|

|

市場調査レポート

商品コード

1423527

バイオプラスチックの世界市場-2024-2031Global Bioplastics Market - 2024-2031 |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| バイオプラスチックの世界市場-2024-2031 |

|

出版日: 2024年02月09日

発行: DataM Intelligence

ページ情報: 英文 191 Pages

納期: 即日から翌営業日

|

- 全表示

- 概要

- 目次

概要

バイオプラスチックの世界市場は2023年に115億米ドルに達し、2031年には635億米ドルに達すると予測され、予測期間2024-2031年のCAGRは18.4%で成長します。

政府が従来のプラスチックが環境に与える有害な影響に対する認識を高めることを重視するようになったことで、持続可能な代替品への需要が急増しています。植物やバクテリアのような再生可能な資源に由来するバイオプラスチックは、環境問題に対処するための環境に優しいソリューションとして際立っています。バイオプラスチックは、二酸化炭素排出量の削減、化石燃料への依存度の低減、廃棄物の削減に重要な役割を果たしています。

アジア太平洋地域では、中国、日本、インドなどの国々で顕著な市場開拓が行われ、バイオプラスチック市場は著しい成長を遂げています。これらの国々の政府は、プラスチック汚染や気候変動などの環境問題に対する意識を高め、積極的に取り組んでいます。

その一例として、2023年4月28日には、シトロニックやブラスケムのような企業が、再生可能なポリプロピレン(PP)を生産するためにエタノール脱水などの革新的な方法を採用し、ジェノはポリマーの必須構成要素を作り出すために砂糖発酵を利用しています。こうした取り組みは、持続可能な慣行へのパラダイムシフトと、アジア太平洋全域で環境への影響を緩和する極めて重要な要素としてのバイオプラスチックの採用を強調しています。

ダイナミクス

持続可能な包装ソリューションの急増

消費者の嗜好は、環境に優しい慣行を優先し、環境への影響を最小限に抑えるように設計されたパッケージング・ソリューションを提供するブランドへとシフトしています。持続可能なパッケージングに対する消費者の需要の高まりは、より環境に優しい代替パッケージング・ソリューションを提供するバイオプラスチック市場を大きく後押ししています。

例えば、2023年3月6日、インドのケララ州にあるGreenamor Venturesの創設者であるArdra Nair氏は、地元で入手可能なコア廃棄物から得られるバイオプラスチックを利用した環境に優しいパッケージング・ソリューションの開発に成功しました。特に化粧品業界において、従来のパッケージングが環境に与える影響を認識していたArdraの革新的なアプローチは、廃棄物管理という世界の課題に取り組みながら、廃棄物を価値ある資源に変えることを目指しました。この注目すべき例は、持続可能なパッケージング・ソリューションの重要性が増していること、そして環境意識の高い消費者の進化する要求に応えるためにバイオプラスチックが極めて重要な役割を担っていることを強調しています。

生分解性バイオプラスチック:プラスチック汚染への持続可能な対応

従来のプラスチックが環境に与える影響に対する意識の高まりは、生分解性の代替プラスチックを採用する方向へのシフトに拍車をかけています。石油由来の従来のプラスチックは、土壌に長期間残留し、土壌汚染の原因となっています。これに対し、生分解性バイオプラスチックは、分解速度が速いため環境への影響を最小限に抑え、持続可能なソリューションを提供します。

2023年6月11日、ワシントン大学の研究者たちが、一般的にスピルリナとして知られる青緑色シアノバクテリアの粉末を用いたバイオプラスチックを開発しました。この革新的なバイオプラスチックは、裏庭の堆肥箱でバナナの皮と同じような分解速度を示し、従来のプラスチックに代わる環境に優しい代替品となります。特筆すべきは、これらのバイオプラスチックは、使い捨ての石油由来プラスチックに匹敵する機械的特性を維持していることで、現在進行中のプラスチック汚染との戦いにおける持続可能な解決策の有望な道を示しています。

高い製品コスト

バイオプラスチックは、環境に優しいという利点がある一方で、従来のプラスチックに比べ、加工に一定の制限があります。バイオプラスチックの種類によっては、低い加工温度や生産速度の制限など、特殊な条件が必要となる場合があります。さらに、一部のバイオプラスチックは酸素や水分に敏感で、製造時や使用時の安定性に影響を与えます。

バイオプラスチックの採用が課題となっている大きな要因は、従来のプラスチックに比べて製造コストが比較的高いことです。このコスト格差は、原材料や製造工程にかかる費用、経済的資源が限られていることに起因しています。その結果、バイオプラスチックの製造コストが高くなるため、用途によっては経済性が低くなり、様々な産業で広く採用されるハードルとなっています。

目次

第1章 調査手法と調査範囲

第2章 定義と概要

第3章 エグゼクティブサマリー

第4章 市場力学

- 影響要因

- 促進要因

- 持続可能な包装ソリューションの急増

- 生分解性バイオプラスチック:プラスチック汚染に対する持続可能なソリューション

- 抑制要因

- 高い製品コスト

- 機会

- 影響分析

- 促進要因

第5章 産業分析

- ポーターのファイブフォース分析

- サプライチェーン分析

- 価格分析

- 規制分析

- ロシア・ウクライナ戦争の影響分析

- DMIの見解

第6章 COVID-19分析

第7章 タイプ別

- 生分解性

- ポリ乳酸

- デンプンブレンド

- ポリブチレンアジペートテレフタレート(PBAT)

- ポリブチレンサクシネート(PBS)

- その他

- 非生分解性

- ポリエチレン

- ポリエチレンテレフタレート

- ポリアミド

- ポリトリメチレンテレフタレート

- その他

第8章 エンドユーザー別

- パッケージング

- 消費財

- 農業

- 自動車・運輸

- 繊維

第9章 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

第10章 競合情勢

- 競合シナリオ

- 市況/シェア分析

- M&A分析

第11章 企業プロファイル

- Arkema

- 会社概要

- 製品ポートフォリオと説明

- 財務概要

- 主な発展

- BASF

- Bioterra

- Kuraray Europe GmbH

- NatureWorks LLC

- Novamont S.p.A.

- TotalEnergies Corbion

- Braskem

- Mitsubishi Chemical Corporation

- Plantic Technologies Ltd

第12章 付録

Overview

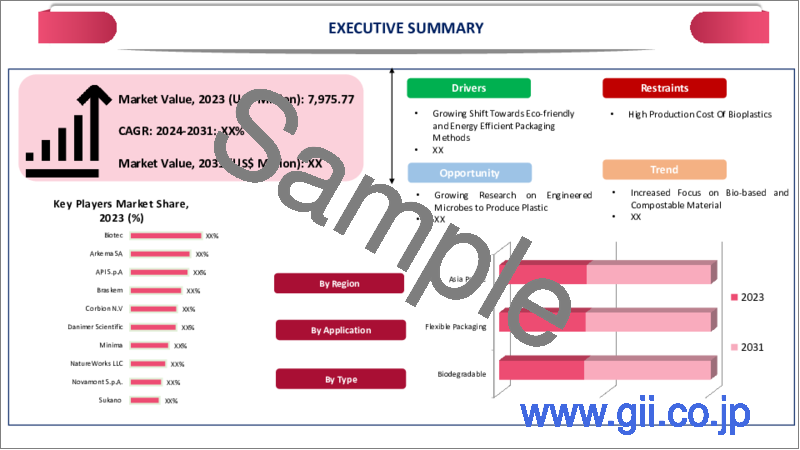

Global Bioplastics Market reached US$ 11.5 billion in 2023 and is expected to reach US$ 63.5 billion by 2031, growing with a CAGR of 18.4% during the forecast period 2024-2031.

The government's heightened emphasis on raising awareness about the detrimental impact of conventional plastics on the environment has spurred a surging demand for sustainable alternatives. Bioplastics, derived from renewable sources like plants or bacteria, stand out as an eco-friendly solution to address environmental concerns. The bioplastics play a vital role in reducing carbon emissions, lessening dependence on fossil fuels and contributing significantly to waste reduction.

Asia-Pacific has experienced remarkable growth in the bioplastic market, with notable developments in countries such as China, Japan and India. The governments in these countries are actively increasing awareness and addressing environmental issues, including plastic pollution and climate change, leading to a substantial uptick in the demand for bioplastics.

As an illustrative example, on April 28, 2023, companies like Citroniq and Braskem have adopted innovative methods, such as ethanol dehydration, to produce renewable polypropylene (PP), while Geno is utilizing sugar fermentation to create essential building blocks for polymers. The initiatives underscore a paradigm shift towards sustainable practices and the adoption of bioplastics as a pivotal component in mitigating environmental impacts across the Asia-Pacific.

Dynamics

Surge in Sustainable Packaging Solutions

Consumer preferences are shifting towards brands that prioritize eco-friendly practices and offer packaging solutions designed to minimize environmental impact. The growing consumer demand for sustainable packaging is significantly boosting the market for bioplastics, which present a more environmentally friendly alternative for packaging solutions.

For instance, on March 6, 2023, Ardra Nair, the founder of Greenamor Ventures in Kerala, India, successfully developed eco-friendly packaging solutions utilizing bioplastics derived from locally available coir waste. Recognizing the environmental repercussions associated with traditional packaging, especially in the cosmetic industry, Ardra's innovative approach aimed to transform waste materials into valuable resources while addressing the global challenge of waste management. The noteworthy example underscores the increasing importance of sustainable packaging solutions and the pivotal role of bioplastics in meeting the evolving demands of environmentally conscious consumers.

Biodegradable Bioplastics: A Sustainable Response to Plastic Pollution

Increasing awareness of the environmental impact of traditional plastics has spurred a shift towards the adoption of biodegradable alternatives. Conventional plastics, derived from petroleum, persist in the soil for extended periods, contributing to soil pollution. In contrast, biodegradable bioplastics offer a sustainable solution by decomposing at a faster rate, minimizing their environmental footprint.

A significant advancement in this realm occurred on June 11, 2023, when researchers at University of Washington developed bioplastics using powdered blue-green cyanobacteria cells, commonly known as spirulina. The innovative bioplastics exhibit a decomposition rate similar to that of a banana peel in backyard compost bins, presenting an eco-friendly alternative to traditional plastics. Notably, these bioplastics maintain mechanical properties comparable to single-use, petroleum-derived plastics, showcasing a promising avenue for sustainable solutions in the ongoing battle against plastic pollution.

High Product Cost

Bioplastics, while offering eco-friendly advantages, are subject to certain limitations in processing compared to their traditional plastic counterparts. Specific conditions, such as lower processing temperatures or restricted production rates, may be necessary for manufacturing certain types of bioplastics. Additionally, some bioplastics exhibit sensitivity to oxygen and moisture, affecting their stability during production and usage.

A significant factor contributing to the challenges of bioplastics adoption is the comparatively higher production cost when compared to conventional plastics. The cost disparity is attributed to the expenses associated with raw materials, manufacturing processes and the limited availability of economic resources. Consequently, the higher production costs associated with bioplastics render them less economically viable for certain applications, posing a hurdle to their widespread adoption in various industries.

Segment Analysis

The global bioplastics market is segmented based on type, end-user and region.

PLA Bioplastics: Renewable, Versatile and EU Taxonomy Compliance

PLA bioplastics are thermoplastic polyester derived from renewable resources that include corn starch, starch and tapioca roots. In 2010 PLA bioplastics is marked as the second most important bioplastics in the world. PLA is biocompatible and also provides the perfect solution for medical implants.

For instance, On 9 Jun 2023, The announcement by the company that its Luminy Polylactic Acid (PLA) bioplastics meet the criteria of the EU Taxonomy Regulation on climate change mitigation and adaptation highlights its significant role in the global sustainable economy. The EU Taxonomy Regulation is crucial for sustainable innovation as it establishes a standard for labeling businesses as 'sustainable' within the European Union.

Geographical Penetration

Growth in Population and Consumer Adoption of Sustainable Material

Asia-Pacific has the largest growth in the bioplastics market. Due to significant growth in the population increases the demand for bioplastics products in this region. Consumers are adopting sustainable materials. People are focusing more on eco-friendly products that reduce plastics. The shift in consumer thinking towards sustainability boosts the growth of the bioplastics market.

For instance, on 25 Sept 2022, news from NHK World Japan, Biodegradable plastics are made up of plant-based materials, these materials gains attraction in various industries including restaurants and food service, due to their eco-friendly properties and ability to degrade in seawater. The bio-plastics, made up from renewable sources such as cornstarch or sugarcane and offers a sustainable alternative to conventional plastics derived from fossil fuels.

Competitive Landscape

The major global players include Arkema, BASF, Bioterra, Kuraray Europe GmbH, NatureWorks LLC, Novamont S.p.A., TotalEnergies Corbion, Braskem, Mitsubishi Chemical Corporation, Plantic Technologies Ltd

COVID-19 Impact Analysis

The pandemic induced widespread disruptions across industries, with the packaging and agricultural sectors experiencing supply chain disturbances due to travel restrictions and lockdowns. The disruptions led to delayed production schedules and shortages in raw materials, posing challenges to the growth of the bioplastics market during the pandemic.

Escalating the predicament, the shortage in development and production of raw materials resulted in increased prices during the pandemic. The economic uncertainty stemming from the global health crisis further translated into reduced investment and funding for various industries, including the bioplastics sector. Financial constraints prompted the postponement or scaling back of projects and research initiatives, casting a shadow on the overall trajectory of the bioplastics market during the challenging times of the pandemic.

By Type

- Biodegradable

- Polylactic Acid

- Starch Blends

- Polybutylene Adipate Terephthalate (PBAT)

- Polybutylene Succinate (PBS)

- Others

- Non-biodegradable

- Polyethylene

- Polyethylene Terephthalate

- Polyamide

- Polytrimethylene Terephthalate

- Others

By End-User

- Packaging

- Consumer goods

- Automotive

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

Key Developments

- On 6 May 2021, TerraVerdae releases its new bioplastic product and the product has three versions blown, injection molding and thermoforming. The launch is for extensive development to produce biodegradable plastics.

- On 26 Oct 2022, Rochling-BioBoom, an international rochling group is launching its two new sustainable products and promoting the usage of biodegradable raw materials.

- On 24 April 2023, Kelpy launches hyper-scalable bioplastics pellets that will replace oil-based plastics. It claim that they are first company that create 100% bio-based product used in rigid packaging.

Why Purchase the Report?

- To visualize the global bioplastics market segmentation based on type, end-user and region as well as understand key commercial assets and players.

- Identify commercial opportunities by analyzing trends and co-development.

- Excel data sheet with numerous data points of bioplastics market-level with all segments.

- PDF report consists of a comprehensive analysis after exhaustive qualitative interviews and an in-depth study.

- Product mapping available as Excel consisting of key products of all the major players.

The global bioplastics market report would provide approximately 53 tables, 57 figures and 191 Pages.

Target Audience 2024

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies

Table of Contents

1. Methodology and Scope

- 1.1. Research Methodology

- 1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

- 3.1. Snippet by Type

- 3.2. Snippet by End-User

- 3.3. Snippet by Region

4. Dynamics

- 4.1. Impacting Factors

- 4.1.1. Drivers

- 4.1.1.1. Surge in Sustainable Packaging Solutions

- 4.1.1.2. Biodegradable Bioplastics: Sustainable Solution for Plastic Pollution

- 4.1.2. Restraints

- 4.1.2.1. High Product Cost

- 4.1.3. Opportunity

- 4.1.4. Impact Analysis

- 4.1.1. Drivers

5. Industry Analysis

- 5.1. Porter's Five Force Analysis

- 5.2. Supply Chain Analysis

- 5.3. Pricing Analysis

- 5.4. Regulatory Analysis

- 5.5. Russia-Ukraine War Impact Analysis

- 5.6. DMI Opinion

6. COVID-19 Analysis

- 6.1. Analysis of COVID-19

- 6.1.1. Scenario Before COVID

- 6.1.2. Scenario During COVID

- 6.1.3. Scenario Post COVID

- 6.2. Pricing Dynamics Amid COVID-19

- 6.3. Demand-Supply Spectrum

- 6.4. Government Initiatives Related to the Market During Pandemic

- 6.5. Manufacturers Strategic Initiatives

- 6.6. Conclusion

7. By Type

- 7.1. Introduction

- 7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

- 7.1.2. Market Attractiveness Index, By Type

- 7.2. Biodegradable*

- 7.2.1. Introduction

- 7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

- 7.2.3. Polylactic Acid

- 7.2.4. Starch Blends

- 7.2.5. Polybutylene Adipate Terephthalate (PBAT)

- 7.2.6. Polybutylene Succinate (PBS)

- 7.2.7. Others

- 7.3. Non-Biodegradable

- 7.3.1. Polyethylene

- 7.3.2. Polyethylene Terephthalate

- 7.3.3. Polyamide

- 7.3.4. Polytrimethylene Terephthalate

- 7.3.5. Others

8. By End-User

- 8.1. Introduction

- 8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

- 8.1.2. Market Attractiveness Index, By End-User

- 8.2. Packaging*

- 8.2.1. Introduction

- 8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

- 8.3. Consumer Goods

- 8.4. Agriculture

- 8.5. Automotive & Transportation

- 8.6. Textile

9. By Region

- 9.1. Introduction

- 9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

- 9.1.2. Market Attractiveness Index, By Region

- 9.2. North America

- 9.2.1. Introduction

- 9.2.2. Key Region-Specific Dynamics

- 9.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

- 9.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

- 9.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 9.2.5.1. U.S.

- 9.2.5.2. Canada

- 9.2.5.3. Mexico

- 9.3. Europe

- 9.3.1. Introduction

- 9.3.2. Key Region-Specific Dynamics

- 9.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

- 9.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

- 9.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 9.3.5.1. Germany

- 9.3.5.2. UK

- 9.3.5.3. France

- 9.3.5.4. Italy

- 9.3.5.5. Spain

- 9.3.5.6. Rest of Europe

- 9.4. South America

- 9.4.1. Introduction

- 9.4.2. Key Region-Specific Dynamics

- 9.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

- 9.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

- 9.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 9.4.5.1. Brazil

- 9.4.5.2. Argentina

- 9.4.5.3. Rest of South America

- 9.5. Asia-Pacific

- 9.5.1. Introduction

- 9.5.2. Key Region-Specific Dynamics

- 9.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

- 9.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

- 9.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 9.5.5.1. China

- 9.5.5.2. India

- 9.5.5.3. Japan

- 9.5.5.4. Australia

- 9.5.5.5. Rest of Asia-Pacific

- 9.6. Middle East and Africa

- 9.6.1. Introduction

- 9.6.2. Key Region-Specific Dynamics

- 9.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

- 9.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

10. Competitive Landscape

- 10.1. Competitive Scenario

- 10.2. Market Positioning/Share Analysis

- 10.3. Mergers and Acquisitions Analysis

11. Company Profiles

- 11.1. Arkema*

- 11.1.1. Company Overview

- 11.1.2. Product Portfolio and Description

- 11.1.3. Financial Overview

- 11.1.4. Key Developments

- 11.2. BASF

- 11.3. Bioterra

- 11.4. Kuraray Europe GmbH

- 11.5. NatureWorks LLC

- 11.6. Novamont S.p.A.

- 11.7. TotalEnergies Corbion

- 11.8. Braskem

- 11.9. Mitsubishi Chemical Corporation

- 11.10. Plantic Technologies Ltd

LIST NOT EXHAUSTIVE

12. Appendix

- 12.1. About Us and Services

- 12.2. Contact Us