|

|

市場調査レポート

商品コード

1393909

欧州の衛星・宇宙船サブシステム市場 - 分析と予測(2023年~2033年)Europe Satellite and Spacecraft Subsystem Market - Analysis and Forecast, 2023-2033 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 欧州の衛星・宇宙船サブシステム市場 - 分析と予測(2023年~2033年) |

|

出版日: 2023年12月08日

発行: BIS Research

ページ情報: 英文 109 Pages

納期: 1~5営業日

|

- 全表示

- 概要

- 図表

- 目次

衛星サブシステムに基づく欧州の衛星・宇宙船サブシステムの市場規模は、2022年の25億9,000万米ドルから2033年には120億6,000万米ドルに達すると予測され、予測期間の2023年~2033年の成長率は6.78%になると見込まれています。

欧州の衛星・宇宙船サブシステム市場は、新しい用途と継続的な技術改良の結果、近年大きく成長しています。この成長の主な原動力は商業宇宙産業であり、前例のない量の衛星打ち上げと軌道上の運用衛星総数の顕著な増加により、堅調な成長と継続的な成長の兆しを見せています。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2023年~2033年 |

| 2023年の評価額 | 62億5,000万米ドル |

| 2033年予測 | 120億6,000万米ドル |

| CAGR | 6.78% |

近年、欧州の衛星・宇宙船サブシステム産業は著しい拡大と発展を遂げています。キューブサット、スモールサット、再使用型ロケットなどの革新的技術が、宇宙分野拡大の原動力となっています。これらの開発により、宇宙システムの開発やペイロードを軌道に打ち上げるコストが削減され、より幅広い組織からの関心を集めています。スモールサットやキューブサットは、よりアクセスしやすい宇宙空間を提供し、衛星コンステレーションなどの新たなビジネスチャンスを開くものであるため、政府機関や企業はスモールサットやキューブサットの開発に特別な関心を示しています。2022年に打ち上げられた全衛星の約95%を占めるSmallSatsは、この分野の能力を大きく向上させました。

さらに、衛星コンステレーションは今後、欧州の宇宙市場で大きな役割を果たすと予想されます。これらの衛星コンステレーションは、地球上のどこからでも少なくとも1つの衛星に常に到達できることを保証します。この継続的なカバレッジは、通信、地球観測、測位システムなど、中断のない接続とデータ取得が重要な応用分野にとって特に価値があります。衛星コンステレーションが利用できるようになると、通信、農業、気候監視、災害対応など、さまざまな業界に新たな機会がもたらされます。

当レポートでは、欧州の衛星・宇宙船サブシステム市場について調査し、市場の概要とともに、エンドユーザー別、衛星サブシステム別、ローンチヴィークルサブシステム別、国別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

第1章 市場

- 業界の見通し

- ビジネスダイナミクス

- ビジネス上の促進要因

- ビジネス上の課題

- 事業戦略

- 経営戦略

- ビジネス上の機会

第2章 地域

- 衛星・宇宙船サブシステム市場(地域別)

- 欧州

- 市場

- 応用

- 製品

- 欧州(国別)

第3章 市場競合ベンチマーキングと企業プロファイル

- 競争力ベンチマーク

- 企業プロファイル

- Airbus S.A.S.

- OneWeb

- OHB System

第4章 調査手法

List of Figures

- Figure 1: Satellite and Spacecraft Subsystem Market (Satellite Subsystem), $Billion, 2022-2033

- Figure 2: Satellite and Spacecraft Subsystem Market (Satellite Subsystem), Units, 2022-2033

- Figure 3: Satellite and Spacecraft Subsystem Market (Launch Vehicle Subsystem), $Billion, 2022-2033

- Figure 4: Satellite and Spacecraft Subsystem Market (Launch Vehicle Subsystem), Units, 2022-2033

- Figure 5: Satellite and Spacecraft Subsystem Market (Deep Space Probe Subsystem), $Million, 2022-2033

- Figure 6: Satellite and Spacecraft Subsystem Market (Deep Space Probe Subsystem), Units, 2022-2033

- Figure 7: Satellite and Spacecraft Subsystem Market (by End User), $Million, 2023 and 2033

- Figure 8: Satellite and Spacecraft Subsystem Market (by End User), Units, 2023 and 2033

- Figure 9: Satellite and Spacecraft Subsystem Market (by Satellite Subsystem), $Million, 2023 and 2033

- Figure 10: Satellite and Spacecraft Subsystem Market (by Satellite Subsystem), Units, 2023 and 2033

- Figure 11: Satellite and Spacecraft Subsystem Market (by Launch Vehicle Subsystem), Units, 2023 and 2033

- Figure 12: Satellite and Spacecraft Subsystem Market (by Launch Vehicle Subsystem), $Million, 2023 and 2033

- Figure 13: Satellite and Spacecraft Subsystem Market (by Region, Satellite), $Billion, 2033

- Figure 14: Satellite and Spacecraft Subsystem Market (by Region, Launch Vehicle), $Billion, 2033

- Figure 15: Supply Chain Analysis for Satellite and Spacecraft Subsystem Market

- Figure 16: Satellite and Spacecraft Subsystem Market, Business Dynamics

- Figure 17: Share of Key Business Strategies and Developments, January 2020-June 2023

- Figure 18: Satellite and Spacecraft Subsystem Market Players, Benchmarking Score (Satellite), 2022

- Figure 19: Airbus S.A.S.: R&D Analysis, $Billion, 2020-2022

- Figure 20: OHB System: R&D Analysis, $Million, 2020-2022

- Figure 21: Research Methodology

- Figure 22: Top-Down and Bottom-Up Approach

- Figure 23: Assumptions and Limitations

List of Tables

- Table 1: New Product Launches, Developments, and Others, January 2020-June 2023

- Table 2: Partnerships, Collaborations, Agreements, Contracts, and Others, January 2020-June 2023

- Table 3: Mergers and Acquisitions, January 2020-June 2023

- Table 4: Satellite and Spacecraft Subsystem Market (by Region), Satellite Subsystem), Units and $Million, 2022-2033

- Table 5: Satellite and Spacecraft Subsystem Market (by Region, Launch Vehicle),Units and $Million, 2022-2033

- Table 6: Europe Satellite and Spacecraft Subsystem Market (by End User), Units and $Million, 2022-2033

- Table 7: Europe Satellite and Spacecraft Subsystem Market (by Satellite Subsystem), Units and $Million, 2022-2033

- Table 8: Europe Satellite and Spacecraft Subsystem Market (by Launch Vehicle Subsystem),$Million and Units, 2022-2033

- Table 9: France Satellite and Spacecraft Subsystem Market (by End User), Units and $Million, 2022-2033

- Table 10: Germany Satellite and Spacecraft Subsystem Market (by End User), Units and $Million, 2022-2033

- Table 11: Russia Satellite and Spacecraft Subsystem Market (by End User), Units and $Million, 2022-2033

- Table 12: U.K. Satellite and Spacecraft Subsystem Market (by End User), Units and $Million, 2022-2033

- Table 13: Rest-of-Europe Satellite and Spacecraft Subsystem Market (by End User), Units and $Million, 2022-2033

- Table 14: Benchmarking and Weightage Parameters

- Table 15: Airbus S.A.S.: Product Portfolio

- Table 16: Airbus S.A.S.: New Product Developments and Fundings

- Table 17: Airbus S.A.S.: Partnerships, Collaborations, Contracts, and Agreements

- Table 18: Airbus S.A.S.: Mergers and Acquisitions

- Table 19: OneWeb: Product Portfolio

- Table 20: OneWeb: New Product Developments and Fundings

- Table 21: OneWeb: Partnerships, Collaborations, Contracts, and Agreements

- Table 22: OHB System: Product Portfolio

- Table 23: OHB System: New Product Developments and Fundings

- Table 24: OHB System: Partnerships, Collaborations, Contracts, and Agreements

“The Europe Satellite and Spacecraft Subsystem Market Expected to Reach $12.06 Billion by 2033.”

Introduction to Europe Satellite and Spacecraft Subsystem Market

The Europe satellite and spacecraft subsystem market based on satellite subsystem is estimated to reach $12.06 billion by 2033 from $2.59 billion in 2022, at a growth rate of 6.78% during the forecast period 2023-2033. The market for satellite and spacecraft subsystems in Europe has grown significantly in recent years as a result of new applications and ongoing technological improvements. The primary engine of this growth is the commercial space industry, which has shown signs of robust growth and ongoing growth with an unprecedented quantity of satellite launches and a notable rise in the total number of operational satellites in orbit.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2023 - 2033 |

| 2023 Evaluation | $6.25 Billion |

| 2033 Forecast | $12.06 Billion |

| CAGR | 6.78% |

Market Introduction

In recent years, the European satellite and spacecraft subsystem industry has seen significant expansion and advancement. Innovative technologies such as CubeSats, SmallSats, and reusable launch vehicles have been the driving force behind the space sector's expansion. These developments have reduced the cost of developing space systems and launching payloads into orbit, which has drawn interest from a wider spectrum of organizations. Government organizations and corporate businesses have shown a special interest in the development of SmallSats and CubeSats because they provide more accessible space and open up new business opportunities, such as satellite constellations. SmallSats, which made up around 95% of all satellites launched in 2022, have greatly improved the capabilities of the sector.

Furthermore, satellite constellations are anticipated to play a major factor in the European space market going forward. These constellations guarantee that at all times at least one satellite is reachable from wherever on Earth. This continuous coverage is particularly valuable for applications such as telecommunications, Earth observation, and positioning systems, where uninterrupted connectivity and data acquisition are crucial. The availability of satellite constellations opens up new opportunities for various industries, including telecommunications, agriculture, climate monitoring, and disaster response, among others.

Market Segmentation:

Segmentation 1: by End User

- Commercial

- Civil Government

- Defense

- Academic/Research Group

Segmentation 2: by Satellite Subsystem

- Payload

- Electrical and Power Subsystem

- Command and Data Handling System

- Communication Subsystem

- Thermal Control Subsystem

- Attitude Determination and Control Subsystem

- Propulsion System

- Mechanism

- Actuator

- Structure

Segmentation 3: by Launch Vehicle Subsystem

- Structure

- Avionics

- Propulsion System

- Control System

- Electrical System

- Stage Separation

- Thermal System

Segmentation 5: by Country

- U.K.

- France

- Germany

- Russia

- Rest-of-Europe

How can this report add value to an organization?

Growth/Marketing Strategy: The Europe satellite and spacecraft subsystem market has seen major development by key players operating in the market, such as contract, collaboration, and joint venture. The favored strategy for the companies has been contracted to strengthen their position in the global satellite and spacecraft subsystem market

Competitive Strategy: Key players in the Europe satellite and spacecraft subsystem market analyzed and profiled in the study involve major Europe satellite and spacecraft subsystem companies providing subsystems, respectively. Moreover, a detailed market share analysis of the players operating in the Europe satellite and spacecraft subsystem market has been done to help the reader understand how players stack against each other, presenting a clear market landscape. Additionally, comprehensive competitive strategies such as partnerships, agreements, and collaborations will aid the reader in understanding the untapped revenue pockets in the market.

Methodology: The research methodology design adopted for this specific study includes a mix of data collected from primary and secondary data sources. Both primary resources (key players, market leaders, and in-house experts) and secondary research (a host of paid and unpaid databases), along with analytical tools, are employed to build the predictive and forecast models.

Key Market Players and Competition Synopsis

The companies that are profiled have been selected based on inputs gathered from primary experts and analyzing company coverage, product portfolio, and regional presence.

Some of the prominent names in this market are:

|

|

|

Table of Contents

1 Market

- 1.1 Industry Outlook

- 1.1.1 New Space Business Scenario: A Growth Factor in the Satellite and Spacecraft Subsystem Market

- 1.1.2 Impact of 3D Printing: Revolutionizing Space Industry

- 1.1.3 Changing Landscape of Space Composites

- 1.1.4 Impact of Commercial-Off-the-Shelf (COTS)Components in Satellite Serial Production

- 1.1.5 Supply Chain Analysis

- 1.2 Business Dynamics

- 1.2.1 Business Drivers

- 1.2.1.1 Increasing Research and Development Activities for Developing Cost-Efficient Subsystem and Component

- 1.2.1.2 Rising Demand for Satellite-Based Downstream Services

- 1.2.2 Business Challenges

- 1.2.2.1 Impact of Space Radiation on Spacecraft and Astronauts

- 1.2.2.2 Rising Impact of Cyberattacks on Satellites

- 1.2.2.3 Evolution of Standardized Satellite and Subsystem Platform

- 1.2.3 Business Strategies

- 1.2.3.1 New Product Launches, Developments, and Others

- 1.2.4 Corporate Strategies

- 1.2.4.1 Partnerships, Collaborations, Agreements, Contracts, and Others

- 1.2.4.2 Mergers and Acquisitions

- 1.2.5 Business Opportunities

- 1.2.5.1 Growing Developments for Cislunar Programs

- 1.2.1 Business Drivers

2 Region

- 2.1 Satellite and Spacecraft Subsystem Market (by Region)

- 2.2 Europe

- 2.2.1 Market

- 2.2.1.1 Key Manufacturers and Suppliers in Europe

- 2.2.1.2 Business Drivers

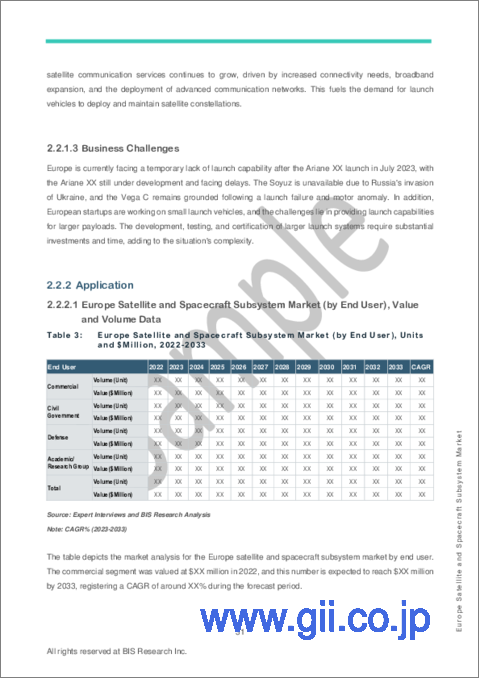

- 2.2.1.3 Business Challenges

- 2.2.2 Application

- 2.2.2.1 Europe Satellite and Spacecraft Subsystem Market (by End User), Value and Volume Data

- 2.2.3 Product

- 2.2.3.1 Europe Satellite and Spacecraft Subsystem Market (by Satellite Subsystem), Value and Volume Data

- 2.2.3.2 Europe Satellite and Spacecraft Subsystem Market (by Launch Vehicle Subsystem), Value and Volume Data

- 2.2.4 Europe (by Country)

- 2.2.4.1 France

- 2.2.4.1.1 Market

- 2.2.4.1.1.1 Key Manufacturers and Suppliers in France

- 2.2.4.1.2 Application

- 2.2.4.1.2.1 France Satellite and Spacecraft Subsystem Market (by End User), Value and Volume Data

- 2.2.4.1.1 Market

- 2.2.4.2 Germany

- 2.2.4.2.1 Market

- 2.2.4.2.1.1 Key Manufacturers and Suppliers in Germany

- 2.2.4.2.2 Application

- 2.2.4.2.2.1 Germany Satellite and Spacecraft Subsystem Market (by End User), Value and Volume Data

- 2.2.4.2.1 Market

- 2.2.4.3 Russia

- 2.2.4.3.1 Market

- 2.2.4.3.1.1 Key Manufacturers and Suppliers in Russia

- 2.2.4.3.2 Application

- 2.2.4.3.2.1 Russia Satellite and Spacecraft Subsystem Market (by End User), Value and Volume Data

- 2.2.4.3.1 Market

- 2.2.4.4 U.K.

- 2.2.4.4.1 Market

- 2.2.4.4.1.1 Key Manufacturers and Suppliers in the U.K.

- 2.2.4.4.2 Application

- 2.2.4.4.2.1 U.K. Satellite and Spacecraft Subsystem Market (by End User), Value and Volume Data

- 2.2.4.4.1 Market

- 2.2.4.5 Rest-of-Europe

- 2.2.4.5.1 Market

- 2.2.4.5.1.1 Key Manufacturers and Suppliers in the Rest-of-Europe

- 2.2.4.5.2 Application

- 2.2.4.5.2.1 Rest-of-Europe Satellite and Spacecraft Subsystem Market (by End User), Value and Volume Data

- 2.2.4.5.1 Market

- 2.2.4.1 France

- 2.2.1 Market

3 Market- Competitive Benchmarking and Company Profile

- 3.1 Competitve Benchmarking

- 3.2 Company Profiles

- 3.2.1 Airbus S.A.S.

- 3.2.1.1 Company Overview

- 3.2.1.1.1 Role of Airbus S.A.S. in the Satellite and Spacecraft Subsystem Market

- 3.2.1.1.2 Product Portfolio

- 3.2.1.2 Business Strategies

- 3.2.1.2.1 New Product Developments and Fundings

- 3.2.1.3 Corporate Strategies

- 3.2.1.3.1 Partnerships, Collaborations, Contracts, and Agreements

- 3.2.1.3.1 Mergers and Acquisitions

- 3.2.1.4 R&D Analysis

- 3.2.1.5 Analyst View

- 3.2.1.1 Company Overview

- 3.2.2 OneWeb

- 3.2.2.1 Company Overview

- 3.2.2.1.1 Role of OneWeb in the Satellite and Spacecraft Subsystem Market

- 3.2.2.1.2 Customers

- 3.2.2.1.3 Product Portfolio

- 3.2.2.2 Business Strategies

- 3.2.2.2.1 New Product Developments and Fundings

- 3.2.2.3 Corporate Strategies

- 3.2.2.3.1 Partnerships, Collaborations, Contracts, and Agreements

- 3.2.2.4 Analyst View

- 3.2.2.1 Company Overview

- 3.2.3 OHB System

- 3.2.3.1 Company Overview

- 3.2.3.1.1 Role of OHB System in the Satellite and Spacecraft Subsystem Market

- 3.2.3.1.2 Product Portfolio

- 3.2.3.2 Business Strategies

- 3.2.3.2.1 New Product Developments and Fundings

- 3.2.3.3 Corporate Strategies

- 3.2.3.3.1 Partnerships, Collaborations, Contracts, and Agreements

- 3.2.3.4 R&D Analysis

- 3.2.3.5 Analyst View

- 3.2.3.1 Company Overview

- 3.2.1 Airbus S.A.S.

4 Research Methodology

- 4.1 Factors for Data Prediction and Modeling