|

|

市場調査レポート

商品コード

1719319

欧州の脊椎ナビゲーション市場:分析と予測(2023年~2032年)Europe Spinal Navigation Market: Analysis and Forecast, 2023-2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 欧州の脊椎ナビゲーション市場:分析と予測(2023年~2032年) |

|

出版日: 2025年05月07日

発行: BIS Research

ページ情報: 英文 141 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

欧州の脊椎ナビゲーションの市場規模は、2023年に1億9,210万米ドルとなりました。

同市場は、2032年には7億5,470万米ドルに達すると予測され、予測期間の2023年~2032年のCAGRは16.42%と見込まれています。手技の精度を高め、患者の安全性を向上させ、より良い臨床結果をもたらす先進機器の使用により、欧州の脊椎ナビゲーション市場は脊椎手術の様相を急速に変えつつあります。しかし、これらのプラットフォームの初期投資と継続的なメンテナンスコストが高いため、EUのヘルスケアシステム全体への普及は依然として限定的です。アクセスを拡大し、欧州全域の患者に質の高い医療を提供するには、独創的な資金モデル、有利な償還スキーム、協力的な調達戦術を通じて、こうした経済的障害を克服することが重要です。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2023年~2032年 |

| 2023年の評価 | 1億9,210万米ドル |

| 2032年予測 | 7億5,470万米ドル |

| CAGR | 16.42% |

欧州の脊椎ナビゲーション市場には、患者の解剖学的構造をリアルタイムで3次元表示することで、外科医が脊椎手術を行うのを支援する最先端のガイダンスシステムが含まれます。これらの技術には、拡張現実(AR)ヘッドセット、AI駆動ソフトウェアオーバーレイ、光学トラッカー、電磁トラッカーなどが含まれ、手術精度の向上、術中リスクの低減、回復の迅速化を目指して設計されています。最近、低侵襲手術の必要性が高まっているのは、欧州の高齢化社会における椎間板変性症、脊柱管狭窄症、外傷の有病率の上昇のためであり、ナビゲーション技術は現代の診療に不可欠なツールとなっています。

ナビゲーションシステムがロボットアームや画像モダリティ(CT、透視、術中MRI)とシームレスに接続し、多機能を提供する統合手術室スイートは、病院や外来手術センターでますます一般的になってきています。財政的な制約を克服するため、機器のアズ・ア・サービスやシェアード・サービスによる調達モデルが登場し、小規模な施設でも多額の設備投資をすることなく最先端のプラットフォームにアクセスできるようになっています。しかし、さまざまな国の法律、複雑な支払い手続き、スタッフの大幅なトレーニングが必要なため、導入はまだ不平等です。

メーカー各社は、追跡精度の向上、ユーザーインターフェースの最適化、将来的な術中の困難を予見するための予測分析の導入に注力しています。保険償還制度を拡大し、基準を調和させるためには、OEM、支払者、ヘルスケアプロバイダーが協力しなければなりません。欧州の脊椎ナビゲーション市場は、患者の予後改善と費用対効果が臨床的に証明され、脊椎手術の進歩やより広範な手術ナビゲーションの応用に拍車がかかるにつれて、着実に拡大すると予想されます。

動向

- リアルタイムの3D術中ガイダンスを提供するため、AI駆動アルゴリズムと拡張現実/仮想現実オーバーレイの統合が増加。

- ロボット支援システムと従来の光学・電磁ナビゲーションプラットフォームの融合による多機能手術室の構築。

- 病院や手術センターが資本支出を分散し、多額の先行投資をすることなく最新システムにアクセスできるようにする、シェアードサービス調達および機器アズ・ア・サービス・モデルの拡大。

促進要因

- 欧州の高齢化と脊椎変性疾患の増加により、在院日数と合併症発生率を低減する精密で低侵襲な手術に対する需要が高まっています。

- 患者の安全性を重視し、アウトカムに基づく償還が行われるため、放射線被ばくを最小限に抑え、手術精度を向上させるナビゲーションツールの採用が加速しています。

- 追跡精度、ユーザー・インターフェース、データ解析といった絶え間ない技術進歩は、外科医の信頼性を高め、日常的な処置以外にも臨床応用の幅を広げています。

課題

- 高額な初期購入価格と継続的なメンテナンス費用が、ヘルスケア予算を圧迫しています。*多様で各国特有の規制要件と一貫性のない償還の枠組みが、全欧展開を妨げ、市場参入を複雑にしています。

- 高度なナビゲーションシステムを既存の手術室インフラに組み込むには、ワークフローの大幅な調整と専任スタッフのトレーニングが必要で、小規模病院や外来センターでの導入が遅れます。

当レポートでは、欧州の脊椎ナビゲーション市場について調査し、市場の概要とともに、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

第1章 エグゼクティブサマリー

第2章 市場の定義と範囲

第3章 調査手法

第4章 規制シナリオとデバイス分類

- EUにおける規制シナリオ

- 英国における規制シナリオ

第5章 償還シナリオ

- 英国における償還シナリオ

第6章 脊椎疾患の手術量

第7章 脊椎ナビゲーション市場(地域別)

- 欧州の脊椎ナビゲーション市場(エンドユーザー別)

- 欧州の脊髄ナビゲーション市場、設置ベース(エンドユーザー別)

- 英国の脊椎ナビゲーション市場

- ドイツの脊椎ナビゲーション市場

- フランスの脊椎ナビゲーション市場

- イタリアの脊椎ナビゲーション市場

- スペインの脊椎ナビゲーション市場

- オーストリアの脊椎ナビゲーション市場

- その他の欧州諸国の脊椎ナビゲーション市場

第8章 病院のプロファイル

第9章 企業プロファイル

- ERGOSURG GmbH

- Brainlab AG

- Siemens Healthineers AG

- B. Braun

- Joimax GmbH

- RIWOspine GmbH

List of Figures

- Figure: Europe Spinal Navigation Market, $Million, 2022-2032

- Figure: Spinal Navigation Market: Research Methodology

- Figure: Secondary Research Sources

- Figure: Data Sources

- Figure: Data Triangulation

- Figure: Assumptions and Limitations

- Figure: Distribution of Spine Surgeries by Procedure Type

- Figure: Spinal Navigation Market (by Region)

- Figure: Spinal Navigation Market (by Region), $Million, 2022-2032

- Figure: Spinal Navigation Market, Growth-Share Matrix (by Region), 2022-2032

- Figure: Europe Spinal Navigation Market, $Million, 2022-2032

- Figure: Europe Spinal Navigation Market (by End User), $Million, 2022-2032

- Figure: Europe Spinal Navigation Market (by End User), Installed Base, 2022-2032

- Figure: U.K. Spinal Navigation Market, $Million, 2022-2032

- Figure: U.K. Spinal Procedure Volume, 2022-2032

- Figure: U.K. Spinal Navigation Market Share, 2022 and 2032

- Figure: Germany Spinal Navigation Market, $Million, 2022-2032

- Figure: Germany Spinal Procedure Volume, 2022-2032

- Figure: Germany Spinal Navigation Market Share, 2022 and 2032

- Figure: France Spinal Navigation Market, $Million, 2022-2032

- Figure: France Spinal Procedure Volume, 2022-2032

- Figure: France Spinal Navigation Market Share, 2022 and 2032

- Figure: Italy Spinal Navigation Market, $Million, 2022-2032

- Figure: Italy Spinal Procedure Volume, 2022-2032

- Figure: Italy Spinal Navigation Market Share, 2022 and 2032

- Figure: Spain Spinal Navigation Market, $Million, 2022-2032

- Figure: Spain Spinal Procedure Volume, 2022-2032

- Figure: Spain Spinal Navigation Market Share, 2022 and 2032

- Figure: Austria Spinal Navigation Market, $Million, 2022-2032

- Figure: Austria Spinal Procedure Volume, 2022-2032

- Figure: Austria Spinal Navigation Market Share, 2022 and 2032

- Figure: Rest-of-Europe Spinal Navigation Market, $Million, 2022-2032

- Figure: Rest-of-Europe Spinal Procedure Volume, 2022-2032

- Figure: Rest-of-Europe Spinal Navigation Market Share, 2022 and 2032

List of Tables

- Table: Primary Research Sources

- Table: U.K. Spinal Navigation Market (by Product Type), $Million, 2022-2032

- Table: U.K. Spinal Navigation Market (by End User), $Million, 2022-2032

- Table: U.K. Spinal Navigation Market, Installed Base, 2022-2032

- Table: U.K. Spinal Navigation Market, Units Sold, 2022-2032

- Table: Germany Spinal Navigation Market (by Product Type), $Million, 2022-2032

- Table: Germany Spinal Navigation Market (by End User), $Million, 2022-2032

- Table: Germany Spinal Navigation Market, Installed Base, 2022-2032

- Table: Germany Spinal Navigation Market, Units Sold, 2022-2032

- Table: France Spinal Navigation Market (by Product Type), $Million, 2022-2032

- Table: France Spinal Navigation Market (by End User), $Million, 2022-2032

- Table: France Spinal Navigation Market, Installed Base, 2022-2032

- Table: France Spinal Navigation Market, Units Sold, 2022-2032

- Table: Italy Spinal Navigation Market (by Product Type), $Million, 2022-2032

- Table: Italy Spinal Navigation Market (by End User), $Million, 2022-2032

- Table: Italy Spinal Navigation Market, Installed Base, 2022-2032

- Table: Italy Spinal Navigation Market, Units Sold, 2022-2032

- Table: Spain Spinal Navigation Market (by Product Type), $Million, 2022-2032

- Table: Spain Spinal Navigation Market (by End User), $Million, 2022-2032

- Table: Spain Spinal Navigation Market, Installed Base, 2022-2032

- Table: Spain Spinal Navigation Market, Units Sold, 2022-2032

- Table: Austria Spinal Navigation Market (by Product Type), $Million, 2022-2032

- Table: Austria Spinal Navigation Market (by End User), $Million, 2022-2032

- Table: Austria Spinal Navigation Market, Installed Base, 2022-2032

- Table: Austria Spinal Navigation Market, Units Sold, 2022-2032

- Table: Rest-of-Europe Spinal Navigation Market (by Product Type), $Million, 2022-2032

- Table: Rest-of-Europe Spinal Navigation Market (by End User), $Million, 2022-2032

- Table: Rest-of-Europe Spinal Navigation Market, Installed Base, 2022-2032

- Table: Rest-of-Europe Spinal Navigation Market, Units Sold, 2022-2032

Introduction to Europe Spinal Navigation Market

The Europe spinal navigation market was valued at $192.1 million in 2023 and is expected to reach $754.7 million by 2032, registering a CAGR of 16.42% during the forecast period 2023-2032. With the use of advanced instruments that increase procedural accuracy, enhance patient safety, and produce better clinical results, the spinal navigation market in Europe is quickly changing the face of spine surgery. However, the high initial investment and continuing maintenance costs of these platforms continue to limit their widespread adoption throughout EU healthcare systems. Expanding access and providing patients across Europe with high-quality care will depend on overcoming these financial obstacles through creative funding models, advantageous reimbursement schemes, and cooperative procurement tactics.

Market Introduction

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2023 - 2032 |

| 2023 Evaluation | $192.1 Million |

| 2032 Forecast | $754.7 Million |

| CAGR | 16.42% |

The market for spinal navigation in Europe includes cutting-edge guidance systems that help surgeons perform spine surgeries by showing the patient's anatomy in three dimensions in real time. These technologies, which include augmented reality headsets, AI-driven software overlays, optical and electromagnetic trackers, and more, are designed to improve surgical accuracy, lower intraoperative risks, and speed up recovery. The need for minimally invasive procedures has increased recently because to the growing prevalence of degenerative disc disease, spinal stenosis, and traumatic injuries in an ageing European population, making navigation technology essential tools for modern practice.

Integrated operating-room suites, where navigation systems seamlessly connect with robotic arms and imaging modalities (CT, fluoroscopy, intraoperative MRI) to provide multifunctional capabilities, are becoming more and more common in hospitals and ambulatory surgical centres. In order to overcome financial limitations, equipment-as-a-service and shared-service procurement models have surfaced, allowing smaller institutions to access state-of-the-art platforms without having to make significant capital expenditures. However, due to a variety of national legislation, complicated payment procedures, and the requirement for substantial staff training, adoption is still unequal.

Manufacturers are concentrating on enhancing tracking precision, optimising user interfaces, and incorporating predictive analytics to foresee intraoperative difficulties in the future. To broaden reimbursement systems and harmonise standards, OEMs, payers, and healthcare providers must cooperate together. The market for spinal navigation in Europe is expected to increase steadily as clinical proof of better patient outcomes and cost-effectiveness mounts, spurring advancements in spine surgery and wider surgical navigation applications.

Market Segmentation:

By Product Type:

- Spinal Navigation Systems

- Instruments

- Services

By End User:

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics and Scoliosis Centers

Regional Insights

Europe:

- Market Share (2022): 27.34%

- CAGR (2023-2032): 16.42%

Europe Spinal Navigation Market Trends, Drivers and Challenges:

Trends

- Increasing integration of AI-driven algorithms and augmented/virtual reality overlays to provide real-time, 3D intraoperative guidance.

- Convergence of robotic-assisted systems with traditional optical and electromagnetic navigation platforms, creating multifunctional operating suites.

- Growth of shared-service procurement and equipment-as-a-service models, enabling hospitals and surgical centres to spread capital expenditures and access the latest systems without large upfront investments.

Drivers

- Europe's aging population and rising incidence of degenerative spinal conditions are driving demand for precise, minimally invasive procedures that reduce hospital stays and complication rates.

- Emphasis on patient safety and outcome-based reimbursement is accelerating adoption of navigation tools that minimise radiation exposure and improve surgical accuracy.

- Continuous technological advances-in tracking accuracy, user interfaces and data analytics-are enhancing surgeon confidence and expanding clinical applications beyond routine procedures.

Challenges

- High initial purchase prices and ongoing maintenance expenses strain healthcare budgets, especially under tight reimbursement caps across different EU member states. * Diverse, country-specific regulatory requirements and inconsistent reimbursement frameworks impede pan-European rollout and create market entry complexities.

- Integrating advanced navigation systems into existing OR infrastructures requires significant workflow adjustments and dedicated staff training, slowing adoption in smaller hospitals and outpatient centres.

Table of Contents

1 Executive Summary

2 Market Definition and Scope

3 Research Methodology

4 Regulatory Scenario and Device Classification

- 4.1 Regulatory Scenario in the EU

- 4.2 Regulatory Scenario in the U.K.

5 Reimbursement Scenario

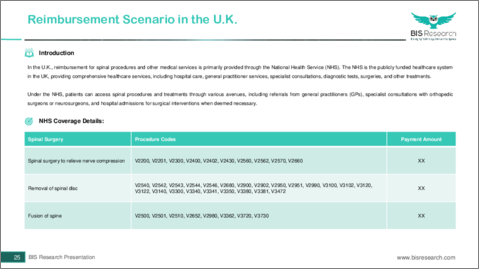

- 5.1 Reimbursement Scenario in the U.K.

6 Procedure Volume of Spinal Conditions

7 Spinal Navigation Market (by Region)

- 7.1 Europe Spinal Navigation Market (by End User)

- 7.2 Europe Spinal Navigation Market, Installed Base (by End User)

- 7.3 U.K. Spinal Navigation Market

- 7.4 Germany Spinal Navigation Market

- 7.5 France Spinal Navigation Market

- 7.6 Italy Spinal Navigation Market

- 7.7 Spain Spinal Navigation Market

- 7.8 Austria Spinal Navigation Market

- 7.9 Rest-of-Europe Spinal Navigation Market

8 Hospital Profiles

9 Company Profiles

- 9.1 ERGOSURG GmbH

- 9.2 Brainlab AG

- 9.3 Siemens Healthineers AG

- 9.4 B. Braun

- 9.5 Joimax GmbH

- 9.6 RIWOspine GmbH