AIコパイロットとIoT向けコード生成:インテリジェントアシスタントによる組込み開発の変革

AI Copilots & Code Generation for the IoT: Transforming Embedded Development with Intelligent Assistants

- 発行

- VDC Strategy

- 発行日

- ページ情報

- 英文 41 Pages; 443 Exhibits

- 納期

- 即日から翌営業日

- 商品コード

- 1802915

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

- 通信/IT関連専門 通信/IT関連専門を専門とする市場調査会社です。

概要

本レポートの内容

AIはソフトウェア開発を根本から変革しました。開発ツールのプロバイダーは、生成AIと自然言語処理の急速な進化を活用し、エンジニアがコーディング作業の大部分を自動化し、プロトタイピングを加速できるよう支援しています。生産性の大幅な向上という利点がある一方で、自動化には本質的にセキュリティと品質のリスクが伴うため、組込みエンジニアリング組織はAI搭載アシスタントを慎重に取り扱う必要があります。カスタムガードレール、ツール統合、ベストプラクティスの指針、モデル改良を通じて、セキュリティ・品質・プロセスの加速を効果的に両立できる商用ソリューションは、この若く急成長中のAIコパイロットおよびコード生成ソリューション市場において、早期にシェアを獲得することができるでしょう。

本レポートは、IoTおよび組込みソフトウェア開発におけるAIコパイロットとコード生成エコシステムの包括的な分析を提供します。現在のエージェント型AIおよびAIコーディングツールの機能と限界、それらの主要IDE、DevOpsパイプライン、組込みツールチェーンとの統合、これらのツールがIoTおよびエッジコンピューティング展開における性能要件や規制要件をどの程度満たせるかを検証しています。

また本レポートには、関連するM&A、LLMエコシステム、ライセンス戦略、エージェント型IDE、AI生成コードに関する懸念、主要ベンダーのプロファイルの分析も含まれています。さらに2024年から2029年までの市場規模および予測を提供し、製品タイプ (汎用ソリューション vs. 専用用途ソリューション)、地域別、産業別、主要ベンダー別のセグメンテーションと解説も行っています。

どのような質問に対応していますか?

- AI強化型コパイロットおよびコード生成ソリューションの需要を牽引している要因は何か?

- AIを活用した開発ソリューションの需要を取り込むために、開発ツールプロバイダーはどのようにポートフォリオを強化できるか?

- この急成長分野の市場成長を牽引するのはどの産業市場か?

- 安全やセキュリティが重要な産業がAIコード生成を大規模に採用するのはいつか?

- エンジニアが軽量アシスタントよりもエージェント型ソリューションを好むのはなぜか?

- 製品イノベーションを推進し、市場に影響を与えている企業はどこか?

本レポートの技術プロバイダー

|

|

|

レポート抜粋

AIの活用でプロジェクト・スケジュールの遵守率が向上

目次

このレポートの内容

エグゼクティブサマリー

- 主な調査結果

調査範囲と調査手法論

- AIの理解

- AIコパイロットとコード生成ツール

世界市場の概要

- エージェントがAIコード生成を変革し、コパイロットに挑戦する

- 戦略的考慮

- LLMの選定とサポートは、市場アドレス可能性に直接影響を与える

- AIツールのライセンス戦略と動向

- JetBrains vs Cursor、AI IDEの台頭

- セキュリティとコード品質の懸念がAI導入を阻む

- 最近の動向

- M&A

地域動向と予測

- 南北アメリカ

- 欧州、中東・アフリカ

- アジア太平洋

垂直市場の動向と予測

- 航空宇宙および防衛

- 自動車

- 通信とネットワーク

- 産業オートメーション

競合情勢

- 既存の組込みソフトウェアソリューションプロバイダーは、AIによる破壊的変化に適応しなければならない

エンドユーザーの洞察

- 組み込みエンジニアリング組織はAIアシスタントの導入に慎重だが、変化は目前に迫っている

- AIの活用はプロジェクトのスケジュール遵守を改善する

- AI生成コードを使用する組み込みエンジニアは、ソフトウェアスタックに対して強い選好を示している

- エンジニアは組織の種類を問わず類似したタスクにAIを活用している

著者について

目次

Inside this Report

AI has fundamentally reshaped software development. Development tool providers have successfully leveraged the rapid evolution of generative AI and natural language processing to help engineers automate large portions of the coding process and accelerate prototyping. Despite massive productivity benefits, automation comes with inherent security and quality risks that force embedded engineering organizations to approach AI-powered assistants with caution. Commercial solutions that can effectively blend security, quality, and process acceleration through custom guardrails, tool integrations, best practices guidance, and model refinement will reap early share in this young but rapidly emerging space for AI copilots and code generation solutions.

This report delivers a comprehensive analysis of the AI copilots and code generation ecosystem as it applies to IoT and embedded software development. It examines the capabilities and limitations of current agentic AI and AI coding tools, their integration with popular IDEs, DevOps pipelines, and embedded toolchains, and the extent to which these tools can meet the performance and regulatory requirements of IoT and edge computing deployments. The report also includes an analysis of relevant mergers and acquisitions, LLM ecosystems, licensing strategies, agentic IDEs, concerns with AI generated code, and profiles of leading vendors. The study includes market sizing and forecasts from 2024 to 2029 with commentary and segmentations by product type (general purpose versus application-specialized solutions), region vertical market, and leading vendors.

What Questions are Addressed?

- What factors are driving demand for AI-enhanced copilots and code generation solutions?

- How can development tool providers strengthen their portfolios to capitalize on demand for AI- powered development solutions?

- Which vertical markets will lead market growth in this burgeoning sector?

- When will safety- and security-critical industries adopt AI code generation at scale?

- Why do engineers favor agentic solutions over lightweight assistants?

- Which companies are driving product innovation and influencing the market?

Who Should Read this Report?

This report was written for those making critical decisions regarding product, market, channel, and competitive strategy and tactics. This report is intended for senior decision-makers who are developing, or are a part of the ecosystem of, AI assistants and code generation tools, including:

|

|

Technology Providers in this Report:

|

|

|

Demand-side Research Overview

VDC launches numerous surveys of the IoT and embedded engineering ecosystem every year using an online survey platform. To support this research, VDC leverages its in-house panel of more than 30,000 individuals from various roles and industries across the world. Our global Voice of the Engineer survey recently captured insights from a total of 600 qualified respondents. This survey was used to inform our insight into key trends, preferences, and predictions within the engineering community.

Executive Summary

AI code generation is emerging as one of the most disruptive forces in IoT software development since the advent of open source. Enterprise/IT organizations eagerly adopted AI-powered coding tools with little hesitation, but demand for code generation capabilities from embedded engineering organizations has lagged behind, resulting in a blossoming opportunity for AI copilot and code generation vendors beginning primarily in 2025. AI copilots accelerate software development, helping engineering organizations cope with the increasing complexity of software codebases and their core role in product-level differentiation. For engineering and product development organizations across industries, AI promises to bridge skill gaps, reduce time to market, and improve developer productivity.

This acceleration in automated coding, however, also increases the need for rigorous quality assurance, compliance checks, and additional security. Currently, there is a large gap in the market for a complete solution that offers safety-critical software testing and analysis alongside standards-compliant code generation. AI-generated code can introduce vulnerabilities, licensing risks, or inefficiencies that are difficult to detect without robust testing and software composition analysis (SCA) in the background. Many of the leading AI development tool vendors do not have partnerships or experience in embedded software development, creating an opportunity for organizations with a long tenure in embedded engineering to partner with AI leaders to safely and securely bring AI-generated code to the IoT for all use cases.

Copilots and code generation will take hold in embedded engineering over the next five years. In the near term, adoption will be strongest in non-safety-critical IoT segments such as communications & networking, consumer electronics, and smart home, where AI-assisted coding can quickly prove ROI without extensive regulatory overhead. As certification bodies and standards organizations formalize guidelines for AI-generated code, safety-critical engineering organizations will adopt copilots more eagerly. To capture a portion of the growing safety-critical market share, vendors must add compliance support, code provenance tracking, and integrate with popular software verification and validation tools.

Key Findings:

- Demand for application- and domain-specialized code generation will accelerate rapidly as embedded engineering organizations embrace AI to add greater amounts of software-driven value to their products.

- As secure, purpose-built AI copilots go to market, the automotive vertical will grow the fastest as OEMs transition toward software-defined vehicle architectures and value-added software features that generate recurring revenue.

- Agentic AI will not only transform code generation but also the complete software development lifecycle as it automates design planning, QA, and project management.

- The Americas is a home market for many of the world's leading AI copilot and code generation solution vendors, contributing to its early market leadership.

- VDC's Voice of the Engineer survey data shows that AI tooling is effectively accelerating project timelines, helping engineers meet and exceed deadlines.

Report Excerpt

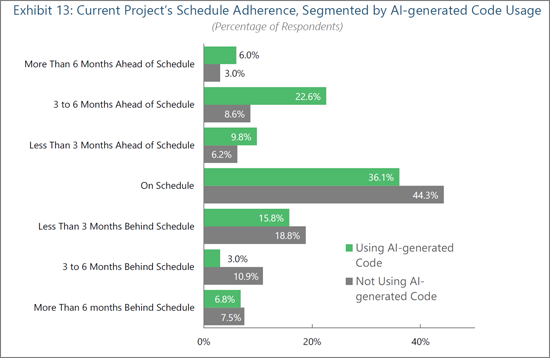

AI Usage Improves Project Schedule Adherence

Organizations leveraging AI for code generation are measurably outperforming their peers in project execution timelines. Engineering organizations employing AI-generated code are significantly more likely to beat expectations, with 38% reportedly ahead of their project schedules (2.1x more likely than organizations not using AI code generation). This discrepancy reflects AI's ability to automate foundational coding tasks, accelerate iteration cycles, and reduce delays caused by manual development bottlenecks.

The sharp difference in three to six month delays (3.0% of AI users versus 10.9% of non-AI users) and overall reduction in delays among AI code users suggest that engineering organizations benefit from AI's ability to preempt errors and improve code reliability earlier in the lifecycle. AI code generation tools that generate boilerplate or repetitive code components allow engineers to focus on architecture, integration, and optimization, which are key elements for fueling product innovation and differentiation in traditional workflows. In edge AI contexts, where deployment environments are heterogeneous and performance tuning is critical, complex task automation (e.g., model integration or hardware abstraction) enables teams to compress development cycles and better align with shifting project requirements. AI-integrated software development strategies free up developers to work proactively on value-creating features. As a result, solution providers should position AI code generation not just as a developer aid, but as a catalyst for predictable, repeatable acceleration, which is especially compelling in embedded markets defined by deployment complexity and constrained engineering resources.

Table of Contents

Inside this Report

Executive Summary

- Key Findings

Report Scope & Methodology

- Understanding AI

- AI Copilots & Code Generation Tools

Global Market Overview

- Agents Will Transform AI Code Generation and Challenge Copilots

- Strategic Considerations

- LLM Selection and Support Directly Impacts Market Addressability

- AI Tool Licensing Strategies and Trends

- JetBrains Versus Cursor and the Rise of AI IDEs

- Security and Code Quality Concerns Deter AI Adoption

- Recent Developments

- Mergers and Acquisitions

Regional Trends & Forecast

- Americas

- Europe, Middle East, and Africa

- Asia-Pacific

Vertical Market Trends & Forecast

- Aerospace & Defense

- Automotive

- Communications & Networking

- Industrial Automation

Competitive Landscape

- Incumbent Embedded Software Solution Providers Must Adapt to AI Disruption

End-User Insights

- Embedded Engineering Organizations are Slow to Adopt AI Assistants, but Change is Imminent

- AI Usage Improves Project Schedule Adherence

- Embedded Engineers Using AI-generated Code Demonstrate Strong Software Stack Preferences

- Engineers Use AI for Similar Tasks Across Organization Types

About the Authors

List of Exhibits:

- Exhibit 1: Global Revenue of Copilots & Code Generation Tools & Related Services Segmented by Tool Type

- Exhibit 2: Percentage of Global Revenue from Copilots & Code Generation Tools & Related Services Segmented by Tool Type

- Exhibit 3: Current Concerns About AI-generated Software Code

- Exhibit 4: Global Revenue of Copilots & Code Generation Tools & Related Services Segmented by Geographic Region

- Exhibit 5: Percentage of Global Revenue from Copilots & Code Generation Tools & Related Services Segmented by Geographic Region

- Exhibit 6: Amount of Trust in AI-generated Software Code Segmented by Vertical Market

- Exhibit 7: Global Revenue of Copilots & Code Generation Tools & Related Services Segmented by Vertical Market

- Exhibit 8: Percentage of Global Revenue from Copilots & Code Generation Tools & Related Services Segmented by Vertical Market

- Exhibit 9: 2024 Percentage of Global Revenue from Copilots & Code Generation Tools & Related Services Segmented by Leading Vendors

- Exhibit 10: 2025 Estimated Market Share of Global Revenue from Copilots & Code Generation Tools & Related Services Segmented by Leading Vendors:

- Exhibit 11: Consideration/Use of AI-generated Software/Code (e.g., Use of Copilot and/or Prompt-based Code Creation)

- Exhibit 12: Expected Changes in Use of AI-generated Software in the Next Three Years

- Exhibit 13: Current Project's Schedule Adherence Segmented by AI-generated Code Usage

- Exhibit 14: Embedded Software Stack Components Required on Current/Most Recent Project Segmented by AI-generated Code Usage

IoT & Embedded Engineering Survey (Partial list):

- Exhibit 1: Primary Role Within Company/Organization

- Exhibit 2: Respondent's Organization's Primary Industry

- Exhibit 3: Total Number of Employees at Respondent's Organization

- Exhibit 4: Primary Region of Residence

- Exhibit 5: Primary Country of Residence

- Exhibit 6: Type of Most Current or Recent Project

- Exhibit 7: Involvement with Engineering of an Embedded/Edge, Enterprise/IT, HPC, AI/ML, or Mobile/System Device or Solution

- Exhibit 8: Type of Purchase by Respondent's Organization

- Exhibit 9: Primary Industry Classification of Project

- Exhibit 10: Type of Aerospace & Defense Application for Most Recent Project

- Exhibit 11: Type of Automotive In-Vehicle Application for Most Recent Project

- Exhibit 12: Type of Communications & Networking Application for Most Recent Project

- Exhibit 13: Type of Consumer Electronics Application for Most Recent Project

- Exhibit 14: Type of Digital Security Application for Most Recent Project

- Exhibit 15: Type of Digital Signage Application for Most Recent Project

- Exhibit 16: Type of Energy and Utilities Application for Most Recent Project

- Exhibit 17: Type of Gaming Application for Most Recent Project

- Exhibit 18: Type of Industrial Automation Application for Most Recent Project

- Exhibit 19: Type of Media & Broadcasting Application for Most Recent Project

- Exhibit 20: Type of Medical Device Application for Most Current Project

- Exhibit 21: Type of Mobile Phone

- Exhibit 22: Type of Office/Business Automation Application for Most Recent Project

- 発行日

- 発行

- VDC Strategy

- ページ情報

- 英文 41 Pages; 443 Exhibits

- 納期

- 即日から翌営業日