|

|

市場調査レポート

商品コード

1401305

航空宇宙用アドバンストセラミックスの世界市場:2023年~2030年Global Aerospace Advanced Ceramics Market - 2023-2030 |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空宇宙用アドバンストセラミックスの世界市場:2023年~2030年 |

|

出版日: 2023年12月29日

発行: DataM Intelligence

ページ情報: 英文 191 Pages

納期: 即日から翌営業日

|

- 全表示

- 概要

- 目次

概要

航空宇宙用アドバンストセラミックスの世界市場は、2022年に8億米ドルに達し、2023~2030年の予測期間中にCAGR 4.8%で成長し、2030年には12億米ドルに達すると予測されています。

航空機事業では持続可能性が重視されるようになり、特に二酸化炭素排出量の削減と環境性能の向上に重点が置かれています。アドバンストセラミックスは丈夫で軽いため、燃料消費量の少ない航空機の設計に役立ち、環境プログラムをサポートします。民間および防衛航空宇宙用途の両方において持続可能性がますます重要になるにつれて、アドバンストセラミックスのニーズは高まると予想されます。

航空宇宙用アドバンストセラミックス市場は、近代化要求や地政学的要因によって世界中で防衛予算が増加していることもあり、拡大しています。アドバンストセラミックスは、高温に耐える材料を必要とする軍用機や防衛システムのようなシステムに最適です。航空宇宙分野における防衛能力への要求の高まりが、高機能セラミックへの需要を押し上げています。

アジア太平洋は、世界の航空宇宙用アドバンストセラミックス市場の1/3以上を占める成長地域の一つです。アジア太平洋の航空機産業は、特に中国とインドで急速に拡大しています。民間および防衛航空機産業における支出の増加は、アドバンストセラミックスに対するニーズの高まりに寄与しています。この材料は、現代の航空技術の進歩を可能にする高性能で軽量な部品の生産に不可欠です。

市場力学

エンジン部品の高温耐性

高温に耐えるアドバンストセラミックスの能力は、航空機、特にエンジン部品の製造に使用される重要な要因です。航空エンジンは灼熱の環境で作動するため、炭化ケイ素や窒化ケイ素のようなアドバンストセラミックスは、顕著な熱安定性と耐熱性を提供します。これらのセラミックスは航空エンジンの極度の熱に耐えることができるため、エンジンの信頼性と効率が向上します。

例えば、2022年、アルテミス・キャピタル・パートナーズは、管状セラミックスと部品の開発と製造を専門とするマクダネル・アドバンスト・セラミック・テクノロジーズを買収しました。McDanelの製品群は、高温環境、腐食性の強い環境、厳しい衝撃環境で効果的に機能するよう特別に設計されています。

航空宇宙分野での軽量材料の需要増加

航空宇宙用途のアドバンストセラミックスの世界市場は、航空宇宙産業の軽量材料に対する需要の高まりが主な要因となっています。アドバンストセラミックスは、その卓越した強度対重量比のため、燃料効率を高め、航空機全体の重量を減らそうとしている航空セクターの可能な答えです。

例えば、2022年、先進セラミックスの大手メーカーであるシントックス・テクノロジーズ社は、テクノロジー・アセスメント・アンド・トランスファー社を買収しました。この戦略的買収は、航空宇宙、防衛、バイオメディカル市場におけるシンクスの能力を大幅に強化し、多様化と強化における重要な一歩となった。この買収は、高度な製造技術を導入し、SINTXのセラミック材料プラットフォームを拡大するもので、同社をさらなる革新に向けて位置づけるものです。

先端セラミックスの高コスト

先端セラミック材料の製造・加工コストが高いことは、航空宇宙分野で使用される先端セラミックの世界市場にとって大きな障壁となっています。適切な品質を得るためには、セラミックスは精密成形、焼結、頻繁に行われる特殊処理などの複雑な手順を用いて製造されなければならないです。

こうした複雑な製造手順と高い製造コストのため、アドバンストセラミックスは従来の材料よりもコストが高いです。厳しい予算制限に直面することの多い航空宇宙分野では、高度なセラミックスを広く使用することは難しいかもしれません。法外な材料費は、改良された性能特徴にもかかわらず、アドバンストセラミックスの広範な使用を制限し、航空宇宙プロジェクトの全体的な費用対効果に影響を与える可能性があります。

限られた設計の柔軟性

特定の金属合金と比較して、これらの材料の制限された設計の柔軟性は、世界の航空宇宙アドバンストセラミックス市場の成長の重要な障害です。セラミックスは優れた機械的・熱的性質を持つが、固有の脆さのため、複雑な形状や構造に成形することは難しいかもしれないです。

特に、複雑で特注の部品が頻繁に必要とされる航空宇宙用途では、設計の柔軟性の欠如が大きな問題となる可能性があります。アドバンストセラミックスは、設計上の制約により、最高の性能を発揮するために複雑な形状が必要とされる重要な部品では、汎用性が低い場合があります。

目次

第1章 調査手法と調査範囲

第2章 定義と概要

第3章 エグゼクティブサマリー

第4章 市場力学

- 影響要因

- 促進要因

- エンジン部品の高温耐性

- 航空宇宙分野における軽量材料の需要増加

- 抑制要因

- アドバンストセラミックスの高コスト

- 設計の柔軟性に限界がある

- 機会

- 影響分析

- 促進要因

第5章 産業分析

- ポーターのファイブフォース分析

- サプライチェーン分析

- 価格分析

- 規制分析

- ロシア・ウクライナ戦争の影響分析

- DMIの見解

第6章 COVID-19分析

第7章 材料別

- アルミナ

- チタン酸塩

- ジルコニア

- フェライト

- 窒化アルミニウム

- 炭化ケイ素

- 窒化ケイ素

- その他

第8章 航空機タイプ別

- 民間航空機

- 軍用機

- 一般航空機

第9章 用途別

- エレクトロニクス・制御システム

- センサー

- アンテナ

- コンデンサ

- 抵抗器

- コネクター

- その他

- 構造部品

- ベアリング

- シール

- インシュレーター

- その他

- エンジン部品

- タービンブレード

- ノズル

- 燃焼ライナー

- その他

- その他

第10章 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

第11章 競合情勢

- 競合シナリオ

- 市況/シェア分析

- M&A分析

第12章 企業プロファイル

- Kyocera Corporation

- 会社概要

- 製品ポートフォリオと説明

- 財務概要

- 主な発展

- CeramTec

- CoorsTek Inc.

- Morgan Advanced Materials

- Saint-Gobain Ceramic Materials

- 3M

- McDanel Advanced Ceramic Technologies

- Corning Incorporated

- LSP Industrial Ceramics, Inc.

- Momentive Performance Materials Inc.

第13章 付録

Overview

Global Aerospace Advanced Ceramics Market reached US$ 0.8 billion in 2022 and is expected to reach US$ 1.2 billion by 2030, growing with a CAGR of 4.8% during the forecast period 2023-2030.

There is a rising emphasis on sustainability in the aircraft business, with a particular focus on lowering carbon emissions and enhancing environmental performance overall. Because advanced ceramics are strong and light, they help design airplanes that use less fuel and support environmental programs. The need for advanced ceramics is anticipated to increase as sustainability becomes more and more important for both commercial and defense aerospace applications.

The aerospace advanced ceramics market is expanding due in part to growing defense budgets around the globe, which are being driven by modernization demands and geopolitical factors. Advanced ceramics are perfect for systems like military aircraft and defense systems that need materials that can withstand high temperatures. The increasing requirement for defensive capabilities in the aerospace sector is driving up demand for sophisticated ceramics.

Asia-Pacific is among the growing regions in the global aerospace advanced ceramics market covering more than 1/3rd of the market. Asia-Pacific's aircraft industry is expanding rapidly, particularly in China and India. Increasing expenditures in the commercial and defense aircraft industries contribute to the growing need for advanced ceramics. The materials are essential to the production of high-performance, lightweight parts that enable the advancement of contemporary aviation technology.

Dynamics

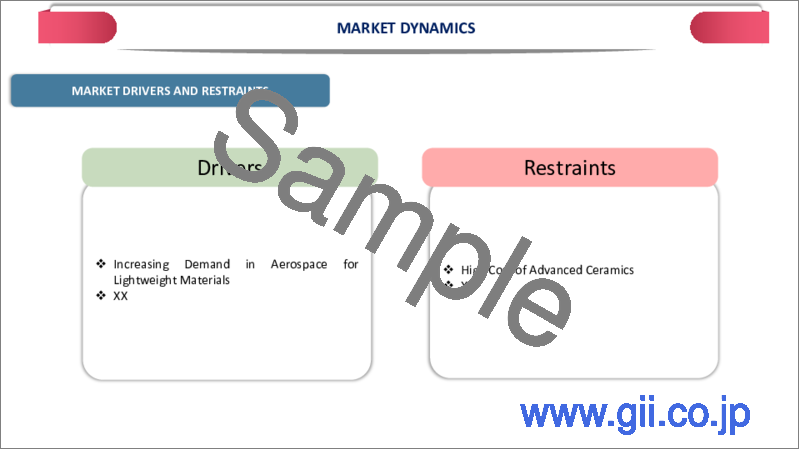

Resistance to High Temperatures in Engine Components

The capability of advanced ceramics to survive high temperatures is a key factor in their use in aircraft, especially in producing engine components. Since aviation engines work in scorching environments, advanced ceramics like silicon carbide and nitride offer remarkable thermal stability and heat resistance. Because these ceramics can endure the extreme heat of aviation engines, engine dependability and efficiency are raised.

For Instance, in 2022, Artemis Capital Partners acquired McDanel Advanced Ceramic Technologies, a company specializing in the development and manufacturing of tubular ceramics and components. McDanel's product range is specifically engineered to function effectively in high-temperature settings, aggressive corrosive conditions and severe shock environments.

Increasing Demand in Aerospace for Lightweight Materials

The global market for advanced ceramics for aerospace applications is mostly driven by the aerospace industry's rising demand for lightweight materials. Advanced ceramics are a possible answer for the aviation sector, which is attempting to enhance fuel efficiency and lower overall aircraft weight, because of their exceptional strength-to-weight ratio.

For Instance, in 2022, SINTX Technologies, Inc., a leading advanced ceramics manufacturer acquired Technology Assessment and Transfer, Inc. The strategic move significantly strengthens SINTX's capabilities in the aerospace, defense and biomedical markets, marking a crucial step in diversification and fortification. The acquisition introduces advanced manufacturing technologies and expands SINTX's ceramic material platforms, positioning the company for increased innovation.

High Cost of Advanced Ceramics

The high cost of producing and processing advanced ceramic materials is a major barrier to the globally market for advanced ceramics used in aerospace. To acquire the appropriate qualities, ceramics must be manufactured using complex procedures such as precision shape, sintering and frequently specific treatments.

Because of these intricate manufacturing procedures and higher production costs, advanced ceramics are more costly than conventional materials. It could be difficult for the aerospace sector, which frequently faces strict budgetary restrictions, to widely use sophisticated ceramics. Exorbitant material costs have the potential to restrict the broad use of advanced ceramics despite their improved performance features and affect the overall cost-effectiveness of aerospace projects.

Limited Design Flexibility

The restricted design flexibility of these materials in comparison to specific metal alloys is a significant impediment to the growth of the globally aerospace advanced ceramics market. Although ceramics have great mechanical and thermal qualities, shaping them into intricate shapes or structures may be difficult due to their inherent brittleness.

The lack of design flexibility can be a big problem, particularly for aerospace applications where complex and bespoke parts are frequently needed. Advanced ceramics may not be as versatile as they may be in some crucial components where complicated geometries are necessary for best performance due to design restrictions.

Segment Analysis

The global aerospace advanced ceramics market is segmented based on material, aircraft type, application and region.

Increasing Electronic Components and Aircraft Applications

The electronics & control system segment is among the growing regions in the global Aerospace advanced ceramics market covering more than 1/3rd of the market. The growing integration of electronics and control systems in contemporary aircraft is driving the expansion of the global aerospace advanced ceramics market. Advanced ceramics are to manufacture electronic components such as sensors, connections and substrates because of their lightweight design and ability to withstand high temperatures.

The increasing emphasis on downsizing, fuel efficiency and dependability by aircraft manufacturers has made ceramics indispensable for accomplishing these goals in electronic systems. It are essential for the harsh environments of aircraft applications because of their superior thermal management and electrical insulation qualities, guaranteeing the durability and effectiveness of avionics and control systems.

Geographical Penetration

Rising Demand for Aerospace Production Capacities in Asia-Pacific

Asia-Pacific has been a dominant force in the global aerospace advanced ceramics market. Due to factors that support the rising demand for these materials, the Asia-Pacific has emerged as a major growth engine in the global aerospace advanced ceramics market. One important contributing lead to is the fast-growing aerospace and defense sectors in countries like India and China.

Advanced ceramics are becoming more and more needed in components like engine parts, avionics and structural elements since both countries have invested heavily in bolstering their defense capabilities and expanding their aerospace manufacturing capability. Furthermore, the aircraft industry's rising focus on lightweight materials and fuel economy has sped up the use of advanced ceramics.

The Asia-Pacific is projected to have substantial development in the demand for advanced ceramics as a result of governments expanding their fleets and modernizing their aviation infrastructure. In addition, the electronics sector is growing in the Asia-Pacific and sophisticated ceramics are utilized in electronic components including avionics sensors and connections.

The demand for sophisticated ceramics in this area is projected to rise as long as technical developments in aerospace and defense electronics persist. Taken together, more aerospace spending, an emphasis on fuel-efficient technologies and a robust electronics industry position Asia-Pacific as a key growth engine for the globally aerospace advanced ceramics market.

COVID-19 Impact Analysis

The COVID-19 pandemic affected numerous industries, including the global market for advanced ceramics in aircraft. The pandemic caused production and demand interruptions in the aircraft industry. Lockdowns and other restrictions brought air traffic to a virtual halt, making it difficult for many aircraft industries to keep up with production deadlines.

The demand for sophisticated ceramics employed in several aircraft applications, including engine parts, structural components and avionics, was directly impacted by this in turn. The aerospace supply chain was negatively impacted by the drop in air travel and the subsequent drop in demand for new aircraft. Aerospace enterprises, encompassing those producing sophisticated ceramics, encountered fiscal difficulties and operational obstacles.

Numerous businesses were forced to review their production schedules and some projects were postponed or delayed. The uncertainty surrounding the intensity and duration of the pandemic complicated the industry's strategic decision-making, which affected investments in advanced ceramic technology research and development.

The pandemic however drew attention to the significance of lightweight, robust materials for aircraft applications, which may stimulate further research and development in the field of advanced ceramics. The market for aerospace advanced ceramics may see growth as the aviation sector steadily improves and there is a need for new, fuel-efficient aircraft.

Russia-Ukraine War Impact Analysis

The aerospace sector is extremely susceptible to geopolitical developments and any unrest or war has the potential to sabotage the world's supply chain. Advanced ceramics are crucial in aircraft applications because they are strong, lightweight and resistant to high temperatures.

If the conflict between Russia and Ukraine worsens or sparks more widespread geopolitical tensions, the aerospace sector might see interruptions to production schedules and the supply chain for essential materials and components, such as sophisticated ceramics. Market dynamics and investment decisions may also be impacted by elevated levels of uncertainty and geopolitical threats.

Furthermore, trade restrictions or economic sanctions against Russia or Ukraine may have a domino impact on international industry. Obtaining supplies or components from impacted areas may provide difficulties for aerospace manufacturers, which might cause delays and higher expenses. Determinations on R&D, collaborations and capital investments may be impacted by changes in investor confidence and the general mood of the market in the aerospace industry.

By Material

- Alumina

- Titanate

- Zirconia

- Ferrite

- Aluminum Nitride

- Silicon Carbide

- Silicon Nitride

- Others

By Aircraft Type

- Commercial Aircraft

- Military Aircraft

- General Aviation

By Application

- Electronics & Control System

- Sensors

- Antennas

- Capacitors

- Resistors

- Connectors

- Others

- Structural Components

- Bearings

- Seals

- Insulators

- Others

- Engine Components

- Turbine Blades

- Nozzles

- Combustion Liners

- Others

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

Key Developments

- On July 22, 2021, The Midlands Industrial Ceramics Group (MICG) secured £18.27 million in government funding, paving the way for the creation of numerous job opportunities. The financial support is expected to catalyze additional investments from MICG's partners, thereby unlocking prospects for the subsequent phase of development of a cutting-edge Advanced Ceramics Campus located in North Staffordshire.

Competitive Landscape

The major global players in the market include Kyocera Corporation, CeramTec, CoorsTek Inc., Morgan Advanced Materials, Saint-Gobain Ceramic Materials, 3M, McDanel Advanced Ceramic Technologies, Corning Incorporated, LSP Industrial Ceramics, Inc. and Momentive Performance Materials Inc.

Why Purchase the Report?

- To visualize the global aerospace advanced ceramics market segmentation based on material, aircraft type, application and region and understand key commercial assets and players.

- Identify commercial opportunities by analyzing trends and co-development.

- Excel data sheet with numerous data points of aerospace advanced ceramics market-level with all segments.

- PDF report consists of a comprehensive analysis after exhaustive qualitative interviews and an in-depth study.

- Product mapping available as Excel consisting of key products of all the major players.

The global aerospace advanced ceramics market report would provide approximately 61 tables, 63 figures and 191 Pages.

Target Audience 2023

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies

Table of Contents

1. Methodology and Scope

- 1.1. Research Methodology

- 1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

- 3.1. Snippet by Material

- 3.2. Snippet by Aircraft Type

- 3.3. Snippet by Application

- 3.4. Snippet by Region

4. Dynamics

- 4.1. Impacting Factors

- 4.1.1. Drivers

- 4.1.1.1. Resistance to High Temperatures in Engine Components

- 4.1.1.2. Increasing Demand in Aerospace for Lightweight Materials

- 4.1.2. Restraints

- 4.1.2.1. High Cost of Advanced Ceramics

- 4.1.2.2. Limited Design Flexibility

- 4.1.3. Opportunity

- 4.1.4. Impact Analysis

- 4.1.1. Drivers

5. Industry Analysis

- 5.1. Porter's Five Force Analysis

- 5.2. Supply Chain Analysis

- 5.3. Pricing Analysis

- 5.4. Regulatory Analysis

- 5.5. Russia-Ukraine War Impact Analysis

- 5.6. DMI Opinion

6. COVID-19 Analysis

- 6.1. Analysis of COVID-19

- 6.1.1. Scenario Before COVID

- 6.1.2. Scenario During COVID

- 6.1.3. Scenario Post COVID

- 6.2. Pricing Dynamics Amid COVID-19

- 6.3. Demand-Supply Spectrum

- 6.4. Government Initiatives Related to the Market During Pandemic

- 6.5. Manufacturers Strategic Initiatives

- 6.6. Conclusion

7. By Material

- 7.1. Introduction

- 7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

- 7.1.2. Market Attractiveness Index, By Material

- 7.2. Alumina*

- 7.2.1. Introduction

- 7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

- 7.3. Titanate

- 7.4. Zirconia

- 7.5. Ferrite

- 7.6. Aluminum Nitride

- 7.7. Silicon Carbide

- 7.8. Silicon Nitride

- 7.9. Others

8. By Aircraft Type

- 8.1. Introduction

- 8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Aircraft Type

- 8.1.2. Market Attractiveness Index, By Aircraft Type

- 8.2. Commercial Aircraft*

- 8.2.1. Introduction

- 8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

- 8.3. Military Aircraft

- 8.4. General Aviation

9. By Application

- 9.1. Introduction

- 9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 9.1.2. Market Attractiveness Index, By Application

- 9.2. Electronics & Control System*

- 9.2.1. Introduction

- 9.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

- 9.2.3. Sensors

- 9.2.4. Antennas

- 9.2.5. Capacitors

- 9.2.6. Resistors

- 9.2.7. Connectors

- 9.2.8. Others

- 9.3. Structural Components

- 9.3.1. Bearings

- 9.3.2. Seals

- 9.3.3. Insulators

- 9.3.4. Others

- 9.4. Engine Components

- 9.4.1. Turbine Blades

- 9.4.2. Nozzles

- 9.4.3. Combustion Liners

- 9.4.4. Others

- 9.5. Others

10. By Region

- 10.1. Introduction

- 10.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

- 10.1.2. Market Attractiveness Index, By Region

- 10.2. North America

- 10.2.1. Introduction

- 10.2.2. Key Region-Specific Dynamics

- 10.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

- 10.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Aircraft Type

- 10.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 10.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 10.2.6.1. U.S.

- 10.2.6.2. Canada

- 10.2.6.3. Mexico

- 10.3. Europe

- 10.3.1. Introduction

- 10.3.2. Key Region-Specific Dynamics

- 10.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

- 10.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Aircraft Type

- 10.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 10.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 10.3.6.1. Germany

- 10.3.6.2. UK

- 10.3.6.3. France

- 10.3.6.4. Russia

- 10.3.6.5. Spain

- 10.3.6.6. Rest of Europe

- 10.4. South America

- 10.4.1. Introduction

- 10.4.2. Key Region-Specific Dynamics

- 10.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

- 10.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Aircraft Type

- 10.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 10.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 10.4.6.1. Brazil

- 10.4.6.2. Argentina

- 10.4.6.3. Rest of South America

- 10.5. Asia-Pacific

- 10.5.1. Introduction

- 10.5.2. Key Region-Specific Dynamics

- 10.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

- 10.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Aircraft Type

- 10.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 10.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 10.5.6.1. China

- 10.5.6.2. India

- 10.5.6.3. Japan

- 10.5.6.4. Australia

- 10.5.6.5. Rest of Asia-Pacific

- 10.6. Middle East and Africa

- 10.6.1. Introduction

- 10.6.2. Key Region-Specific Dynamics

- 10.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

- 10.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Aircraft Type

- 10.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

11. Competitive Landscape

- 11.1. Competitive Scenario

- 11.2. Market Positioning/Share Analysis

- 11.3. Mergers and Acquisitions Analysis

12. Company Profiles

- 12.1. Kyocera Corporation*

- 12.1.1. Company Overview

- 12.1.2. Product Portfolio and Description

- 12.1.3. Financial Overview

- 12.1.4. Key Developments

- 12.2. CeramTec

- 12.3. CoorsTek Inc.

- 12.4. Morgan Advanced Materials

- 12.5. Saint-Gobain Ceramic Materials

- 12.6. 3M

- 12.7. McDanel Advanced Ceramic Technologies

- 12.8. Corning Incorporated

- 12.9. LSP Industrial Ceramics, Inc.

- 12.10. Momentive Performance Materials Inc.

LIST NOT EXHAUSTIVE

13. Appendix

- 13.1. About Us and Services

- 13.2. Contact Us