|

|

市場調査レポート

商品コード

1364836

バイオLPG市場:現状分析と予測(2023-2030年)Bio-LPG Market: Current Analysis and Forecast (2023-2030) |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| バイオLPG市場:現状分析と予測(2023-2030年) |

|

出版日: 2023年09月30日

発行: UnivDatos Market Insights Pvt Ltd

ページ情報: 英文 151 Pages

納期: 即日から翌営業日

|

- 全表示

- 概要

- 目次

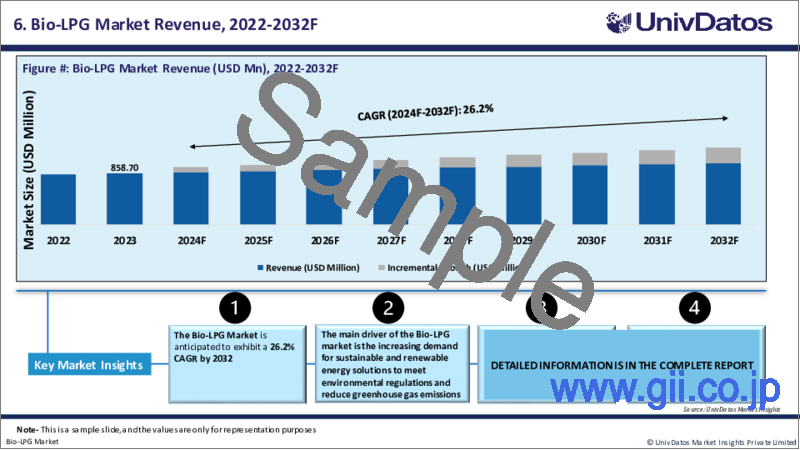

代替バイオ燃料としてのバイオLPGは、現在、輸送、住宅、工業、石油化学部門の脱炭素化のための有望な分野と考えられています。有機残渣や廃棄物からプロパンやブタンを製造することで、CO2排出量を最大90%削減することが可能です。バイオ燃料は従来の燃料に代わるもので、まだ開発の初期段階にあります。しかし、2030年までに世界のLPG市場(潜在的なバイオLPG市場)は最大3億5,000万トンに成長すると予想され、バイオLPGの市場規模は年間140万トンに達すると見込まれています。

バイオLPG市場は予測期間中27.9%という力強いCAGRで成長すると予想されます。これは主に、二酸化炭素排出量を削減し、よりクリーンな燃料を世界的に普及させるという政府の要求によるものです。さらに、気候変動目標の達成に向けた政府の政策や規制と投資が、予測期間中のバイオLPG市場を牽引しています。複数の生産経路が開発されている一方で、現在生産されているバイオLPGのほぼすべては、植物油や廃油を原料とし、水素化処理を経て水素化処理植物油(HVO)や持続可能な航空燃料(SAF)を製造する際の製品別です。このプロセスから得られるバイオLPGの収率は、通常3%から10%です。

バイオLPG製品は、製油所の近代化プロセスの強化やバイオ燃料製造のための新しいプロジェクトの立ち上げにより、欧州市場で主に消費されています。その中で最大のものは、オランダのロッテルダムにあるネステ工場で、年間40,000トンのバイオLPGを生産することができます。欧州市場には、ポーランドのEcobenz触媒バイオエタノールプラント(22.5トン/年)など、他のバイオ精製業者も大量に供給しています。欧州以外では、シンガポールのバイオLPG生産施設と日本の実証プロジェクトが、アジアでのサプライチェーン確立の可能性を提供しています。

バイオLPG市場は、原料に基づき、残渣/廃棄物、石油、その他のセグメントに分けられます。残渣/廃棄物セグメントはバイオLPG市場で大半のシェアを獲得しており、予測期間中に大幅な成長率を示すと予想されます。ある生産経路に必要な原料は、そのビジネス合理性にとって極めて重要であり、プロセスの実行可能性、操業コスト、投資の損益分岐価格に影響を与えます。各プロセスにおける原料の入手可能性、必要な研究開発投資と市場投入までの時間、商業化された技術の効率性が、各原料市場に影響を与える主な要因です。

エンドユーザーに基づくと、バイオLPG市場は住宅用セグメントと商業用セグメントに分けられます。商業用セグメントはバイオLPG市場で大半のシェアを獲得しており、予測期間中に大幅な成長率を示すと予想されます。住宅セグメントはLPG市場で大半のシェアを獲得しているが、バイオLPG市場は初期段階にあり、通常は業務用として利用されています。バイオLPG市場の主な促進要因は、こうした業務用企業に対する政府の優遇措置によるクリーン燃料の普及促進です。バイオLPGの入手可能性が低いことが、バイオLPG市場において住宅用セグメントが過半数を占めていない主な阻害要因となっています。

バイオLPGの市場普及をより理解するために、市場は北米・南米(米国、カナダ、その他北米・南米地域)、欧州(ドイツ、イタリア、英国、オランダ、フランス、その他欧州地域)、アジア太平洋地域(中国、日本、韓国、その他アジア太平洋地域)、世界のその他の地域における世界の存在に基づいて分析されています。欧州はバイオLPG市場で最大のシェアを獲得しており、予測期間中に影響力のあるCAGRを示すことが期待されています。これは主に、ドイツ、イタリア、フランス、英国で多数のバイオLPG運用プロジェクトが行われているためです。さらに、気候変動目標の達成に向けた政府の政策、規制と政策投資が、予測期間中のバイオLPG市場を牽引しています。この市場の主要プレーヤーは、英蘭シェル、伊エニ、仏トタル・エナジー、フィンランド・ネステ、スウェーデン・プリームなどの大手エネルギー企業です。これらの企業の大半は、生産施設を欧州に置いています。欧州市場には、ポーランドのエコベンツ触媒式バイオエタノールプラント(年産2万2,500トン)をはじめとする数多くのバイオ精製工場からの製品も大量に供給されています。欧州におけるバイオLPG市場開拓のインセンティブは、欧州委員会のFit for 55プログラムの要件に従って、最終消費構造における再生可能燃料の目標シェア40%を達成する必要があること、2025年までに欧州排出権取引制度が住宅部門にも拡大される見込みであることです。

市場に参入している主な企業は、英蘭シェル、伊エニ、仏トタル・エナジー、フィンランド・ネステ、スウェーデン・プレム、アバンティガス、レプソル、アービング・オイル、リニューアブル・エナジー・グループ、SHVエナジーなどです。

目次

第1章 市場イントロダクション

- 市場の定義

- 主な目標

- ステークホルダー

- 制限事項

第2章 調査手法または前提

- 調査プロセス

- 調査手法

- 回答者プロファイル

第3章 市場の主要な洞察

第4章 エグゼクティブサマリー

第5章 世界のバイオLPG市場収益 、2020-2030年

第6章 原料別の市場洞察

- 残留物・廃棄物

- 油

- その他

第7章 エンドユーザー別市場洞察

- 住宅用

- 商業用

第8章 地域別の市場洞察

- 北&南米のバイオLPG市場

- 米国

- カナダ

- 北米および南米の残りの地域

- 欧州のバイオLPG市場

- ドイツ

- オランダ

- 英国

- フランス

- イタリア

- その他欧州地域

- アジア太平洋のバイオLPG市場

- 日本

- 中国

- 韓国

- APACのその他諸国

- その他地域のバイオLPG市場

第9章 バイオLPG市場力学

- 市場促進要因

- 市場の課題

- 影響分析

第10章 バイオLPG市場機会

第11章 バイオLPG市場動向

第12章 需要側と供給側の分析

- 需要側分析

- 供給側分析

第13章 バリューチェーン分析

第14章 政府の政策と規制

第15章 競合シナリオ

- 競合情勢

- ポーターのファイブフォース分析

第16章 企業プロファイル

- British-Dutch Shell

- Italian Eni

- French Total Energies

- Finnish Neste

- Swedish Preem

- AvantiGas

- Repsol

- Irving Oil

- Renewable Energy Group, Inc.

- SHV Energy

第17章 免責事項

Bio-LPG as an alternative biofuel is currently considered a promising area for decarbonization of the transport, housing, industry and petrochemical sectors. By producing propane and butane from organic residues and waste materials, it is possible to reduce CO2 emissions by up to 90%. Biofuels are alternatives to conventional fuels and are still in the early stages of development. However, by 2030, the global LPG market (potential Bio-LPG market) is expected to grow to a maximum of 350 million tons, and the Bio-LPG market size is expected to reach 1.4 million tons per year.

The Bio-LPG Market is expected to grow at a strong CAGR of 27.9% during the forecast period. This is mainly owing to the government's requirements to reduce carbon emissions and promote cleaner fuel globally. Moreover, favorable government policies, regulations, and investments in achieving climate change goals are driving the Bio-LPG Market during the forecast period. While multiple production pathways are under development, nearly all bio-LPG produced today is a byproduct of vegetable and waste-based oil feedstocks that undergo hydrotreatment to make hydrotreated vegetable oil (HVO) and sustainable aviation fuel (SAF). The bio-LPG yield from this process is typically between 3 percent and 10 percent.

One of the biggest markets is Europe and most of the volumes of Bio-LPG products are mainly consumed in the European market, a result of the intensification of refinery modernization processes and the launch of new projects for biofuel production. The largest of these is the Neste plant in Rotterdam, the Netherlands, which can produce up to 40,000 tonnes of bio-LPG per year. The European market is also supplied by a number of other bio-refiners in large quantities, such as the Ecobenz catalytic bioethanol plant in Poland (22.5 kt/year). Outside of Europe, a Bio-LPG production facility in Singapore and a demonstration project in Japan offer the potential to establish supply chains in Asia.

Based on feedstock, the Bio-LPG market is divided into residual/waste, oil, and other segments. The Residual/Waste segment acquired a majority share in the Bio-LPG market and is expected to showcase a substantial growth rate during the forecast period. The feedstock required for a given production pathway is critical to its business rationale, impacting process viability, operating costs and the breakeven price of the investments. Feedstock availability for each process, Required research and development investment and time to market, and Efficiency of the commercialized technology are the main factors affecting the market for each feedstock.

Based on End-User, the Bio-LPG market is divided into residential and commercial segments. The commercial segment acquired a majority share in the Bio-LPG market and is expected to showcase a substantial growth rate during the forecast period. Although the residential segment captured a majority share in the LPG market, the Bio-LPG market is in its initial phase and is usually available for commercial use. The major driver for the Bio-LPG market is the promotion of cleaner fuel with government incentives for these commercial enterprises. The low availability of bio-LPG is the major restraint for the residential segment not having a majority share in the Bio-LPG market.

For a better understanding of the market adoption of Bio-LPG, the market is analyzed based on its worldwide presence in countries such as North & South America (U.S.A, Canada, and the Rest of North & South America), Europe (Germany, Italy, United Kingdom, Netherlands, France, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, and Rest of Asia-Pacific) and Rest of World. Europe acquired the largest share in the Bio-LPG market and is expected to witness an influential CAGR in the forecasted period. It is mainly owing to a large number of Bio-LPG operational projects taking place in Germany, Italy, France, and the UK. Moreover, favorable government policies, regulations, and investments in achieving climate change goals are driving the Bio-LPG Market during the forecast period. The key players in this market are leading energy companies, including the British-Dutch Shell, Italian Eni, French Total Energies, Finnish Neste, Swedish Preem. Majority of these companies have their production facilities located in Europe. The European market also receives significant volumes of product from a number of other bio-refineries, including the Ekobenz catalytic bioethanol plant (22.5 thousand tons/year) in Poland. Incentives for the development of the bioLPG market in Europe are the need to achieve the target share of renewable fuels at 40% in the structure of final consumption in accordance with the requirements of the European Commission's Fit for 55 programs; the prospect of extending the European ETS to the housing sector by 2025.

Some of the major players operating in the market are British-Dutch Shell, Italian Eni, French Total Energies, Finnish Neste, Swedish Preem, AvantiGas¸ Repsol, Irving Oil, Renewable Energy Group, Inc., and SHV Energy.

TABLE OF CONTENTS

1 MARKET INTRODUCTION

- 1.1. Market Definitions

- 1.2. Main Objective

- 1.3. Stakeholders

- 1.4. Limitation

2 RESEARCH METHODOLOGY OR ASSUMPTION

- 2.1. Research Process of the Bio-LPG Market

- 2.2. Research Methodology of the Bio-LPG Market

- 2.3. Respondent Profile

3 MARKET KEY INSIGHTS

4 EXECUTIVE SUMMARY

5 GLOBAL BIO-LPG MARKET REVENUE, 2020-2030F

6 MARKET INSIGHTS BY FEEDSTOCK

- 6.1. Residual/Waste

- 6.2. Oil

- 6.3. Others

7 MARKET INSIGHTS BY END-USER

- 7.1. Residential

- 7.2. Commercial

8 MARKET INSIGHTS BY REGION

- 8.1. North & South America Bio-LPG Market

- 8.1.1. U.S.A

- 8.1.2. Canada

- 8.1.3. Rest of North & South America

- 8.2. Europe Bio-LPG Market

- 8.2.1. Germany

- 8.2.2. Netherland

- 8.2.3. United Kingdom

- 8.2.4. France

- 8.2.5. Italy

- 8.2.6. Rest of Europe

- 8.3. Asia-Pacific Bio-LPG Market

- 8.3.1. Japan

- 8.3.2. China

- 8.3.3. South Korea

- 8.3.4. Rest of APAC

- 8.4. Rest of the World Bio-LPG Market

9 BIO-LPG MARKET DYNAMICS

- 9.1. Market Drivers

- 9.2. Market Challenges

- 9.3. Impact Analysis

10 BIO-LPG MARKET OPPORTUNITIES

11 BIO-LPG MARKET TRENDS

12 DEMAND AND SUPPLY-SIDE ANALYSIS

- 12.1. Demand Side Analysis

- 12.2. Supply Side Analysis

13 VALUE CHAIN ANALYSIS

14 GOVERNMENT POLICIES AND REGULATIONS

15 COMPETITIVE SCENARIO

- 15.1. Competitive Landscape

- 15.1.1. Porters Fiver Forces Analysis

16 COMPANY PROFILED

- 16.1. British-Dutch Shell

- 16.2. Italian Eni

- 16.3. French Total Energies

- 16.4. Finnish Neste

- 16.5. Swedish Preem

- 16.6. AvantiGas

- 16.7. Repsol

- 16.8. Irving Oil

- 16.9. Renewable Energy Group, Inc.

- 16.10. SHV Energy