|

|

市場調査レポート

商品コード

1716260

欧州のプレハブ・モジュール型データセンター市場:データセンタータイプ別、コンフィギュレーション別、フォームファクター別、国別 - 分析と予測(2024年~2034年)Europe Prefabricated and Modular Data Centers Market: Focus on Data Center Types, Configuration, Form Factor, and Country - Analysis and Forecast, 2024-2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 欧州のプレハブ・モジュール型データセンター市場:データセンタータイプ別、コンフィギュレーション別、フォームファクター別、国別 - 分析と予測(2024年~2034年) |

|

出版日: 2025年05月01日

発行: BIS Research

ページ情報: 英文 86 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

欧州のプレハブ・モジュール型データセンターの市場規模は、2024年に10億470万米ドルとなりました。

同市場は、15.05%のCAGRで拡大し、2034年には40億8,150万米ドルに達すると予測されています。プレハブ・モジュール型データセンターは、柔軟性、経済性、エネルギー効率に優れ、EUの厳しい規制を満たすデジタルインフラを提供できるため、欧州全域でこの種の施設への需要が高まっています。信頼性や電力使用効率(PUE)を犠牲にすることなく導入リードタイムを短縮できるため、都市中心部における大規模なハイパースケール設備やエッジコンピューティングプロジェクトは、こうしたターンキーソリューションに特に適しています。欧州の企業は、モジュラーアーキテクチャとオフサイトアセンブリの進歩により、GDPRとEN 50600データセンター基準への完全なコンプライアンスを維持しながら、IT要件の変化に応じて容量を迅速に拡張または再コンフィギュレーションすることができます。さらに、自然エネルギー(オンサイト太陽光発電や風力発電など)と最先端の冷却技術のシームレスな統合は、EUのグリーンディール目標に合致しているため、事業者は二酸化炭素排出量と運用コストを同時に削減することができます。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2024年~2034年 |

| 2024年の評価 | 10億470万米ドル |

| 2034年予測 | 40億8,150万米ドル |

| CAGR | 15.05% |

欧州のプレハブ・モジュール型データセンター市場は、欧州大陸のデジタル・インフラ・エコシステムの重要な一部となっています。これらのソリューションは、迅速な展開スケジュール、予測可能なコスト、高いエネルギー効率とスペース効率など、従来の「レンガとモルタル」建設に比べ大きなメリットを提供します。これらのソリューションは、あらかじめ設計されたモジュールをオフサイトで製造し、現地で配送・組み立てを行うのが特徴です。欧州の企業、コロケーション・プロバイダー、ネットワーク事業者は、クラウド・サービス、5Gの展開、エッジ・コンピューティング・アプリケーションからのデータ・トラフィックに対する需要の高まりに対応するため、変化するワークロード要件に合わせてプラグアンドプレイで拡張可能なモジュール設計を導入するケースが増えています。

強力な信頼性、セキュリティ、電力使用効率(PUE)基準を要求するEN 50600やISO 30134といったEUの厳しい規制枠組みが、市場拡大の基盤となっています。一方、欧州グリーン・ディールの脱炭素化目標が、廃熱回収計画、高度な冷却方法、再生可能エネルギー源のモジュール式建物への組み込みを後押ししています。サプライチェーンや標準化、特に加盟国間の設備要件の調和にはまだ問題があるもの、工場の自動化やデジタルツインテクノロジーへの継続的な投資により、製品の一貫性が向上し、リードタイムが短縮されています。このため、プレハブ・モジュール型データセンターは、欧州のデジタル経済の急速な拡大に不可欠なものとなっています。

欧州のプレハブ・モジュール型データセンター市場動向と促進要因・課題-動向

- 都市部のマイクロハブや遠隔地でのエッジサイト展開の加速

- プラグアンドプレイによる容量拡張を可能にする標準化されたスケーラブルなモジュール

- PUE向上のための先進的な液冷、蒸発冷却、自由冷却技術の採用

- リアルタイム監視と予知保全のためのAI駆動型DCIMツールの統合

- クラウドおよびコロケーション・プロバイダー向けのハイパースケール・コンテナ化ユニットの成長

- EN 50600およびISO 30134仕様に準拠したモジュラーアーキテクチャ

促進要因

- データおよび5Gトラフィックの急増に対応するための迅速な導入需要

- EUグリーン・ディールの下、エネルギー効率とカーボンニュートラルな運用を求める規制の後押し

- オフサイト製造と設置スケジュールの短縮別総コストの削減

- 企業のデジタル変革イニシアチブをサポートする柔軟なインフラへのニーズ

- モジュール式の配備に合わせた融資やリースモデルの利用可能性

- 企業の持続可能性へのコミットメントがグリーンインフラ投資を促進

課題

- 部品のリードタイムとコストに影響するサプライチェーンの混乱

- さまざまな国の規制やグリッドコードにまたがる標準化のハードル

- ブリックス&モルタル型と比較した場合のモジュール型機器の高額な初期費用

- 大規模なプレハブ製造のための地域内の製造能力の限界

- モジュラー・システムの専門的な設置・統合におけるスキル・ギャップ

- 従来の現場データホール環境との統合の複雑さ

製品/イノベーション戦略:製品タイプ別では、データセンターのタイプ(エンタープライズデータセンター、ハイパースケールデータセンター、コロケーションデータセンター、エッジデータセンターなどの集中型データセンター)、コンフィギュレーション(パワーモジュール* 完全組み立て型、パワースキッド* 半組み立て型)、フォームファクター(コンテナ型データセンター、オールインワンモジュラー型データセンター、スキッドマウント型データセンター、個別モジュール)に基づく、欧州のプレハブ型およびモジュール型データセンターの多様な用途に関する洞察を提供します。絶え間ない技術革新、デジタルインフラへの投資拡大、クラウドコンピューティングやエッジコンピューティングに対する需要の高まりが、こうしたモジュラー型ソリューションの採用を後押ししています。その結果、プレハブ・モジュール型データセンター市場は高成長・高収益のビジネスモデルとして、業界各社に大きな成長機会をもたらしています。

成長/マーケティング戦略:欧州のプレハブ・モジュール型データセンター市場は急速なペースで成長しています。同市場は既存および新興の市場参入企業に大きなビジネスチャンスを提供しています。このセグメントで取り上げる戦略には、M&A、製品投入、提携・協力、事業拡大、投資などがあります。企業が市場での地位を維持・強化するために好む戦略には、主に製品開発が含まれます。

競合戦略:本調査で分析・プロファイリングした欧州のプレハブ・モジュール型データセンター市場の主要企業には、自動車や自動車分野の専門家が含まれています。さらに、パートナーシップ、契約、提携などの包括的な競合情勢は、市場の未開拓の収益ポケットを理解する上で読者を支援するものと期待されます。

欧州のプレハブ・モジュール型データセンター市場でプロファイリングされている企業プロファイルは、企業カバレッジ、製品ポートフォリオ、市場浸透度を分析した主要専門家から収集した情報に基づいて選定されています。

当レポートでは、欧州のプレハブ・モジュール型データセンター市場について調査し、市場の概要とともに、データセンタータイプ別、コンフィギュレーション別、フォームファクター別、国別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

第1章 市場

- 動向:現状と将来への影響評価

- サプライチェーンの概要

- 規制状況

- 研究開発レビュー

- プレハブ式データセンターと従来型データセンターの比較

- 市場力学の概要

- スタートアップの情勢

第2章 地域

- 地域サマリー

- 欧州

- 地域概要

- 市場成長促進要因

- 市場成長抑制要因

- 用途

- 製品

- 欧州(国別)

第3章 市場-競合ベンチマーキングと企業プロファイル

- 今後の見通し

- 地理的評価

- Schneider Electric

- Rittal Pvt. Ltd.

- Eaton.

- Cannon Technologies Ltd

- Colt Data Centre Services Holdings.

- Eltek ( Delta Electronics, Inc.)

- BladeRoom Group Limited

- STULZ GMBH

第4章 調査手法

List of Figures

- Figure 1: Europe Prefabricated and Modular Data Centers Market (by Scenario), $Million, 2024, 2027, and 2034

- Figure 2: Europe Prefabricated and Modular Data Centers Market (by Data Center Type), $Million, 2023, 2027, and 2034

- Figure 3: Europe Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023, 2027, and 2034

- Figure 4: Europe Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023, 2027, and 2034

- Figure 5: Key Events

- Figure 6: Estimated Increase in IoT Adoption in 2023

- Figure 7: Companies Using Renewable Sources of Energy, 2021

- Figure 8: Supply Chain and Risks within the Supply Chain

- Figure 9: Value Chain Analysis

- Figure 10: Regulations for Data Centers Including Prefabricated and Modular Data Centers

- Figure 11: Patent Analysis (by Country), January 2021-December 2024

- Figure 12: Patent Analysis (by Company), January 2021-December 2024

- Figure 13: End-User and Buying Criteria in the Prefabricated and Modular Data Centers Market

- Figure 14: Cost Analysis of Prefabricated and Traditional Data Centers

- Figure 15: Capital Expenditure and Capital Expenditure Incurred per Watt

- Figure 16: Impact Analysis of Market Navigating Factors, 2023-2034

- Figure 17: Estimated Share of Worldwide 5G Adoption (Excluding IoT)

- Figure 18: Percentage of Enterprises Buying Cloud Computing Services in Europe and Some Countries in Europe, 2021 and 2023

- Figure 19: Germany Prefabricated and Modular Data Centers Market, $Million, 2023-2034

- Figure 20: France Prefabricated and Modular Data Centers Market, $Million, 2023-2034

- Figure 21: U.K. Prefabricated and Modular Data Centers Market, $Million, 2023-2034

- Figure 22: Netherlands Prefabricated and Modular Data Centers Market, $Million, 2023-2034

- Figure 23: Spain Prefabricated and Modular Data Centers Market, $Million, 2023-2034

- Figure 24: Italy Prefabricated and Modular Data Centers Market, $Million, 2023-2034

- Figure 25: Rest-of-Europe Prefabricated and Modular Data Centers Market, $Million, 2023-2034

- Figure 26: Strategic Initiatives, January 2021-December 2024

- Figure 27: Share of Strategic Initiatives, 2023

- Figure 28: Data Triangulation

- Figure 29: Top-Down and Bottom-Up Approach

- Figure 30: Assumptions and Limitations

List of Tables

- Table 1: Market Snapshot

- Table 2: Opportunities across Region

- Table 3: Competitive Landscape Snapshot

- Table 4: Trends Overview

- Table 5: Consortiums and Associations for Data Centers Including Prefabricated and Modular Data Centers

- Table 6: Comparison of Traditional and Prefabricated Data Centers

- Table 7: Start-Up Landscape of Prefabricated and Modular Data Centers Market

- Table 8: Prefabricated and Modular Data Centers Market (by Region), $Million, 2023-2034

- Table 9: Europe Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 10: Europe Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 11: Europe Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 12: Germany Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 13: Germany Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 14: Germany Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 15: France Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 16: France Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 17: France Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 18: U.K. Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 19: U.K. Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 20: U.K. Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 21: Netherlands Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 22: Netherlands Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 23: Netherlands Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 24: Spain Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 25: Spain Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 26: Spain Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 27: Italy Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 28: Italy Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 29: Italy Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 30: Rest-of-Europe Prefabricated and Modular Data Centers Market (by Data Center Types), $Million, 2023-2034

- Table 31: Rest-of-Europe Prefabricated and Modular Data Centers Market (by Configuration), $Million, 2023-2034

- Table 32: Rest-of-Europe Prefabricated and Modular Data Centers Market (by Form Factor), $Million, 2023-2034

- Table 33: Market Share

Introduction to Europe Prefabricated and Modular Data Centers Market

The Europe prefabricated and modular data centers market was valued at $1,004.7 million in 2024 and is expected to grow at a CAGR of 15.05% and reach $4,081.5 million by 2034. The ability of prefabricated and modular data centres to provide flexible, economical, and energy-efficient digital infrastructure that satisfies strict EU regulations is driving up demand for these types of facilities throughout Europe. Large-scale hyperscale installations and edge computing projects in urban centres are especially well-suited to these turnkey solutions since they reduce deployment lead times without sacrificing reliability or power-usage effectiveness (PUE). European enterprises can quickly expand or reconfigure capacity in response to changing IT requirements-while maintaining complete compliance with GDPR and EN 50600 data-center norms-thanks to advancements in modular architecture and off-site assembly. Moreover, the seamless integration of renewables (such as on-site solar or wind) and state-of-the-art cooling technologies dovetails with the EU's Green Deal objectives, helping operators drive down carbon emissions and operational costs simultaneously-an imperative that is accelerating adoption across the region.

Market Introduction

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2024 - 2034 |

| 2024 Evaluation | $1,004.7 Million |

| 2034 Forecast | $4,081.5 Million |

| CAGR | 15.05% |

The market for prefabricated and modular data centres in Europe has become a crucial part of the continent's larger digital infrastructure ecosystem. These solutions provide significant benefits over conventional ""brick-and-mortar"" constructions, including expedited deployment schedules, predictable costs, and high levels of energy and space efficiency. They are characterised by the off-site fabrication of pre-engineered modules that are delivered and assembled on-site. European businesses, colocation providers, and network operators are increasingly implementing modular designs that can be scaled in a plug-and-play manner to meet changing workload requirements in response to the growing demands for data traffic from cloud services, 5G roll-outs, and edge computing applications.

Stringent EU regulatory frameworks, such EN 50600 and ISO 30134, which require strong reliability, security, and power-usage effectiveness (PUE) standards, are the foundation for the market's expansion. In the meantime, the decarbonisation objective of the European Green Deal is propelling the incorporation of waste-heat recovery plans, sophisticated cooling methods, and renewable energy sources into modular buildings. Although there are still issues with the supply chain and standardisation, especially with regard to harmonising equipment requirements throughout member states, continuous investments in factory automation and digital twinning technologies are improving product consistency and cutting lead times. Prefabricated and modular data centres are therefore well-positioned to be essential to the rapid expansion of Europe's digital economy.

Market Segmentation

Segmentation 1: by Data Center Types

- Centralized Data Center

- Enterprise Data Centers

- Hyperscale Data Centers

- Colocation Data Centers

- Edge Data Centers

Segmentation 2: by Configuration

- Power Module (Fully Fabricated)

- Power Skid (Semi-Fabricated)

Segmentation 3: by Form Factor

- Containerized Data Center (ISO)

- All-in-One Modular Data Center

- Skid-Mounted Data Center

- Individual Module

Segmentation 4: by Region

- Europe: Germany, France, U.K., Netherlands, Spain, Italy, and Rest-of-Europe

Europe Prefabricated and Modular Data Centers Market trends, Drivers and Challenges -Trends

- Accelerated edge-site roll-outs in urban micro-hubs and remote locations

- Standardised, scalable modules enabling plug-and-play capacity expansions

- Adoption of advanced liquid, evaporative and free-cooling techniques to boost PUE

- Integration of AI-driven DCIM tools for real-time monitoring and predictive maintenance

- Growth of hyperscale containerised units for cloud and colocation providers

- Modular architecture aligned to EN 50600 and ISO 30134 specifications

Drivers

- Demand for rapid deployment to meet surging data and 5G traffic

- Regulatory push for energy efficiency and carbon-neutral operations under the EU Green Deal

- Total cost savings from off-site fabrication and condensed installation schedules

- Need for flexible infrastructure to support enterprise digital-transformation initiatives

- Availability of financing and leasing models tailored to modular deployments

- Corporate sustainability commitments driving green infrastructure investments

Challenges

- Supply-chain disruptions affecting component lead times and costs

- Standardisation hurdles across diverse national regulations and grid codes

- High upfront premiums on modular equipment versus bricks-and-mortar builds

- Limited in-region manufacturing capacity for large-scale prefabrication

- Skills gap in specialised installation and integration of modular systems

- Integration complexities with legacy on-site data-hall environments

How can this report add value to an organization?

Product/Innovation Strategy: The product segment provides insights into the diverse applications of Europe prefabricated and modular data centers based on data center types (centralized data centers, including enterprise, hyperscale, and colocation data centers, and edge data centers), configuration (power module * fully fabricated and power skid *semi-fabricated), and form factor (containerized data centers, all-in-one modular data centers, skid-mounted data centers, and individual modules). Continuous technological innovations, growing investments in digital infrastructure, and rising demand for cloud and edge computing have been driving the adoption of these modular solutions. Consequently, the prefabricated and modular data centers market represents a high-growth and high-revenue business model with substantial opportunities for industry players.

Growth/Marketing Strategy: The Europe prefabricated and modular data centers market has been growing at a rapid pace. The market offers enormous opportunities for existing and emerging market players. Some of the strategies covered in this segment are mergers and acquisitions, product launches, partnerships and collaborations, business expansions, and investments. The strategies preferred by companies to maintain and strengthen their market position primarily include product development.

Competitive Strategy: The key players in the Europe prefabricated and modular data centers market analyzed and profiled in the study include professionals with expertise in the automobile and automotive domains. Additionally, a comprehensive competitive landscape such as partnerships, agreements, and collaborations are expected to aid the reader in understanding the untapped revenue pockets in the market.

Key Market Players and Competition Synopsis

The companies that are profiled in the Europe prefabricated and modular data centers market have been selected based on inputs gathered from primary experts who have analyzed company coverage, product portfolio, and market penetration.

Some of the prominent names in this market are:

- Schneider Electric

- Rittal Pvt. Ltd.

- Eaton

- Cannon Technologies Ltd

- Colt Data Centre Services Holdings.

- Eltek ( Delta Electronics, Inc.)

- BladeRoom Group Limited

- STULZ GMBH

Table of Contents

Executive Summary

Scope and Definition

1 Markets

- 1.1 Trends: Current and Future Impact Assessment

- 1.1.1 Integration of Cloud, IoT, Mobile Internet, Big Data, and AI for Scalable, Efficient Data Centers

- 1.1.2 Growth of Edge Computing Driving Modular Deployments

- 1.1.3 Sustainability and Green Data Center Initiatives

- 1.2 Supply Chain Overview

- 1.2.1 Value Chain Analysis

- 1.3 Regulatory Landscape

- 1.3.1 Consortiums and Associations

- 1.3.2 Regulatory Bodies

- 1.4 Research and Development Review

- 1.4.1 Patent Filing Trend (by Country, by Company)

- 1.4.2 End-User Buying Criteria

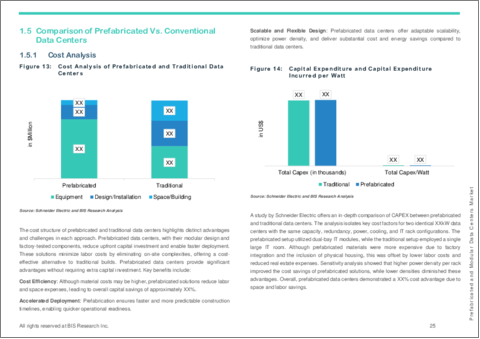

- 1.5 Comparison of Prefabricated Vs. Conventional Data Centers

- 1.5.1 Cost Analysis

- 1.5.2 Deployment Time and Flexibility

- 1.5.3 Energy Efficiency

- 1.5.4 Operational Efficiency

- 1.6 Market Dynamics Overview

- 1.6.1 Market Drivers

- 1.6.1.1 Increased IT and 5G-Driven Infrastructure Demand

- 1.6.1.2 Scalability, Mobility, and Disaster Recovery Benefits

- 1.6.1.3 Expansion of Cloud Providers

- 1.6.2 Market Restraints

- 1.6.2.1 Seamless Integration with Existing Infrastructure

- 1.6.2.2 Power Efficiency and Sustainability Issues with Power and Cooling

- 1.6.3 Market Opportunities

- 1.6.3.1 Opportunities for Solution Providers to Collaborate with Hyperscale Cloud Providers

- 1.6.3.2 Retrofit Opportunities

- 1.6.1 Market Drivers

- 1.7 Start-Up Landscape

2 Regions

- 2.1 Regional Summary

- 2.2 Europe

- 2.2.1 Regional Overview

- 2.2.2 Driving Factors for Market Growth

- 2.2.3 Factors Challenging the Market

- 2.2.4 Application

- 2.2.5 Product

- 2.2.6 Europe (by Country)

- 2.2.6.1 Germany

- 2.2.6.1.1 Application

- 2.2.6.1.2 Product

- 2.2.6.2 France

- 2.2.6.2.1 Application

- 2.2.6.2.2 Product

- 2.2.6.3 U.K.

- 2.2.6.3.1 Application

- 2.2.6.3.2 Product

- 2.2.6.4 Netherlands

- 2.2.6.4.1 Application

- 2.2.6.4.2 Product

- 2.2.6.5 Spain

- 2.2.6.5.1 Application

- 2.2.6.5.2 Product

- 2.2.6.6 Italy

- 2.2.6.6.1 Application

- 2.2.6.6.2 Product

- 2.2.6.7 Rest-of-Europe

- 2.2.6.7.1 Application

- 2.2.6.7.2 Product

- 2.2.6.1 Germany

3 Markets - Competitive Benchmarking and Company Profiles

- 3.1 Next Frontiers

- 3.2 Geographic Assessment

- 3.2.1 Schneider Electric

- 3.2.1.1 Overview

- 3.2.1.2 Top Products/Product Portfolio

- 3.2.1.3 Top Competitors

- 3.2.1.4 Target Customers/End Users

- 3.2.1.5 Key Personnel

- 3.2.1.6 Analyst View

- 3.2.1.7 Market Share, 2023

- 3.2.2 Rittal Pvt. Ltd.

- 3.2.2.1 Overview

- 3.2.2.2 Top Products/Product Portfolio

- 3.2.2.3 Top Competitors

- 3.2.2.4 Target Customers/End Users

- 3.2.2.5 Key Personnel

- 3.2.2.6 Analyst View

- 3.2.2.7 Market Share, 2023

- 3.2.3 Eaton.

- 3.2.3.1 Overview

- 3.2.3.2 Top Products/Product Portfolio

- 3.2.3.3 Top Competitors

- 3.2.3.4 Target Customers/End Users

- 3.2.3.5 Key Personnel

- 3.2.3.6 Analyst View

- 3.2.3.7 Market Share, 2023

- 3.2.4 Cannon Technologies Ltd

- 3.2.4.1 Overview

- 3.2.4.2 Top Products/Product Portfolio

- 3.2.4.3 Top Competitors

- 3.2.4.4 Target Customers/End Users

- 3.2.4.5 Key Personnel

- 3.2.4.6 Analyst View

- 3.2.4.7 Market Share, 2023

- 3.2.5 Colt Data Centre Services Holdings.

- 3.2.5.1 Overview

- 3.2.5.2 Top Products/Product Portfolio

- 3.2.5.3 Top Competitors

- 3.2.5.4 Target Customers/End Users

- 3.2.5.5 Key Personnel

- 3.2.5.6 Analyst View

- 3.2.5.7 Market Share, 2023

- 3.2.6 Eltek ( Delta Electronics, Inc.)

- 3.2.6.1 Overview

- 3.2.6.2 Top Products/Product Portfolio

- 3.2.6.3 Top Competitors

- 3.2.6.4 Target Customers/End Users

- 3.2.6.5 Key Personnel

- 3.2.6.6 Analyst View

- 3.2.6.7 Market Share, 2023

- 3.2.7 BladeRoom Group Limited

- 3.2.7.1 Overview

- 3.2.7.2 Top Products/Product Portfolio

- 3.2.7.3 Top Competitors

- 3.2.7.4 Target Customers/End Users

- 3.2.7.5 Key Personnel

- 3.2.7.6 Analyst View

- 3.2.7.7 Market Share, 2023

- 3.2.8 STULZ GMBH

- 3.2.8.1 Overview

- 3.2.8.2 Top Products/Product Portfolio

- 3.2.8.3 Top Competitors

- 3.2.8.4 Target Customers/End Users

- 3.2.8.5 Key Personnel

- 3.2.8.6 Analyst View

- 3.2.8.7 Market Share, 2023

- 3.2.1 Schneider Electric

4 Research Methodology

- 4.1 Data Sources

- 4.1.1 Primary Data Sources

- 4.1.2 Secondary Data Sources

- 4.1.3 Data Triangulation

- 4.2 Market Estimation and Forecast