|

|

市場調査レポート

商品コード

1439027

欧州の電動農業トラクター市場:分析と予測(2023年~2028年)Europe Electric Farm Tractor Market: Analysis and Forecast, 2023-2028 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 欧州の電動農業トラクター市場:分析と予測(2023年~2028年) |

|

出版日: 2024年02月29日

発行: BIS Research

ページ情報: 英文 132 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

| 主要市場統計 | |

|---|---|

| 予測期間 | 2023年~2028年 |

| 2023年評価 | 3,294万米ドル |

| 2028年予測 | 6,320万米ドル |

| CAGR | 13.92% |

欧州の電動農業トラクターの市場規模(英国を除く)は、2023年に3,294万米ドルとなりました。

同市場は、2023年から2028年にかけて13.92%のCAGRで拡大し、2028年には6,320万米ドルに達すると予測されています。電動農業トラクター市場は、農業分野における持続可能な農法に対する需要の増加、農業機械における電動化と自動化の採用、エネルギー貯蔵システムの進歩など、さまざまな要因によって大きな成長を遂げています。近年、農業分野の農家、製造業者、調査研究者の間で電動農作業用トラクターへの関心が顕著に高まっており、この分野における電気自動車(EV)の記録的な販売につながっています。

欧州の電動農用トラクター市場は、複数の要因によって大幅な成長を遂げています。同大陸では持続可能な農法が重視されるようになり、環境に優しい農業ソリューションへの需要が高まっています。さらに、農業機械の電動化と自動化の採用が勢いを増しており、市場の成長をさらに後押ししています。欧州諸国は、農業機械の電動化を支援するため、高度なエネルギー貯蔵システムにも投資しています。さらに、農業活動から排出されるガスの削減を目的とした厳しい規制が、農家の電動農機トラクターへの移行を促しています。このような変化は、この地域の農家、メーカー、研究者の間での販売台数の増加や関心の高まりに反映されており、欧州の電動農機トラクター市場の有望な見通しを示しています。

当レポートでは、欧州の電動農業トラクター市場について調査し、市場の概要とともに、用途別、運転モード別、ドライブトレイン技術別、国別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

第1章 市場

- 業界の展望

- ビジネスダイナミクス

- ケーススタディ

- スタートアップの情勢

- ロシア・ウクライナ危機が農業用電動トラクター市場に与える影響

- コスト分析- 従来型トラクターと電動トラクターの比較

- 市場の主要製品のアーキテクチャ/技術比較

- 電動トラクター市場におけるアグリボルタティクスの役割

- 主要なバッテリー技術

第2章 地域

- 欧州

- 市場

- 用途

- 製品

- 欧州の電動農業トラクター市場(国別)

- 英国

- 市場

- 用途

- 製品

第3章 市場-競合ベンチマーキングと企業プロファイル

- 競合ベンチマーキング

- 農業用電動トラクター会社

- 企業プロファイル

- Rigitrac Traktorenbau AG

- CLAAS KGaA mbH

- EOX Tractors (Formerly H2Trac)

- EVE Srl

- SABI AGRI

- その他

第4章 調査手法

List of Figures

- Figure 1: Market Dynamics of the Europe Electric Farm Tractor Market, Drivers, Challenges, and Opportunities

- Figure 2: Europe Electric Farm Tractor Market, $Million, 2022-2028

- Figure 3: Europe Electric Farm Tractor Market (by Application), $Million, 2022 and 2028

- Figure 4: Europe Electric Farm Tractor Market (by Mode of Operation), Share (%) 2022

- Figure 5: Europe Electric Farm Tractor Market (by Drivetrain Technology), Share (%) 2022

- Figure 6: Electric Farm Tractor Market (by Region), $Million, 2022

- Figure 7: Applications of 5G in Electric Farm Tractors

- Figure 8: Basic Infrastructural Requirements of Electric Farm Tractor Ecosystem

- Figure 9: Product Development and Innovation (by Company), January 2017-March 2023

- Figure 10: Partnerships, Joint Ventures, Collaborations, and Alliances (by Company), January 2017-March 2023

- Figure 11: Wente Vineyards Energy Case Study - Monarch Tractor

- Figure 12: Solectrac Inc Mushroom Farm Case Study

- Figure 13: Charging Infrastructure, Government Subsidies, and Farm Information

- Figure 14: Charging Infrastructure, Government Subsidies, and Farm Information

- Figure 15: Charging Infrastructure, Government Subsidies, and Farm Information

- Figure 16: Charging Infrastructure, Government Subsidies, and Farm Information

- Figure 17: Charging Infrastructure, Government Subsidies, and Farm Information

- Figure 18: Charging Infrastructure, Government Subsidies, and Farm Information

- Figure 19: Charging Infrastructure, Government Subsidies, and Farm Information

- Figure 20: Charging Infrastructure, Government Subsidies, and Farm Information

- Figure 21: Charging Infrastructure, Government Subsidies, and Farm Information

- Figure 22: Charging Infrastructure, Government Subsidies, and Farm Information

- Figure 23: Charging Infrastructure, Government Subsidies, and Farm Information

- Figure 24: Competitive Position Matrix for Electric Farm Tractor Companies

- Figure 25: Data Triangulation

- Figure 26: Top-Down and Bottom-Up Approach

- Figure 27: Assumptions and Limitations

List of Tables

- Table 1: Key Consortiums and Associations in the Electric Farm Tractor Market

- Table 2: Key Regulatory Bodies

- Table 3: Key Government Initiatives/Programs

- Table 4: Internet and Electricity Access in Key Countries, 2020

- Table 5: Cost Analysis - Conventional vs. Electric Farm Tractor

- Table 6: Technical Parameters Comparison - Monarch Tractor vs. Solectrac Electric Farm Tractors

- Table 7: Key Lithium-Ion Battery-Powered Electric Farm Tractor Companies

- Table 8: Electric Farm Tractor Market (by Region), $Million, 2022-2028

- Table 9: Electric Farm Tractor Market (by Region), Units, 2022-2028

- Table 10: Europe Electric Farm Tractor Market (by Application), $Million, 2022-2028

- Table 11: Europe Electric Farm Tractor Market (by Application), Units, 2022-2028

- Table 12: Europe Electric Farm Tractor Market (by Mode of Operation), $Million, 2022-2028

- Table 13: Europe Electric Farm Tractor Market (by Mode of Operation), Units, 2022-2028

- Table 14: Europe Electric Farm Tractor Market (by Drivetrain Technology), $Million, 2022-2028

- Table 15: Europe Electric Farm Tractor Market (by Drivetrain Technology), Units, 2022-2028

- Table 16: Europe Electric Farm Tractor Market (by Country), $Million, 2022-2028

- Table 17: Europe Electric Farm Tractor Market (by Country), Units, 2022-2028

- Table 18: Germany Electric Farm Tractor Market (by Application), $Million, 2022-2028

- Table 19: Germany Electric Farm Tractor Market (by Application), Units, 2022-2028

- Table 20: Germany Electric Farm Tractor Market (by Drivetrain Technology), $Million, 2022-2028

- Table 21: Germany Electric Farm Tractor Market (by Drivetrain Technology), Units, 2022-2028

- Table 22: Germany Electric Farm Tractor Market (by Mode of Operation), $Million, 2022-2028

- Table 23: Germany Electric Farm Tractor Market (by Mode of Operation), Units, 2022-2028

- Table 24: France Electric Farm Tractor Market (by Application), $Million, 2022-2028

- Table 25: France Electric Farm Tractor Market (by Application), Units, 2022-2028

- Table 26: France Electric Farm Tractor Market (by Drivetrain Technology), $Million, 2022-2028

- Table 27: France Electric Farm Tractor Market (by Drivetrain Technology), Units, 2022-2028

- Table 28: France Electric Farm Tractor Market (by Mode of Operation), $Million, 2022-2028

- Table 29: France Electric Farm Tractor Market (by Mode of Operation), Units, 2022-2028

- Table 30: Netherlands Electric Farm Tractor Market (by Application), $Million, 2022-2028

- Table 31: Netherlands Electric Farm Tractor Market (by Application), Units, 2022-2028

- Table 32: Netherlands Electric Farm Tractor Market (by Drivetrain Technology), $Million, 2022-2028

- Table 33: Netherlands Electric Farm Tractor Market (by Drivetrain Technology), Units, 2022-2028

- Table 34: Netherlands Electric Farm Tractor Market (by Mode of Operation), $Million, 2022-2028

- Table 35: Netherlands Electric Farm Tractor Market (by Mode of Operation), Units, 2022-2028

- Table 36: Norway Electric Farm Tractor Market (by Application), $Million, 2022-2028

- Table 37: Norway Electric Farm Tractor Market (by Application), Units, 2022-2028

- Table 38: Norway Electric Farm Tractor Market (by Drivetrain Technology), $Million, 2022-2028

- Table 39: Norway Electric Farm Tractor Market (by Drivetrain Technology), Units, 2022-2028

- Table 40: Norway Electric Farm Tractor Market (by Mode of Operation), $Million, 2022-2028

- Table 41: Norway Electric Farm Tractor Market (by Mode of Operation), Units, 2022-2028

- Table 42: Sweden Electric Farm Tractor Market (by Application), $Million, 2022-2028

- Table 43: Sweden Electric Farm Tractor Market (by Application), Units, 2022-2028

- Table 44: Sweden Electric Farm Tractor Market (by Drivetrain Technology), $Million, 2022-2028

- Table 45: Sweden Electric Farm Tractor Market (by Drivetrain Technology), Units, 2022-2028

- Table 46: Sweden Electric Farm Tractor Market (by Mode of Operation), $Million, 2022-2028

- Table 47: Sweden Electric Farm Tractor Market (by Mode of Operation), Units, 2022-2028

- Table 48: Greece Electric Farm Tractor Market (by Application), $Million, 2022-2028

- Table 49: Greece Electric Farm Tractor Market (by Application), Units, 2022-2028

- Table 50: Greece Electric Farm Tractor Market (by Drivetrain Technology), $Million, 2022-2028

- Table 51: Greece Electric Farm Tractor Market (by Drivetrain Technology), Units, 2022-2028

- Table 52: Greece Electric Farm Tractor Market (by Mode of Operation), $Million, 2022-2028

- Table 53: Greece Electric Farm Tractor Market (by Mode of Operation), Units, 2022-2028

- Table 54: Switzerland Electric Farm Tractor Market (by Application), $Million, 2022-2028

- Table 55: Switzerland Electric Farm Tractor Market (by Application), Units, 2022-2028

- Table 56: Switzerland Electric Farm Tractor Market (by Drivetrain Technology), $Million, 2022-2028

- Table 57: Switzerland Electric Farm Tractor Market (by Drivetrain Technology), Units, 2022-2028

- Table 58: Switzerland Electric Farm Tractor Market (by Mode of Operation), $Million, 2022-2028

- Table 59: Switzerland Electric Farm Tractor Market (by Mode of Operation), Units, 2022-2028

- Table 60: Ukraine Electric Farm Tractor Market (by Application), $Million, 2022-2028

- Table 61: Ukraine Electric Farm Tractor Market (by Application), Units, 2022-2028

- Table 62: Ukraine Electric Farm Tractor Market (by Drivetrain Technology), $Million, 2022-2028

- Table 63: Ukraine Electric Farm Tractor Market (by Drivetrain Technology), Units, 2022-2028

- Table 64: Ukraine Electric Farm Tractor Market (by Mode of Operation), $Million, 2022-2028

- Table 65: Ukraine Electric Farm Tractor Market (by Mode of Operation), Units, 2022-2028

- Table 66: Belgium Electric Farm Tractor Market (by Application), $Million, 2022-2028

- Table 67: Belgium Electric Farm Tractor Market (by Application), Units, 2022-2028

- Table 68: Belgium Electric Farm Tractor Market (by Drivetrain Technology), $Million, 2022-2028

- Table 69: Belgium Electric Farm Tractor Market (by Drivetrain Technology), Units, 2022-2028

- Table 70: Belgium Electric Farm Tractor Market (by Mode of Operation), $Million, 2022-2028

- Table 71: Belgium Electric Farm Tractor Market (by Mode of Operation), Units, 2022-2028

- Table 72: Rest-of-Europe Electric Farm Tractor Market (by Application), $Million, 2022-2028

- Table 73: Rest-of-Europe Electric Farm Tractor Market (by Application), Units, 2022-2028

- Table 74: Rest-of-Europe Electric Farm Tractor Market (by Drivetrain Technology), $Million, 2022-2028

- Table 75: Rest-of-Europe Electric Farm Tractor Market (by Drivetrain Technology), Units, 2022-2028

- Table 76: Rest-of-Europe Electric Farm Tractor Market (by Mode of Operation), $Million, 2022-2028

- Table 77: Rest-of-Europe Electric Farm Tractor Market (by Mode of Operation), Units, 2022-2028

- Table 78: U.K. Electric Farm Tractor Market (by Application), $Million, 2022-2028

- Table 79: U.K. Electric Farm Tractor Market (by Application), Units, 2022-2028

- Table 80: U.K. Electric Farm Tractor Market (by Mode of Operation), $Million, 2022-2028

- Table 81: U.K. Electric Farm Tractor Market (by Mode of Operation), Units, 2022-2028

- Table 82: U.K. Electric Farm Tractor Market (by Drivetrain Technology), $Million, 2022-2028

- Table 83: U.K. Electric Farm Tractor Market (by Drivetrain Technology), Units, 2022-2028

- Table 84: Rigitrac Traktorenbau AG: Product Portfolio

- Table 85: Rigitrac Traktorenbau AG: Product Pricing

- Table 86: CLAAS KGaA mbH: Pricing and Product Portfolio

- Table 87: CLAAS KGaA mbH: Merger and Acquisition

- Table 88: EOX Tractors: Product Portfolio

- Table 89: EOX Tractors: Product Pricing

- Table 90: EOX Tractors: Partnership, Agreement, and Collaboration

- Table 91: EVE Srl: Product Portfolio

- Table 92: SABI AGRI: Product Portfolio

- Table 93: SABI AGRI: Product Pricing

- Table 94: Other Key Players in Electric Farm Tractor Market

The Europe Electric Farm Tractor Market (excluding U.K.) Expected to Reach $63.20 Million by 2028

Introduction to Europe Electric Farm Tractor Market

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2023 - 2028 |

| 2023 Evaluation | $32.94 Million |

| 2028 Forecast | $63.20 Million |

| CAGR | 13.92% |

The Europe electric farm tractor market (excluding U.K.) was valued at $32.94 million in 2023 and is expected to reach $63.20 million by 2028, growing at a CAGR of 13.92% between 2023 and 2028. The electric farm tractor market is experiencing significant growth due to various factors such as increased demand for sustainable farming practices within the agriculture sector, the adoption of electrification and automation in agricultural machinery, and advancements in energy storage systems. Over recent years, there has been a notable increase in interest in electric farm tractors among farmers, manufacturers, and researchers in the agriculture industry, leading to record-breaking sales of electric vehicles (EVs) in this sector.

Market Introduction

The Europe electric farm tractor market in Europe is undergoing substantial growth, driven by multiple factors. There is a growing emphasis on sustainable agricultural practices across the continent, prompting increased demand for environmentally friendly farming solutions. Additionally, the adoption of electrification and automation in agriculture machinery is gaining momentum, further propelling market growth. European countries are also investing in advanced energy storage systems to support the electrification of farm equipment. Moreover, stringent regulations aimed at reducing emissions from agricultural activities are encouraging farmers to transition to electric farm tractors. This shift is reflected in rising sales and heightened interest among farmers, manufacturers, and researchers in the region, indicating a promising outlook for the Europe electric farm tractor market.

Market Segmentation:

Segmentation 1: by Application

- Light-Duty Tractor

- Medium-Duty Tractor

- Heavy-Duty Tractor

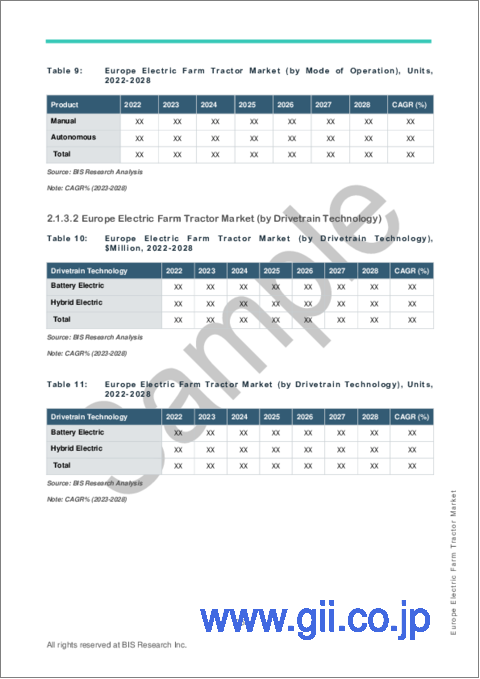

Segmentation 2: by Mode of Operation

- Manual

- Autonomous

Segmentation 3: by Drivetrain Technology

- Battery Electric

- Hybrid Electric

Segmentation 4: by Country

- Germany

- France

- Norway

- Ukraine

- Netherlands

- Sweden

- Belgium

- Greece

- Switzerland

- Rest-of-Europe

How Can This Report Add Value to an Organization?

Product/Innovation Strategy: The product segment helps the reader understand the different types of electric farm tractors available for deployment and their potential. Moreover, the study provides the reader with a detailed understanding of the electric farm tractor market by application (light-duty tractor, medium-duty tractor, and heavy-duty tractor), mode of operation (manual and autonomous), and by drivetrain technology (battery electric and hybrid electric).

Growth/Marketing Strategy: The Europe electric farm tractor market has seen major development by key players operating in the market, such as business expansion, product launch, partnership, collaboration, and joint venture. The favored strategy for the companies has been product development to strengthen their position in the electric farm tractor market.

Competitive Strategy: Key players in the Europe electric farm tractor market analyzed and profiled in the study involve major electric farm tractor manufacturers. Moreover, a detailed competitive benchmarking of the players operating in the electric farm tractor market has been done to help the reader understand how players stack against each other, presenting a clear market landscape. Additionally, comprehensive competitive strategies such as partnerships, agreements, and collaborations will aid the reader in understanding the untapped revenue pockets in the market.

Key Market Players and Competition Synopsis

The companies that are profiled have been selected based on inputs gathered from primary experts and analysing the company's coverage, product portfolio, its market penetration.

Key Companies Profiled:

- Rigitrac Traktorenbau AG

- CLAAS KGaA mbH

- EOX Tractors (Formerly H2Trac)

- EVE Srl

- SABI AGRI

Table of Contents

Executive Summary

1 Markets

- 1.1 Industry Outlook

- 1.1.1 Market Definition

- 1.1.2 Market Trends

- 1.1.2.1 Advanced Battery Technology and Future Connectivity Trends

- 1.1.2.1.1 Advancements in Battery Technology

- 1.1.2.1.2 Future Connectivity Trends (5G and LoRaWAN)

- 1.1.2.2 Climate Smart Agriculture Practices

- 1.1.2.1 Advanced Battery Technology and Future Connectivity Trends

- 1.1.3 Ecosystem/Ongoing Programs

- 1.1.3.1 Consortiums and Associations

- 1.1.3.2 Regulatory Bodies

- 1.1.3.3 Government Initiatives/Programs

- 1.2 Business Dynamics

- 1.2.1 Business Drivers

- 1.2.1.1 Rise in Awareness toward Sustainable Practices in Agriculture

- 1.2.1.2 Increased Farm Mechanization and Technology Adoption

- 1.2.1.3 Favoring Policies toward Electric Vehicle Adoption

- 1.2.1.4 Increased Demand for Electrification in Agriculture Industry

- 1.2.2 Business Challenges

- 1.2.2.1 Inadequate Charging, Network Infrastructure, and Battery Recycling Challenges

- 1.2.2.2 High Initial Cost of Equipment

- 1.2.2.3 Development of Alternative Engine Models

- 1.2.2.4 Limited Market Penetration Owing to Dominance of Conventional Tractors

- 1.2.3 Business Strategies

- 1.2.3.1 Product Development and Innovation

- 1.2.3.2 Market Development

- 1.2.4 Corporate Strategies

- 1.2.4.1 Mergers and Acquisitions

- 1.2.4.2 Partnerships, Joint Ventures, Collaborations, and Alliances

- 1.2.5 Business Opportunities

- 1.2.5.1 Integration of New/Advanced Technologies with Electric Farm Tractor

- 1.2.5.2 Opportunities in Developing Nations

- 1.2.1 Business Drivers

- 1.3 Case Studies

- 1.3.1 Monarch Tractor Wente Vineyards Energy Case Study

- 1.3.2 Solectrac Inc Mushroom Farm Case Study

- 1.4 Start-Up Landscape

- 1.4.1 Key Start-Ups in the Ecosystem

- 1.5 Impact of Russia-Ukraine Crisis on Electric Farm Tractor Market

- 1.6 Cost Analysis - Comparision of Conventional and Electric Tractor

- 1.7 Architectural/Technical Comparison of Key Products in the Market

- 1.8 Role of Agrivoltaics in Electric Farm Tractor Market

- 1.9 Key Battery Technologies

- 1.9.1 Lithium-Ion Battery

- 1.9.2 Nickel, Mercury-Based Batteries, and Others

2 Region

- 2.1 Europe

- 2.1.1 Market

- 2.1.1.1 Key Companies in Europe

- 2.1.1.2 Business Drivers

- 2.1.1.3 Business Challenges

- 2.1.2 Application

- 2.1.2.1 Europe Electric Farm Tractor Market (by Application)

- 2.1.3 Product

- 2.1.3.1 Europe Electric Farm Tractor Market (by Mode of Operation)

- 2.1.3.2 Europe Electric Farm Tractor Market (by Drivetrain Technology)

- 2.1.4 Europe Electric Farm Tractor Market (by Country)

- 2.1.4.1 Germany

- 2.1.4.1.1 Market

- 2.1.4.1.1.1 Buyer Attributes

- 2.1.4.1.1.1.1 Charging Infrastructure, Government Subsidies, and Farm Information

- 2.1.4.1.1.2 Business Challenges

- 2.1.4.1.1.3 Business Drivers

- 2.1.4.1.2 Application

- 2.1.4.1.2.1 Germany Electric Farm Tractor Market (by Application)

- 2.1.4.1.3 Product

- 2.1.4.1.1 Market

- 2.1.4.2 France

- 2.1.4.2.1 Market

- 2.1.4.2.1.1 Buyer Attributes

- 2.1.4.2.1.1.1 Charging Infrastructure, Government Subsidies, and Farm Information

- 2.1.4.2.1.2 Business Challenges

- 2.1.4.2.1.3 Business Drivers

- 2.1.4.2.2 Application

- 2.1.4.2.2.1 France Electric Farm Tractor Market (by Application)

- 2.1.4.2.3 Product

- 2.1.4.2.1 Market

- 2.1.4.3 Netherlands

- 2.1.4.3.1 Market

- 2.1.4.3.1.1 Buyer Attributes

- 2.1.4.3.1.1.1 Charging Infrastructure, Government Subsidies, and Farm Information

- 2.1.4.3.1.2 Business Challenges

- 2.1.4.3.1.3 Business Drivers

- 2.1.4.3.2 Application

- 2.1.4.3.2.1 Netherlands Electric Farm Tractor Market (by Application)

- 2.1.4.3.3 Product

- 2.1.4.3.1 Market

- 2.1.4.4 Norway

- 2.1.4.4.1 Market

- 2.1.4.4.1.1 Buyer Attributes

- 2.1.4.4.1.1.1 Charging Infrastructure, Government Subsidies, and Farm Information

- 2.1.4.4.1.2 Business Challenges

- 2.1.4.4.1.3 Business Drivers

- 2.1.4.4.2 Application

- 2.1.4.4.2.1 Norway Electric Farm Tractor Market (by Application)

- 2.1.4.4.3 Product

- 2.1.4.4.1 Market

- 2.1.4.5 Sweden

- 2.1.4.5.1 Market

- 2.1.4.5.1.1 Buyer Attributes

- 2.1.4.5.1.1.1 Charging Infrastructure, Government Subsidies, and Farm Information

- 2.1.4.5.1.2 Business Challenges

- 2.1.4.5.1.3 Business Drivers

- 2.1.4.5.2 Application

- 2.1.4.5.2.1 Sweden Electric Farm Tractor Market (by Application)

- 2.1.4.5.3 Product

- 2.1.4.5.1 Market

- 2.1.4.6 Greece

- 2.1.4.6.1 Market

- 2.1.4.6.1.1 Buyer Attributes

- 2.1.4.6.1.1.1 Charging Infrastructure, Government Subsidies, and Farm Information

- 2.1.4.6.1.2 Business Challenges

- 2.1.4.6.1.3 Business Drivers

- 2.1.4.6.2 Application

- 2.1.4.6.2.1 Greece Electric Farm Tractor Market (by Application)

- 2.1.4.6.3 Product

- 2.1.4.6.1 Market

- 2.1.4.7 Switzerland

- 2.1.4.7.1 Market

- 2.1.4.7.1.1 Buyer Attributes

- 2.1.4.7.1.1.1 Charging Infrastructure, Government Subsidies, and Farm Information

- 2.1.4.7.1.2 Business Challenges

- 2.1.4.7.1.3 Business Drivers

- 2.1.4.7.2 Application

- 2.1.4.7.2.1 Switzerland Electric Farm Tractor Market (by Application)

- 2.1.4.7.3 Product

- 2.1.4.7.1 Market

- 2.1.4.8 Ukraine

- 2.1.4.8.1 Market

- 2.1.4.8.1.1 Buyer Attributes

- 2.1.4.8.1.1.1 Charging Infrastructure, Government Subsidies, and Farm Information

- 2.1.4.8.1.2 Business Challenges

- 2.1.4.8.1.3 Business Drivers

- 2.1.4.8.2 Application

- 2.1.4.8.2.1 Ukraine Electric Farm Tractor Market (by Application)

- 2.1.4.8.3 Product

- 2.1.4.8.1 Market

- 2.1.4.9 Belgium

- 2.1.4.9.1 Market

- 2.1.4.9.1.1 Buyer Attributes

- 2.1.4.9.1.1.1 Charging Infrastructure, Government Subsidies, and Farm Information

- 2.1.4.9.1.2 Business Challenges

- 2.1.4.9.1.3 Business Drivers

- 2.1.4.9.2 Application

- 2.1.4.9.2.1 Belgium Electric Farm Tractor Market (by Application)

- 2.1.4.9.3 Product

- 2.1.4.9.1 Market

- 2.1.4.10 Rest-of-Europe

- 2.1.4.10.1 Market

- 2.1.4.10.1.1 Buyer Attributes

- 2.1.4.10.1.1.1 Charging Infrastructure, Government Subsidies, and Farm Information

- 2.1.4.10.1.2 Business Challenges

- 2.1.4.10.1.3 Business Drivers

- 2.1.4.10.2 Application

- 2.1.4.10.2.1 Rest-of-Europe Electric Farm Tractor Market (by Application)

- 2.1.4.10.3 Product

- 2.1.4.10.1 Market

- 2.1.4.1 Germany

- 2.1.1 Market

- 2.2 U.K.

- 2.2.1 Market

- 2.2.1.1 Buyer Attributes

- 2.2.1.1.1 Charging Infrastructure, Government Subsidies, and Farm Information

- 2.2.1.2 Key Companies in the U.K.

- 2.2.1.3 Business Drivers

- 2.2.1.4 Business Challenges

- 2.2.1.1 Buyer Attributes

- 2.2.2 Application

- 2.2.2.1 U.K. Electric Farm Tractor Market (by Application)

- 2.2.3 Product

- 2.2.3.1 U.K. Electric Farm Tractor Market (by Mode of Operation)

- 2.2.3.2 U.K. Electric Farm Tractor Market (by Drivetrain Technology)

- 2.2.1 Market

3 Markets - Competitive Benchmarking and Company Profiles

- 3.1 Competitive Benchmarking

- 3.1.1 Electric Farm Tractor Companies

- 3.2 Company Profiles

- 3.2.1 Rigitrac Traktorenbau AG

- 3.2.1.1 Company Overview

- 3.2.1.2 Role of Rigitrac Traktorenbau AG in the Electric Farm Tractor Market

- 3.2.1.3 Product Portfolio

- 3.2.1.4 Product Pricing

- 3.2.1.5 Customer Profiles

- 3.2.1.5.1 Target Customers

- 3.2.1.6 Analyst View

- 3.2.2 CLAAS KGaA mbH

- 3.2.2.1 Company Overview

- 3.2.2.2 Role of CLAAS KGaA mbH in the Electric Farm Tractor Market

- 3.2.2.3 Product Portfolio

- 3.2.2.4 Customer Profile

- 3.2.2.4.1 Target Customers

- 3.2.2.5 Corporate Strategies

- 3.2.2.5.1 Merger and Acquisition

- 3.2.2.6 Analyst View

- 3.2.3 EOX Tractors (Formerly H2Trac)

- 3.2.3.1 Company Overview

- 3.2.3.2 Role of EOX Tractors in the Electric Farm Tractor Market

- 3.2.3.3 Product Portfolio

- 3.2.3.4 Product Pricing

- 3.2.3.5 Customer Profiles

- 3.2.3.5.1 Target Customers

- 3.2.3.6 Corporate Strategies

- 3.2.3.6.1 Partnerships, Joint Ventures, Collaborations, and Alliances

- 3.2.3.7 Analyst View

- 3.2.4 EVE Srl

- 3.2.4.1 Company Overview

- 3.2.4.2 Role of EVE Srl in the Electric Farm Tractor Market

- 3.2.4.3 Product Portfolio

- 3.2.4.4 Customer Profiles

- 3.2.4.4.1 Target Customers

- 3.2.4.5 Analyst View

- 3.2.5 SABI AGRI

- 3.2.5.1 Company Overview

- 3.2.5.2 Role of SABI AGRI in the Electric Farm Tractor Market

- 3.2.5.3 Product Portfolio

- 3.2.5.4 Product Pricing

- 3.2.5.5 Customer Profiles

- 3.2.5.5.1 Target Customers

- 3.2.5.6 Analyst View

- 3.2.6 Other Key Players

- 3.2.1 Rigitrac Traktorenbau AG

4 Research Methodology

- 4.1 Data Sources

- 4.1.1 Primary Data Sources

- 4.1.2 Secondary Data Sources

- 4.1.3 Data Triangulation

- 4.2 Market Estimation and Forecast