|

|

市場調査レポート

商品コード

1489993

米国の生ゴミ処理機市場:見通しと予測(2024年~2029年)U.S. Garbage Disposal Unit Market - Industry Outlook & Forecast 2024-2029 |

||||||

|

|||||||

|

|||||||

| 米国の生ゴミ処理機市場:見通しと予測(2024年~2029年) |

|

出版日: 2024年06月05日

発行: Arizton Advisory & Intelligence

ページ情報: 英文 173 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

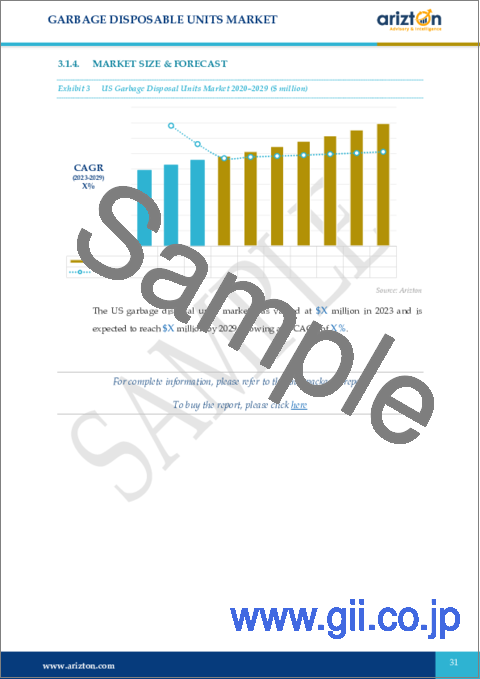

米国の生ゴミ処理機の市場規模は、2023年~2029年に4.71%のCAGRで拡大すると予測されています。

世界の廃棄物危機の深刻化は、廃棄物管理における革新的ソリューションの緊急ニーズを反映しています。政府や地方自治体が廃棄物管理の圧倒的な責任に取り組む中で、スマートテクノロジーの統合は、既存のシステムを合理化し効率を高めるための重要な戦略として浮上しています。米国の生ゴミ処理機市場にスマート技術を取り入れることは、効率性、持続可能性、利用者の利便性向上への変革的飛躍を意味します。スマート生ゴミ処理機は、IoT(モノのインターネット)、センサー、接続性などの最先端技術を活用して機能を強化します。これらの装置は、ゴミ処理プロセスのリアルタイム監視、制御、最適化をユーザーに提供するよう設計されています。また、スマートホーム技術への需要が高まり続ける中、生ゴミ処理機にスマート機能を統合することは、市場の標準になりつつあります。この動向を認識しているベンダーは、ユーザー体験を向上させ、より持続可能で効率的な廃棄物管理の実践に貢献しています。

都市化と可処分所得は住宅動向を大きく形成し、結果として米国の生ゴミ処理機業界に影響を与えます。都市部の発展に伴い、家庭用生ゴミ処理機を含む効率的な廃棄物管理ソリューションへの需要が高まっています。都市環境では人口密度が高いため、コンパクトで便利なゴミ処理方法が必要とされることが多いです。都市部に住む人が増えれば、生ゴミ処理機の需要も堅調に推移するとみられています。都市環境の住宅所有者は、生活空間の利便性と清潔さを高めるために、生ゴミ処理機の設置やアップグレードを優先するかもしれません。生ゴミ処理機は、有機物を現場で処理することで埋め立てゴミの削減に貢献できるため、これはより広範な持続可能性の動向と一致します。また、住宅動向はディスポーザーの需要をさらに押し上げます。住宅所有者がキッチンを改築したり新築に投資したりする際に、近代的で持続可能な技術を取り入れることが重視されるようになっています。

当レポートでは、米国の生ゴミ処理機市場について調査し、市場の概要とともに、製品タイプ別、用途別、動力別、流通チャネル別、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

第1章 範囲と対象範囲

第2章 重要考察

第3章 市場の概要

第4章 イントロダクション

第5章 市場機会と動向

- スマートテクノロジーの統合

- コンパクトで省スペースなユニットの採用

- 次世代ゴミ処理機のイントロダクション

第6章 市場の促進要因

第7章 市場の抑制要因

第8章 市場情勢

- 市場概要

- 消費者行動と意識

- 市場規模と予測

- ファイブフォース分析

第9章 製品タイプ

- 市場スナップショットと成長促進要因

- 市場概要

- 連続フィード

- バッチフィード

第10章 用途

- 市場スナップショットと成長促進要因

- 市場概要

- 住宅

- 商用

第11章 動力

- 市場スナップショットと成長促進要因

- 市場概要

- 0~0.5HP

- 0.55~1HP

- 1HP以上

第12章 流通チャネル

- 市場スナップショットと成長促進要因

- 市場概要

- オフライン

- オンライン

第13章 地域

第14章 南部

第15章 西部

第16章 中西部

第17章 北東部

第18章 競合情勢

- 競合概要

第19章 主要企業プロファイル

- WASTE KING

- WHIRLPOOL CORPORATION

第20章 その他の主要ベンダー

- BLANCO

- GE APPLIANCES

- SALVAJOR

- HOBART

- FRIGIDAIRE

- FRANKE GROUP

- HANGZHOU CLEESINK MECHANICAL & ELECTRICAL

- JONECA COMPANY

- KOHLER

- KRAUS USA PLUMBING

- LONGBANK

- MOUNTAIN PLUMBING PRODUCTS

- MOEN

- SHUN HING ELECTRIC WORKS AND ENGINEERING

第21章 報告書の概要

第22章 定量的要約

第23章 付録

List Of Exhibits

LIST OF EXHIBITS

- EXHIBIT 1 MARKET SIZE CALCULATION APPROACH (2023)

- EXHIBIT 2 FLOW OF FOOD WASTE USING GARBAGE DISPOSAL UNITS

- EXHIBIT 3 LIFECYCLE OF FOOD WASTAGE USING DISPOSAL UNIT

- EXHIBIT 4 IMPACT OF INTEGRATION OF SMART TECHNOLOGY

- EXHIBIT 5 IMPACT OF ADOPTION OF COMPACT & SPACE-SAVING UNITS

- EXHIBIT 6 IMPACT OF INTRODUCTION OF NEXT-GENERATION GARBAGE DISPOSALS

- EXHIBIT 7 IMPACT OF GOVERNMENT INITIATIVES & REGULATIONS

- EXHIBIT 8 IMPACT OF URBANIZATION & HOUSING TRENDS

- EXHIBIT 9 IMPACT OF INCREASING DEMAND FOR SUSTAINABLE SOLUTIONS

- EXHIBIT 10 IMPACT OF ENVIRONMENTAL IMPACT

- EXHIBIT 11 IMPACT OF HIGH INITIAL COST

- EXHIBIT 12 IMPACT OF SHIFT TOWARD OTHER ADVANCED TECHNOLOGIES

- EXHIBIT 13 US GARBAGE DISPOSAL UNITS MARKET 2020-2029 ($ MILLION)

- EXHIBIT 14 FIVE FORCES ANALYSIS (2023)

- EXHIBIT 15 INCREMENTAL GROWTH BY PRODUCT TYPE (2023 & 2029)

- EXHIBIT 16 US CONTINUOUS FEED GARBAGE DISPOSAL UNIT MARKET 2020-2029 ($ MILLION)

- EXHIBIT 17 US BATCH FEED GARBAGE DISPOSAL UNIT MARKET 2020-2029 ($ MILLION)

- EXHIBIT 18 INCREMENTAL GROWTH BY APPLICATIONS (2023 & 2029)

- EXHIBIT 19 GARBAGE DISPOSAL UNITS MARKET IN RESIDENTIAL APPLICATION 2020-2029 ($ MILLION)

- EXHIBIT 20 GARBAGE DISPOSAL HORSEPOWER IN COMMERCIAL APPLICATIONS

- EXHIBIT 21 GARBAGE DISPOSAL UNITS MARKET IN COMMERCIAL APPLICATION 2020-2029 ($ MILLION)

- EXHIBIT 22 INCREMENTAL GROWTH BY POWER (2023 & 2029)

- EXHIBIT 23 GARBAGE DISPOSAL UNITS MARKET WITH 0-0.5 HP 2020-2029 ($ MILLION)

- EXHIBIT 24 GARBAGE DISPOSAL UNITS MARKET WITH 0.55-1 HP 2020-2029 ($ MILLION)

- EXHIBIT 25 GARBAGE DISPOSAL UNITS MARKET WITH ABOVE 1 HP 2020-2029 ($ MILLION)

- EXHIBIT 26 INCREMENTAL GROWTH BY DISTRIBUTION CHANNEL (2023 & 2029)

- EXHIBIT 27 GARBAGE DISPOSAL UNITS MARKET BY OFFLINE CHANNEL 2020-2029 ($ MILLION)

- EXHIBIT 28 US GARBAGE DISPOSAL UNITS MARKET BY ONLINE CHANNEL 2020-2029 ($ MILLION)

- EXHIBIT 29 INCREMENTAL GROWTH BY REGION (2023 & 2029)

- EXHIBIT 30 US MARKEY REVENUE BY REGIONS 2023 ($ MILLION)

- EXHIBIT 31 SOUTHERN US GARBAGE DISPOSAL UNIT MARKET 2020-2029 ($ MILLION)

- EXHIBIT 32 WESTERN US GARBAGE DISPOSAL UNITS 2020-2029 ($ MILLION)

- EXHIBIT 33 MIDWEST US GARBAGE DISPOSAL UNITS 2020-2029 ($ MILLION)

- EXHIBIT 34 NORTHEAST US GARBAGE DISPOSAL UNITS 2020-2029 ($ MILLION)

- EXHIBIT 35 COMPANY MARKET SHARE ANALYSIS

- EXHIBIT 36 US COMPANY MARKET SHARE GARBAGE DISPOSERS MARKET

- EXHIBIT 37 KEY TRENDS SHAPING INDUSTRY

- EXHIBIT 38 KEY CAVEATS

List Of Tables

LIST OF TABLES

- TABLE 1 INSTALLATION OF GARBAGE DISPOSAL UNIT MAXIMIZE SAVINGS ($)

- TABLE 2 AVERAGE GARBAGE DISPOSAL INSTALLATION COST

- TABLE 3 TYPES OF GARBAGE DISPOSAL UNITS

- TABLE 4 TYPES OF GARBAGE DISPOSAL UNITS

- TABLE 5 PRICES OF GARBAGE DISPOSALS WITH DIFFERENT POWER

- TABLE 6 CHOOSING GARBAGE DISPOSAL SIZE

- TABLE 7 BRANDS WITH PRICE RANGE

- TABLE 8 WASTE KING: MAJOR PRODUCT OFFERINGS

- TABLE 9 WHIRLPOOL CORPORATION: MAJOR PRODUCT OFFERINGS

- TABLE 10 BLANCO: MAJOR PRODUCT OFFERINGS

- TABLE 11 GE APPLIANCES: MAJOR PRODUCT OFFERINGS

- TABLE 12 SALVAJOR: MAJOR PRODUCT OFFERINGS

- TABLE 13 HOBART: MAJOR PRODUCT OFFERINGS

- TABLE 14 FRIGIDAIRE: MAJOR PRODUCT OFFERINGS

- TABLE 15 FRANKE GROUP: MAJOR PRODUCT OFFERINGS

- TABLE 16 HANGZHOU CLEESINK MECHANICAL & ELECTRICAL: MAJOR PRODUCT OFFERINGS

- TABLE 17 JONECA COMPANY: MAJOR PRODUCT OFFERINGS

- TABLE 18 KOHLER: MAJOR PRODUCT OFFERINGS

- TABLE 19 KRAUS USA PLUMBING: MAJOR PRODUCT OFFERINGS

- TABLE 20 LONGBANK: MAJOR PRODUCT OFFERINGS

- TABLE 21 MOUNTAIN PLUMBING PRODUCTS: MAJOR PRODUCT OFFERINGS

- TABLE 22 MOEN: MAJOR PRODUCT OFFERINGS

- TABLE 23 SHUN HING ELECTRIC WORKS AND ENGINEERING: MAJOR PRODUCT OFFERINGS

- TABLE 24 US GARBAGE DISPOSAL UNITS MARKET 2023-2029 ($ MILLION)

- TABLE 25 US GARBAGE DISPOSAL MARKET BY PRODUCT TYPE 2023-2029 ($ MILLION)

- TABLE 26 US GARBAGE DISPOSAL UNITS MARKET BY POWER 2023-2029 ($ MILLION)

- TABLE 27 US GARBAGE DISPOSAL MARKET BY APPLICATIONS 2023-2029 ($ MILLION)

- TABLE 28 US GARBAGE DISPOSAL MARKET BY DISTRIBUTION CHANNEL 2023-2029 ($ MILLION)

- TABLE 29 CURRENCY CONVERSION (2016-2023)

The U.S. garbage disposal unit market is expected to grow at a CAGR of 4.71% from 2023-2029.

MARKET TRENDS & DRIVERS

Integration of Smart Technology

The escalating global waste crisis reflects the urgent need for innovative solutions in waste management. As governments and local authorities grapple with the overwhelming responsibility of waste management, integrating smart technologies emerges as a crucial strategy to streamline and enhance the efficiency of existing systems. Integrating smart technology into the U.S. garbage disposal unit market represents a transformative leap toward efficiency, sustainability, and user convenience. Smart garbage disposal units leverage cutting-edge technologies such as IoT (Internet of Things), sensors, and connectivity to enhance their functionality. These units are designed to provide users with real-time monitoring, control, and optimization of waste disposal processes. Also, as the demand for smart home technologies continues to rise, integrating smart features in garbage disposal units is poised to become a standard in the market. Vendors recognizing this trend enhance user experience and contribute to more sustainable and efficient waste management practices.

Urbanization & Housing Trends

Urbanization & disposable income significantly shape housing trends and, consequently, influence the U.S. garbage disposal unit industry. As urban areas grow, there is an increased demand for efficient waste management solutions, including home garbage disposal units. The higher population density in urban environments often necessitates compact and convenient waste disposal methods. With more people living in urban areas, the demand for garbage disposal units will likely remain robust. Homeowners in urban settings may prioritize installing or upgrading garbage disposal units to enhance the convenience and cleanliness of their living spaces. This aligns with broader sustainability trends, as these units can contribute to reducing landfill waste by processing organic matter on-site. Also, housing trends further drive the demand for garbage disposal units, especially during renovations and newly built houses. As homeowners renovate their kitchens or invest in new constructions, there is a growing emphasis on integrating modern and sustainable technologies.

SEGMENTATION INSIGHTS

INSIGHTS BY PRODUCT TYPE

The continuous feed product type holds the largest U.S. garbage disposal unit market share. Continuous feed garbage disposal units, which enable waste disposal while continuously adding waste, have historically dominated the market due to their convenience, especially in residential and smaller commercial settings. However, batch feed units, requiring waste to be loaded before operation and offering added safety benefits, are growing prominently in the market during the forecast period. For households with safety concerns-fearless handypersons, curious kids, or adventurous pets-the batch feed disposal is favored for its safety features. The absence of activation switches ensures protection against accidental injuries. Companies that offer batch-feed garbage disposals include InSinkErator, Waste King, and MOEN. These companies provide models with varying features and capacities.

Segmentation by Product Type

- Continuous Feed

- Batch Feed

INSIGHTS BY APPLICATIONS

The U.S. garbage disposal unit market by applications is segmented into residential and commercial. The residential applications segment stands out as a dominant force, driven by the increasing demand for convenient and hygienic waste disposal solutions, especially in the growing trend of smart homes. Conversely, commercial applications, particularly within the hospitality and food service industries, are witnessing rapid growth fueled by stringent waste management regulations and a heightened focus on environmental sustainability. Further, the residential segment will likely grow at an absolute rate of 30-35% during the forecast period. With both sectors showcasing significant potential for expansion, the market is poised for continued growth and innovation to meet the diverse needs of consumers and businesses alike.

Segmentation by Applications

- Residential

- Commercial

INSIGHTS BY POWER

The U.S. garbage disposal unit market by power is segmented as 0-0.5 HP, 0.55-1 HP, and above 1 HP. Garbage disposals, particularly with horsepower ranging from 0 to 0.5 HP, dominate the market owing to the widespread adoption in households. The demand for garbage disposal units with 0-0.5 horsepower has risen as lower horsepower models are generally more affordable, making them an attractive option for budget-conscious consumers. Additionally, homes with limited space, common in urban or smaller living environments, often require compact appliances that can still handle everyday kitchen waste. The 0-0.5 horsepower range balances space efficiency and functionality, providing adequate power for standard food waste disposal without the need for excessive space or higher investment. However, the segment with horsepower between 0.55 and 1 HP is projected to witness the highest compound annual growth rate (CAGR), driven by the growing demand for more powerful units in both residential and light commercial sectors.

Segmentation by Power

- 0-0.5 HP

- 0.55-1 HP

- Above 1 HP

INSIGHTS BY DISTRIBUTION CHANNEL

The offline distribution channel dominated the U.S. garbage disposal unit market in 2023. offline channels, including specialty stores, home improvement centers, and appliance stores, dominate the market share owing to their established presence and personalized customer service. On the other hand, online platforms provide a wide range of options, easy comparison, and doorstep delivery, which appeals to both residential and commercial consumers. This segment is projected to witness the market's highest compound annual growth rate (CAGR) during the forecast period.

Segmentation by Distribution Channel

- Offline

- Online

REGIONAL ANALYSIS

Regional dynamics significantly shape consumer preferences and U.S. garbage disposal unit market trends. In the South, where warmer climates prevail, there is a greater emphasis on convenience and functionality, leading to a preference for high-capacity and durable disposal units. The West, known for its eco-consciousness, sees a rising demand for energy-efficient and environmentally friendly disposal solutions, driving innovation in sustainable technologies. In the Midwest, affordability is often a key consideration, with consumers gravitating towards mid-range disposal units offering reliable performance at competitive prices. Furthermore, in the Northeast, where urban spaces are more densely populated and compact, noise-reducing disposal units are favored, reflecting the importance of space optimization and noise mitigation in residential settings. The South region held the most prominent share of the U.S. garbage disposal unit market, valued at over USD 292 million in 2023. The considerable surge in disposable income in the region has created a high demand for garbage disposal units in the Southern region.

Segmentation by Geography

- The U.S.

- South

- Midwest

- Northeast

- West

COMPETITIVE LANDSCAPE

The U.S. garbage disposal unit market is characterized by intense competition among key players, including prominent manufacturers such as InSinkErator, Waste Management, and MOEN. InSinkErator holds a significant market share with its innovative products and established brand reputation. Waste Management dominates the waste collection and disposal segment, leveraging its extensive network and comprehensive waste management services. MOEN, a leading faucet manufacturer, has entered the U.S. garbage disposal unit industry with its line of garbage disposals, adding to the competitive dynamics. Additionally, several smaller players and emerging startups contribute to the competitive landscape by introducing niche products and technologies, driving innovation and market diversification.

Key Company Profiles

- WASTE KING

- Whirlpool Corporation

Other Prominent Vendors

- BLANCO

- GE Appliances

- SALVAJOR

- Hobart

- Frigidaire

- Franke Group

- Hangzhou Cleesink Mechanical & Electrical

- Joneca Company

- Kohler

- Kraus USA Plumbing

- Longbank

- Mountain Plumbing Products

- Moen

- SHUN HING ELECTRIC WORKS AND ENGINEERING

KEY QUESTIONS ANSWERED:

1.What is the growth rate of the U.S. garbage disposal unit market?

2.How big is the U.S. garbage disposal unit market?

3.Which region dominated the U.S. garbage disposal unit market share?

4.Who are the key players in the U.S. garbage disposal unit market?

5.What are the significant U.S. garbage disposal unit industry trends?

TABLE OF CONTENTS

1. SCOPE & COVERAGE

- 1.1. MARKET DEFINITION

- 1.1.1. INCLUSIONS

- 1.1.2. EXCLUSIONS

- 1.1.3. MARKET ESTIMATION CAVEATS

- 1.2. SEGMENTS COVERED & DEFINITIONS

- 1.2.1. MARKET BY PRODUCT TYPE

- 1.2.2. MARKET BY APPLICATIONS

- 1.2.3. MARKET BY POWER

- 1.2.4. MARKET BY DISTRIBUTION CHANNEL

- 1.2.5. COUNTRY COVERED

- 1.3. MARKET DERIVATION

- 1.3.1. HISTORIC, BASE & FORECAST YEARS

2. PREMIUM INSIGHTS

- 2.1. OPPORTUNITY POCKETS

- 2.1.1. MARKET MATURITY INDICATOR

- 2.1.2. COUNTRY INSIGHTS

- 2.2. MARKET DEFINITION

- 2.3. REPORT OVERVIEW

- 2.4. SEGMENT ANALYSIS

- 2.4.1. INSIGHTS BY PRODUCT TYPE

- 2.4.2. INSIGHTS BY APPLICATION

- 2.4.3. INSIGHTS BY POWER

- 2.4.4. INSIGHTS BY DISTRIBUTION CHANNEL

- 2.4.5. REGIONAL ANALYSIS

- 2.5. COMPETITIVE LANDSCAPE

3. MARKET AT A GLANCE

4. INTRODUCTION

- 4.1. OVERVIEW

- 4.2. LIFECYCLE OF FOOD WASTAGE

- 4.3. THE BAN ON GARBAGE DISPOSAL UNITS: UNVEILING REASONS

- 4.4. FOOD WASTE LAWS BY STATES

- 4.5. IMPACT OF COVID-19

5. MARKET OPPORTUNITIES & TRENDS

- 5.1. INTEGRATION OF SMART TECHNOLOGY

- 5.2. ADOPTION OF COMPACT & SPACE-SAVING UNITS

- 5.3. INTRODUCTION OF NEXT-GENERATION GARBAGE DISPOSALS

6. MARKET GROWTH ENABLERS

- 6.1. GOVERNMENT INITIATIVES & REGULATIONS

- 6.2. URBANIZATION & HOUSING TRENDS

- 6.3. INCREASING DEMAND FOR SUSTAINABLE SOLUTIONS

7. MARKET RESTRAINTS

- 7.1. ENVIRONMENTAL IMPACT

- 7.2. HIGH INITIAL COST

- 7.3. SHIFT TOWARD OTHER ADVANCED TECHNOLOGIES

8. MARKET LANDSCAPE

- 8.1. MARKET OVERVIEW

- 8.1.1. DEMAND INSIGHTS

- 8.1.2. SUPPLY INSIGHTS

- 8.2. CONSUMER BEHAVIOR & AWARENESS

- 8.3. MARKET SIZE & FORECAST

- 8.4. FIVE FORCES ANALYSIS

- 8.4.1. THREAT OF NEW ENTRANTS

- 8.4.2. BARGAINING POWER OF SUPPLIERS

- 8.4.3. BARGAINING POWER OF BUYERS

- 8.4.4. THREAT OF SUBSTITUTES

- 8.4.5. COMPETITIVE RIVALRY

9. PRODUCT TYPE

- 9.1. MARKET SNAPSHOT & GROWTH ENGINE

- 9.2. MARKET OVERVIEW

- 9.3. CONTINUOUS FEED

- 9.3.1. MARKET SIZE & FORECAST

- 9.4. BATCH FEED

- 9.4.1. MARKET SIZE & FORECAST

10. APPLICATIONS

- 10.1. MARKET SNAPSHOT & GROWTH ENGINE

- 10.2. MARKET OVERVIEW

- 10.3. RESIDENTIAL

- 10.3.1. MARKET SIZE & FORECAST

- 10.4. COMMERCIAL

- 10.4.1. MARKET SIZE & FORECAST

11. POWER

- 11.1. MARKET SNAPSHOT & GROWTH ENGINE

- 11.2. MARKET OVERVIEW

- 11.3. 0-0.5 HP

- 11.3.1. MARKET SIZE & FORECAST

- 11.4. 0.55-1 HP

- 11.4.1. MARKET SIZE & FORECAST

- 11.5. ABOVE 1 HP

- 11.5.1. MARKET SIZE & FORECAST

12. DISTRIBUTION CHANNEL

- 12.1. MARKET SNAPSHOT & GROWTH ENGINE

- 12.2. MARKET OVERVIEW

- 12.3. OFFLINE

- 12.3.1. MARKET SIZE & FORECAST

- 12.4. ONLINE

- 12.4.1. MARKET SIZE & FORECAST

13. REGION

- 13.1. MARKET SNAPSHOT & GROWTH ENGINE

- 13.2. MARKET OVERVIEW

14. SOUTH

- 14.1. MARKET OVERVIEW

- 14.2. MARKET SIZE & FORECAST

15. WEST

- 15.1. MARKET OVERVIEW

- 15.2. MARKET SIZE & FORECAST

16. MIDWEST

- 16.1. MARKET OVERVIEW

- 16.2. MARKET SIZE & FORECAST

17. NORTHEAST

- 17.1. MARKET OVERVIEW

- 17.2. MARKET SIZE & FORECAST

18. COMPETITIVE LANDSCAPE

- 18.1. COMPETITION OVERVIEW

19. KEY COMPANY PROFILES

- 19.1. WASTE KING

- 19.1.1. BUSINESS OVERVIEW

- 19.1.2. PRODUCT OFFERINGS

- 19.1.3. KEY STRATEGIES

- 19.1.4. KEY STRENGTHS

- 19.1.5. KEY OPPORTUNITIES

- 19.2. WHIRLPOOL CORPORATION

- 19.2.1. BUSINESS OVERVIEW

- 19.2.2. PRODUCT OFFERINGS

- 19.2.3. KEY STRATEGIES

- 19.2.4. KEY STRENGTHS

- 19.2.5. KEY OPPORTUNITIES

20. OTHER PROMINENT VENDORS

- 20.1. BLANCO

- 20.1.1. BUSINESS OVERVIEW

- 20.1.2. PRODUCT OFFERINGS

- 20.2. GE APPLIANCES

- 20.2.1. BUSINESS OVERVIEW

- 20.2.2. PRODUCT OFFERINGS

- 20.3. SALVAJOR

- 20.3.1. BUSINESS OVERVIEW

- 20.3.2. PRODUCT OFFERINGS

- 20.4. HOBART

- 20.4.1. BUSINESS OVERVIEW

- 20.4.2. PRODUCT OFFERINGS

- 20.5. FRIGIDAIRE

- 20.5.1. BUSINESS OVERVIEW

- 20.5.2. PRODUCT OFFERINGS

- 20.6. FRANKE GROUP

- 20.6.1. BUSINESS OVERVIEW

- 20.6.2. PRODUCT OFFERINGS

- 20.7. HANGZHOU CLEESINK MECHANICAL & ELECTRICAL

- 20.7.1. BUSINESS OVERVIEW

- 20.7.2. PRODUCT OFFERINGS

- 20.8. JONECA COMPANY

- 20.8.1. BUSINESS OVERVIEW

- 20.8.2. PRODUCT OFFERINGS

- 20.9. KOHLER

- 20.9.1. BUSINESS OVERVIEW

- 20.9.2. PRODUCT OFFERINGS

- 20.10. KRAUS USA PLUMBING

- 20.10.1. BUSINESS OVERVIEW

- 20.10.2. PRODUCT OFFERINGS

- 20.11. LONGBANK

- 20.11.1. BUSINESS OVERVIEW

- 20.11.2. PRODUCT OFFERINGS

- 20.12. MOUNTAIN PLUMBING PRODUCTS

- 20.12.1. BUSINESS OVERVIEW

- 20.12.2. PRODUCT OFFERINGS

- 20.13. MOEN

- 20.13.1. BUSINESS OVERVIEW

- 20.13.2. PRODUCT OFFERINGS

- 20.14. SHUN HING ELECTRIC WORKS AND ENGINEERING

- 20.14.1. BUSINESS OVERVIEW

- 20.14.2. PRODUCT OFFERINGS

21. REPORT SUMMARY

- 21.1. KEY TAKEAWAYS

- 21.2. STRATEGIC RECOMMENDATIONS

22. QUANTITATIVE SUMMARY

- 22.1. MARKET BY GEOGRAPHY

- 22.2. MARKET BY PRODUCT TYPE

- 22.2.1. MARKET SIZE & FORECAST

- 22.3. MARKET BY POWER

- 22.3.1. MARKET SIZE & FORECAST

- 22.4. MARKET BY APPLICATIONS

- 22.4.1. MARKET SIZE & FORECAST

- 22.5. MARKET BY DISTRIBUTION CHANNEL

- 22.5.1. MARKET SIZE & FORECAST

23. APPENDIX

- 23.1. RESEARCH METHODOLOGY

- 23.2. RESEARCH PROCESS

- 23.3. REPORT ASSUMPTIONS & CAVEATS

- 23.3.1. KEY CAVEATS

- 23.3.2. CURRENCY CONVERSION

- 23.4. ABBREVIATIONS