|

|

市場調査レポート

商品コード

1779206

タービン用空気ろ過市場 - 世界の産業規模、シェア、動向、機会、予測:FV別、アプリケーション別、地域別、競合、2020年~2030年Turbine Air Filtration Market - Global Industry Size, Share, Trends, Opportunity, and Forecast, Segmented By Face Velocity, By Application, By Region & Competition, 2020-2030F |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| タービン用空気ろ過市場 - 世界の産業規模、シェア、動向、機会、予測:FV別、アプリケーション別、地域別、競合、2020年~2030年 |

|

出版日: 2025年07月29日

発行: TechSci Research

ページ情報: 英文 188 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

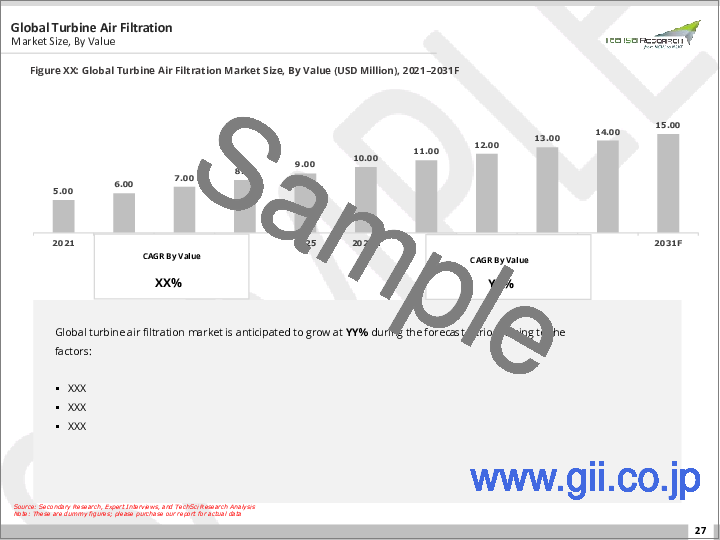

タービン用空気ろ過の世界市場規模は2024年に21億米ドル、2030年には30億米ドルに達し、2030年までのCAGRで6.2%の成長が予測されています。

タービン用空気ろ過の世界市場は、エネルギー需要の高まりと発電システムの運用効率に対するニーズの高まりが原動力となっています。ガスタービンがエネルギー生産、特にコンバインドサイクル発電所や産業施設でますます使用されるようになるにつれ、粉塵、塩分、水分などの汚染物質からタービンを保護するための高性能空気ろ過システムへの需要が高まっています。排出ガスと大気質基準に関する厳しい環境規制は、汚染物質を削減しながら最適な燃焼効率を維持するのに役立つ高度なろ過ソリューションの採用を事業者にさらに促しています。

| 市場概要 | |

|---|---|

| 予測期間 | 2026-2030 |

| 市場規模:2024年 | 21億米ドル |

| 市場規模:2030年 | 30億米ドル |

| CAGR:2025年~2030年 | 6.2% |

| 急成長セグメント | MV |

| 最大市場 | 北米 |

さらに、ナノファイバーフィルター、セルフクリーニングシステム、IoT対応モニタリングなどの技術革新により、フィルターの性能、信頼性、予知保全能力が向上しています。持続可能でクリーンなエネルギー源への世界のシフトも、特にインフラ開発が加速しているアジア太平洋や中東などの地域で、ガスタービンの設置増加に寄与しています。タービンのエアフィルターは、腐食や汚れを最小限に抑えることでメンテナンスコストを削減し、タービンの寿命を向上させる上で重要な役割を果たしています。産業界がダウンタイムの削減とライフサイクルコストの向上に一層注力する中、効率的なエアフィルターの役割は極めて重要なものとなり、現代のエネルギー・エコシステムにおける信頼性、効率性、コンプライアンスの重要な実現者としての地位を確固たるものにしています。

市場促進要因

世界のエネルギー需要の増加とガスタービン設備の拡大

主な市場課題

高いメンテナンスコストと運転休止時間

主な市場動向

スマートモニタリングと予知保全技術の統合

目次

第1章 概要

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 顧客の声

第5章 世界のタービン用空気ろ過市場展望

- 市場規模・予測

- 金額別

- 市場シェア・予測

- FV別(LV、MV、HV)

- アプリケーション別(発電、石油・ガス、その他)

- 地域別(北米、欧州、南米、中東・アフリカ、アジア太平洋)

- 企業別(2024)

- 市場マップ

第6章 北米のタービン用空気ろ過市場展望

- 市場規模・予測

- 市場シェア・予測

- 北米:国別分析

- 米国

- カナダ

- メキシコ

第7章 欧州のタービン用空気ろ過市場展望

- 市場規模・予測

- 市場シェア・予測

- 欧州:国別分析

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

第8章 アジア太平洋地域のタービン用空気ろ過市場展望

- 市場規模・予測

- 市場シェア・予測

- アジア太平洋地域:国別分析

- 中国

- インド

- 日本

- 韓国

- オーストラリア

第9章 中東・アフリカのタービン用空気ろ過市場展望

- 市場規模・予測

- 市場シェア・予測

- 中東・アフリカ:国別分析

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第10章 南米のタービン用空気ろ過市場展望

- 市場規模・予測

- 市場シェア・予測

- 南米:国別分析

- ブラジル

- コロンビア

- アルゼンチン

第11章 市場力学

- 促進要因

- 課題

第12章 市場動向と発展

- 合併と買収

- 製品上市

- 最近の動向

第13章 企業プロファイル

- Camfil AB

- Parker Hannifin Corporation

- Donaldson Company, Inc.

- MANN+HUMMEL GmbH

- Eaton Corporation plc

- Atlas Copco AB

- Freudenberg Filtration Technologies SE & Co. KG

- AAF International(a Daikin Group Company)

第14章 戦略的提言

第15章 調査会社について・免責事項

The Global Turbine Air Filtration Market was valued at USD 2.1 billion in 2024 and is expected to reach USD 3.0 billion by 2030 with a CAGR of 6.2% through 2030. The global turbine air filtration market is driven by rising energy demands and the growing need for operational efficiency in power generation systems. As gas turbines are increasingly used in energy production, especially in combined cycle plants and industrial facilities, the demand for high-performance air filtration systems has intensified to protect turbines from contaminants such as dust, salt, and moisture. Stringent environmental regulations on emissions and air quality standards are further pushing operators to adopt advanced filtration solutions that help maintain optimal combustion efficiency while reducing pollutants.

| Market Overview | |

|---|---|

| Forecast Period | 2026-2030 |

| Market Size 2024 | USD 2.1 Billion |

| Market Size 2030 | USD 3.0 Billion |

| CAGR 2025-2030 | 6.2% |

| Fastest Growing Segment | Medium Velocity |

| Largest Market | North America |

Additionally, technological innovations such as nanofiber filters, self-cleaning systems, and IoT-enabled monitoring are enhancing filter performance, reliability, and predictive maintenance capabilities. The global shift toward sustainable and cleaner energy sources is also contributing to increased installations of gas turbines, particularly in regions like Asia-Pacific and the Middle East, where infrastructure development is accelerating. Turbine air filters play a critical role in reducing maintenance costs and improving turbine longevity by minimizing corrosion and fouling. As industries focus more on reducing downtime and enhancing lifecycle costs, the role of efficient air filtration becomes pivotal, solidifying its position as a key enabler of reliability, efficiency, and compliance in the modern energy ecosystem.

Key Market Drivers

Rising Global Energy Demand and the Expansion of Gas Turbine Installations

One of the primary drivers of the turbine air filtration market is the rising global demand for energy and the subsequent expansion of gas turbine installations across power generation and industrial sectors. As global economies continue to grow-particularly in emerging markets like India, China, and Southeast Asia-the demand for stable, scalable, and efficient electricity sources has surged. Gas turbines, known for their high efficiency, quick ramp-up capabilities, and compatibility with both conventional and renewable energy systems, have become central to modern power infrastructure. However, to operate at peak efficiency and reliability, turbines require clean air intake systems, which is where advanced air filtration becomes critical.

Turbine air filters prevent airborne contaminants such as dust, sand, salt, moisture, and industrial pollutants from entering the turbine system. These particles, if unfiltered, can cause erosion, fouling, and corrosion of turbine blades-leading to reduced efficiency, unplanned downtime, and increased maintenance costs. In regions with challenging environmental conditions-such as deserts (Middle East) or coastal areas (Southeast Asia)-the reliance on high-performance filtration solutions is even more pronounced.

Furthermore, the growth of distributed energy systems and cogeneration plants (CHP) that use gas turbines in industrial zones is adding to the demand. As more industries seek reliable, on-site power generation solutions, the requirement for efficient turbine air filtration grows. In addition, gas turbines are increasingly favored in peaking power plants due to their fast response time-requiring robust air filtration to manage sudden operational changes. As countries invest in gas-based infrastructure to reduce coal dependency and meet clean energy targets, the turbine air filtration market is expected to see steady growth. The performance and longevity of turbines heavily depend on effective filtration, making it an indispensable component of energy infrastructure development. Global energy consumption is projected to increase by around 25% over the next decade. Renewable energy sources are expected to account for more than 30% of total energy demand growth. Energy demand in developing regions is forecasted to grow at an average annual rate of approximately 3%. Industrial and transportation sectors contribute to nearly 60% of the rise in global energy use. Energy efficiency improvements are estimated to offset about 10% of the overall increase in demand.

Key Market Challenges

High Maintenance Costs and Operational Downtime

One of the significant challenges in the turbine air filtration market is the high maintenance cost and the operational downtime associated with the installation, monitoring, and replacement of filtration systems. While air filtration is crucial for protecting turbines from contaminants and ensuring operational efficiency, the filters themselves require regular maintenance, cleaning, or replacement-especially in harsh environments such as deserts, coastal areas, or industrial zones. These areas often have high particulate matter or salt-laden air, which clogs filters faster, necessitating more frequent servicing.

Filter maintenance involves scheduled shutdowns of turbines, which can lead to revenue losses, especially in continuous-process industries or power generation facilities operating on tight availability margins. Additionally, improper maintenance practices-such as delayed filter replacement or incorrect installation-can lead to reduced filtration efficiency, resulting in blade erosion, fouling, and long-term damage to turbine components.

Moreover, operators may face logistical challenges in remote or offshore locations where transporting filters and deploying skilled personnel is both costly and time-consuming. The expense is compounded for large facilities that operate multiple turbines, each requiring tailored filter solutions.

Advanced filter technologies such as HEPA-grade or self-cleaning filters offer improved performance but come at a higher upfront cost, which may deter cost-sensitive operators, especially in developing regions. Furthermore, inadequate predictive maintenance systems can make it difficult to optimize filter lifecycle, leading to either premature replacements or prolonged use of degraded filters-both scenarios increasing operational costs.

Key Market Trends

Integration of Smart Monitoring and Predictive Maintenance Technologies

A prominent trend reshaping the global turbine air filtration market is the adoption of smart monitoring systems and predictive maintenance technologies. Traditional turbine air filters require manual inspection and scheduled replacements, often leading to inefficiencies such as premature filter changes or excessive wear before detection. However, with the rise of the Industrial Internet of Things (IIoT), filter systems are now being equipped with sensors that monitor pressure drops, airflow rates, temperature, and particle accumulation in real time.

These intelligent systems allow operators to track the performance of air filters remotely and predict optimal replacement intervals based on actual operating conditions rather than fixed schedules. This shift enhances turbine efficiency, reduces unexpected downtime, and minimizes maintenance costs-especially crucial in mission-critical applications like power plants, offshore rigs, and aviation. Predictive analytics also aids in inventory management by preventing overstocking or under-provisioning of spare filters.

Furthermore, cloud-based dashboards and mobile alerts enable facility managers to make data-driven decisions and proactively address filtration issues before they escalate. Advanced digital twins and AI-based platforms are also being explored to simulate turbine-environment interactions, helping operators choose the most suitable filter types for specific geographies.

This trend is especially gaining traction in developed markets like North America and Europe, where operators are focused on operational excellence and regulatory compliance. However, adoption is also growing in emerging markets as infrastructure modernizes. The integration of smart monitoring not only increases the lifespan of both filters and turbines but also supports sustainability goals by optimizing resource usage. As digital transformation accelerates across industries, smart turbine air filtration systems are expected to become the new standard, marking a significant evolution in asset management and maintenance practices.

Key Market Players

- Camfil AB

- Parker Hannifin Corporation

- Donaldson Company, Inc.

- MANN+HUMMEL GmbH

- Eaton Corporation plc

- Atlas Copco AB

- Freudenberg Filtration Technologies SE & Co. KG

- AAF International (a Daikin Group Company)

Report Scope:

In this report, the Global Turbine Air Filtration Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

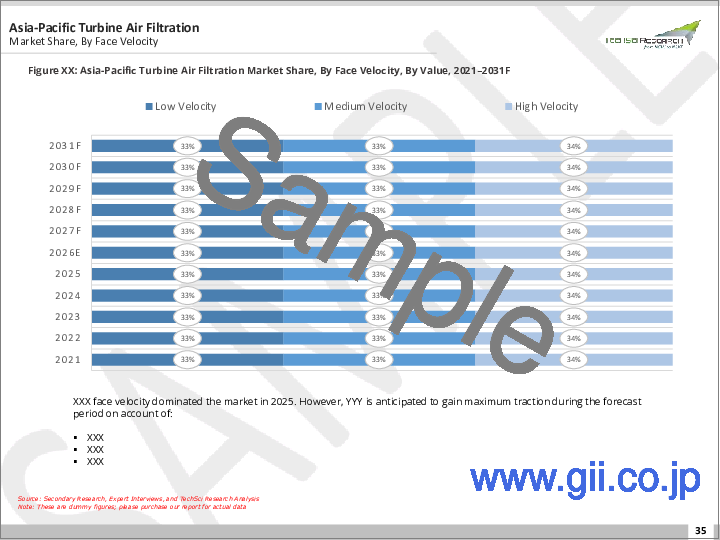

Turbine Air Filtration Market, By Face Velocity:

- Low Velocity

- Medium Velocity

- High Velocity

Turbine Air Filtration Market, By Application:

- Power Generation

- Oil & Gas

- Others

Turbine Air Filtration Market, By Region:

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- South America

- Brazil

- Colombia

- Argentina

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Global Turbine Air Filtration Market.

Available Customizations:

Global Turbine Air Filtration Market report with the given market data, Tech Sci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Table of Contents

1. Product Overview

- 1.1. Market Definition

- 1.2. Scope of the Market

- 1.2.1. Markets Covered

- 1.2.2. Years Considered for Study

- 1.2.3. Key Market Segmentations

2. Research Methodology

- 2.1. Objective of the Study

- 2.2. Baseline Methodology

- 2.3. Key Industry Partners

- 2.4. Major Association and Secondary Sources

- 2.5. Forecasting Methodology

- 2.6. Data Triangulation & Validation

- 2.7. Assumptions and Limitations

3. Executive Summary

- 3.1. Overview of the Market

- 3.2. Overview of Key Market Segmentations

- 3.3. Overview of Key Market Players

- 3.4. Overview of Key Regions/Countries

- 3.5. Overview of Market Drivers, Challenges, and Trends

4. Voice of Customer

5. Global Turbine Air Filtration Market Outlook

- 5.1. Market Size & Forecast

- 5.1.1. By Value

- 5.2. Market Share & Forecast

- 5.2.1. By Face Velocity (Low Velocity, Medium Velocity, High Velocity)

- 5.2.2. By Application (Power Generation, Oil & Gas, Others)

- 5.2.3. By Region (North America, Europe, South America, Middle East & Africa, Asia Pacific)

- 5.3. By Company (2024)

- 5.4. Market Map

6. North America Turbine Air Filtration Market Outlook

- 6.1. Market Size & Forecast

- 6.1.1. By Value

- 6.2. Market Share & Forecast

- 6.2.1. By Face Velocity

- 6.2.2. By Application

- 6.2.3. By Country

- 6.3. North America: Country Analysis

- 6.3.1. United States Turbine Air Filtration Market Outlook

- 6.3.1.1. Market Size & Forecast

- 6.3.1.1.1. By Value

- 6.3.1.2. Market Share & Forecast

- 6.3.1.2.1. By Face Velocity

- 6.3.1.2.2. By Application

- 6.3.1.1. Market Size & Forecast

- 6.3.2. Canada Turbine Air Filtration Market Outlook

- 6.3.2.1. Market Size & Forecast

- 6.3.2.1.1. By Value

- 6.3.2.2. Market Share & Forecast

- 6.3.2.2.1. By Face Velocity

- 6.3.2.2.2. By Application

- 6.3.2.1. Market Size & Forecast

- 6.3.3. Mexico Turbine Air Filtration Market Outlook

- 6.3.3.1. Market Size & Forecast

- 6.3.3.1.1. By Value

- 6.3.3.2. Market Share & Forecast

- 6.3.3.2.1. By Face Velocity

- 6.3.3.2.2. By Application

- 6.3.3.1. Market Size & Forecast

- 6.3.1. United States Turbine Air Filtration Market Outlook

7. Europe Turbine Air Filtration Market Outlook

- 7.1. Market Size & Forecast

- 7.1.1. By Value

- 7.2. Market Share & Forecast

- 7.2.1. By Face Velocity

- 7.2.2. By Application

- 7.2.3. By Country

- 7.3. Europe: Country Analysis

- 7.3.1. Germany Turbine Air Filtration Market Outlook

- 7.3.1.1. Market Size & Forecast

- 7.3.1.1.1. By Value

- 7.3.1.2. Market Share & Forecast

- 7.3.1.2.1. By Face Velocity

- 7.3.1.2.2. By Application

- 7.3.1.1. Market Size & Forecast

- 7.3.2. France Turbine Air Filtration Market Outlook

- 7.3.2.1. Market Size & Forecast

- 7.3.2.1.1. By Value

- 7.3.2.2. Market Share & Forecast

- 7.3.2.2.1. By Face Velocity

- 7.3.2.2.2. By Application

- 7.3.2.1. Market Size & Forecast

- 7.3.3. United Kingdom Turbine Air Filtration Market Outlook

- 7.3.3.1. Market Size & Forecast

- 7.3.3.1.1. By Value

- 7.3.3.2. Market Share & Forecast

- 7.3.3.2.1. By Face Velocity

- 7.3.3.2.2. By Application

- 7.3.3.1. Market Size & Forecast

- 7.3.4. Italy Turbine Air Filtration Market Outlook

- 7.3.4.1. Market Size & Forecast

- 7.3.4.1.1. By Value

- 7.3.4.2. Market Share & Forecast

- 7.3.4.2.1. By Face Velocity

- 7.3.4.2.2. By Application

- 7.3.4.1. Market Size & Forecast

- 7.3.5. Spain Turbine Air Filtration Market Outlook

- 7.3.5.1. Market Size & Forecast

- 7.3.5.1.1. By Value

- 7.3.5.2. Market Share & Forecast

- 7.3.5.2.1. By Face Velocity

- 7.3.5.2.2. By Application

- 7.3.5.1. Market Size & Forecast

- 7.3.1. Germany Turbine Air Filtration Market Outlook

8. Asia Pacific Turbine Air Filtration Market Outlook

- 8.1. Market Size & Forecast

- 8.1.1. By Value

- 8.2. Market Share & Forecast

- 8.2.1. By Face Velocity

- 8.2.2. By Application

- 8.2.3. By Country

- 8.3. Asia Pacific: Country Analysis

- 8.3.1. China Turbine Air Filtration Market Outlook

- 8.3.1.1. Market Size & Forecast

- 8.3.1.1.1. By Value

- 8.3.1.2. Market Share & Forecast

- 8.3.1.2.1. By Face Velocity

- 8.3.1.2.2. By Application

- 8.3.1.1. Market Size & Forecast

- 8.3.2. India Turbine Air Filtration Market Outlook

- 8.3.2.1. Market Size & Forecast

- 8.3.2.1.1. By Value

- 8.3.2.2. Market Share & Forecast

- 8.3.2.2.1. By Face Velocity

- 8.3.2.2.2. By Application

- 8.3.2.1. Market Size & Forecast

- 8.3.3. Japan Turbine Air Filtration Market Outlook

- 8.3.3.1. Market Size & Forecast

- 8.3.3.1.1. By Value

- 8.3.3.2. Market Share & Forecast

- 8.3.3.2.1. By Face Velocity

- 8.3.3.2.2. By Application

- 8.3.3.1. Market Size & Forecast

- 8.3.4. South Korea Turbine Air Filtration Market Outlook

- 8.3.4.1. Market Size & Forecast

- 8.3.4.1.1. By Value

- 8.3.4.2. Market Share & Forecast

- 8.3.4.2.1. By Face Velocity

- 8.3.4.2.2. By Application

- 8.3.4.1. Market Size & Forecast

- 8.3.5. Australia Turbine Air Filtration Market Outlook

- 8.3.5.1. Market Size & Forecast

- 8.3.5.1.1. By Value

- 8.3.5.2. Market Share & Forecast

- 8.3.5.2.1. By Face Velocity

- 8.3.5.2.2. By Application

- 8.3.5.1. Market Size & Forecast

- 8.3.1. China Turbine Air Filtration Market Outlook

9. Middle East & Africa Turbine Air Filtration Market Outlook

- 9.1. Market Size & Forecast

- 9.1.1. By Value

- 9.2. Market Share & Forecast

- 9.2.1. By Face Velocity

- 9.2.2. By Application

- 9.2.3. By Country

- 9.3. Middle East & Africa: Country Analysis

- 9.3.1. Saudi Arabia Turbine Air Filtration Market Outlook

- 9.3.1.1. Market Size & Forecast

- 9.3.1.1.1. By Value

- 9.3.1.2. Market Share & Forecast

- 9.3.1.2.1. By Face Velocity

- 9.3.1.2.2. By Application

- 9.3.1.1. Market Size & Forecast

- 9.3.2. UAE Turbine Air Filtration Market Outlook

- 9.3.2.1. Market Size & Forecast

- 9.3.2.1.1. By Value

- 9.3.2.2. Market Share & Forecast

- 9.3.2.2.1. By Face Velocity

- 9.3.2.2.2. By Application

- 9.3.2.1. Market Size & Forecast

- 9.3.3. South Africa Turbine Air Filtration Market Outlook

- 9.3.3.1. Market Size & Forecast

- 9.3.3.1.1. By Value

- 9.3.3.2. Market Share & Forecast

- 9.3.3.2.1. By Face Velocity

- 9.3.3.2.2. By Application

- 9.3.3.1. Market Size & Forecast

- 9.3.1. Saudi Arabia Turbine Air Filtration Market Outlook

10. South America Turbine Air Filtration Market Outlook

- 10.1. Market Size & Forecast

- 10.1.1. By Value

- 10.2. Market Share & Forecast

- 10.2.1. By Face Velocity

- 10.2.2. By Application

- 10.2.3. By Country

- 10.3. South America: Country Analysis

- 10.3.1. Brazil Turbine Air Filtration Market Outlook

- 10.3.1.1. Market Size & Forecast

- 10.3.1.1.1. By Value

- 10.3.1.2. Market Share & Forecast

- 10.3.1.2.1. By Face Velocity

- 10.3.1.2.2. By Application

- 10.3.1.1. Market Size & Forecast

- 10.3.2. Colombia Turbine Air Filtration Market Outlook

- 10.3.2.1. Market Size & Forecast

- 10.3.2.1.1. By Value

- 10.3.2.2. Market Share & Forecast

- 10.3.2.2.1. By Face Velocity

- 10.3.2.2.2. By Application

- 10.3.2.1. Market Size & Forecast

- 10.3.3. Argentina Turbine Air Filtration Market Outlook

- 10.3.3.1. Market Size & Forecast

- 10.3.3.1.1. By Value

- 10.3.3.2. Market Share & Forecast

- 10.3.3.2.1. By Face Velocity

- 10.3.3.2.2. By Application

- 10.3.3.1. Market Size & Forecast

- 10.3.1. Brazil Turbine Air Filtration Market Outlook

11. Market Dynamics

- 11.1. Drivers

- 11.2. Challenges

12. Market Trends and Developments

- 12.1. Merger & Acquisition (If Any)

- 12.2. Product Launches (If Any)

- 12.3. Recent Developments

13. Company Profiles

- 13.1. Camfil AB

- 13.1.1. Business Overview

- 13.1.2. Key Revenue and Financials

- 13.1.3. Recent Developments

- 13.1.4. Key Personnel

- 13.1.5. Key Product/Services Offered

- 13.2. Parker Hannifin Corporation

- 13.3. Donaldson Company, Inc.

- 13.4. MANN+HUMMEL GmbH

- 13.5. Eaton Corporation plc

- 13.6. Atlas Copco AB

- 13.7. Freudenberg Filtration Technologies SE & Co. KG

- 13.8. AAF International (a Daikin Group Company)