防衛用陸上プラットフォーム用エンジンの世界市場

Global Defense Land Platforms Engine Market- 発行日

- ページ情報

- 英文 150+ Pages

- 納期

- 3営業日

- 商品コード

- 2027687

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

- 航空宇宙/防衛関連専門 航空宇宙/防衛関連専門を専門とする市場調査会社です。

世界の防衛用陸上プラットフォーム用エンジン市場

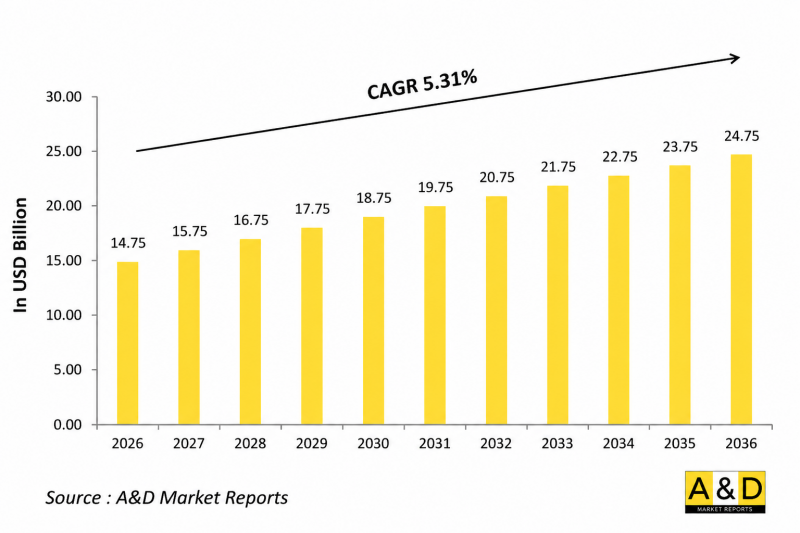

世界の防衛用陸上プラットフォーム用エンジンの市場規模は、2026年に推定147億5,000万米ドルであり、2036年までに247億5,000万米ドルに達すると予測され、2026年~2036年の予測期間にCAGRで5.31%の成長が見込まれています。

1. イントロダクション

世界の防衛用陸上プラットフォーム用エンジン市場は、軍用機動システムと戦闘車両システムにおける主要セグメントです。防衛用陸上プラットフォーム向けに設計されたエンジンは、主力戦車、歩兵戦闘車、装甲人員輸送車、戦術輸送ユニットなど、幅広い車両に動力を供給します。これらのエンジンは、過酷な地形、高温、戦闘環境などの極限条件下においても、高いトルク、耐久性、運用上の信頼性を発揮するよう設計されています。

現代の軍事作戦では、単に動力を供給するだけでなく、機動性、生存性、作戦の柔軟性を支えるエンジンが求められています。軍隊がネットワーク中心の戦争や迅速展開戦略へと移行する中、エンジンの性能は作戦上の有効性を左右する決定的な要因となっています。

この市場は、旧式フリートの更新や次世代戦闘車両の導入を目的とした、進行中の近代化プログラムの影響を受けています。さらに、軍が航続距離の延長と兵站負荷の軽減を図る中、ハイブリッド推進のコンセプトや燃費効率の向上が注目を集めています。国産化と技術的自立の重視も、この市場の進化をさらに形作っています。

2. 防衛用陸上プラットフォーム用エンジン市場における技術の影響

技術の進歩は、特に燃費効率、出力密度、ハイブリッド推進システムといった分野において、防衛用陸上プラットフォーム用エンジン市場を再構築しています。現代のエンジンは、小さなサイズと軽量さを維持しつつより高い出力を発揮するよう設計される傾向が強まっており、これにより車両の機動性と敏捷性が向上しています。

デジタルエンジン制御システムの統合により、パフォーマンスパラメーターのリアルタイムモニタリングと最適化が可能となり、信頼性が向上し、メンテナンス要件が軽減されています。また、先進の材料や製造技術により、耐久性や過酷な運用環境への耐性も向上しています。

ハイブリッド推進技術と電気推進技術は、燃料消費の削減、熱シグネチャの低減、ステルス性能の向上をもたらす変革的な動向として台頭しています。これらのシステムは、偵察や特殊作戦作戦において重要な、静粛な機動性もサポートします。

さらに、環境への配慮や運用上の持続可能性に対応するため、排出ガス制御技術や代替燃料の進歩も模索されています。これらのイノベーションは、ともに運用効率と作戦遂行能力の向上に寄与しています。

3. 防衛用陸上プラットフォーム用エンジン市場の主な促進要因

防衛用陸上プラットフォーム用エンジン市場は、現代の戦争における先進の機動性ソリューションへの需要の高まりによって牽引されています。軍隊は、高い性能と信頼性を維持しつつ、多様な地形を横断して運用可能な車両を必要としています。

主な促進要因の1つは、装甲車両の近代化です。老朽化したプラットフォームが、より効率的で強力なエンジンへとアップグレードされています。これにより、戦場での機動性と作戦上の有効性が向上します。

高性能エンジンへの需要は、迅速な展開能力や遠征能力への注目の高まりによっても後押しされています。軍事作戦においては、遠隔地や敵対的な環境においても迅速に輸送され、効率的に運用できる車両への需要がますます高まっています。

もう1つの大きな促進要因は、動的防護システム、強化装甲、統合電子機器などの先進技術を組み込んだ次世代戦闘車両の開発です。これらの機能には、より高い出力と効率性を備えたエンジンが求められます。

さらに、燃料消費と兵站負荷を削減しようとする動きが、ハイブリッド推進システムの採用を後押ししています。これにより、作戦継続時間が延長されるだけでなく、紛争時には脆弱になりがちな燃料サプライチェーンへの依存度も低減されます。

当レポートでは、世界の防衛用陸上プラットフォーム用エンジン市場について調査分析し、市場に影響を与える技術、今後10年間の予測、各地域の動向などの情報を提供しています。

目次

防衛用陸上プラットフォーム用エンジン市場レポートの定義

防衛用陸上プラットフォーム用エンジン市場のセグメンテーション

HP別

プラットフォーム別

地域別

防衛用陸上プラットフォーム用エンジン市場の今後10年間の分析

防衛用陸上プラットフォーム用エンジン市場の技術

世界の防衛用陸上プラットフォーム用エンジン市場の予測

地域の防衛用陸上プラットフォーム用エンジン市場の動向と予測

北米

促進要因、抑制要因、課題

PEST

市場予測とシナリオ分析

主要企業

サプライヤーのTierの状況

企業ベンチマーク

欧州

中東

アジア太平洋

南米

防衛用陸上プラットフォーム用エンジン市場の国の分析

米国

防衛計画

最新ニュース

特許

この市場における現在の技術成熟度

市場予測とシナリオ分析

カナダ

イタリア

フランス

ドイツ

オランダ

ベルギー

スペイン

スウェーデン

ギリシャ

オーストラリア

南アフリカ

インド

中国

ロシア

韓国

日本

マレーシア

シンガポール

ブラジル

防衛用陸上プラットフォーム用エンジン市場の機会マトリクス

防衛用陸上プラットフォーム用エンジン市場レポートに関する専門家の意見

結論

Aviation and Defense Market Reportsについて

- 発行日

- 発行

- Aviation & Defense Market Reports (A&D)

- ページ情報

- 英文 150+ Pages

- 納期

- 3営業日