

- 収益シェア分析、樹脂タイプ別

成長機会分析:コーティング樹脂

- セグメントの特徴と概要

- 成長指標

- 促進要因

- 促進要因分析

- 予測の前提条件

- 収益・数量予測

- 予測分析

- 収益予測、モノマータイプ別

- 数量予測、モノマータイプ別

- 予測分析、モノマータイプ別

- 収益予測、地域別

- 数量予測、地域別

- 予測分析、地域別

成長機会分析:アクリル系粘着剤・シーラント樹脂

- セグメントの特徴と概要

- 成長指標

- 促進要因

- 促進要因分析

- 予測の前提条件

- 収益・数量予測

- 予測分析

- 収益予測、モノマータイプ別

- 数量予測、モノマータイプ別

- 予測分析、モノマータイプ別

- 収益予測、地域別

- 数量予測、地域別

- 予測分析、地域別

成長機会分析:アクリル系エラストマー樹脂

- セグメントの特徴と概要

- 成長指標

- 促進要因

- 促進要因分析

- 予測の前提条件

- 収益・数量予測

- 予測分析

- 収益予測、モノマータイプ別

- 数量予測、モノマータイプ別

- 予測分析、モノマータイプ別

- 収益予測、地域別

- 数量予測、地域別

- 予測分析、地域別

成長機会分析:SAP(高吸水性ポリマー)樹脂

- セグメントの特徴と概要

- 成長指標

- 促進要因

- 促進要因分析

- 予測の前提条件

- 収益・数量予測

- 予測分析

- 収益予測、モノマータイプ別

- 数量予測、モノマータイプ別

- 予測分析、モノマータイプ別

- 収益予測、地域別

- 数量予測、地域別

- 予測分析、地域別

成長機会分析:PMMA(ポリメチルメタクリレート)樹脂

- セグメントの特徴と概要

- 成長指標

- 促進要因

- 促進要因分析

- 予測の前提条件

- 収益・数量予測

- 予測分析

- 収益予測、モノマータイプ別

- 数量予測、モノマータイプ別

- 予測分析、モノマータイプ別

- 収益予測、地域別

- 数量予測、地域別

- 予測分析、地域別

成長機会分析:テキスタイル用樹脂

- セグメントの特徴と概要

- 成長指標

- 促進要因

- 促進要因分析

- 予測の前提条件

- 収益・数量予測

- 予測分析

- 収益予測、モノマータイプ別

- 数量予測、モノマータイプ別

- 予測分析、モノマータイプ別

- 収益予測、地域別

- 数量予測、地域別

- 予測分析、地域別

成長機会分析:その他のアプリケーション

- セグメントの特徴と概要

- 成長指標

- 促進要因

- 促進要因分析

- 予測の前提条件

- 収益・数量予測

- 予測分析

- 収益予測、モノマータイプ別

- 数量予測、モノマータイプ別

- 予測分析、モノマータイプ別

- 収益予測、地域別

- 数量予測、地域別

- 予測分析、地域別

成長機会ユニバース

- 成長機会1:M&Aで市場フットプリント拡大

- 成長機会2:垂直統合で事業優位性を獲得

- 成長機会3:持続可能なアクリル製品の開発

付録

次のステップ

Innovative Approaches to Meet Sustainability Requirements will Significantly Drive Research and Development Initiatives

Acrylics are a group of highly versatile materials that find extensive application as raw materials in end-products such as in coatings, adhesives, sealants, elastomers, superabsorbent polymers (SAPs), polymethyl methacrylate (PMMA), textiles, additives, inks, water treatment chemicals, construction chemicals, detergents, cosmetics, and paper products. Multiple end industries have adopted these products, including transportation, consumer goods, industrial, medical, and paper and packaging. The growth of various end-use industries will drive the market for acrylic monomers and resins from 2023 to 2029.

Acrylic acid, acrylonitrile, ethyl acrylate, butyl acrylate, methyl methacrylate, acrylamide, and 2-ethylhexyl acrylate are the seven major acrylic monomer types that fall within the scope of this study on the global acrylics market. For each end-use application, regional volume consumption and regional revenue estimates are discussed, along with revenue and volume estimates by monomer type. The report also examines market share of the top acrylic monomer and resin manufacturers at the global level.

Acrylic monomer and raw material suppliers as well as acrylic resin suppliers are witnessing increasing end-consumer demand for products that will help meet their sustainability requirements, such as bio-based monomers, raw materials, and resins that aid in the development of sustainable processes and end products.

Acrylic resin producers will need to make strategic acquisitions either to quickly develop an innovative product portfolio or to enter new geographies and gain competitive advantage. China, India, Southeast Asia, and Latin America represent the markets set to witness high growth in the next 7 years due to their large, fast-growing end-use industries that support acrylic resin and product consumption growth.

It will be essential for global acrylic resin producers to vertically integrate to gain a dominate foothold in acquiring their acrylic monomer and other raw materials, in terms of sustaining consistent long-term supply, raw material quality, and competitive raw material prices. Mergers and acquisitions thus represent the inorganic strategy stakeholders across the value chain should adopt to quickly achieve vertical integration, apart from organic strategies. The increasing consumption of acrylic resins by end-use industries and the development of bio-based and high-performance products will contribute to market growth in 5 to 7 years.

Table of Contents

Strategic Imperatives

- Why is it Increasingly Difficult to Grow?

- The Strategic Imperative 8™

- The Impact of the Top 3 Strategic Imperatives on the Acrylics Industry

- Growth Opportunities Fuel the Growth Pipeline Engine™

Growth Opportunity Analysis

- Scope of Analysis

- Segmentation

- Acrylics-Mapping of Resin & Product Applications and Relevant Monomer Type(s) Used

- Geographic Scope

- Growth Metrics

- Value Chain

- Value Chain Analysis

- Growth Drivers

- Growth Restraints

- Forecast Assumptions

- Revenue and Volume Forecast

- Revenue Forecast by Monomer Type

- Volume Forecast by Monomer Type

- Revenue Forecast by Resin Application

- Volume Forecast by Resin Application

- Revenue and Volume Forecast Analysis

- Revenue Forecast by Region

- Volume Forecast by Region

- Revenue and Volume Analysis by Region

- Average Price Forecast

- Pricing Trends and Forecast

- Pricing Trends and Forecast Analysis

- Competitive Environment

- Key Competitors (Monomer and Resin Suppliers)

- Key Competitors (Resin End-use Industries)

- Revenue Share by Monomer Type

- Revenue Share Analysis by Monomer Type

- Revenue Share by Resin Type

- Revenue Share Analysis by Resin Type

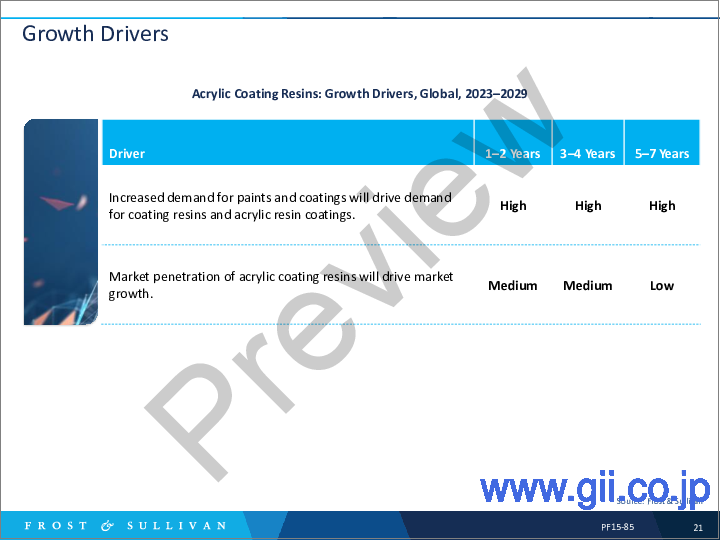

Growth Opportunity Analysis-Coating Resins

- Segment Characteristics and Overview

- Growth Metrics

- Growth Drivers

- Growth Driver Analysis

- Forecast Assumptions

- Revenue and Volume Forecast

- Forecast Analysis

- Revenue Forecast by Monomer Type

- Volume Forecast by Monomer Type

- Forecast Analysis by Monomer Type

- Revenue Forecast by Region

- Volume Forecast by Region

- Forecast Analysis by Region

Growth Opportunity Analysis-Acrylic Adhesive & Sealant Resins

- Segment Characteristics and Overview

- Growth Metrics

- Growth Drivers

- Growth Driver Analysis

- Forecast Assumptions

- Revenue and Volume Forecast

- Forecast Analysis

- Revenue Forecast by Monomer Type

- Volume Forecast by Monomer Type

- Forecast Analysis by Monomer Type

- Revenue Forecast by Region

- Volume Forecast by Region

- Forecast Analysis by Region

Growth Opportunity Analysis-Acrylic Elastomer Resins

- Segment Characteristics and Overview

- Growth Metrics

- Growth Drivers

- Growth Driver Analysis

- Forecast Assumptions

- Revenue and Volume Forecast

- Forecast Analysis

- Revenue Forecast by Monomer Type

- Volume Forecast by Monomer Type

- Forecast Analysis by Monomer Type

- Revenue Forecast by Region

- Volume Forecast by Region

- Forecast Analysis by Region

Growth Opportunity Analysis- Superabsorbent Polymer (SAP) Resins

- Segment Characteristics and Overview

- Growth Metrics

- Growth Drivers

- Growth Driver Analysis

- Forecast Assumptions

- Revenue and Volume Forecast

- Forecast Analysis

- Revenue Forecast by Monomer Type

- Volume Forecast by Monomer Type

- Forecast Analysis by Monomer Type

- Revenue Forecast by Region

- Volume Forecast by Region

- Forecast Analysis by Region

Growth Opportunity Analysis-Polymethyl Methacrylate (PMMA) Resins

- Segment Characteristics and Overview

- Growth Metrics

- Growth Drivers

- Growth Driver Analysis

- Forecast Assumptions

- Revenue and Volume Forecast

- Forecast Analysis

- Revenue Forecast by Region

- Volume Forecast by Region

- Forecast Analysis by Region

Growth Opportunity Analysis-Resins for Textiles

- Segment Characteristics and Overview

- Growth Metrics

- Growth Drivers and Restraints

- Growth Driver Analysis

- Growth Restraint Analysis

- Forecast Assumptions

- Revenue and Volume Forecast

- Forecast Analysis

- Revenue Forecast by Monomer Type

- Volume Forecast by Monomer Type

- Forecast Analysis by Monomer Type

- Revenue Forecast by Region

- Volume Forecast by Region

- Forecast Analysis by Region

Growth Opportunity Analysis-Other Applications

- Segment Characteristics and Overview

- Growth Metrics

- Growth Drivers

- Growth Driver Analysis

- Forecast Assumptions

- Revenue and Volume Forecast

- Forecast Analysis

- Revenue Forecast by Monomer Type

- Volume Forecast by Monomer Type

- Forecast Analysis by Monomer Type

- Revenue Forecast by Region

- Volume Forecast by Region

- Forecast Analysis by Region

Growth Opportunity Universe

- Growth Opportunity 1: M&As to Expand Market Footprint

- Growth Opportunity 2: Vertical Integration to Gain a Business Advantage

- Growth Opportunity 3: Developing Sustainable Acrylic Products

Appendix

- List of Abbreviations

Next Steps

- Your Next Steps

- Why Frost, Why Now?

- List of Exhibits

- Legal Disclaimer