|

|

市場調査レポート

商品コード

1759280

尖圭コンジローマ市場- 世界および地域別分析:国別・地域別分析 - 分析と予測(2025年~2035年)Genital Warts Market - A Global and Regional Analysis: Focus on Country and Region - Analysis and Forecast, 2025-2035 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 尖圭コンジローマ市場- 世界および地域別分析:国別・地域別分析 - 分析と予測(2025年~2035年) |

|

出版日: 2025年06月30日

発行: BIS Research

ページ情報: 英文 100 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

尖圭コンジローマは、ヒトパピローマウイルス(HPV)の特定の株、特に低リスク株とされるHPV6型と11型によって引き起こされる一般的な性感染症(STI)です。

これらの疣贅は通常、性器、肛門、口腔領域に小さな肉色の隆起や増殖として現れます。がん化することはありませんが、尖圭コンジローマは、その目に見える性質と、しばしば性病に関連する汚名のために、大きな不快感、かゆみ、精神的苦痛を引き起こす可能性があります。

HPVは感染力が強く、通常、膣、肛門、オーラルセックスを含む性行為中の皮膚同士の接触によって感染します。尖圭コンジローマは治療可能ですが、根本的なHPV感染を治療する方法はなく、治療後も再発することがあります。一般的な治療法としては、外用薬、凍結療法、レーザー療法、場合によっては外科的切除などがあります。HPVワクチン接種は最も効果的な予防法であり、尖圭コンジローマとHPV関連がんの両方のリスクを大幅に減少させる。コンドームの継続的な使用など、安全な性行為もリスクを低下させるが、ゼロにすることはできません。

尖圭コンジローマ市場の主な促進要因のひとつは、HPVワクチン接種と効果的な治療オプションに対する需要の高まりです。HPV関連疾患と尖圭コンジローマの関連リスクに対する認識が高まるにつれ、HPVワクチンなどの予防措置の採用が大幅に増加しています。ガーダシルやサーバリックスのようなワクチンは、尖圭コンジローマの原因となるHPVの最も一般的な株を予防するもので、世界的に公衆衛生プログラムや定期接種スケジュールに広く組み込まれるようになってきています。

このようなワクチン接種の急増は、新たなHPV感染の減少につながり、その結果、外用薬、凍結療法、レーザー治療などの治療需要に影響を及ぼしています。しかし、尖圭コンジローマは性的に活発な人々、特に30歳未満の人々の間で依然として流行しているため、診断サービス、治療オプション、予防医療に対する需要は引き続き伸びています。

尖圭コンジローマ市場の成長にもかかわらず、いくつかの課題がその進展を妨げ続けています。主な課題の一つは、HPVや尖圭コンジローマを含む性感染症(STI)を取り巻く偏見と社会的タブーです。STIにまつわる社会的な偏見により、性器いぼの治療を受けることを恥ずかしく感じたり、躊躇したりする人は少なくないです。その結果、ヘルスケア提供者に症状を話すことを避けたり、症状が悪化するまで助けを求めなかったりするため、診断や治療が遅れる可能性があります。

もう一つの大きな課題は、尖圭コンジローマやその他のHPV関連疾患の予防におけるHPVワクチン接種の有効性に関する認識不足です。ガーダシルやサーバリックスのようなワクチンが利用可能であるにもかかわらず、一部の人々はワクチンの利点を知らないままであったり、誤った情報や安全性への不安のためにワクチン接種をためらうことがあります。このことが、特にワクチンや健康教育へのアクセスが限られている新興諸国など、特定の地域におけるワクチン接種率の低下の一因となっています。

さらに、尖圭コンジローマに対する治療の選択肢は存在するもの、侵襲的であったり、痛みを伴ったり、複数回の治療が必要であったりするため、患者のアドヒアランスが低いこともあります。凍結療法、レーザー治療、外科手術は効果的かもしれないが、不快感、回復時間、高額な費用を伴うことが多く、患者の治療意欲を削いでしまう。局所治療も場合によっては効果が低く、患者の不満の一因となっています。

最後に、感染症の再発は依然として課題です。初期治療が成功しても、尖圭コンジローマが再発することがあり、継続的な治療が必要となり、ヘルスケアコストが増加します。根本的なHPV感染に対する治療法がないため、尖圭コンジローマの患者は、再発を繰り返しながら、しばしば精神的・肉体的な負担に直面しながら、病状を管理し続けなければならないです。このような要因が、尖圭コンジローマ市場の継続的な開拓と利用可能性に大きな障害をもたらしています。

世界の尖圭コンジローマ市場は競争が激しく、複数の主要企業が技術革新と市場成長を牽引しています。Verrica Pharmaceuticals、Novan Inc.、Aresus Pharma、AbbVie Inc.などの企業が市場の拡大に積極的に貢献しています。これらの企業は、イミキモド、シネカテキン(Veregen)のような局所治療薬や、免疫調節機構と抗ウイルス機構を活用したVP-102(Verrica Pharmaceuticals)やSB204(Novan Inc.)のような新しい革新的治療薬など、HPV誘発性尖圭コンジローマに対する効果的な治療法の開発に注力しています。

尖圭コンジローマの発症におけるHPVの役割に対する認識が高まる中、これらの企業は、より簡便で侵襲性が低く効果的な解決策を提供することにより、患者のアドヒアランスと治療成績の改善に取り組んでいます。さらに、これらの企業が主導するHPVワクチン接種プログラムや健康教育キャンペーンは、尖圭コンジローマの長期的な負担を軽減し、市場の成長にさらに貢献しています。継続的な研究開発およびコラボレーションを通じて、これらの企業は性器いぼの治療と予防の未来を形成しています。

市場セグメンテーション:

セグメンテーション1:地域別

- 北米

- 欧州

- アジア太平洋

世界の尖圭コンジローマ市場は、予防、治療、公衆衛生イニシアチブの展望を再構築しているいくつかの重要な要因に後押しされ、大きな変革期を迎えています。主な促進要因の一つは、尖圭コンジローマを含むHPV関連疾患の発生率を減少させるのに非常に効果的なHPVワクチン接種プログラムの採用が増加していることです。ガーダシルやサーバリックスのようなワクチンは、尖圭コンジローマの原因となるHPVの最も一般的な株を予防し、新たな感染の減少、ひいては治療法の必要性の減少につながります。ワクチン接種プログラムに女児と男児の両方を含めることで、こうしたイニシアチブの効果はさらに拡大しています。

もうひとつの変革要因は、特に公衆衛生キャンペーンや教育的イニシアティブを通じて、HPVや尖圭コンジローマに対する認識が高まっていることです。HPV感染のリスクについて多くの人々が知るようになり、予防(ワクチン接種)と治療(凍結療法、レーザー治療、局所治療など)の両方の選択肢が利用できるようになったため、市場では診断サービスと治療介入の両方に対する需要が増加しています。

低侵襲治療やより効果的な治療法の開発が進んでいることも、市場の変革に寄与しています。レーザー治療や免疫療法のような低侵襲技術の革新は、患者により快適で便利な治療選択肢を提供し、患者の満足度向上と治療レジメンの遵守につながっています。さらに、経口抗ウイルス治療が尖圭コンジローマを管理する有望な選択肢として台頭しており、患者が治療を受けやすくなっています。

最後に、男性の健康への関心が高まり、HPVが男女双方に与える影響が認識されるようになったことが、より広範な世界的ワクチン接種・治療戦略に寄与しています。より多くの男性がHPVワクチン接種プログラムに参加するようになれば、尖圭コンジローマの発生率は低下し、市場の成長をさらに促進すると予想されます。

サマリーをまとめると、尖圭コンジローマ市場は、HPVワクチン接種プログラムの増加、意識と教育の高まり、治療技術の進歩、包括的な予防ヘルスケアへの注目の高まりに牽引され、変貌を遂げています。これらの要因により、予防措置の範囲が拡大し、治療成績が向上し、尖圭コンジローマおよびHPV関連疾患との闘いにおける公衆衛生全体が強化されています。

当レポートでは、世界の尖圭コンジローマ市場について調査し、市場の概要とともに、国別・地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

第1章 世界の尖圭コンジローマ市場:業界見通し

- イントロダクション

- 市場動向

- 規制の枠組み

- 疫学分析

- 臨床試験分析

- 市場力学

第2章 世界の尖圭コンジローマ市場(地域別)、2023年~2035年

- 北米

- 欧州

- アジア太平洋

第3章 世界の尖圭コンジローマ市場:競合情勢と企業プロファイル

- 主要戦略と開発

- 合併と買収

- 相乗効果のある活動

- 事業拡大と資金調達

- 製品の発売と承認

- その他の活動

- 企業プロファイル

- Verrica Pharmaceuticals

- Tamir Biotechnology

- Novan Inc.

- Medicis Pharmaceuticals

- Aresus Pharma

- AbbVie Inc.

第4章 調査手法

List of Figures

- Figure: Global Genital Warts Market (by Region), $Billion, 2024 and 2035

- Figure: Global Genital Warts Market Key Trends, Analysis

List of Tables

- Table: Global Genital Warts Market Dynamics, Impact Analysis

- Table: Global Genital Warts Market (by Region), $Billion, 2024-2035

Global Genital Warts Market, Analysis and Forecast: 2025-2035

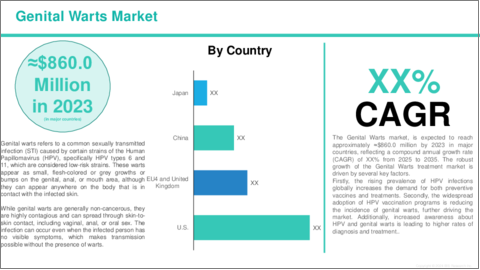

Genital warts are a common sexually transmitted infection (STI) caused by certain strains of the Human Papillomavirus (HPV), particularly HPV types 6 and 11, which are considered low-risk strains. These warts typically appear as small, flesh-colored bumps or growths on the genital, anal, or oral areas. While they are not cancerous, genital warts can cause significant discomfort, itching, and emotional distress due to their visible nature and the stigma often associated with STIs.

HPV is highly contagious and is usually transmitted through skin-to-skin contact during sexual activity, including vaginal, anal, and oral sex. Although genital warts can be treated, there is no cure for the underlying HPV infection, and warts may recur even after treatment. Common treatment options include topical medications, cryotherapy, laser therapy, and in some cases, surgical removal. HPV vaccination is the most effective method of prevention, significantly reducing the risk of both genital warts and HPV-related cancers. Safe sexual practices, such as consistent condom use, can also lower the risk, though they do not eliminate it.

One of the key drivers of the genital warts market is the growing demand for HPV vaccination and effective treatment options. With increasing awareness about HPV-related diseases and the associated risks of genital warts, there has been a significant rise in the adoption of preventive measures such as the HPV vaccine. Vaccines like Gardasil and Cervarix, which protect against the most common strains of HPV responsible for genital warts, are gaining widespread integration into public health programs and routine vaccination schedules globally.

This surge in vaccination efforts has led to a decline in new HPV infections, which in turn has affected the demand for treatments like topical medications, cryotherapy, and laser therapy. However, as genital warts remain prevalent among sexually active individuals, particularly those under 30, the demand for diagnostic services, treatment options, and preventive care continues to grow.

Despite the growth of the Genital Warts market, several challenges continue to hinder its progress. One of the primary challenges is the stigma and societal taboos surrounding sexually transmitted infections (STIs), including HPV and genital warts. Many individuals may feel embarrassed or reluctant to seek treatment for genital warts due to the social stigma associated with STIs. This can result in delayed diagnosis and treatment, as people may avoid discussing their symptoms with healthcare providers or may not seek help until the condition worsens.

Another significant challenge is the lack of awareness about the effectiveness of HPV vaccination in preventing genital warts and other HPV-related diseases. Despite the availability of vaccines like Gardasil and Cervarix, some people remain unaware of the vaccine's benefits or may be hesitant to receive it due to misinformation or fears about safety. This contributes to lower vaccination rates in certain regions, particularly in developing countries, where access to vaccines and health education is limited.

Additionally, while treatment options for genital warts exist, they can sometimes be invasive, painful, or require multiple sessions, leading to poor patient adherence. Cryotherapy, laser treatments, and surgical options may be effective, but they often involve discomfort, recovery time, and high costs, which can discourage patients from pursuing treatment. Topical treatments may also be less effective in some cases, contributing to patient dissatisfaction.

Lastly, recurrent infections remain a challenge. Even with successful initial treatments, genital warts can reappear, leading to ongoing treatment needs and increased healthcare costs. The lack of a cure for the underlying HPV infection means that individuals with genital warts must continue to manage their condition, often facing emotional and physical strain as they navigate recurrent outbreaks. These factors collectively pose significant hurdles in the ongoing development and accessibility of the genital warts market.

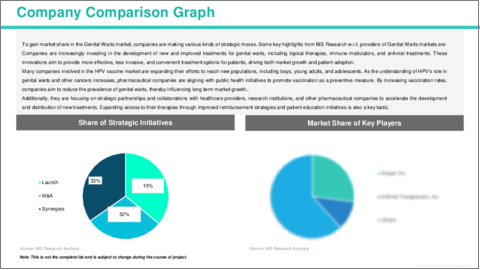

The global Genital Warts market is highly competitive, with several leading companies driving innovation and market growth. Companies such as Verrica Pharmaceuticals, Novan Inc., Aresus Pharma, and AbbVie Inc. are actively contributing to the expansion of the market. These companies focus on developing effective treatments for HPV-induced genital warts, including topical treatments like Imiquimod, sinecatechins (Veregen), and new innovative therapies like VP-102 (Verrica Pharmaceuticals) and SB204 (Novan Inc.), which leverage immune modulatory and antiviral mechanisms.

With a growing awareness of the role of HPV in the development of genital warts, these companies are working to improve patient adherence and treatment outcomes by offering more convenient, less invasive, and effective solutions. Additionally, HPV vaccination programs and health education campaigns led by these firms further contribute to the market's growth, reducing the long-term burden of genital warts. Through continuous research, development, and collaboration, these companies are shaping the future of genital warts treatment and prevention.

Market Segmentation:

Segmentation 1: by Region

- North America

- Europe

- Asia-Pacific

The global Genital Warts market is undergoing significant transformation, fueled by several key factors that are reshaping the landscape of prevention, treatment, and public health initiatives. One of the primary drivers is the increasing adoption of HPV vaccination programs, which have been highly effective in reducing the incidence of HPV-related diseases, including genital warts. Vaccines like Gardasil and Cervarix protect against the most common strains of HPV that cause genital warts, leading to a decrease in new infections and, by extension, a reduction in the need for treatment options. The inclusion of both girls and boys in vaccination programs is further expanding the impact of these initiatives.

Another transformative factor is the growing awareness of HPV and genital warts, particularly through public health campaigns and educational initiatives. As more people become informed about the risks of HPV infection and the availability of both preventive (vaccination) and therapeutic options (such as cryotherapy, laser therapy, and topical treatments), the market is seeing an increase in demand for both diagnostic services and treatment interventions.

The ongoing development of less invasive treatments and more effective therapies is also contributing to the transformation of the market. Innovations in minimally invasive techniques like laser therapy and immunotherapies offer patients more comfortable and convenient treatment options, leading to better patient satisfaction and adherence to treatment regimens. Additionally, oral antiviral treatments are emerging as promising options for managing genital warts, making it easier for patients to access care.

Finally, increased focus on men's health and the recognition of the impact of HPV on both men and women are contributing to a broader global vaccination and treatment strategy. As more men are included in HPV vaccination programs, the incidence of genital warts is expected to decline, further driving the growth of the market.

In summary, the Genital Warts market is experiencing a transformation driven by the rise of HPV vaccination programs, growing awareness and education, advancements in treatment technologies, and a greater focus on comprehensive, preventive healthcare. These factors are expanding the reach of preventive measures, improving treatment outcomes, and enhancing overall public health in the fight against genital warts and HPV-related diseases.

Table of Contents

Executive Summary

Scope and Definition

Market/Product Definition

Inclusion and Exclusion

Key Questions Answered

Analysis and Forecast Note

1. Global Genital Warts Market: Industry Outlook

- 1.1 Introduction

- 1.2 Market Trends

- 1.3 Regulatory Framework

- 1.4 Epidemiology Analysis

- 1.5 Clinical Trial Analysis

- 1.6 Market Dynamics

- 1.6.1 Impact Analysis

- 1.6.2 Market Drivers

- 1.6.3 Market Challenges

- 1.6.4 Market Opportunities

2. Global Genital Warts Market (Region), ($Billion), 2023-2035

- 2.1 North America

- 2.1.1 Key Findings

- 2.1.2 Market Dynamics

- 2.1.3 Market Sizing and Forecast

- 2.1.3.1 North America Genital Warts Market, by Country

- 2.1.3.1.1 U.S.

- 2.1.3.1 North America Genital Warts Market, by Country

- 2.2 Europe

- 2.2.1 Key Findings

- 2.2.2 Market Dynamics

- 2.2.3 Market Sizing and Forecast

- 2.2.3.1 Europe Genital Warts Market, by Country

- 2.2.3.1.1 Germany

- 2.2.3.1.2 U.K.

- 2.2.3.1.3 France

- 2.2.3.1.4 Italy

- 2.2.3.1 Europe Genital Warts Market, by Country

- 2.3 Asia Pacific

- 2.3.1 Key Findings

- 2.3.2 Market Dynamics

- 2.3.3 Market Sizing and Forecast

- 2.3.3.1 Asia Pacific Genital Warts Market, by Country

- 2.3.3.1.1 China

- 2.3.3.1.2 Japan

- 2.3.3.1 Asia Pacific Genital Warts Market, by Country

3. Global Genital Warts Market: Competitive Landscape and Company Profiles

- 3.1 Key Strategies and Development

- 3.1.1 Mergers and Acquisitions

- 3.1.2 Synergistic Activities

- 3.1.3 Business Expansions and Funding

- 3.1.4 Product Launches and Approvals

- 3.1.5 Other Activities

- 3.2 Company Profiles

- 3.2.1 Verrica Pharmaceuticals

- 3.2.1.1 Overview

- 3.2.1.2 Top Products / Product Portfolio

- 3.2.1.3 Top Competitors

- 3.2.1.4 Target Customers/End-Users

- 3.2.1.5 Key Personnel

- 3.2.1.6 Analyst View

- 3.2.2 Tamir Biotechnology

- 3.2.2.1 Overview

- 3.2.2.2 Top Products / Product Portfolio

- 3.2.2.3 Top Competitors

- 3.2.2.4 Target Customers/End-Users

- 3.2.2.5 Key Personnel

- 3.2.2.6 Analyst View

- 3.2.3 Novan Inc.

- 3.2.3.1 Overview

- 3.2.3.2 Top Products / Product Portfolio

- 3.2.3.3 Top Competitors

- 3.2.3.4 Target Customers/End-Users

- 3.2.3.5 Key Personnel

- 3.2.3.6 Analyst View

- 3.2.4 Medicis Pharmaceuticals

- 3.2.4.1 Overview

- 3.2.4.2 Top Products / Product Portfolio

- 3.2.4.3 Top Competitors

- 3.2.4.4 Target Customers/End-Users

- 3.2.4.5 Key Personnel

- 3.2.4.6 Analyst View

- 3.2.5 Aresus Pharma

- 3.2.5.1 Overview

- 3.2.5.2 Top Products / Product Portfolio

- 3.2.5.3 Top Competitors

- 3.2.5.4 Target Customers/End-Users

- 3.2.5.5 Key Personnel

- 3.2.5.6 Analyst View

- 3.2.6 AbbVie Inc.

- 3.2.6.1 Overview

- 3.2.6.2 Top Products / Product Portfolio

- 3.2.6.3 Top Competitors

- 3.2.6.4 Target Customers/End-Users

- 3.2.6.5 Key Personnel

- 3.2.6.6 Analyst View

- 3.2.1 Verrica Pharmaceuticals