|

|

市場調査レポート

商品コード

1319200

自動車アフターマーケットにおける循環型経済への取り組みと再製造による成長機会、2023年Circular Economy Initiatives and Growth Opportunities from Remanufacturing in the Automotive Aftermarket, 2023 |

||||||

|

|

|||||||

|

|||||||

| 自動車アフターマーケットにおける循環型経済への取り組みと再製造による成長機会、2023年 |

|

出版日: 2023年07月14日

発行: Frost & Sullivan

ページ情報: 英文 116 Pages

納期: 即日から翌営業日

|

- 全表示

- 概要

- 目次

従来型エンジン、トランスミッション、および関連部品は、世界最大の交換売上カテゴリーであり続ける

自動車アフターマーケットは、液体、バッテリー、温室効果ガス、部品から出る使用済み材料など、廃棄物や公害の大きな原因となっています。サーキュラー・エコノミー(循環型経済)とは、製品や素材をできるだけ長く使い続けることで廃棄物や汚染を減らすことに焦点を当てた代替経済モデルです。再製造は、中古部品を保証付きで新品同様の状態に戻すプロセスであり、循環型経済の重要な構成要素であり、リサイクル、リデュース、修理と密接に協力することで、自動車アフターマーケットにおける廃棄物と汚染を削減する上で重要な役割を果たすことができます。

この調査レポートは、クラス1からクラス3の乗用車における自動車部品のサーキュラーエコノミーに焦点を当てています。基準年は2022年、予測期間は2023年から2030年です。売上はメーカーレベルで算出し、米国ドル表示。成長促進要因と阻害要因、関連団体、主要動向、法規制、インセンティブについて論じています。

各地域のセクションでは、その地域におけるVIO、アフターマーケット全体の収益、再製造による収益などの主要なアフターマーケット指標をハイライトしています。

再製造の収益と収益の可能性は、主要カテゴリー(エンジンと関連部品、ホイールとブレーキエンド、電気と電子機器、eコンポーネント[バッテリー再製造とパワーエレクトロニクス])に基づいてさらに分類されています。また、競合、チャネル分析(該当する場合)、地域展望、各バリューチェーン参加者の成長機会などの競合情勢も明らかにしています。企業プロファイルとサプライヤーおよび販売業者のリマンプログラムの例も含まれています。

主要課題

- OEMやティアiサプライヤーは再製造においてどのような取り組みを行っているのか?

- どのようなバリューチェーンが成長を促進しているのか?

- グリーンコンポーネントの分野で事業を展開するOEMとティアIサプライヤーはどこか、またその主なアフターマーケット・プログラムは何か。

- アフターマーケット収益における従来型部品と電子部品の市場ポテンシャルは?

- どのような地域動向、ビジネスモデル、法律、マクロ経済変数が部品の循環経済に影響を与えているか?

- サプライヤー、OEM、バリューチェーン参加者にとって、どのような成長機会とホワイトスペースが存在するか?

目次

戦略的課題

- なぜ成長が難しくなっているのか?

- The Strategic Imperative 8(TM)

- リマン(再製造)アフターマーケットのサーキュラー・エコノミーへの取り組みにおける戦略的課題トップ3のインパクト

- Growth Pipeline Engine(TM)を後押しする成長機会

分析範囲と定義

- 分析の範囲

- 本調査が回答する主な質問

- セグメントと定義

- 循環型経済-リバース・ロジスティクス・バリューチェーン・プロセスフロー

- リマン(再製造)コンポーネントの循環型経済

- 流通チャネル

- 国際再製造規格

- 関連団体

- 調査対象企業の例とバリューチェーン参加企業

- 成長促進要因

- 成長阻害要因

世界の自動車再生アフターマーケット

- 主な調査結果

- リマン(再製造)アフターマーケットの世界売上高-市場潜在力

- リマン(再製造)アフターマーケットの世界収益-地域別アフターマーケットスナップショット

- 製品としてのリマン(再製造)-成熟サイクル

- 2022年、OESとIAMのリマン(再製造)アフターマーケットの比較

- M&Aとバリューチェーン・パートナーシップ-主要テーマ

- 新たなビジネスモデルと地域動向

- 自動車部品の循環型経済に影響を与える法律

- 主要OEMとティアiサプライヤーのサ循環型経済への取り組み

- EVエコシステムにおける主要バッテリー4R企業

- 自動車部品の循環型経済における中核物流パートナーの役割

- アフターマーケットにおける持続可能なコアハンドリングプラクティスの未来

- 自動車部品の循環型経済によるコストと材料の節約

- アフターマーケット部品の循環型経済におけるグリーン包装

- 循環型経済の取り組みへのインセンティブ-地域別スナップショット

部品の循環型経済の将来を決定づける動向

- 概要-グリーン部品の循環型経済が勢いを増す

- 動向1-コア企業の買収とリバース・ロジスティクスへの投資

- 動向2-フレームワークの開発と導入

- 動向3-部品のモジュール化とメンテナンス

- 動向4-トレーサビリティとライフサイクル管理

- 動向5-CASEコンポーネントの循環型経済への対応

- 動向6-IAMにおけるプライベート・ラベリング

- 予測の前提条件

北米自動車リマン(再製造)アフターマーケット

- ダッシュボード:主要アフターマーケット指標:北米

- 北米-リマン(再製造)アフターマーケットの収益市場規模の可能性

- 北米-リマン(再製造)コンポーネントチャネルの選択

- 2022年の北米リマン(再製造)アフターマーケットの展望

- 北米-成長機会

- 北米-リマン(再製造)エコシステムにおける主要サプライヤー*の競合情勢

欧州の自動車用リマン(再製造)アフターマーケット

- ダッシュボード-主要アフターマーケット指標:欧州

- 欧州アフターマーケット・リマン(再製造)レベニュー市場規模の可能性

- リマンの情勢-EU4と英国

- 欧州-リマン(再製造)コンポーネント・チャネルの嗜好性

- 2022年の欧州リマン(再製造)アフターマーケットの状況

- 成長機会-欧州

- 欧州-リマン(再製造)エコシステムにおける主要サプライヤー*の競合情勢

アジア太平洋自動車リマン(再製造)アフターマーケット

- ダッシュボード:主要アフターマーケット指標:アジア太平洋地域

- APACアフターマーケット・リマン(再製造)レベニュー市場規模の可能性

- リマン(再製造)の情勢-インドと中国

- 2022年のAPACリマン(再製造)アフターマーケットの状況

- 成長機会-APAC

ラテンアメリカの自動車リマン(再製造)アフターマーケット

- ダッシュボード-主要アフターマーケット指標ラタム

- ラテンアメリカ:リマン(再製造)アフターマーケットの売上高市場規模の可能性

- 2022年の中南米リマン(再製造)アフターマーケットの情勢

- 成長機会-ラタム

- ラテンアメリカ-リマン(再製造)エコシステムにおける主要サプライヤー*の競合情勢

主要企業プロファイル

- 企業プロファイル

ケーススタディ

- ケーススタディ-Stellantis N.V.

- ケーススタディ--Ford Remanufacturing Program

- ケーススタディ-Cardone Industries

- ケーススタディ-Groupe Renault

- ケーススタディ-ZF Reman

- ケーススタディ-LKQ

成長機会ユニバース

- 成長機会1-従来型部品アフターマーケット[サプライヤー]

- 成長機会2-部品・バッテリー再生[サプライヤー]

- 成長機会3-リバース・ロジスティクス【OES、小売店、WD

- 成長機会4-プライベートブランドとバリューライン【サプライヤー、OEM、小売業者、WD

- 成長機会5-コア・バイバック・プログラム[サプライヤー、OEM、コア調達先、小売業者、WD]

最後の一言

- 最後の一言-3大予測

次のステップ

- 次のステップ

- なぜフロストなのか、なぜ今なのか?

付録

- 調査対象企業の例とバリューチェーン参加企業

- 別紙リスト

- 免責事項

Conventional Engine, Transmission, and Affiliated Components Will Continue to Be the Largest Replacement Revenue Category Globally

The automotive aftermarket is a significant contributor to waste and pollution including fluids, batteries, greenhouse gases, and used materials from parts. The circular economy is an alternative economic model that focuses on reducing waste and pollution by keeping products and materials in use for as long as possible. Remanufacturing, which is the process of restoring used parts to like-new condition with affiliated warranty, is a key component of the circular economy and can play a significant role in reducing waste and pollution in the automotive aftermarket in close cooperation with recycling, reducing, and repairing.

This research report focuses on the circular economy of automotive parts in Class 1 to 3 passenger vehicles. The base year is 2022 and the forecast period is from 2023 to 2030. Revenue is calculated at the manufacturer level and represented in US dollars. Growth drivers and restraints, associations, and key trends, legislation, and incentives are discussed.

Each regional section highlights the key aftermarket indicators such as VIO, overall aftermarket revenue and revenue from reman in that region.

Reman revenue and revenue potential is further classified based on primary categories (engine and related components, wheel and brake end, electrical and electronics, and eComponents [battery reman and power electronics]). The study also highlights the competitive landscape in terms of competitors, channel analysis (where applicable), regional outlook, and growth opportunities for each value chain participant. Company profiles and examples of supplier and distributor reman programs are included.

Key Issues Addressed

- What initiatives are OEMs and Tier I suppliers undertaking in remanufacturing?

- What notable value chain enablers are driving growth?

- Which OEMs and Tier I suppliers operate in the green components space and what are their main aftermarket programs?

- What is the market potential for conventional and eComponents in terms of aftermarket revenue?

- What regional trends, business models, legislation, and macroeconomic variables are influencing the circular economy of parts?

- What growth opportunities and white spaces exist for suppliers, OEMs, and value chain participants?

Table of Contents

Strategic Imperatives

- Why is it Increasingly Difficult to Grow?

- The Strategic Imperative 8™

- The Impact of the Top 3 Strategic Imperatives on Circular Economy Initiatives from the Reman Aftermarket

- Growth Opportunities Fuel the Growth Pipeline Engine™

Scope and Definition

- Scope of Analysis

- Key Questions This Study Will Answer

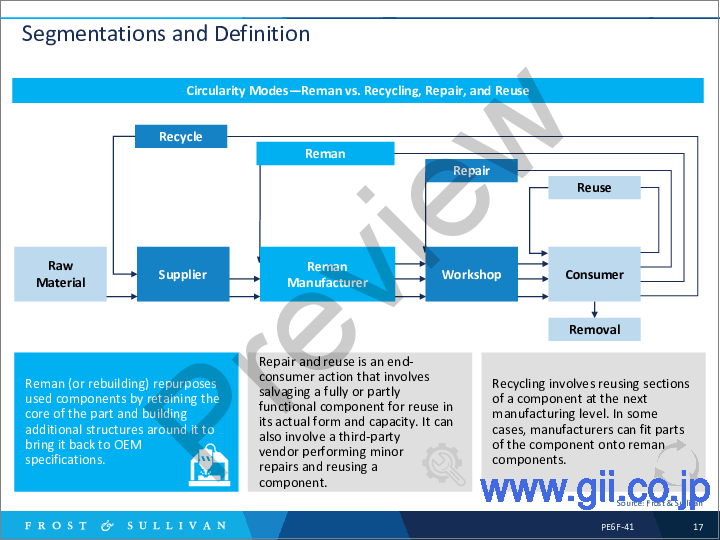

- Segmentations and Definition

- Circular Economy-Reverse Logistics Value Chain Process Flow

- Reman Components' Circular Economy

- Distribution Channels

- International Remanufacturing Standards

- Associations

- Selected Competitors and Value Chain Participants

- Growth Drivers

- Growth Restraints

Global Automotive Reman Aftermarket

- Primary Findings

- Global Reman Aftermarket Revenue-Market Potential

- Global Reman Aftermarket Revenue-Regional Aftermarket Snapshot

- Reman-as-a-Product-Maturity Cycle

- OES vs. IAM-Channel Preference for Reman Replacements, 2022

- M&A and Value Chain Partnerships-Primary Themes

- Emerging Business Models and Regional Trends

- Legislation Influencing the Circular Economy of Auto Components

- Primary OEMs and Tier I Suppliers and Their Circular Economy Initiatives

- Primary Battery 4R Companies in the EV Ecosystem

- Core Logistics Partners' Role in Circular Economy of Auto Parts

- The Future of Sustainable Core-handling Practices in the Aftermarket

- Cost and Material Savings from Circular Economy of Automotive Parts

- Green Packaging in the Aftermarket Parts' Circular Economy

- Incentivizing Circular Economy Initiatives-Regional Snapshot

Trends Likely to Define the Future of the Circular Economy of Parts

- Overview-Green Components' Circular Economy to Gain Momentum

- Trend 1-Core Acquisition and Investment in Reverse Logistics

- Trend 2-Developing and Implementing a Framework

- Trend 3-Component Modularization and Maintenance

- Trend 4-Traceability and Life Cycle Management

- Trend 5-Future-proofing the Circular Economy of CASE Components

- Trend 6-Private Labeling in the IAM

- Forecast Assumptions

North America Automotive Reman Aftermarket

- Dashboard-Key Aftermarket Indicators: North America

- North America-Aftermarket Reman Revenue Market Size Potential

- North America-Channel Preference for Select Reman Components

- North American Reman Aftermarket Landscape in 2022

- Growth Opportunity-North America

- North America-Competitive Landscape of Primary Suppliers* in the Reman Ecosystem

Europe Automotive Reman Aftermarket

- Dashboard-Key Aftermarket Indicators: Europe

- European Aftermarket Reman Revenue Market Size Potential

- Reman Landscape-EU4 and the United Kingdom

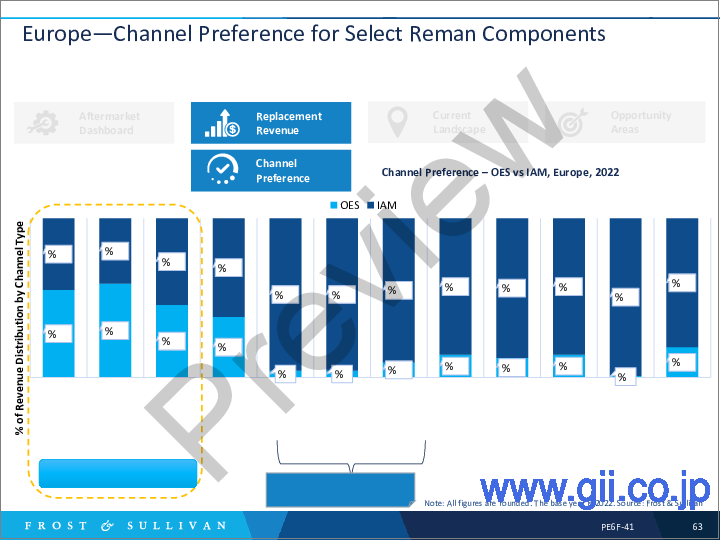

- Europe-Channel Preference for Select Reman Components

- European Reman Aftermarket Landscape in 2022

- Growth Opportunity-Europe

- Europe-Competitive Landscape of Primary Suppliers* in the Reman Ecosystem

Asia-Pacific Automotive Reman Aftermarket

- Dashboard-Key Aftermarket Indicators: APAC

- APAC Aftermarket Reman Revenue Market Size Potential

- The Reman Landscape-India and China

- APAC Reman Aftermarket Landscape in 2022

- Growth Opportunity-APAC

Latin America Automotive Reman Aftermarket

- Dashboard-Key Aftermarket Indicators: LATAM

- LATAM-Aftermarket Reman Revenue Market Size Potential

- LATAM Reman Aftermarket Landscape in 2022

- Growth Opportunity-LATAM

- LATAM-Competitive Landscape of Primary Suppliers* in the Reman Ecosystem

Key Company Profiles

- Company Profiles

Case Studies

- Case Study-Stellantis N.V.

- Case Study-Ford Remanufacturing Program

- Case Study-Cardone Industries (Rebuild & Return [R&R] Service)

- Case Study-Groupe Renault

- Case Study-ZF Reman

- Case Study-LKQ

Growth Opportunity Universe

- Growth Opportunity 1-Conventional Components Aftermarket[Suppliers]

- Growth Opportunity 2-eComponents and Battery Remanufacturing[Suppliers]

- Growth Opportunity 3-Reverse Logistics [OES, Retailers, and WDs]

- Growth Opportunity 4-Private Label and Value Line [Suppliers, OEMs, Retailers, and WDs]

- Growth Opportunity 5-Core Buyback Programs [Suppliers, OEMs, Core Procurers, Retailers, and WDs]

The Last Word

- The Last Word-3 Big Predictions

Next Steps

- Your Next Steps

- Why Frost, Why Now?

Appendix

- Selected Primary Competitors and Value Chain Participants

- List of Exhibits

- Legal Disclaimer