|

市場調査レポート

商品コード

1344334

燃料電池プラントバランス市場:材料別、コンポーネント別:世界の機会分析と産業予測、2023-2032年Fuel Cell Balance of Plant Market By Material, By Component : Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

|

|||||||

| 燃料電池プラントバランス市場:材料別、コンポーネント別:世界の機会分析と産業予測、2023-2032年 |

|

出版日: 2023年06月01日

発行: Allied Market Research

ページ情報: 英文 244 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

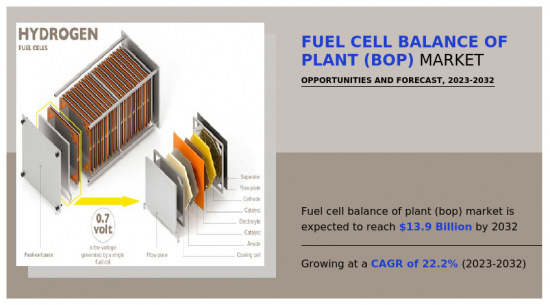

Allied Market Researchが発行した調査レポート「燃料電池プラントバランス(BOP)市場」によると、燃料電池プラントバランス(BOP)市場の2022年の市場規模は19億米ドルで、2032年には139億米ドルに達し、2023年から2032年までのCAGRは22.2%で成長すると予測されています。

燃料電池は、燃料(一般的には水素など)の化学エネルギーを利用して、クリーンかつ効率的に電気を生産する装置です。燃料電池プラントバランス(BOP)は、燃料電池が最適に機能するために不可欠なコンポーネントです。燃料電池プラントバランスには、燃料改質器、熱交換器、化学反応器、ファン/ブロワー、バーナーを必要とする燃料処理システム、タービン、コンプレッサー、熱交換器、モーター、ファンを必要とする空気管理システム、コンバーター、インバーター、バッテリー、モーターからなる電力調整システムなど、さまざまなコンポーネントが含まれます。世界の燃料電池プラントバランス(BOP)市場は、自動車、軍事、インフラ、産業など様々な用途での燃料電池需要の増加により、大きなペースで拡大すると予想されています。

BOP(バランス・オブ・プラント)に見られるパワーエレクトロニクスとコンバータは、効率的な電力変換と管理を促進する上で重要な役割を果たします。その主な機能は、燃料電池スタックによって生成された直流(DC)を、さまざまな用途に必要な交流(AC)に変換することです。この効果的な変換プロセスは、エネルギー損失を最小限に抑え、生成された電力の利用を最適化するのに役立ちます。燃料電池プラントバランス(BOP)の構成要素は、この技術の環境面での利点に貢献する重要な役割を果たしています。燃料電池は電気化学反応によって発電し、排出するのは水蒸気と最小限の汚染物質だけです。うまく設計されたBOPシステムを組み込むことで、効率的な空気ろ過、排ガス処理、騒音低減対策を通じて、環境面でのメリットをさらに高めることができます。

BOPコンポーネントを燃料電池システムに組み込むことは、システム全体のコストに寄与します。パワーエレクトロニクス、冷却システム、制御システムなどのコンポーネントは、製造や統合にコストがかかります。その結果、これらのコンポーネントに関連する追加費用によって、燃料電池システムは従来の発電技術に比べて高価になる可能性があります。このコスト要因は、燃料電池システムの普及に制限をもたらす可能性があります。BOPコンポーネントと燃料電池スタックおよびその他のシステム要素との統合は、さまざまな課題をもたらす可能性があります。適切な機能性、耐久性、性能を保証するためには、異なるコンポーネント、材料、サブシステム間の互換性を確保することが極めて重要です。しかし、これらのコンポーネントを統合するプロセスは、設計の複雑化、開発期間の長期化、コストの上昇につながる可能性があります。

燃料電池BOPコンポーネントは、太陽光や風力などの再生可能エネルギー源と統合し、ハイブリッド発電システムを構築することができます。この統合により、より持続可能で効率的なエネルギー生成・貯蔵ソリューションが可能になります。BOPコンポーネントは、こうしたハイブリッド・システムにおける電力入力、貯蔵、配電を管理し、安定性とグリッド互換性を提供する役割を果たすことができます。さまざまな燃料電池の用途や運転条件に合わせてBOPを最適化する機会が存在します。出力、動作温度範囲、応答時間といった特定の要件に合わせてBOPコンポーネントやシステムを調整することで、システム性能を向上させ、燃料電池システムをより幅広い用途に適用できるようになります。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 市場概要

- 市場の定義と範囲

- 主な調査結果

- 影響要因

- 主な投資機会

- ポーターのファイブフォース分析

- 市場力学

- 促進要因

- 効率的な電力変換

- 環境面でのメリット

- 安全性と制御システム

- 抑制要因

- システムの複雑さ

- 燃料電池のコスト増

- 互換性と統合の課題

- 機会

- コスト削減

- システムの最適化と柔軟性

- 再生可能エネルギーとの統合

- 促進要因

- COVID-19による市場への影響分析

- バリューチェーン分析

- 特許情勢

- 規制ガイドライン

第4章 燃料電池プラントバランス(BOP)市場:材料別

- 構造用プラスチック

- エラストマー

- 冷却剤

- 組立補助剤

- 金属

- その他

第5章 燃料電池プラントバランス(BOP)市場:コンポーネント別

- 電力供給

- 水循環

- 水素処理

- 冷却

- 熱安定剤

- その他

第6章 燃料電池プラントバランス(BOP)市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ・中東・アフリカ

- ブラジル

- サウジアラビア

- 南アフリカ

- その他の地域

第7章 競合情勢

- イントロダクション

- 主要成功戦略

- 主要10社の製品マッピング

- 競合ダッシュボード

- 競合ヒートマップ

- 主要企業のポジショニング、2022年

第8章 企業プロファイル

- INN Balance

- Cummins, Inc.

- Hydrogenics Corporation

- Ballard Power Systems

- Bloom Energy

- SFC Energy AG

- Doosan Fuel Cell Co., Ltd.

- HORIBA FuelCon GmbH

- Elcogen AS

- Dana Limited

LIST OF TABLES

- TABLE 01. GLOBAL FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 02. FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR STRUCTURAL PLASTICS, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR ELASTOMERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR COOLANTS, BY REGION, 2022-2032 ($MILLION)

- TABLE 05. FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR ASSEMBLY AIDS, BY REGION, 2022-2032 ($MILLION)

- TABLE 06. FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR METALS, BY REGION, 2022-2032 ($MILLION)

- TABLE 07. FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 08. GLOBAL FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 09. FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR POWER SUPPLY, BY REGION, 2022-2032 ($MILLION)

- TABLE 10. FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR WATER CIRCULATION, BY REGION, 2022-2032 ($MILLION)

- TABLE 11. FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR HYDROGEN PROCESSING, BY REGION, 2022-2032 ($MILLION)

- TABLE 12. FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR COOLING, BY REGION, 2022-2032 ($MILLION)

- TABLE 13. FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR HEAT STABILIZERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 14. FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 15. FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 16. NORTH AMERICA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 17. NORTH AMERICA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 18. NORTH AMERICA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 19. U.S. FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 20. U.S. FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 21. CANADA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 22. CANADA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 23. MEXICO FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 24. MEXICO FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 25. EUROPE FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 26. EUROPE FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 27. EUROPE FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 28. GERMANY FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 29. GERMANY FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 30. UK FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 31. UK FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 32. FRANCE FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 33. FRANCE FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 34. ITALY FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 35. ITALY FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 36. SPAIN FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 37. SPAIN FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 38. REST OF EUROPE FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 39. REST OF EUROPE FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 40. ASIA-PACIFIC FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 41. ASIA-PACIFIC FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 42. ASIA-PACIFIC FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 43. CHINA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 44. CHINA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 45. JAPAN FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 46. JAPAN FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 47. INDIA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 48. INDIA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 49. SOUTH KOREA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 50. SOUTH KOREA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 51. AUSTRALIA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 52. AUSTRALIA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 53. REST OF ASIA-PACIFIC FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 54. REST OF ASIA-PACIFIC FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 55. LAMEA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 56. LAMEA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 57. LAMEA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 58. BRAZIL FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 59. BRAZIL FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 60. SAUDI ARABIA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 61. SAUDI ARABIA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 62. SOUTH AFRICA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 63. SOUTH AFRICA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 64. REST OF LAMEA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 65. REST OF LAMEA FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 66. INN BALANCE: KEY EXECUTIVES

- TABLE 67. INN BALANCE: COMPANY SNAPSHOT

- TABLE 68. INN BALANCE: PRODUCT SEGMENTS

- TABLE 69. INN BALANCE: PRODUCT PORTFOLIO

- TABLE 70. CUMMINS, INC.: KEY EXECUTIVES

- TABLE 71. CUMMINS, INC.: COMPANY SNAPSHOT

- TABLE 72. CUMMINS, INC.: PRODUCT SEGMENTS

- TABLE 73. CUMMINS, INC.: PRODUCT PORTFOLIO

- TABLE 74. CUMMINS, INC.: KEY STRATERGIES

- TABLE 75. HYDROGENICS CORPORATION: KEY EXECUTIVES

- TABLE 76. HYDROGENICS CORPORATION: COMPANY SNAPSHOT

- TABLE 77. HYDROGENICS CORPORATION: PRODUCT SEGMENTS

- TABLE 78. HYDROGENICS CORPORATION: PRODUCT PORTFOLIO

- TABLE 79. BALLARD POWER SYSTEMS: KEY EXECUTIVES

- TABLE 80. BALLARD POWER SYSTEMS: COMPANY SNAPSHOT

- TABLE 81. BALLARD POWER SYSTEMS: PRODUCT SEGMENTS

- TABLE 82. BALLARD POWER SYSTEMS: PRODUCT PORTFOLIO

- TABLE 83. BALLARD POWER SYSTEMS: KEY STRATERGIES

- TABLE 84. BLOOM ENERGY: KEY EXECUTIVES

- TABLE 85. BLOOM ENERGY: COMPANY SNAPSHOT

- TABLE 86. BLOOM ENERGY: SERVICE SEGMENTS

- TABLE 87. BLOOM ENERGY: PRODUCT PORTFOLIO

- TABLE 88. BLOOM ENERGY: KEY STRATERGIES

- TABLE 89. SFC ENERGY AG: KEY EXECUTIVES

- TABLE 90. SFC ENERGY AG: COMPANY SNAPSHOT

- TABLE 91. SFC ENERGY AG: PRODUCT SEGMENTS

- TABLE 92. SFC ENERGY AG: PRODUCT PORTFOLIO

- TABLE 93. DOOSAN FUEL CELL CO., LTD.: KEY EXECUTIVES

- TABLE 94. DOOSAN FUEL CELL CO., LTD.: COMPANY SNAPSHOT

- TABLE 95. DOOSAN FUEL CELL CO., LTD.: SERVICE SEGMENTS

- TABLE 96. DOOSAN FUEL CELL CO., LTD.: PRODUCT PORTFOLIO

- TABLE 97. DOOSAN FUEL CELL CO., LTD.: KEY STRATERGIES

- TABLE 98. HORIBA FUELCON GMBH: KEY EXECUTIVES

- TABLE 99. HORIBA FUELCON GMBH: COMPANY SNAPSHOT

- TABLE 100. HORIBA FUELCON GMBH: SERVICE SEGMENTS

- TABLE 101. HORIBA FUELCON GMBH: PRODUCT PORTFOLIO

- TABLE 102. ELCOGEN AS: KEY EXECUTIVES

- TABLE 103. ELCOGEN AS: COMPANY SNAPSHOT

- TABLE 104. ELCOGEN AS: PRODUCT SEGMENTS

- TABLE 105. ELCOGEN AS: PRODUCT PORTFOLIO

- TABLE 106. DANA LIMITED: KEY EXECUTIVES

- TABLE 107. DANA LIMITED: COMPANY SNAPSHOT

- TABLE 108. DANA LIMITED: PRODUCT SEGMENTS

- TABLE 109. DANA LIMITED: PRODUCT PORTFOLIO

- TABLE 110. DANA LIMITED: KEY STRATERGIES

LIST OF FIGURES

- FIGURE 01. FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032

- FIGURE 03. TOP INVESTMENT POCKETS IN FUEL CELL BALANCE OF PLANT (BOP) MARKET (2023-2032)

- FIGURE 04. LOW BARGAINING POWER OF SUPPLIERS

- FIGURE 05. LOW THREAT OF NEW ENTRANTS

- FIGURE 06. LOW THREAT OF SUBSTITUTES

- FIGURE 07. LOW INTENSITY OF RIVALRY

- FIGURE 08. LOW BARGAINING POWER OF BUYERS

- FIGURE 09. DRIVERS, RESTRAINTS AND OPPORTUNITIES: GLOBALFUEL CELL BALANCE OF PLANT (BOP) MARKET

- FIGURE 10. PATENT ANALYSIS BY COMPANY

- FIGURE 11. PATENT ANALYSIS BY COUNTRY

- FIGURE 12. REGULATORY GUIDELINES: FUEL CELL BALANCE OF PLANT (BOP) MARKET

- FIGURE 12. FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL, 2022(%)

- FIGURE 13. COMPARATIVE SHARE ANALYSIS OF FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR STRUCTURAL PLASTICS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 14. COMPARATIVE SHARE ANALYSIS OF FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR ELASTOMERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR COOLANTS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR ASSEMBLY AIDS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR METALS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 19. FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT, 2022(%)

- FIGURE 20. COMPARATIVE SHARE ANALYSIS OF FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR POWER SUPPLY, BY COUNTRY 2022 AND 2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR WATER CIRCULATION, BY COUNTRY 2022 AND 2032(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR HYDROGEN PROCESSING, BY COUNTRY 2022 AND 2032(%)

- FIGURE 23. COMPARATIVE SHARE ANALYSIS OF FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR COOLING, BY COUNTRY 2022 AND 2032(%)

- FIGURE 24. COMPARATIVE SHARE ANALYSIS OF FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR HEAT STABILIZERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 25. COMPARATIVE SHARE ANALYSIS OF FUEL CELL BALANCE OF PLANT (BOP) MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 26. FUEL CELL BALANCE OF PLANT (BOP) MARKET BY REGION, 2022

- FIGURE 27. U.S. FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 28. CANADA FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 29. MEXICO FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 30. GERMANY FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 31. UK FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 32. FRANCE FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 33. ITALY FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 34. SPAIN FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 35. REST OF EUROPE FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 36. CHINA FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 37. JAPAN FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 38. INDIA FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 39. SOUTH KOREA FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 40. AUSTRALIA FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 41. REST OF ASIA-PACIFIC FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 42. BRAZIL FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 43. SAUDI ARABIA FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 44. SOUTH AFRICA FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 45. REST OF LAMEA FUEL CELL BALANCE OF PLANT (BOP) MARKET, 2022-2032 ($MILLION)

- FIGURE 46. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 47. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 48. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 49. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 50. COMPETITIVE DASHBOARD

- FIGURE 51. COMPETITIVE HEATMAP: FUEL CELL BALANCE OF PLANT (BOP) MARKET

- FIGURE 52. TOP PLAYER POSITIONING, 2022

- FIGURE 53. CUMMINS, INC.: RESEARCH & DEVELOPMENT EXPENDITURE, 2020-2022 ($MILLION)

- FIGURE 54. CUMMINS, INC.: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 55. CUMMINS, INC.: REVENUE SHARE BY SEGMENT, 2021 (%)

- FIGURE 56. CUMMINS, INC.: REVENUE SHARE BY REGION, 2021 (%)

- FIGURE 57. BALLARD POWER SYSTEMS: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 58. BALLARD POWER SYSTEMS: REVENUE SHARE BY SEGMENT, 2021 (%)

- FIGURE 59. BALLARD POWER SYSTEMS: REVENUE SHARE BY REGION, 2021 (%)

- FIGURE 60. BLOOM ENERGY: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 61. BLOOM ENERGY: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 62. SFC ENERGY AG: NET SALES, 2020-2022 ($MILLION)

- FIGURE 63. SFC ENERGY AG: REVENUE SHARE BY SEGMENT, 2021 (%)

- FIGURE 64. SFC ENERGY AG: REVENUE SHARE BY REGION, 2021 (%)

- FIGURE 65. DOOSAN FUEL CELL CO., LTD.: NET SALES, 2020-2022 ($MILLION)

- FIGURE 66. DOOSAN FUEL CELL CO., LTD.: REVENUE SHARE BY SEGMENT, 2021 (%)

- FIGURE 67. DANA LIMITED: NET SALES, 2020-2022 ($MILLION)

- FIGURE 68. DANA LIMITED: RESEARCH & DEVELOPMENT EXPENDITURE, 2020-2022 ($MILLION)

- FIGURE 69. DANA LIMITED: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 70. DANA LIMITED: REVENUE SHARE BY REGION, 2022 (%)

According to a new report published by Allied Market Research, titled, "Fuel Cell Balance of Plant (BOP) Market," The fuel cell balance of plant (BOP) market was valued at $1.9 billion in 2022, and is estimated to reach $13.9 billion by 2032, growing at a CAGR of 22.2% from 2023 to 2032.

A fuel cell is a device that utilizes the chemical energy of a fuel, typically hydrogen or others to cleanly and efficiently produce electricity. Fuel Cell Balance of Plant (BOP) are the vital components for the optimal functioning of the fuel cell. Fuel cell balance of plant includes various components such as fuel processing system that requires a fuel reformer, heat exchangers, chemical reactors, fans/blowers, and burner; air management system that requires a turbine, compressor, heat exchangers, motor, and fan; and power conditioning system that comprises a converter, inverter, batteries, and motor. The global fuel cell balance of plant (BOP) market is expected to expand at a significant pace owing to an increase in the demand for fuel cells in various applications such as automotive, military, infrastructure, and industrial.

The power electronics and converters found in the BOP (Balance of Plant) play a crucial role in facilitating efficient power conversion and management. Their main function is to transform the direct current (DC) generated by the fuel cell stack into the alternating current (AC) needed for different applications. This effective conversion process helps to minimize energy losses and optimize the utilization of the electricity produced. The components of the Balance of Plant (BOP) in fuel cells play a significant role in contributing to the environmental advantages of this technology. Fuel cells generate electricity via electrochemical reactions, emitting only water vapor and minimal pollutants. By incorporating well-designed BOP systems, environmental benefits can be further enhanced through efficient air filtration, exhaust gas treatment, and noise reduction measures.

The inclusion of BOP components in a fuel cell system contributes to its overall cost. Components like power electronics, cooling systems, and control systems can be costly to manufacture and integrate. As a result, the additional expenses associated with these components can make fuel cell systems more expensive compared to conventional power generation technologies. This cost factor can pose a limitation to the widespread adoption of fuel cell systems. The integration of BOP components with the fuel cell stack and other system elements can pose various challenges. Ensuring compatibility between different components, materials, and subsystems is crucial to guarantee proper functionality, durability, and performance. However, the process of integrating these components can lead to increased design complexity, longer development times, and higher costs.

Fuel cell BOP components can be integrated with renewable energy sources, such as solar or wind, to create hybrid power systems. This integration allows for a more sustainable and efficient energy generation and storage solution. BOP components can play a role in managing the power input, storage, and distribution in these hybrid systems, providing stability and grid compatibility. Opportunities exist to optimize the BOP for different fuel cell applications and operating conditions. Tailoring the BOP components and systems to specific requirements such as power output, operating temperature range, and response time, can enhance system performance and enable fuel cell systems to be applied in a wider range of applications.

The fuel cell balance of plants (BOP) market scope covers segmentation and is analyzed on the basis of material, component, and region. The report highlights the details of various materials used in fuel cell balance of plants (BOP) including structural plastics, elastomers, coolants, assembly aids, metals, and others. In addition, the component covered in the study includes the fuel cell balance of plants (BOP) market is segmented into power supply, water circulation, hydrogen processing, cooling, heat stabilizers, and others. Moreover, the report analyzes the current market trends of fuel cell balance of plants (BOP) across different regions such as North America, Europe, Asia-Pacific, and LAMEA (Latin America, the Middle East, and Africa), and suggests future growth opportunities. Assembly aids in the fuel cell balance of plants and refers to various materials, tools, and techniques used to facilitate the assembly and manufacturing processes of fuel cell systems. These aids help improve efficiency, accuracy, and reliability during the construction and integration of fuel cell components and systems. Some of the assembly aids such as adhesives & sealants, fixtures & jigs, fasteners, alignment tools, and handling & installation tools are made from different materials. Alignment tools are used to ensure accurate alignment of components during assembly. This is particularly important for fuel cell stacks, where proper alignment of individual cells is critical for optimal performance.

The key players operating profiled in the fuel cell balance of plants (BOP) industry are INN Balance, Cummins Inc., Hydrogenics Corporations, Ballard Power Systems, Bloom Energy, SFC Energy AG, Doosan Fuel Cell America, Inc., HORIBA Group, Elcogen AS, and Dana Limited. These players have been adopting various strategies to gain a higher share or to retain leading positions in the market.

The growth drivers, restraints, and opportunities are explained in the report to better understand the market dynamics. This report further highlights the key areas of investment. In addition, it includes Porter's five forces analysis to understand the competitive scenario of the industry and the role of each stakeholder. The report features strategies adopted by key market players to maintain their foothold in the market. Furthermore, it highlights the competitive landscape of key players to increase their market share and sustain the intense competition in the industry

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the fuel cell balance of plant (BOP) market analysis from 2022 to 2032 to identify the prevailing fuel cell balance of plant (BOP) market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the fuel cell balance of plant (BOP) market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global fuel cell balance of plant (BOP) market trends, key players, market segments, application areas, and market growth strategies.

Key Market Segments

By Material

- Structural Plastics

- Elastomers

- Coolants

- Assembly Aids

- Metals

- Others

By Component

- Power Supply

- Water Circulation

- Hydrogen Processing

- Cooling

- Heat Stabilizers

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- LAMEA

- Brazil

- Saudi Arabia

- South Africa

- Rest of LAMEA

Key Market Players:

- Ballard Power Systems

- Bloom Energy

- Cummins, Inc.

- Dana Limited

- Doosan Fuel Cell Co., Ltd.

- Elcogen AS

- HORIBA FuelCon GmbH

- Hydrogenics Corporation

- INN Balance

- SFC Energy AG

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research Methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.3.1. Low bargaining power of suppliers

- 3.3.2. Low threat of new entrants

- 3.3.3. Low threat of substitutes

- 3.3.4. Low intensity of rivalry

- 3.3.5. Low bargaining power of buyers

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.1.1. Efficient Power Conversion

- 3.4.1.2. Environmental Benefits

- 3.4.1.3. Safety and Control Systems

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.2.1. Complexity of the system

- 3.4.2.2. Cost addition to fuel cells

- 3.4.2.3. Compatibility and integration challenges

- 3.4.3. Opportunities

- 3.4.3.1. Cost reduction

- 3.4.3.2. System optimization and flexibility

- 3.4.3.3. Integration with renewable energy sources

- 3.5. COVID-19 Impact Analysis on the market

- 3.6. Value Chain Analysis

- 3.7. Patent Landscape

- 3.8. Regulatory Guidelines

CHAPTER 4: FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY MATERIAL

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Structural Plastics

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Elastomers

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.4. Coolants

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

- 4.5. Assembly Aids

- 4.5.1. Key market trends, growth factors and opportunities

- 4.5.2. Market size and forecast, by region

- 4.5.3. Market share analysis by country

- 4.6. Metals

- 4.6.1. Key market trends, growth factors and opportunities

- 4.6.2. Market size and forecast, by region

- 4.6.3. Market share analysis by country

- 4.7. Others

- 4.7.1. Key market trends, growth factors and opportunities

- 4.7.2. Market size and forecast, by region

- 4.7.3. Market share analysis by country

CHAPTER 5: FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY COMPONENT

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Power Supply

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Water Circulation

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

- 5.4. Hydrogen Processing

- 5.4.1. Key market trends, growth factors and opportunities

- 5.4.2. Market size and forecast, by region

- 5.4.3. Market share analysis by country

- 5.5. Cooling

- 5.5.1. Key market trends, growth factors and opportunities

- 5.5.2. Market size and forecast, by region

- 5.5.3. Market share analysis by country

- 5.6. Heat Stabilizers

- 5.6.1. Key market trends, growth factors and opportunities

- 5.6.2. Market size and forecast, by region

- 5.6.3. Market share analysis by country

- 5.7. Others

- 5.7.1. Key market trends, growth factors and opportunities

- 5.7.2. Market size and forecast, by region

- 5.7.3. Market share analysis by country

CHAPTER 6: FUEL CELL BALANCE OF PLANT (BOP) MARKET, BY REGION

- 6.1. Overview

- 6.1.1. Market size and forecast By Region

- 6.2. North America

- 6.2.1. Key trends and opportunities

- 6.2.2. Market size and forecast, by Material

- 6.2.3. Market size and forecast, by Component

- 6.2.4. Market size and forecast, by country

- 6.2.4.1. U.S.

- 6.2.4.1.1. Key market trends, growth factors and opportunities

- 6.2.4.1.2. Market size and forecast, by Material

- 6.2.4.1.3. Market size and forecast, by Component

- 6.2.4.2. Canada

- 6.2.4.2.1. Key market trends, growth factors and opportunities

- 6.2.4.2.2. Market size and forecast, by Material

- 6.2.4.2.3. Market size and forecast, by Component

- 6.2.4.3. Mexico

- 6.2.4.3.1. Key market trends, growth factors and opportunities

- 6.2.4.3.2. Market size and forecast, by Material

- 6.2.4.3.3. Market size and forecast, by Component

- 6.3. Europe

- 6.3.1. Key trends and opportunities

- 6.3.2. Market size and forecast, by Material

- 6.3.3. Market size and forecast, by Component

- 6.3.4. Market size and forecast, by country

- 6.3.4.1. Germany

- 6.3.4.1.1. Key market trends, growth factors and opportunities

- 6.3.4.1.2. Market size and forecast, by Material

- 6.3.4.1.3. Market size and forecast, by Component

- 6.3.4.2. UK

- 6.3.4.2.1. Key market trends, growth factors and opportunities

- 6.3.4.2.2. Market size and forecast, by Material

- 6.3.4.2.3. Market size and forecast, by Component

- 6.3.4.3. France

- 6.3.4.3.1. Key market trends, growth factors and opportunities

- 6.3.4.3.2. Market size and forecast, by Material

- 6.3.4.3.3. Market size and forecast, by Component

- 6.3.4.4. Italy

- 6.3.4.4.1. Key market trends, growth factors and opportunities

- 6.3.4.4.2. Market size and forecast, by Material

- 6.3.4.4.3. Market size and forecast, by Component

- 6.3.4.5. Spain

- 6.3.4.5.1. Key market trends, growth factors and opportunities

- 6.3.4.5.2. Market size and forecast, by Material

- 6.3.4.5.3. Market size and forecast, by Component

- 6.3.4.6. Rest of Europe

- 6.3.4.6.1. Key market trends, growth factors and opportunities

- 6.3.4.6.2. Market size and forecast, by Material

- 6.3.4.6.3. Market size and forecast, by Component

- 6.4. Asia-Pacific

- 6.4.1. Key trends and opportunities

- 6.4.2. Market size and forecast, by Material

- 6.4.3. Market size and forecast, by Component

- 6.4.4. Market size and forecast, by country

- 6.4.4.1. China

- 6.4.4.1.1. Key market trends, growth factors and opportunities

- 6.4.4.1.2. Market size and forecast, by Material

- 6.4.4.1.3. Market size and forecast, by Component

- 6.4.4.2. Japan

- 6.4.4.2.1. Key market trends, growth factors and opportunities

- 6.4.4.2.2. Market size and forecast, by Material

- 6.4.4.2.3. Market size and forecast, by Component

- 6.4.4.3. India

- 6.4.4.3.1. Key market trends, growth factors and opportunities

- 6.4.4.3.2. Market size and forecast, by Material

- 6.4.4.3.3. Market size and forecast, by Component

- 6.4.4.4. South Korea

- 6.4.4.4.1. Key market trends, growth factors and opportunities

- 6.4.4.4.2. Market size and forecast, by Material

- 6.4.4.4.3. Market size and forecast, by Component

- 6.4.4.5. Australia

- 6.4.4.5.1. Key market trends, growth factors and opportunities

- 6.4.4.5.2. Market size and forecast, by Material

- 6.4.4.5.3. Market size and forecast, by Component

- 6.4.4.6. Rest of Asia-Pacific

- 6.4.4.6.1. Key market trends, growth factors and opportunities

- 6.4.4.6.2. Market size and forecast, by Material

- 6.4.4.6.3. Market size and forecast, by Component

- 6.5. LAMEA

- 6.5.1. Key trends and opportunities

- 6.5.2. Market size and forecast, by Material

- 6.5.3. Market size and forecast, by Component

- 6.5.4. Market size and forecast, by country

- 6.5.4.1. Brazil

- 6.5.4.1.1. Key market trends, growth factors and opportunities

- 6.5.4.1.2. Market size and forecast, by Material

- 6.5.4.1.3. Market size and forecast, by Component

- 6.5.4.2. Saudi Arabia

- 6.5.4.2.1. Key market trends, growth factors and opportunities

- 6.5.4.2.2. Market size and forecast, by Material

- 6.5.4.2.3. Market size and forecast, by Component

- 6.5.4.3. South Africa

- 6.5.4.3.1. Key market trends, growth factors and opportunities

- 6.5.4.3.2. Market size and forecast, by Material

- 6.5.4.3.3. Market size and forecast, by Component

- 6.5.4.4. Rest of LAMEA

- 6.5.4.4.1. Key market trends, growth factors and opportunities

- 6.5.4.4.2. Market size and forecast, by Material

- 6.5.4.4.3. Market size and forecast, by Component

CHAPTER 7: COMPETITIVE LANDSCAPE

- 7.1. Introduction

- 7.2. Top winning strategies

- 7.3. Product Mapping of Top 10 Player

- 7.4. Competitive Dashboard

- 7.5. Competitive Heatmap

- 7.6. Top player positioning, 2022

CHAPTER 8: COMPANY PROFILES

- 8.1. INN Balance

- 8.1.1. Company overview

- 8.1.2. Key Executives

- 8.1.3. Company snapshot

- 8.1.4. Operating business segments

- 8.1.5. Product portfolio

- 8.2. Cummins, Inc.

- 8.2.1. Company overview

- 8.2.2. Key Executives

- 8.2.3. Company snapshot

- 8.2.4. Operating business segments

- 8.2.5. Product portfolio

- 8.2.6. Business performance

- 8.2.7. Key strategic moves and developments

- 8.3. Hydrogenics Corporation

- 8.3.1. Company overview

- 8.3.2. Key Executives

- 8.3.3. Company snapshot

- 8.3.4. Operating business segments

- 8.3.5. Product portfolio

- 8.4. Ballard Power Systems

- 8.4.1. Company overview

- 8.4.2. Key Executives

- 8.4.3. Company snapshot

- 8.4.4. Operating business segments

- 8.4.5. Product portfolio

- 8.4.6. Business performance

- 8.4.7. Key strategic moves and developments

- 8.5. Bloom Energy

- 8.5.1. Company overview

- 8.5.2. Key Executives

- 8.5.3. Company snapshot

- 8.5.4. Operating business segments

- 8.5.5. Product portfolio

- 8.5.6. Business performance

- 8.5.7. Key strategic moves and developments

- 8.6. SFC Energy AG

- 8.6.1. Company overview

- 8.6.2. Key Executives

- 8.6.3. Company snapshot

- 8.6.4. Operating business segments

- 8.6.5. Product portfolio

- 8.6.6. Business performance

- 8.7. Doosan Fuel Cell Co., Ltd.

- 8.7.1. Company overview

- 8.7.2. Key Executives

- 8.7.3. Company snapshot

- 8.7.4. Operating business segments

- 8.7.5. Product portfolio

- 8.7.6. Business performance

- 8.7.7. Key strategic moves and developments

- 8.8. HORIBA FuelCon GmbH

- 8.8.1. Company overview

- 8.8.2. Key Executives

- 8.8.3. Company snapshot

- 8.8.4. Operating business segments

- 8.8.5. Product portfolio

- 8.9. Elcogen AS

- 8.9.1. Company overview

- 8.9.2. Key Executives

- 8.9.3. Company snapshot

- 8.9.4. Operating business segments

- 8.9.5. Product portfolio

- 8.10. Dana Limited

- 8.10.1. Company overview

- 8.10.2. Key Executives

- 8.10.3. Company snapshot

- 8.10.4. Operating business segments

- 8.10.5. Product portfolio

- 8.10.6. Business performance

- 8.10.7. Key strategic moves and developments