|

|

市場調査レポート

商品コード

1716262

アジア太平洋のプレハブ・モジュール型データセンター市場:データセンタータイプ別、コンフィギュレーション別、フォームファクター別、国別 - 分析と予測(2024年~2034年)Asia-Pacific Prefabricated and Modular Data Centers Market: Focus on Data Center Types, Configuration, Form Factor, and Country - Analysis and Forecast, 2024-2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| アジア太平洋のプレハブ・モジュール型データセンター市場:データセンタータイプ別、コンフィギュレーション別、フォームファクター別、国別 - 分析と予測(2024年~2034年) |

|

出版日: 2025年05月01日

発行: BIS Research

ページ情報: 英文 73 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

アジア太平洋のプレハブ・モジュール型データセンターの市場規模は、2024年に6億7,330万米ドルとなりました。

同市場は、12.46%のCAGRで拡大し、2034年には21億7,930万米ドルに達すると予測されています。アジア太平洋のプレハブ・モジュール型データセンターに対するニーズが急速に高まっているのは、適応性が高く、手頃な価格でエネルギー効率の高いデジタルインフラを提供でき、さまざまな規制要件に合わせてカスタマイズできるためです。これらのターンキー・ソリューションは、信頼性や電力使用効率(PUE)を犠牲にすることなく、導入スケジュールを大幅に短縮できるため、アジア太平洋の混雑した都市ハブにおける大規模なハイパースケール・プロジェクトや急成長するエッジコンピューティング設備に特に適しています。アジア太平洋の組織は、モジュラー設計とオフサイト建設の開発により、変化するビジネス要件を満たすためにITインフラを迅速に拡張または変更することができます。さらに、太陽光や風力などの再生可能エネルギー源と最先端の冷却技術の統合が進んでおり、地域の持続可能性目標や国のネットゼロ公約をサポートしています。このような運用効率、環境責任、展開の俊敏性の組み合わせにより、アジア太平洋でプレハブ・モジュール型データセンターの導入が加速しています。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2024年~2034年 |

| 2024年の評価 | 6億7,330万米ドル |

| 2034年の予測 | 21億7,930万米ドル |

| CAGR | 12.46% |

アジア太平洋のプレハブ・モジュール型データセンター市場は、同地域の急速なデジタル化、クラウド導入、5Gインフラ展開により急速に拡大しています。一般的な構造物に比べ、完全に統合されたデータセンター・モジュールをオフサイトで製造し、オンサイトで組み立てるプレハブ・モジュラー・ソリューションには、エネルギー効率の向上、拡張性、迅速な展開など、いくつかのメリットがあります。これらの利点は、ITニーズの変化やデータ需要の増加に迅速に対応する必要がある、アジア太平洋のめまぐるしい経済において特に魅力的です。

中国、インド、日本、オーストラリア、東南アジアなどの主要国では、政府主導のデジタル・イニシアティブ、スマート・シティへの投資の拡大、エッジ・コンピューティングへの注目の高まりにより、モジュール型施設への需要が高まっています。最先端の冷却技術と再生可能エネルギー源を使用することで、モジュール設計は環境への悪影響を軽減し、持続可能性の目標にも貢献します。さまざまな規制、高額な立ち上げコスト、既存国と新興国のインフラの違いといった障害にもかかわらず、未来はまだ明るいです。モジュール型データセンターは、AI主導の管理システムの開発やカスタマイズの選択肢の拡大により、ますます魅力的になっています。プレハブ・モジュール型データセンターは、インターネットとモバイルの成長で世界をリードするアジア太平洋地域のデジタルの未来を決定する上で、極めて重要な役割を果たすと考えられます。

アジア太平洋プレハブ・モジュール型データセンターの市場動向と促進要因・課題

動向

- 5GとIoTの拡大をサポートするため、都市部や遠隔地でエッジ対応のモジュラー型ユニットを急速に展開

- 再生可能エネルギー源と高度な冷却システムの統合別エネルギー効率と持続可能性の向上

- リアルタイムの監視と予知保全のためのAI主導のインフラ管理ツールの採用

- ヘルスケア、金融、政府機関などの業界固有の要件を満たすためのモジュラー型データセンターのカスタマイズ

促進要因

- デジタル化とクラウド導入の増加に対応するため、拡張性と柔軟性に優れたデータセンター・ソリューションに対する需要の高まり

- 地域全体のデジタルインフラ開発に対する政府の取り組みと投資

- データセンター施設の迅速な導入と市場投入までの時間短縮の必要性

- 企業や規制の目標に沿ったエネルギー効率と環境の持続可能性の重視

課題

- モジュラー型データセンターの導入に伴う初期資本支出の高さ

- 規制が複雑で、域内のさまざまな国で標準化が進んでいない

- モジュラー型データセンターのメリットやROIに対する潜在的導入企業の認識や理解が限定的であること

- 電力や冷却の可用性など、特定の分野におけるインフラの制約

製品/イノベーション戦略:製品タイプ別では、データセンターのタイプ(エンタープライズデータセンター、ハイパースケールデータセンター、コロケーションデータセンター、エッジデータセンターなどの集中型データセンター)、コンフィギュレーション(パワーモジュール- 完全ファブリケーション、パワースキッド- セミファブリケーション)、フォームファクター(コンテナ型データセンター、オールインワンモジュラー型データセンター、スキッドマウント型データセンター、個別モジュール)に基づくアジア太平洋プレハブおよびモジュール型データセンターの多様な用途に関する洞察を提供します。絶え間ない技術革新、デジタルインフラへの投資の拡大、クラウドコンピューティングやエッジコンピューティングに対する需要の高まりが、こうしたモジュラー型ソリューションの採用を後押ししています。その結果、プレハブ・モジュール型データセンター市場は高成長・高収益のビジネスモデルとして、業界各社に大きな成長機会をもたらしています。

成長/マーケティング戦略:アジア太平洋のプレハブ・モジュール型データセンター市場は急速なペースで成長しています。同市場は既存および新興の市場プレーヤーに大きなビジネスチャンスを提供しています。このセグメントで取り上げている戦略には、M&A、製品投入、提携・協力、事業拡大、投資などがあります。企業が市場での地位を維持・強化するために好む戦略には、主に製品開発が含まれます。

競合戦略:本調査で分析・プロファイリングしたアジア太平洋プレハブ・モジュール型データセンター市場の主要企業には、自動車や自動車分野の専門家が含まれています。さらに、パートナーシップ、協定、提携などの包括的な競合情勢は、市場の未開拓の収益ポケットを理解する上で読者を支援するものと期待されます。

当レポートでは、アジア太平洋のプレハブ・モジュール型データセンター市場について調査し、市場の概要とともに、データセンタータイプ別、コンフィギュレーション別、フォームファクター別、国別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

第1章 市場

- 動向:現状と将来への影響評価

- サプライチェーンの概要

- 規制状況

- 研究開発レビュー

- プレハブ式データセンターと従来型データセンターの比較

- 市場力学の概要

- スタートアップの情勢

第2章 地域

- 地域のサマリー

- アジア太平洋

- 地域概要

- 市場成長促進要因

- 市場成長抑制要因

- 用途

- 製品

- アジア太平洋(国別)

第3章 市場-競合ベンチマーキングと企業プロファイル

- 今後の見通し

- 地理的評価

- Huawei Technologies Co., Ltd.

第4章 調査手法

List of Figures

- Figure 1: Asia-Pacific Prefabricated and Modular Data Centers Market (by Scenario), $Million, 2024, 2027, and 2034

- Figure 2: Asia-Pacific Prefabricated and Modular Data Centers Market (by Data Center Type), $Million, 2023, 2027, and 2034

- Figure 3: Asia-Pacific Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023, 2027, and 2034

- Figure 4: Asia-Pacific Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023, 2027, and 2034

- Figure 5: Key Events

- Figure 6: Estimated Increase in IoT Adoption in 2023

- Figure 7: Companies Using Renewable Sources of Energy, 2021

- Figure 8: Supply Chain and Risks within the Supply Chain

- Figure 9: Value Chain Analysis

- Figure 10: Regulations for Data Centers Including Prefabricated and Modular Data Centers

- Figure 11: Patent Analysis (by Country), January 2021-December 2024

- Figure 12: Patent Analysis (by Company), January 2021-December 2024

- Figure 13: End-User and Buying Criteria in the Prefabricated and Modular Data Centers Market

- Figure 14: Cost Analysis of Prefabricated and Traditional Data Centers

- Figure 15: Capital Expenditure and Capital Expenditure Incurred per Watt

- Figure 16: Impact Analysis of Market Navigating Factors, 2023-2034

- Figure 17: Estimated Share of Worldwide 5G Adoption (Excluding IoT)

- Figure 18: China Prefabricated and Modular Data Centers Market, $Million, 2023-2034

- Figure 19: Japan Prefabricated and Modular Data Centers Market, $Million, 2023-2034

- Figure 20: Australia Prefabricated and Modular Data Centers Market, $Million, 2023-2034

- Figure 21: India Prefabricated and Modular Data Centers Market, $Million, 2023-2034

- Figure 22: Singapore Prefabricated and Modular Data Centers Market, $Million, 2023-2034

- Figure 23: Rest-of-Asia-Pacific Prefabricated and Modular Data Centers Market, $Million, 2023-2034

- Figure 24: Strategic Initiatives, January 2021-December 2024

- Figure 25: Share of Strategic Initiatives, 2023

- Figure 26: Data Triangulation

- Figure 27: Top-Down and Bottom-Up Approach

- Figure 28: Assumptions and Limitations

List of Tables

- Table 1: Market Snapshot

- Table 2: Opportunities across Region

- Table 3: Competitive Landscape Snapshot

- Table 4: Trends Overview

- Table 5: Consortiums and Associations for Data Centers Including Prefabricated and Modular Data Centers

- Table 6: Comparison of Traditional and Prefabricated Data Centers

- Table 7: Start-Up Landscape of Prefabricated and Modular Data Centers Market

- Table 8: Prefabricated and Modular Data Centers Market (by Region), $Million, 2023-2034

- Table 9: Asia-Pacific Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 10: Asia-Pacific Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 11: Asia-Pacific Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 12: China Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 13: China Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 14: China Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 15: Japan Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 16: Japan Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 17: Japan Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 18: Australia Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 19: Australia Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 20: Australia Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 21: India Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 22: India Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 23: India Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 24: Singapore Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 25: Singapore Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 26: Singapore Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 27: Rest-of-Asia-Pacific Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 28: Rest-of-Asia-Pacific Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 29: Rest-of-Asia-Pacific Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 30: Market Share

Introduction to Asia-Pacific Prefabricated and Modular Data Centers Market

The Asia-Pacific prefabricated and modular data centers market was valued at $673.3 million in 2024 and is expected to grow at a CAGR of 12.46% and reach $2,179.3 million by 2034. The Asia-Pacific region's need for prefabricated and modular data centres is growing quickly due to its capacity to provide adaptable, affordable, and energy-efficient digital infrastructure that can be customised to meet a variety of regulatory requirements. Because these turnkey solutions drastically reduce deployment timetables without sacrificing reliability or power-usage effectiveness (PUE), they are especially well-suited to large-scale hyperscale projects and quickly growing edge computing installations in APAC's crowded urban hubs. Organisations in Asia Pacific can quickly scale or modify their IT infrastructure to satisfy changing business requirements thanks to developments in modular design and off-site construction. Additionally, the growing integration of renewable energy sources, such as solar and wind, along with cutting-edge cooling technologies, supports regional sustainability goals and national net-zero commitments. This combination of operational efficiency, environmental responsibility, and deployment agility is accelerating the adoption of prefabricated and modular data centres throughout APAC.

Market Introduction

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2024 - 2034 |

| 2024 Evaluation | $673.3 Million |

| 2034 Forecast | $2,179.3 Million |

| CAGR | 12.46% |

The market for prefabricated and modular data centres in Asia-Pacific (APAC) is expanding rapidly due to the region's fast digitalisation, cloud adoption, and 5G infrastructure rollout. Compared to typical structures, prefabricated and modular solutions-which entail the off-site fabrication and on-site assembly of fully integrated data centre modules-offer several benefits, including increased energy efficiency, scalability, and quicker deployment. These advantages are especially alluring in APAC's fast-paced economies, where businesses need to react swiftly to changing IT needs and rising data demands.

Demand for modular facilities is being driven by government-led digital initiatives, growing investments in smart cities, and heightened attention to edge computing in key economies such as China, India, Japan, Australia, and Southeast Asia. By using cutting-edge cooling technology and renewable energy sources, modular designs also contribute to sustainability objectives by lessening their negative effects on the environment. The future is still favourable despite obstacles such different regulations, expensive startup costs, and infrastructure differences between established and emerging nations. Modular data centres are becoming more and more appealing due to developments in AI-driven management systems and expanding customisation choices. Prefabricated and modular data centres are positioned to be crucial in determining the digital future of the Asia-Pacific region, which is still leading the world in internet and mobile growth.

Market Segmentation

Segmentation 1: by Data Center Types

- Centralized Data Center

- Enterprise Data Centers

- Hyperscale Data Centers

- Colocation Data Centers

- Edge Data Centers

Segmentation 2: by Configuration

- Power Module (Fully Fabricated)

- Power Skid (Semi-Fabricated)

Segmentation 3: by Form Factor

- Containerized Data Center (ISO)

- All-in-One Modular Data Center

- Skid-Mounted Data Center

- Individual Module

Segmentation 4: by Region

- Asia-Pacific: China, Japan, Australia, India, Singapore, and Rest-of-Asia-Pacific

APAC Prefabricated and Modular Data Centers Market trends, Drivers and Challenges

Trends

- Rapid deployment of edge-ready modular units in urban and remote areas to support 5G and IoT expansion

- Integration of renewable energy sources and advanced cooling systems to enhance energy efficiency and sustainability.

- Adoption of AI-driven infrastructure management tools for real-time monitoring and predictive maintenance.

- Customization of modular data centres to meet industry-specific requirements in sectors like healthcare, finance, and government.

Drivers

- Growing demand for scalable and flexible data centre solutions to accommodate increasing digitalisation and cloud adoption.

- Government initiatives and investments in digital infrastructure development across the region.

- Need for rapid deployment and reduced time-to-market for data centre facilities.

- Emphasis on energy efficiency and environmental sustainability aligning with corporate and regulatory goals.

Challenges

- High initial capital expenditure associated with modular data centre deployment.

- Regulatory complexities and lack of standardisation across different countries in the region.

- Limited awareness and understanding of the benefits and ROI of modular data centres among potential adopters.

- Infrastructure limitations in certain areas, including power and cooling availability.

How can this report add value to an organization?

Product/Innovation Strategy: The product segment provides insights into the diverse applications of APAC prefabricated and modular data centers based on data center types (centralized data centers, including enterprise, hyperscale, and colocation data centers, and edge data centers), configuration (power module - fully fabricated and power skid - semi-fabricated), and form factor (containerized data centers, all-in-one modular data centers, skid-mounted data centers, and individual modules). Continuous technological innovations, growing investments in digital infrastructure, and rising demand for cloud and edge computing have been driving the adoption of these modular solutions. Consequently, the prefabricated and modular data centers market represents a high-growth and high-revenue business model with substantial opportunities for industry players.

Growth/Marketing Strategy: The APAC prefabricated and modular data centers market has been growing at a rapid pace. The market offers enormous opportunities for existing and emerging market players. Some of the strategies covered in this segment are mergers and acquisitions, product launches, partnerships and collaborations, business expansions, and investments. The strategies preferred by companies to maintain and strengthen their market position primarily include product development.

Competitive Strategy: The key players in the APAC prefabricated and modular data centers market analyzed and profiled in the study include professionals with expertise in the automobile and automotive domains. Additionally, a comprehensive competitive landscape such as partnerships, agreements, and collaborations are expected to aid the reader in understanding the untapped revenue pockets in the market.

Table of Contents

Executive Summary

Scope and Definition

1 Markets

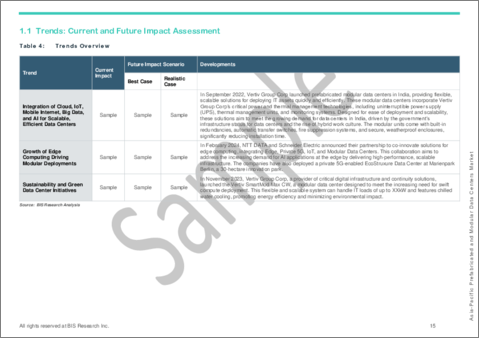

- 1.1 Trends: Current and Future Impact Assessment

- 1.1.1 Integration of Cloud, IoT, Mobile Internet, Big Data, and AI for Scalable, Efficient Data Centers

- 1.1.2 Growth of Edge Computing Driving Modular Deployments

- 1.1.3 Sustainability and Green Data Center Initiatives

- 1.2 Supply Chain Overview

- 1.2.1 Value Chain Analysis

- 1.3 Regulatory Landscape

- 1.3.1 Consortiums and Associations

- 1.3.2 Regulatory Bodies

- 1.4 Research and Development Review

- 1.4.1 Patent Filing Trend (by Country, by Company)

- 1.4.2 End-User Buying Criteria

- 1.5 Comparison of Prefabricated Vs. Conventional Data Centers

- 1.5.1 Cost Analysis

- 1.5.2 Deployment Time and Flexibility

- 1.5.3 Energy Efficiency

- 1.5.4 Operational Efficiency

- 1.6 Market Dynamics Overview

- 1.6.1 Market Drivers

- 1.6.1.1 Increased IT and 5G-Driven Infrastructure Demand

- 1.6.1.2 Scalability, Mobility, and Disaster Recovery Benefits

- 1.6.1.3 Expansion of Cloud Providers

- 1.6.2 Market Restraints

- 1.6.2.1 Seamless Integration with Existing Infrastructure

- 1.6.2.2 Power Efficiency and Sustainability Issues with Power and Cooling

- 1.6.3 Market Opportunities

- 1.6.3.1 Opportunities for Solution Providers to Collaborate with Hyperscale Cloud Providers

- 1.6.3.2 Retrofit Opportunities

- 1.6.1 Market Drivers

- 1.7 Start-Up Landscape

2 Regions

- 2.1 Regional Summary

- 2.2 Asia-Pacific

- 2.2.1 Regional Overview

- 2.2.2 Driving Factors for Market Growth

- 2.2.3 Factors Challenging the Market

- 2.2.4 Application

- 2.2.5 Product

- 2.2.6 Asia-Pacific (by Country)

- 2.2.6.1 China

- 2.2.6.1.1 Application

- 2.2.6.1.2 Product

- 2.2.6.2 Japan

- 2.2.6.2.1 Application

- 2.2.6.2.2 Product

- 2.2.6.3 Australia

- 2.2.6.3.1 Application

- 2.2.6.3.2 Product

- 2.2.6.4 India

- 2.2.6.4.1 Application

- 2.2.6.4.2 Product

- 2.2.6.5 Singapore

- 2.2.6.5.1 Application

- 2.2.6.5.2 Product

- 2.2.6.6 Rest-of-Asia-Pacific

- 2.2.6.6.1 Application

- 2.2.6.6.2 Product

- 2.2.6.1 China

3 Markets - Competitive Benchmarking and Company Profiles

- 3.1 Next Frontiers

- 3.2 Geographic Assessment

- 3.2.1 Huawei Technologies Co., Ltd.

- 3.2.1.1 Overview

- 3.2.1.2 Top Products/Product Portfolio

- 3.2.1.3 Top Competitors

- 3.2.1.4 Target Customers/End Users

- 3.2.1.5 Key Personnel

- 3.2.1.6 Analyst View

- 3.2.1.7 Market Share, 2023

- 3.2.1 Huawei Technologies Co., Ltd.

4 Research Methodology

- 4.1 Data Sources

- 4.1.1 Primary Data Sources

- 4.1.2 Secondary Data Sources

- 4.1.3 Data Triangulation

- 4.2 Market Estimation and Forecast