|

|

市場調査レポート

商品コード

1455870

コンパニオン診断の世界市場- 世界および地域別分析:用途別、エンドユーザー別、技術別、地域別 - 分析と予測(2023年~2033年)Companion Diagnostics Market - A Global and Regional Analysis: Focus on Application, End User, Technology, and Region - Analysis and Forecast, 2023-2033 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| コンパニオン診断の世界市場- 世界および地域別分析:用途別、エンドユーザー別、技術別、地域別 - 分析と予測(2023年~2033年) |

|

出版日: 2024年03月28日

発行: BIS Research

ページ情報: 英文

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

世界のコンパニオン診断の市場規模は、2023年に37億6,200万米ドルとなりました。

同市場は、2033年には124億9,870万米ドルに達し、2023年~2033年のCAGRは12.76%になると予測されています。コンパニオン診断市場の成長は、がん患者の有病率の上昇、コンパニオン診断分野における製品承認の増加、精密医療のコンパニオン診断の原動力となる生物医学的イメージングの進歩によってもたらされます。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2023年~2033年 |

| 2023年の評価額 | 37億6,000万米ドル |

| 2033年予測 | 124億9,000万米ドル |

| CAGR | 12.76% |

コンパニオン診断市場は、個別化医療の領域で極めて重要な要素として台頭し、疾病診断と治療の状況を一変させています。この革新的な分野は、特定の疾患に関連するバイオマーカーや遺伝子変異の同定を支援する診断検査の開発に焦点を当てています。コンパニオン診断の主な目的は、ヘルスケア専門家が患者の個々の特徴に応じて治療計画を調整し、より的を絞った効果的なアプローチを確保できるようにすることです。がんのような複雑な疾患の有病率の上昇に伴い、コンパニオン診断に対する需要は著しく増加しています。

この市場の進化は、技術の進歩、製薬企業と診断薬企業の戦略的提携、そしてこれらの診断ツールの安全性と有効性を確保するための規制当局の努力の融合によって特徴付けられてきました。ヘルスケア産業が精密医療を受け入れ続ける中、コンパニオン診断市場は最前線に立ち、個別化されたより効果的な医療介入の時代に大きく貢献する態勢を整えています。

コンパニオン診断市場の出現は、特にヘルスケア、診断薬、製薬の領域において、産業界に大きな影響を与えました。この革新的な分野は、個別化された標的を絞った戦略を導入することにより、疾患の診断と治療に対する従来のアプローチを根本的に変えました。製薬会社は、コンパニオン診断を医薬品開発パイプラインに組み入れる傾向を強めており、バイオマーカーの同定や特定の治療法に最も反応しやすい患者集団の選択を容易にしています。

当レポートでは、世界のコンパニオン診断市場について調査し、市場の概要とともに、用途別、エンドユーザー別、技術別、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

第1章 市場

- 動向:現在および将来の影響評価

- サプライチェーンの概要

- 研究開発レビュー

- 規制状況

- 歴史的観点から見たCDx

- コンパニオン診断(CDx)開発の構成要素

- コンパニオン診断(CDx):将来の可能性

- 市場力学の概要

第2章 用途

- 用途別セグメンテーション

- 世界のコンパニオン診断市場(用途別)

- 世界のコンパニオン診断市場(エンドユーザー別)

第3章 製品

- 製品セグメンテーション

- 製品概要

- 世界のコンパニオン診断市場(技術別)

第4章 地域

- 地域別概要

- 促進要因と抑制要因

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第5章 市場-競合ベンチマーキングと企業プロファイル

- 今後の見通し

- 地理的評価

- Abbott Laboratories

- Agilent Technologies, Inc.

- Amoy Diagnostics Co., Ltd.

- bioMerieux

- Danaher Corporation

- DiaCarta

- F. Hoffmann-La Roche Ltd

- ICON plc

- Illumina, Inc.

- Invivoscribe Technologies, Inc.

- Myriad Genetics, Inc.

- Novogene Co, Ltd.

- QIAGEN N.V.

- Sysmex Corporation

- Thermo Fisher Scientific Inc.

第6章 調査手法

List of Figures

- Figure 1: Global Companion Diagnostics Market, $Million, 2023, 2026, and 2033

- Figure 2: Global Companion Diagnostics Market (by Region), $Million, 2022, 2026, and 2033

- Figure 3: Global Companion Diagnostics Market (by Application), $Million, 2022, 2026, and 2033

- Figure 4: Global Companion Diagnostics Market (by Technology), $Million, 2022, 2026, and 2033

- Figure 5: Global Companion Diagnostics Market (by End User), $Million, 2022, 2026, and 2033

- Figure 6: Key Players in the Companion Diagnostics Industry

- Figure 7: Key Industrial Developments in Global Companion Diagnostics Market, 2023

- Figure 8: Key Aspects Related to Liquid Biopsy-Based Companion Diagnostics

- Figure 9: Applications of Digital Diagnostics

- Figure 10: Supply Chain and Risks within the Supply Chain

- Figure 11: Global Companion Diagnostics Market (by Country), January 2021-December 2023

- Figure 12: Global Companion Diagnostics (by Year), January 2021-December 2023

- Figure 13: Evolution of Companion Diagnostics

- Figure 14: Components Required to Develop Companion Diagnostics

- Figure 15: Future Prospects of CDx

- Figure 16: Impact Analysis of Market Navigating Factors, 2023-2033

- Figure 17: Factors Impacting Reimbursement Scenario

- Figure 18: Advancements in Companion Diagnostics

- Figure 19: Future Outlook of Epigenomics

- Figure 20: North America Companion Diagnostics Market, $Million, 2022-2033

- Figure 21: U.S. Companion Diagnostics Market, $Million, 2022-2033

- Figure 22: Canada Companion Diagnostics Market, $Million, 2022-2033

- Figure 23: Europe Companion Diagnostics Market, $Million, 2022-2033

- Figure 24: France Companion Diagnostics Market, $Million, 2022-2033

- Figure 25: Germany Companion Diagnostics Market, $Million, 2022-2033

- Figure 26: U.K. Companion Diagnostics Market, $Million, 2022-2033

- Figure 27: Spain Companion Diagnostics Market, $Million, 2022-2033

- Figure 28: Italy Companion Diagnostics Market, $Million, 2022-2033

- Figure 29: Rest-of-Europe Companion Diagnostics Market, $Million, 2022-2033

- Figure 30: Asia-Pacific Companion Diagnostics Market, $Million, 2022-2033

- Figure 31: China Companion Diagnostics Market, $Million, 2022-2033

- Figure 32: India Companion Diagnostics Market, $Million, 2022-2033

- Figure 33: Australia Companion Diagnostics Market, $Million, 2022-2033

- Figure 34: Japan Companion Diagnostics Market, $Million, 2022-2033

- Figure 35: South Korea Companion Diagnostics Market, $Million, 2022-2033

- Figure 36: Rest-of-Asia-Pacific Companion Diagnostics Market, $Million, 2022-2033

- Figure 37: Latin America Companion Diagnostics Market, $Million, 2022-2033

- Figure 38: Brazil Companion Diagnostics Market, $Million, 2022-2033

- Figure 39: Mexico Companion Diagnostics Market, $Million, 2022-2033

- Figure 40: Rest-of-Latin America Companion Diagnostics Market, $Million, 2022-2033

- Figure 41: Middle East and Africa Companion Diagnostics Market, $Million, 2022-2033

- Figure 42: U.A.E. Companion Diagnostics Market, $Million, 2022-2033

- Figure 43: South Africa Companion Diagnostics Market, $Million, 2022-2033

- Figure 44: Rest-of-Middle East and Africa Companion Diagnostics Market, $Million, 2022-2033

- Figure 45: Strategic Initiatives, 2021-2023

- Figure 46: Share of Strategic Initiatives, 2021-2023

- Figure 47: Data Triangulation

- Figure 48: Top-Down and Bottom-Up Approach

- Figure 49: Assumptions and Limitations

List of Tables

- Table 1: Market Snapshot

- Table 2: Global Companion Diagnostics Market, Opportunities

- Table 3: Some of FDA Approved Liquid Biopsy CDx Tests

- Table 4: Cancer Cases Expected between 2020 and 2040

- Table 5: Product Approvals in the Field of Companion Diagnostics

- Table 6: Global Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 7: Companion Diagnostics Preparation (by Region), $Million, 2022-2033

- Table 8: North America Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 9: North America Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 10: North America Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 11: U.S. Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 12: U.S. Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 13: U.S. Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 14: Canada Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 15: Canada Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 16: Canada Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 17: Europe Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 18: Europe Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 19: Europe Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 20: France Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 21: France Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 22: France Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 23: Germany Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 24: Germany Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 25: Germany Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 26: U.K. Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 27: U.K. Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 28: U.K. Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 29: Spain Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 30: Spain Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 31: Spain Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 32: Italy Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 33: Italy Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 34: Italy Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 35: Rest-of-Europe Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 36: Rest-of-Europe Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 37: Rest-of-Europe Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 38: Asia-Pacific Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 39: Asia-Pacific Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 40: Asia-Pacific Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 41: China Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 42: China Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 43: China Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 44: India Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 45: India Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 46: India Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 47: Australia Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 48: Australia Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 49: Australia Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 50: Japan Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 51: Japan Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 52: Japan Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 53: South Korea Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 54: South Korea Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 55: South Korea Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 56: Rest-of-Asia-Pacific Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 57: Rest-of-Asia-Pacific Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 58: Rest-of-Asia-Pacific Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 59: Latin America Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 60: Latin America Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 61: Latin America Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 62: Brazil Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 63: Brazil Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 64: Brazil Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 65: Mexico Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 66: Mexico Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 67: Mexico Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 68: Rest-of-Latin America Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 69: Rest-of-Latin America Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 70: Rest-of-Latin America Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 71: Middle East and Africa Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 72: Middle East and Africa Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 73: Middle East and Africa Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 74: U.A.E. Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 75: U.A.E. Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 76: U.A.E. Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 77: South Africa Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 78: South Africa Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 79: South Africa Companion Diagnostics Market (by Technology), $Million, 2022-2033

- Table 80: Rest-of-Middle East and Africa Companion Diagnostics Market (by Application), $Million, 2022-2033

- Table 81: Rest-of-Middle East and Africa Companion Diagnostics Market (by End User), $Million, 2022-2033

- Table 82: Rest-of-Middle East and Africa Companion Diagnostics Market (by Technology), $Million, 2022-2033

Global Companion Diagnostics Market Industry Overview

The global companion diagnostics market was valued at $3,762.0 million in 2023 and is expected to reach $12,498.7 million by 2033, growing at a CAGR of 12.76% between 2023 and 2033. The growth of the companion diagnostics market is driven by the rising prevalence of cancer cases, increasing product approvals in the field of companion diagnostics, and advancing biomedical imaging as the driving force for precision medicine's companion diagnostics.

Market Introduction

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2023 - 2033 |

| 2023 Evaluation | $3.76 Billion |

| 2033 Forecast | $12.49 Billion |

| CAGR | 12.76% |

The companion diagnostics market has emerged as a pivotal component in the realm of personalized medicine, transforming the landscape of disease diagnosis and treatment. This innovative sector focuses on developing diagnostic tests that aid in the identification of biomarkers and genetic variations associated with specific diseases. The primary objective of companion diagnostics is to enable healthcare professionals to tailor treatment plans according to the individual characteristics of patients, ensuring a more targeted and effective approach. With the rising prevalence of complex diseases such as cancer, the demand for companion diagnostics has grown significantly.

The market's evolution has been characterized by a blend of technological advancements, strategic collaborations between pharmaceutical and diagnostic companies, and regulatory efforts to ensure the safety and efficacy of these diagnostic tools. As the healthcare industry continues to embrace precision medicine, the companion diagnostics market stands at the forefront, poised to make substantial contributions to the era of personalized and more effective medical interventions.

Industrial Impact

The advent of the companion diagnostics market has had a profound industrial impact, particularly within the realms of healthcare, diagnostics, and pharmaceuticals. This innovative sector has fundamentally altered the traditional approach to disease diagnosis and treatment by introducing personalized and targeted strategies. Pharmaceutical companies are increasingly integrating companion diagnostics into their drug development pipelines, facilitating the identification of biomarkers and the selection of patient populations that are most likely to respond positively to specific therapies.

Market Segmentation:

Segmentation 1: by Technology

- Polymerase Chain Reaction (PCR)

- Immunohistochemistry (IHC)

- In-Situ Hybridization (ISH)

- Next-Generation Sequencing (NGS)

- Others

PCR Segment to Dominate the Companion Diagnostics Market (by Technology)

Based on technology, the global companion diagnostics market was led by PCR in 2022 primarily due to its exceptional accuracy and sensitivity in detecting nucleic acid sequences, making it particularly adept at identifying specific genetic mutations or biomarkers associated with diseases. This precision enables clinicians to make personalized treatment decisions based on reliable diagnostic information. Additionally, PCR's versatility allows it to detect a wide range of genetic variations, including single nucleotide polymorphisms (SNPs) and gene fusions, facilitating the development of companion diagnostics for diverse diseases and therapeutic targets. Furthermore, PCR techniques, such as real-time PCR (qPCR), offer rapid turnaround times, enabling timely diagnosis and treatment monitoring, which is crucial in companion diagnostics.

Segmentation 2: by Application

- Lung Cancer

- Breast Cancer

- Colorectal Cancer

- Leukemia

- Stomach Cancer

- Melanoma

- Others

Lung Cancer Segment to Witness the Highest Growth between 2023 and 2033

The lung cancer segment holds the largest share in the companion diagnostics market for several compelling reasons. Firstly, lung cancer is one of the most prevalent and deadliest forms of cancer worldwide, driving the demand for effective diagnostic tools to guide treatment decisions. Companion diagnostics play a crucial role in lung cancer management by identifying specific genetic mutations or biomarkers that can inform targeted therapy selection. For example, mutations in genes such as EGFR, ALK, ROS1, and BRAF are commonly found in non-small cell lung cancer (NSCLC) and are associated with responses to targeted therapies.

Segmentation 3: by End User

- Pharmaceutical and Biotechnology Companies

- Reference Laboratories and Hospitals

- Others

Reference Laboratories and Hospitals Segment to Witness the Highest Growth between 2023 and 2033

Reference laboratories and hospitals hold a significant share of the end user market in the global companion diagnostics market for several reasons. The reference laboratories and hospitals typically have access to advanced diagnostic technologies and expertise, which allows them to perform complex molecular testing required for companion diagnostics. These facilities often have state-of-the-art equipment and trained personnel capable of conducting molecular assays with high accuracy and precision, which is crucial for reliable companion diagnostic testing.

Moreover, reference laboratories and hospitals serve as central hubs for patient care, where individuals seek diagnosis and treatment for various diseases, including those requiring companion diagnostics. As a result, these facilities handle a large volume of diagnostic testing, providing economies of scale and driving demand for companion diagnostics.

Segmentation 5: by Region

- North America

- U.S.

- Canada

- Europe

- Germany

- U.K.

- France

- Italy

- Spain

- Rest-of-Europe

- Asia-Pacific

- Japan

- India

- China

- South Korea

- Australia

- Rest-of-Asia-Pacific

- Latin America

- Brazil

- Mexico

- Rest-of-Latin America

- Middle East and Africa

- South Africa

- U.A.E.

- Rest-of-Middle East and Africa

The North America region is expected to hold a significant share of the global companion diagnostics market for several reasons. North America, particularly the U.S., boasts advanced healthcare infrastructure and a strong emphasis on precision medicine initiatives. This environment fosters the adoption of companion diagnostics, which play a vital role in guiding targeted therapies and improving patient outcomes.

The region is home to a large number of pharmaceutical and biotechnology companies engaged in the development of targeted therapies. These companies often collaborate with diagnostic companies to co-develop companion diagnostics alongside their therapeutic products. As a result, there has been a rise in demand for companion diagnostics in North America to support the use of these targeted therapies in clinical practices.

Recent Developments in the Companion Diagnostics Market

- In August 2023, Amoy Diagnostics Co., Ltd entered into a collaboration agreement with AstraZeneca. As per the agreement, AmoyDx's Essential NGS panel can be utilized as a companion diagnostic for ENHERTU. This diagnostic tool would be used to identify HER2 (ERBB2) mutations, specifically in patients with non-small cell lung cancer (NSCLC).

- In March 2023, Illumina Inc. and Myriad Genetics Inc. announced an expansion of their strategic partnership to enhance access to and availability of oncology homologous recombination deficiency (HRD) testing in the U.S. As part of the agreement, Illumina TruSight Oncology 500 HRD (TSO 500 HRD), initially a research-use-only test, would now be accessible in the U.S. The expanded collaboration would further establish a unique companion diagnostic (CDx) alliance for the pharmaceutical industry.

- In November 2023, Abbott Laboratories got approval from the U.S. Food and Drug Administration (FDA) for its HPV screening solution. This new tool can help identify high-risk HPV infections and would now be part of the Alinity m family of diagnostic tests, strengthening its capabilities in cancer screening.

- In December 2022, the U.S. Food and Drug Administration (FDA) granted approval for Agilent Technologies, Inc.'s Resolution ctDx FIRST to serve as a companion diagnostic (CDx). This approval would allow the use of Resolution ctDx FIRST to identify patients with advanced non-small cell lung cancer (NSCLC) who have KRAS G12C mutations. The purpose would be to identify individuals who could potentially benefit from treatment with KRAZATITM (adagrasib).

Demand - Drivers, Challenges, and Opportunities

Market Demand Drivers:

Increasing Product Approvals in the Field of Companion Diagnostics: As the range of approved companion diagnostic products widens, healthcare providers would gain access to more sophisticated tools that enable precise patient stratification, ultimately contributing to improved therapeutic outcomes and the realization of the promise of personalized medicine.

Market Challenges:

Uncertain Reimbursement Scenario: The companion diagnostics market faces a notable impediment in the form of an uncertain reimbursement scenario, casting a shadow over its potential growth and adoption. This uncertainty introduces financial challenges for healthcare providers, who heavily depend on reimbursements to offset the costs associated with integrating companion diagnostics into their clinical practices.

Market Opportunities:

Continuous Developments and Technological Advancements to Drive Progress in Companion Diagnostics: The landscape of companion diagnostics is continually shaped by ongoing developments and technological evolution. Advancements in genetic and molecular research have paved the way for a deeper understanding of disease mechanisms at the molecular level. This progress has led to the identification and validation of a plethora of biomarkers, allowing for more precise and targeted diagnostic approaches.

How can this report add value to an organization?

Product/Innovation Strategy: The global companion diagnostics market has been segmented based on various categories, such as technology, application, end user, and region.

Growth/Marketing Strategy: Product launches and approvals and synergistic activities together accounted for the maximum number of key developments, accounting for nearly 94.59% of the total developments in the companion diagnostics market between January 2021 and December 2023.

Competitive Strategy: The global companion diagnostics market is a highly fragmented market, with many smaller and private companies constantly entering the market. Key players in the companion diagnostics market analyzed and profiled in the study involve established players that offer various kinds of products and services.

Methodology

Key Considerations and Assumptions in Market Engineering and Validation

- The base year considered for the calculation of the market size is 2022. A historical year analysis has been done for the period FY2019-FY2021. The market size has been estimated for FY2022 and projected for the period FY2023-FY2033.

- The scope of this report has been carefully derived based on interactions with experts in different companies across the world. This report provides a market study of clinical biomarkers.

- The market contribution of companion diagnostics anticipated to be launched in the future has been calculated based on the historical analysis of the solutions.

- Revenues of the companies have been referenced from their annual reports for FY2022 and FY2023. For private companies, revenues have been estimated based on factors such as inputs obtained from primary research, funding history, market collaborations, and operational history.

- The market has been mapped based on the available companion diagnostics solutions. All the key companies with significant offerings in this field have been considered and profiled in this report.

Primary Research:

The primary sources involve industry experts in companion diagnostics, including the market players offering products and services. Resources such as CEOs, vice presidents, marketing directors, and technology and innovation directors have been interviewed to obtain and verify both qualitative and quantitative aspects of this research study.

The key data points taken from the primary sources include:

- validation and triangulation of all the numbers and graphs

- validation of the report's segmentation and key qualitative findings

- understanding the competitive landscape and business model

- current and proposed production values of a product by market players

- validation of the numbers of the different segments of the market in focus

- percentage split of individual markets for regional analysis

Secondary Research

Open Sources

- Certified publications, articles from recognized authors, white papers, directories, and major databases, among others

- Annual reports, SEC filings, and investor presentations of the leading market players

- Company websites and detailed study of their product portfolio

- Gold standard magazines, journals, white papers, press releases, and news articles

- Paid databases

The key data points taken from the secondary sources include:

- segmentations and percentage shares

- data for market value

- key industry trends of the top players of the market

- qualitative insights into various aspects of the market, key trends, and emerging areas of innovation

- quantitative data for mathematical and statistical calculations

Key Market Players and Competition Synopsis

The companies that are profiled have been selected based on inputs gathered from primary experts and analyzing company coverage, product portfolio, and market penetration.

The lung cancer application segment players leading the market captured around 37.39% of the market's presence as of 2022. The breast cancer segment, on the other hand, captured approximately 25.58% of the market presence in 2022.

Some prominent names established in this market are:

- Agilent Technologies, Inc.

- Abbott Laboratories

- Amoy Diagnostics Co., Ltd.

- bioMerieux

- Danaher Corporation

- DiaCarta

- F. Hoffmann-La Roche Ltd

- ICON Plc

- Illumina, Inc.

- Invivoscribe Technologies, Inc.

- Myriad Genetics, Inc.

- Novogene Co, Ltd.

- QIAGEN N.V.

- Sysmex Corporation

- Thermo Fisher Scientific Inc.

Table of Contents

Executive Summary

Scope and Definition

1 Markets

- 1.1 Trends: Current and Future Impact Assessment

- 1.1.1 Companion Diagnostics Market Trend Analysis

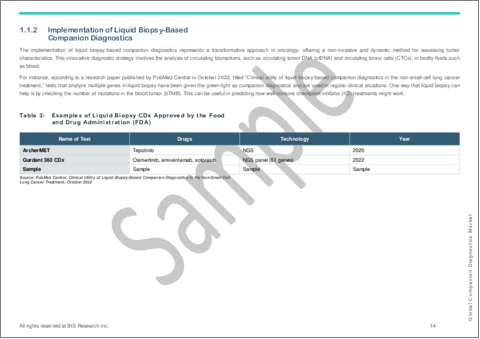

- 1.1.2 Implementation of Liquid Biopsy-Based Companion Diagnostics

- 1.1.3 Combining Artificial Intelligence and Companion Diagnostics

- 1.2 Supply Chain Overview

- 1.2.1 Value Chain Analysis

- 1.3 Research and Development Review

- 1.3.1 Patent Filing Trend (by Country, Year)

- 1.4 Regulatory Landscape

- 1.4.1 Legal Requirements and Framework by the FDA

- 1.4.2 Legal Requirements and Framework by the EMA

- 1.4.3 Legal Requirements and Framework by the MHLW

- 1.5 CDx from a Historical Perspective

- 1.6 Constituents for Companion Diagnostics (CDx) Development

- 1.7 Companion Diagnostics (CDx): Future Potential

- 1.8 Market Dynamics Overview

- 1.8.1 Market Drivers

- 1.8.1.1 Rising Prevalence of Cancer Cases

- 1.8.1.2 Increasing Product Approvals in the Field of Companion Diagnostics

- 1.8.1.3 Advancing Biomedical Imaging as the Driving Force for Precision Medicine's Companion Diagnostics

- 1.8.2 Market Restraints

- 1.8.2.1 Uncertain Reimbursement Scenario

- 1.8.2.2 Stringent Regulatory Approval Processes

- 1.8.3 Market Opportunities

- 1.8.3.1 Progress in Companion Diagnostics Driven by Continuous Development and Technological Advancements

- 1.8.3.2 Introduction of Epigenomics-Based Companion Diagnostics

- 1.8.1 Market Drivers

2 Application

- 2.1 Application Segmentation

- 2.1.1 Application Summary

- 2.1.2 End User Summary

- 2.2 Global Companion Diagnostics Market (by Application)

- 2.2.1 Lung Cancer

- 2.2.2 Breast Cancer

- 2.2.3 Colorectal Cancer

- 2.2.4 Leukemia

- 2.2.5 Stomach Cancer

- 2.2.6 Melanoma

- 2.2.7 Others

- 2.3 Global Companion Diagnostics Market (by End User)

- 2.3.1 Pharmaceutical and Biotechnology Companies

- 2.3.2 Reference Laboratories

- 2.3.3 Others

3 Products

- 3.1 Product Segmentation

- 3.2 Product Summary

- 3.3 Global Companion Diagnostics Market (by Technology)

- 3.3.1 Polymerase Chain Reaction (PCR)

- 3.3.2 Immunohistochemistry (IHC)

- 3.3.3 In-Situ Hybridization (ISH)

- 3.3.4 Next-Generation Sequencing

4 Regions

- 4.1 Regional Summary

- 4.2 Drivers and Restraints

- 4.3 North America

- 4.3.1 Regional Overview

- 4.3.2 Driving Factors for Market Growth

- 4.3.3 Factors Challenging the Market

- 4.3.4 Application

- 4.3.5 Product

- 4.3.6 U.S.

- 4.3.7 Application

- 4.3.8 Product

- 4.3.9 Canada

- 4.3.10 Application

- 4.3.11 Product

- 4.4 Europe

- 4.4.1 Regional Overview

- 4.4.2 Driving Factors for Market Growth

- 4.4.3 Factors Challenging the Market

- 4.4.4 Application

- 4.4.5 Product

- 4.4.6 France

- 4.4.7 Application

- 4.4.8 Product

- 4.4.9 Germany

- 4.4.10 Application

- 4.4.11 Product

- 4.4.12 U.K.

- 4.4.13 Application

- 4.4.14 Product

- 4.4.15 Spain

- 4.4.16 Application

- 4.4.17 Product

- 4.4.18 Italy

- 4.4.19 Application

- 4.4.20 Product

- 4.4.21 Rest-of-Europe

- 4.4.22 Application

- 4.4.23 Product

- 4.5 Asia-Pacific

- 4.5.1 Regional Overview

- 4.5.2 Driving Factors for Market Growth

- 4.5.3 Factors Challenging the Market

- 4.5.4 Application

- 4.5.5 Product

- 4.5.6 China

- 4.5.7 Application

- 4.5.8 Product

- 4.5.9 India

- 4.5.10 Application

- 4.5.11 Product

- 4.5.12 Australia

- 4.5.13 Application

- 4.5.14 Product

- 4.5.15 Japan

- 4.5.16 Application

- 4.5.17 Product

- 4.5.18 South Korea

- 4.5.19 Application

- 4.5.20 Product

- 4.5.21 Rest-of-Asia-Pacific

- 4.5.22 Application

- 4.5.23 Product

- 4.6 Latin America

- 4.6.1 Regional Overview

- 4.6.2 Driving Factors for Market Growth

- 4.6.3 Factors Challenging the Market

- 4.6.4 Application

- 4.6.5 Product

- 4.6.6 Brazil

- 4.6.7 Application

- 4.6.8 Product

- 4.6.9 Mexico

- 4.6.10 Application

- 4.6.11 Product

- 4.6.12 Rest-of-Latin America

- 4.6.13 Application

- 4.6.14 Product

- 4.7 Middle East and Africa

- 4.7.1 Regional Overview

- 4.7.2 Driving Factors for Market Growth

- 4.7.3 Factors Challenging the Market

- 4.7.4 Application

- 4.7.5 Product

- 4.7.1 U.A.E.

- 4.7.2 Application

- 4.7.3 Product

- 4.7.4 South Africa

- 4.7.5 Application

- 4.7.6 Product

- 4.7.7 Rest-of-Middle East and Africa

- 4.7.8 Application

- 4.7.9 Product

5 Markets - Competitive Benchmarking & Company Profiles

- 5.1 Next Frontiers

- 5.2 Geographic Assessment

- 5.2.1 Abbott Laboratories

- 5.2.1.1 Overview

- 5.2.1.2 Top Products/Product Portfolio

- 5.2.1.3 Top Competitors

- 5.2.1.4 Target Customers

- 5.2.1.5 Key Personnel

- 5.2.1.6 Analyst View

- 5.2.2 Agilent Technologies, Inc.

- 5.2.2.1 Overview

- 5.2.2.2 Top Products/Product Portfolio

- 5.2.2.3 Top Competitors

- 5.2.2.4 Target Customers

- 5.2.2.5 Key Personnel

- 5.2.2.6 Analyst View

- 5.2.3 Amoy Diagnostics Co., Ltd.

- 5.2.3.1 Overview

- 5.2.3.2 Top Products/Product Portfolio

- 5.2.3.3 Top Competitors

- 5.2.3.4 Target Customers

- 5.2.3.5 Key Personnel

- 5.2.3.6 Analyst View

- 5.2.4 bioMerieux

- 5.2.4.1 Overview

- 5.2.4.2 Top Products

- 5.2.4.3 Top Competitors

- 5.2.4.4 Target Customers

- 5.2.4.5 Key Personnel

- 5.2.4.6 Analyst View

- 5.2.5 Danaher Corporation

- 5.2.5.1 Overview

- 5.2.5.2 Top Products/Product Portfolio

- 5.2.5.3 Top Competitors

- 5.2.5.4 Target Customers

- 5.2.5.5 Key Personnel

- 5.2.5.6 Analyst View

- 5.2.6 DiaCarta

- 5.2.6.1 Overview

- 5.2.6.2 Top Products/Product Portfolio

- 5.2.6.3 Top Competitors

- 5.2.6.4 Target Customers

- 5.2.6.5 Key Personnel

- 5.2.6.6 Analyst View

- 5.2.7 F. Hoffmann-La Roche Ltd

- 5.2.7.1 Overview

- 5.2.7.2 Top Products/Product Portfolio

- 5.2.7.3 Top Competitors

- 5.2.7.4 Target Customers

- 5.2.7.5 Key Personnel

- 5.2.7.6 Analyst View

- 5.2.8 ICON plc

- 5.2.8.1 Overview

- 5.2.8.2 Top Products/Product Portfolio

- 5.2.8.3 Top Competitors

- 5.2.8.4 Target Customers

- 5.2.8.5 Key Personnel

- 5.2.8.6 Analyst View

- 5.2.9 Illumina, Inc.

- 5.2.9.1 Overview

- 5.2.9.2 Top Products/Product Portfolio

- 5.2.9.3 Top Competitors

- 5.2.9.4 Target Customers

- 5.2.9.5 Key Personnel

- 5.2.9.6 Analyst View

- 5.2.10 Invivoscribe Technologies, Inc.

- 5.2.10.1 Overview

- 5.2.10.2 Top Products/Product Portfolio

- 5.2.10.3 Top Competitors

- 5.2.10.4 Target Customers

- 5.2.10.5 Key Personnel

- 5.2.10.6 Analyst View

- 5.2.11 Myriad Genetics, Inc.

- 5.2.11.1 Overview

- 5.2.11.2 Top Products/Product Portfolio

- 5.2.11.3 Top Competitors

- 5.2.11.4 Target Customers

- 5.2.11.5 Key Personnel

- 5.2.11.6 Analyst View

- 5.2.12 Novogene Co, Ltd.

- 5.2.12.1 Overview

- 5.2.12.2 Top Products/Product Portfolio

- 5.2.12.3 Top Competitors

- 5.2.12.4 Target Customers

- 5.2.12.5 Key Personnel

- 5.2.12.6 Analyst View

- 5.2.13 QIAGEN N.V.

- 5.2.13.1 Overview

- 5.2.13.2 Top Products/Product Portfolio

- 5.2.13.3 Top Competitors

- 5.2.13.4 Target Customers

- 5.2.13.5 Key Personnel

- 5.2.13.6 Analyst View

- 5.2.14 Sysmex Corporation

- 5.2.14.1 Overview

- 5.2.14.2 Top Products/Product Portfolio

- 5.2.14.3 Top Competitors

- 5.2.14.4 Target Customers

- 5.2.14.5 Key Personnel

- 5.2.14.6 Analyst View

- 5.2.15 Thermo Fisher Scientific Inc.

- 5.2.15.1 Overview

- 5.2.15.2 Top Products/Product Portfolio

- 5.2.15.3 Top Competitors

- 5.2.15.4 Target Customers

- 5.2.15.5 Key Personnel

- 5.2.15.6 Analyst View

- 5.2.1 Abbott Laboratories

6 Research Methodology

- 6.1 Data Sources

- 6.1.1 Primary Data Sources

- 6.1.2 Secondary Data Sources

- 6.1.3 Data Triangulation

- 6.2 Market Estimation and Forecast