|

|

市場調査レポート

商品コード

1572733

レーザーセンサー市場- 世界の産業規模、シェア、動向、機会、予測、タイプ別、コンポーネント別、用途別、産業別、地域別、競合別、2019~2029年Laser Sensors Market - Global Industry Size, Share, Trends, Opportunity, and Forecast, Segmented By Type, By Component, By Application, By Industry, By Region & Competition, 2019-2029F |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| レーザーセンサー市場- 世界の産業規模、シェア、動向、機会、予測、タイプ別、コンポーネント別、用途別、産業別、地域別、競合別、2019~2029年 |

|

出版日: 2024年10月18日

発行: TechSci Research

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

レーザーセンサーの世界市場規模は2023年に7億4,900万米ドルとなり、2029年のCAGRは9.19%で堅調な成長が予測されています。

レーザーセンサー市場は、より広範なセンサー技術産業の中で、ダイナミックで急速に発展しているセグメントを指します。レーザーベースセンサの生産、販売、応用を包含しており、レーザー技術を広範な測定や検出の目的に利用するデバイスです。これらのセンサは、レーザービームを照射し、様々な材料や物体からの反射や応答を分析するように設計されており、高精度で非接触の測定を可能にします。

| 市場概要 | |

|---|---|

| 予測期間 | 2025~2029年 |

| 市場規模:2023年 | 7億4,900万米ドル |

| 市場規模:2029年 | 12億8,077万米ドル |

| CAGR:2024~2029年 | 9.19% |

| 急成長セグメント | 民生用電子機器 |

| 最大市場 | 北米 |

レーザーセンサーは、製造、産業オートメーション、自動車、航空宇宙、医療、コンシューマー・エレクトロニクスなど、さまざまな産業で多様な用途に使用されています。精密測定、物体検出、アライメント、近接センシング、速度測定などのタスクに利用されています。これらのセンサは、卓越した精度、信頼性、課題環境での機能といった利点を備えています。

レーザーセンサー市場は、様々なセグメントにおける精度の向上、安全性の改善、自動化の強化の必要性により、絶え間ない技術の進歩によって特徴付けられます。政府の規制、環境基準、革新的なアプリケーションに対する市場の需要といった要因の影響を受けます。その結果、この業界は競争が激しく、ダイナミックな業界となっており、各企業は常に最先端のレーザーセンサ技術を開発し、幅広い業界の顧客の進化するニーズに応えようと努力しています。

市場促進要因

産業オートメーションとインダストリー4.0

自動車産業の進歩

医療とライフサイエンス用途

政府の政策が市場を促進する可能性が高い

研究開発への資金援助

環境規制とエネルギー効率基準

貿易と関税

主要市場課題

初期コストの高さと価格への敏感さ

急速な技術進歩と市場の飽和状態

主要市場動向

レーザーセンサーとIoTとインダストリー4.0技術の統合

目次

第1章 概要

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 顧客の声

第5章 世界のレーザーセンサー市場展望

- 市場規模・予測

- 金額別

- 市場シェア・予測

- タイプ別(コンパクト、超コンパクト)

- コンポーネント別(ハードウェア、ソフトウェア、サービス)

- 用途別(セキュリティと監視、動作と誘導、品質管理、距離測定、製造工場管理、プロセス監視、その他)

- 業界別(民生用電子機器、飲食品、自動車、化学、航空宇宙・防衛、医療、その他)

- 地域別

- 企業別(2023年)

- 市場マップ

第6章 北米のレーザーセンサー市場展望

- 市場規模・予測

- 金額別

- 市場シェア・予測

- タイプ別

- コンポーネント別

- 用途別

- 業界別

- 国別

- 北米:国別分析

- 米国

- カナダ

- メキシコ

第7章 欧州のレーザーセンサー市場展望

- 市場規模・予測

- 金額別

- 市場シェア・予測

- タイプ別

- コンポーネント別

- 用途別

- 業界別

- 国別

- 欧州:国別分析

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

第8章 アジア太平洋のレーザーセンサー市場展望

- 市場規模・予測

- 金額別

- 市場シェア・予測

- タイプ別

- コンポーネント別

- 用途別

- 業界別

- 国別

- アジア太平洋:国別分析

- 中国

- インド

- 日本

- 韓国

- オーストラリア

第9章 南米のレーザーセンサー市場展望

- 市場規模・予測

- 金額別

- 市場シェア・予測

- タイプ別

- コンポーネント別

- 用途別

- 業界別

- 国別

- 南米:国別分析

- ブラジル

- アルゼンチン

- コロンビア

第10章 中東・アフリカのレーザーセンサー市場展望

- 市場規模・予測

- 金額別

- 市場シェア・予測

- タイプ別

- コンポーネント別

- 用途別

- 業界別

- 国別

- 中東・アフリカ:国別分析

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- クウェート

- トルコ

第11章 市場力学

- 促進要因

- 課題

第12章 市場動向と発展

第13章 企業プロファイル

- SICK AG

- Rockwell Automation Inc.

- Honeywell International Inc.

- OMRON Corporation

- Panasonic Corporation

- Keyence Corporation

- Baumer Holding AG

- Pepperl+Fuchs SE

- TE Connectivity Ltd.

- Leuze electronic GmbH+Co. KG

第14章 戦略的提言

第15章 調査会社について・免責事項

Global Laser Sensors Market was valued at USD 749 million in 2023 and is anticipated to project robust growth in the forecast period with a CAGR of 9.19% through 2029. The Laser Sensors market, refers to a dynamic and rapidly evolving sector within the broader sensor technology industry. It encompasses the production, sale, and application of laser-based sensors, devices that utilize laser technology for a wide range of measurement and detection purposes. These sensors are designed to emit laser beams and analyze the reflections or responses from various materials or objects, allowing for highly accurate and non-contact measurements.

| Market Overview | |

|---|---|

| Forecast Period | 2025-2029 |

| Market Size 2023 | USD 749 Million |

| Market Size 2029 | USD 1280.77 Million |

| CAGR 2024-2029 | 9.19% |

| Fastest Growing Segment | Consumer Electronics |

| Largest Market | North America |

Laser sensors find diverse applications across multiple industries, including manufacturing, industrial automation, automotive, aerospace, healthcare, consumer electronics, and more. They are utilized for tasks such as precision measurement, object detection, alignment, proximity sensing, and speed measurement. These sensors offer advantages like exceptional precision, reliability, and the ability to function in challenging environments.

The Laser Sensors market is characterized by constant technological advancements, driven by the need for increased accuracy, improved safety, and enhanced automation in various sectors. It is influenced by factors such as government regulations, environmental standards, and market demand for innovative applications. As a result, it is a competitive and dynamic industry where companies continually strive to develop cutting-edge laser sensor technologies to meet the evolving needs of their clients across a wide spectrum of industries.

Key Market Drivers

Industrial Automation and Industry 4.0

The global Laser Sensors market is experiencing robust growth due to the expanding adoption of industrial automation and the Industry 4.0 revolution. In a world where efficiency, productivity, and safety are paramount, laser sensors are proving indispensable. They are instrumental for precision measurements, object detection, and positioning in manufacturing and logistics. As Industry 4.0 continues to reshape industries with its focus on data-driven decision-making, laser sensors are in high demand. These sensors provide high precision, non-contact measurements, making them a critical component in the smart factories of today and tomorrow.

Automotive Industry Advancements

The automotive industry is another major driver of the global Laser Sensors market. Laser sensors are deployed extensively in automotive manufacturing for quality control, vehicle alignment, and safety applications. As electric vehicles and autonomous driving technology take center stage, laser sensors play a pivotal role in providing precise data, ensuring the safety and reliability of these vehicles. With the constant evolution of the automotive sector and its increasing market reach, the demand for laser sensors is set to soar.

Healthcare and Life Sciences Applications

Laser sensors have found a burgeoning market in healthcare and life sciences, propelling the overall growth of this technology. These sensors play a pivotal role in various healthcare applications, from medical devices and diagnostics to scientific research. They are integral for tasks such as measuring blood glucose levels, conducting DNA sequencing, and monitoring vital signs. The growing focus on precision medicine and technological advances in the healthcare sector is driving the demand for laser sensors in these applications.

Government Policies are Likely to Propel the Market

Research and Development Funding

Government policies that promote and fund research and development (R&D) are critical for the growth of the global Laser Sensors market. R&D drives innovation and technological advancements in laser sensor technology, leading to improved performance, increased reliability, and cost-effectiveness. Governments around the world are recognizing the importance of supporting R&D in emerging technologies like laser sensors. They offer grants, tax incentives, and funding programs to universities, research institutions, and private companies involved in laser sensor research and development. These policies stimulate innovation and foster collaboration, ultimately driving the market's expansion.

Environmental Regulations and Energy Efficiency Standards

Government policies aimed at regulating environmental and energy efficiency standards impact the Laser Sensors market significantly. With increasing concerns about environmental sustainability and energy conservation, governments worldwide are enacting policies that mandate the use of energy-efficient technologies, including laser sensors. These regulations often set standards for power consumption, emission reduction, and sustainability criteria. Manufacturers and users of laser sensors must adhere to these standards, encouraging the development and adoption of eco-friendly and efficient sensor technologies.

Trade and Tariffs

Trade policies and tariffs can have both positive and negative impacts on the global Laser Sensors market. Governments may impose tariffs or trade restrictions on sensor components or finished products, affecting the cost of production and market access. On the other hand, policies that promote free trade and reduce trade barriers can benefit the market by increasing market access, reducing production costs, and fostering international collaboration. These policies influence the competitiveness and pricing dynamics of laser sensor manufacturers.

Key Market Challenges

High Initial Costs and Price Sensitivity

One of the foremost challenges in the global Laser Sensors market is the relatively high initial cost of laser sensor technology. While laser sensors offer numerous advantages such as high precision, accuracy, and non-contact operation, their advanced technology and components can be expensive to manufacture. These costs are driven by factors like the quality of materials, the precision of manufacturing processes, and the incorporation of cutting-edge technology.

The high initial costs can present a barrier to entry for smaller businesses and startups looking to enter the market. For manufacturers, it can be a challenge to offer laser sensors at competitive prices while maintaining profitability. This issue becomes even more prominent when considering price sensitivity, as many industries and consumers are cost-conscious and seek budget-friendly solutions.

As a result, companies operating in the Laser Sensors market must strike a delicate balance between cost and quality. Reducing costs without sacrificing quality is an ongoing challenge that often requires innovative manufacturing techniques, supply chain optimizations, and economies of scale. Additionally, intense market competition can exert further pressure on manufacturers to lower prices, making profitability a constant challenge in the industry.

The industry has witnessed gradual cost reductions as technology advances, production processes become more efficient, and economies of scale are realized. Government policies that support research and development can also help mitigate these challenges by fostering innovation and reducing manufacturing costs.

Rapid Technological Advancements and Market Saturation

The rapid pace of technological advancements and market saturation poses a significant challenge to the global Laser Sensors market. The technology landscape is dynamic, with continuous innovation leading to the development of new, more advanced laser sensor products. This not only creates a constant need for companies to invest in research and development to remain competitive but also makes it challenging to predict the future demands and preferences of the market.

Market saturation has become a concern in several industries where laser sensors are already widely adopted. For example, in automotive manufacturing and industrial automation, laser sensors have become standard equipment for various applications, and the markets may reach a point of saturation. In such scenarios, companies must look for new applications or expand into emerging markets to sustain growth.

Another facet of this challenge is the need for laser sensor manufacturers to stay ahead of the technology curve. Obsolescence can occur rapidly in technology-based industries, and companies must continuously innovate to remain relevant. As technology evolves, businesses must also deal with product life cycles, as older models are replaced by newer, more advanced alternatives.

To address these challenges, companies in the Laser Sensors market must maintain a strong focus on research and development to stay at the cutting edge of technology. They need to diversify their product offerings and explore new applications, such as the adoption of laser sensors in consumer electronics, environmental monitoring, or emerging industries like autonomous vehicles. Building strong partnerships and collaborations with research institutions and industry associations can also help companies navigate these challenges effectively.

Key Market Trends

Integration of Laser Sensors with IoT and Industry 4.0 Technologies

The Global Laser Sensors Market is experiencing a notable trend of integration with Internet of Things (IoT) and Industry 4.0 technologies. As industries increasingly adopt smart manufacturing and automation, laser sensors are becoming integral to enhancing operational efficiency, precision, and productivity. This trend is driven by the need for real-time data, improved connectivity, and advanced analytics in manufacturing and industrial processes.

The integration of laser sensors with IoT and Industry 4.0 technologies enables seamless data collection and analysis. Laser sensors are used to measure various parameters such as distance, displacement, position, and level with high accuracy. When connected to IoT networks, these sensors can transmit data in real-time to centralized systems for monitoring and analysis. This connectivity allows for better decision-making and more efficient management of industrial processes.

In smart manufacturing environments, laser sensors are essential for automation and robotics. They provide precise measurements and feedback required for tasks such as object detection, alignment, and quality control. For example, in automotive manufacturing, laser sensors are used to ensure the correct placement of components and to inspect the quality of welds. The data collected by these sensors can be analyzed to optimize production lines, reduce defects, and improve overall product quality.

The integration of laser sensors with IoT and Industry 4.0 technologies offers several benefits that are driving their adoption. These benefits include enhanced accuracy, real-time monitoring, predictive maintenance, and increased productivity. By providing precise measurements and enabling real-time data transmission, laser sensors help industries achieve higher levels of automation and efficiency.

Predictive maintenance is another significant advantage. By continuously monitoring equipment and processes, laser sensors can detect anomalies and predict potential failures before they occur. This proactive approach minimizes downtime, reduces maintenance costs, and extends the lifespan of equipment. For instance, in the aerospace industry, laser sensors are used to monitor the condition of critical components, ensuring timely maintenance and avoiding costly failures.

The integration with IoT and Industry 4.0 technologies supports the development of smart factories. These factories leverage advanced analytics and machine learning algorithms to optimize operations and make data-driven decisions. Laser sensors play a crucial role in collecting the necessary data to support these advanced analytics, contributing to the overall efficiency and competitiveness of the manufacturing sector.

Segmental Insights

Component Insights

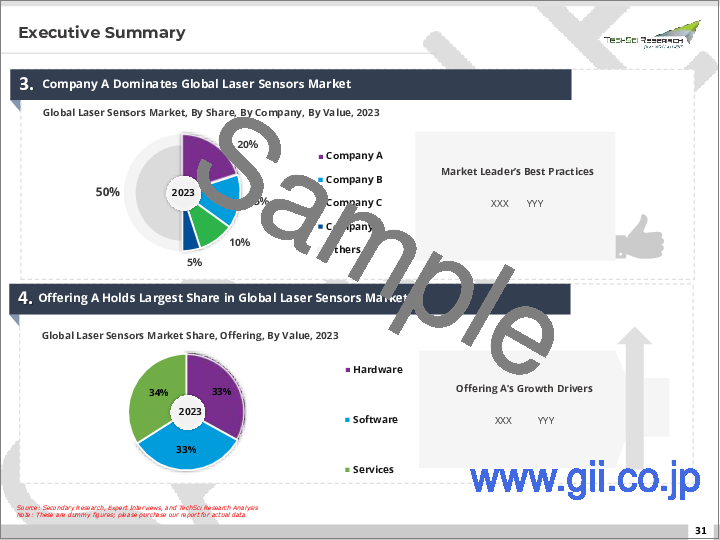

The Hardware segment held the largest Market share in 2023. Hardware components are the heart of laser sensors. They include lasers, photodetectors, lenses, and other physical components that emit laser beams, capture reflections, and perform the actual measurements. Without robust and reliable hardware, laser sensors would not be able to function, making hardware components indispensable. Hardware components are responsible for the high accuracy and precision that laser sensors offer. These components are designed to emit and detect laser beams with exceptional precision, allowing for accurate measurements. This accuracy is vital in applications where precision matters, such as manufacturing, industrial automation, and scientific research. Hardware components are built to withstand harsh industrial and environmental conditions. They are often designed to be robust, durable, and capable of operating in challenging environments, making them suitable for various industries, including automotive, aerospace, and construction. Manufacturers can customize hardware components to meet specific application requirements. This flexibility allows laser sensor providers to tailor their hardware to suit the unique needs of different industries and applications. Hardware components are relatively easy to integrate into existing systems and machinery. This ease of integration simplifies the adoption of laser sensors in various industries, as it doesn't require extensive software development or complex service implementations. Many industries have well-established standards for hardware components used in laser sensors. These standards ensure consistency and compatibility across different applications, making it easier for manufacturers to produce and consumers to adopt laser sensor hardware. Continuous advancements in hardware technology, such as miniaturization and increased performance, have allowed laser sensors to become more versatile and cost-effective. These advancements have further propelled the dominance of hardware in the market.

Regional Insights

North America

North America held the largest market share in 2023. North America has established itself as a dominant force in the Global Laser Sensors Market. This dominance can be attributed to several factors including technological advancements, strong industrial base, robust R&D capabilities, and a favorable regulatory environment. These elements collectively drive the region's leadership in the laser sensors market, making it a hub for innovation and growth.

One of the primary reasons for North America's dominance in the laser sensors market is its leadership in technological advancements. The region is home to some of the world's leading technology companies and research institutions that are at the forefront of innovation. Companies such as Keyence, Banner Engineering, and Rockwell Automation are based in North America and are known for their cutting-edge laser sensor technologies. These companies invest heavily in R&D to develop new and improved laser sensing solutions that meet the evolving needs of various industries.

North America's robust technological infrastructure supports the rapid development and deployment of laser sensors. The region has a well-established network of suppliers, manufacturers, and service providers that contribute to the growth of the laser sensors market. The presence of advanced manufacturing facilities and access to high-quality raw materials further bolster the region's ability to produce superior laser sensors.

North America's strong industrial base is another significant factor contributing to its dominance in the laser sensors market. The region is home to a diverse range of industries including automotive, aerospace, healthcare, and consumer electronics, all of which are major consumers of laser sensor technology. The automotive industry, in particular, relies heavily on laser sensors for applications such as distance measurement, object detection, and quality control in manufacturing processes.

The aerospace industry also benefits from the precision and reliability of laser sensors for various applications including navigation, inspection, and maintenance. In healthcare, laser sensors are used in medical devices and equipment for precise measurements and diagnostics. The widespread adoption of laser sensors across these industries drives demand and fosters innovation, reinforcing North America's leadership in the market.

Research and development (R&D) capabilities are crucial to maintaining a competitive edge in the laser sensors market, and North America excels in this area. The region's strong emphasis on R&D is supported by substantial investments from both the public and private sectors. Government initiatives and funding programs encourage innovation and the development of advanced technologies.

Universities and research institutions in North America play a pivotal role in advancing laser sensor technology. Collaborations between academic institutions and industry players facilitate the transfer of knowledge and the commercialization of new technologies. For instance, institutions like MIT, Stanford, and Caltech are known for their cutting-edge research in laser technology, contributing significantly to the growth of the laser sensors market.

A favorable regulatory environment also contributes to North America's dominance in the laser sensors market. Regulatory agencies such as the U.S. Food and Drug Administration (FDA) and the Federal Communications Commission (FCC) provide clear guidelines and standards for the development and use of laser sensors. These regulations ensure the safety, reliability, and quality of laser sensor products, fostering consumer confidence and market growth.

Key Market Players

- SICK AG

- Rockwell Automation Inc.

- Honeywell International Inc.

- OMRON Corporation

- Panasonic Corporation

- Keyence Corporation

- Baumer Holding AG

- Pepperl+Fuchs SE

- TE Connectivity Ltd.

- Leuze electronic GmbH + Co. KG

Report Scope:

In this report, the Global Laser Sensors Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

Laser Sensors Market, By Type:

- Compact

- Ultra-Compact

Laser Sensors Market, By Application:

- Security and Surveillance

- Motion and Guidance

- Quality Control

- Distance Measurement

- Manufacturing Plant Management

- Process Monitoring

- Others

Laser Sensors Market, By Component:

- Hardware

- Software

- Service

Laser Sensors Market, By Industry:

- Consumer Electronics

- Food and Beverages

- Automotive

- Chemical

- Aerospace and Defense

- Healthcare

- Others

Laser Sensors Market, By Region:

- North America

- United States

- Canada

- Mexico

- Europe

- France

- United Kingdom

- Italy

- Germany

- Spain

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- South America

- Brazil

- Argentina

- Colombia

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Kuwait

- Turkey

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Global Laser Sensors Market.

Available Customizations:

Global Laser Sensors Market report with the given Market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional Market players (up to five).

Table of Contents

1. Product Overview

- 1.1. Market Definition

- 1.2. Scope of the Market

- 1.2.1. Markets Covered

- 1.2.2. Years Considered for Study

- 1.3. Key Market Segmentations

2. Research Methodology

- 2.1. Objective of the Study

- 2.2. Baseline Methodology

- 2.3. Formulation of the Scope

- 2.4. Assumptions and Limitations

- 2.5. Sources of Research

- 2.5.1. Secondary Research

- 2.5.2. Primary Research

- 2.6. Approach for the Market Study

- 2.6.1. The Bottom-Up Approach

- 2.6.2. The Top-Down Approach

- 2.7. Methodology Followed for Calculation of Market Size & Market Shares

- 2.8. Forecasting Methodology

- 2.8.1. Data Triangulation & Validation

3. Executive Summary

4. Voice of Customer

5. Global Laser Sensors Market Outlook

- 5.1. Market Size & Forecast

- 5.1.1. By Value

- 5.2. Market Share & Forecast

- 5.2.1. By Type (Compact, Ultra-Compact)

- 5.2.2. By Component (Hardware, Software, Service)

- 5.2.3. By Application (Security and Surveillance, Motion and Guidance, Quality Control, Distance Measurement, Manufacturing Plant Management, Process Monitoring, Others)

- 5.2.4. By Industry (Consumer Electronics, Food and Beverages, Automotive, Chemical, Aerospace and Defense, Healthcare, Others)

- 5.2.5. By Region

- 5.2.6. By Company (2023)

- 5.3. Market Map

6. North America Laser Sensors Market Outlook

- 6.1. Market Size & Forecast

- 6.1.1. By Value

- 6.2. Market Share & Forecast

- 6.2.1. By Type

- 6.2.2. By Component

- 6.2.3. By Application

- 6.2.4. By Industry

- 6.2.5. By Country

- 6.3. North America: Country Analysis

- 6.3.1. United States Laser Sensors Market Outlook

- 6.3.1.1. Market Size & Forecast

- 6.3.1.1.1. By Value

- 6.3.1.2. Market Share & Forecast

- 6.3.1.2.1. By Type

- 6.3.1.2.2. By Component

- 6.3.1.2.3. By Application

- 6.3.1.2.4. By Industry

- 6.3.1.1. Market Size & Forecast

- 6.3.2. Canada Laser Sensors Market Outlook

- 6.3.2.1. Market Size & Forecast

- 6.3.2.1.1. By Value

- 6.3.2.2. Market Share & Forecast

- 6.3.2.2.1. By Type

- 6.3.2.2.2. By Component

- 6.3.2.2.3. By Application

- 6.3.2.2.4. By Industry

- 6.3.2.1. Market Size & Forecast

- 6.3.3. Mexico Laser Sensors Market Outlook

- 6.3.3.1. Market Size & Forecast

- 6.3.3.1.1. By Value

- 6.3.3.2. Market Share & Forecast

- 6.3.3.2.1. By Type

- 6.3.3.2.2. By Component

- 6.3.3.2.3. By Application

- 6.3.3.2.4. By Industry

- 6.3.3.1. Market Size & Forecast

- 6.3.1. United States Laser Sensors Market Outlook

7. Europe Laser Sensors Market Outlook

- 7.1. Market Size & Forecast

- 7.1.1. By Value

- 7.2. Market Share & Forecast

- 7.2.1. By Type

- 7.2.2. By Component

- 7.2.3. By Application

- 7.2.4. By Industry

- 7.2.5. By Country

- 7.3. Europe: Country Analysis

- 7.3.1. Germany Laser Sensors Market Outlook

- 7.3.1.1. Market Size & Forecast

- 7.3.1.1.1. By Value

- 7.3.1.2. Market Share & Forecast

- 7.3.1.2.1. By Type

- 7.3.1.2.2. By Component

- 7.3.1.2.3. By Application

- 7.3.1.2.4. By Industry

- 7.3.1.1. Market Size & Forecast

- 7.3.2. United Kingdom Laser Sensors Market Outlook

- 7.3.2.1. Market Size & Forecast

- 7.3.2.1.1. By Value

- 7.3.2.2. Market Share & Forecast

- 7.3.2.2.1. By Type

- 7.3.2.2.2. By Component

- 7.3.2.2.3. By Application

- 7.3.2.2.4. By Industry

- 7.3.2.1. Market Size & Forecast

- 7.3.3. Italy Laser Sensors Market Outlook

- 7.3.3.1. Market Size & Forecast

- 7.3.3.1.1. By Value

- 7.3.3.2. Market Share & Forecast

- 7.3.3.2.1. By Type

- 7.3.3.2.2. By Component

- 7.3.3.2.3. By Application

- 7.3.3.2.4. By Industry

- 7.3.3.1. Market Size & Forecast

- 7.3.4. France Laser Sensors Market Outlook

- 7.3.4.1. Market Size & Forecast

- 7.3.4.1.1. By Value

- 7.3.4.2. Market Share & Forecast

- 7.3.4.2.1. By Type

- 7.3.4.2.2. By Component

- 7.3.4.2.3. By Application

- 7.3.4.2.4. By Industry

- 7.3.4.1. Market Size & Forecast

- 7.3.5. Spain Laser Sensors Market Outlook

- 7.3.5.1. Market Size & Forecast

- 7.3.5.1.1. By Value

- 7.3.5.2. Market Share & Forecast

- 7.3.5.2.1. By Type

- 7.3.5.2.2. By Component

- 7.3.5.2.3. By Application

- 7.3.5.2.4. By Industry

- 7.3.5.1. Market Size & Forecast

- 7.3.1. Germany Laser Sensors Market Outlook

8. Asia-Pacific Laser Sensors Market Outlook

- 8.1. Market Size & Forecast

- 8.1.1. By Value

- 8.2. Market Share & Forecast

- 8.2.1. By Type

- 8.2.2. By Component

- 8.2.3. By Application

- 8.2.4. By Industry

- 8.2.5. By Country

- 8.3. Asia-Pacific: Country Analysis

- 8.3.1. China Laser Sensors Market Outlook

- 8.3.1.1. Market Size & Forecast

- 8.3.1.1.1. By Value

- 8.3.1.2. Market Share & Forecast

- 8.3.1.2.1. By Type

- 8.3.1.2.2. By Component

- 8.3.1.2.3. By Application

- 8.3.1.2.4. By Industry

- 8.3.1.1. Market Size & Forecast

- 8.3.2. India Laser Sensors Market Outlook

- 8.3.2.1. Market Size & Forecast

- 8.3.2.1.1. By Value

- 8.3.2.2. Market Share & Forecast

- 8.3.2.2.1. By Type

- 8.3.2.2.2. By Component

- 8.3.2.2.3. By Application

- 8.3.2.2.4. By Industry

- 8.3.2.1. Market Size & Forecast

- 8.3.3. Japan Laser Sensors Market Outlook

- 8.3.3.1. Market Size & Forecast

- 8.3.3.1.1. By Value

- 8.3.3.2. Market Share & Forecast

- 8.3.3.2.1. By Type

- 8.3.3.2.2. By Component

- 8.3.3.2.3. By Application

- 8.3.3.2.4. By Industry

- 8.3.3.1. Market Size & Forecast

- 8.3.4. South Korea Laser Sensors Market Outlook

- 8.3.4.1. Market Size & Forecast

- 8.3.4.1.1. By Value

- 8.3.4.2. Market Share & Forecast

- 8.3.4.2.1. By Type

- 8.3.4.2.2. By Component

- 8.3.4.2.3. By Application

- 8.3.4.2.4. By Industry

- 8.3.4.1. Market Size & Forecast

- 8.3.5. Australia Laser Sensors Market Outlook

- 8.3.5.1. Market Size & Forecast

- 8.3.5.1.1. By Value

- 8.3.5.2. Market Share & Forecast

- 8.3.5.2.1. By Type

- 8.3.5.2.2. By Component

- 8.3.5.2.3. By Application

- 8.3.5.2.4. By Industry

- 8.3.5.1. Market Size & Forecast

- 8.3.1. China Laser Sensors Market Outlook

9. South America Laser Sensors Market Outlook

- 9.1. Market Size & Forecast

- 9.1.1. By Value

- 9.2. Market Share & Forecast

- 9.2.1. By Type

- 9.2.2. By Component

- 9.2.3. By Application

- 9.2.4. By Industry

- 9.2.5. By Country

- 9.3. South America: Country Analysis

- 9.3.1. Brazil Laser Sensors Market Outlook

- 9.3.1.1. Market Size & Forecast

- 9.3.1.1.1. By Value

- 9.3.1.2. Market Share & Forecast

- 9.3.1.2.1. By Type

- 9.3.1.2.2. By Component

- 9.3.1.2.3. By Application

- 9.3.1.2.4. By Industry

- 9.3.1.1. Market Size & Forecast

- 9.3.2. Argentina Laser Sensors Market Outlook

- 9.3.2.1. Market Size & Forecast

- 9.3.2.1.1. By Value

- 9.3.2.2. Market Share & Forecast

- 9.3.2.2.1. By Type

- 9.3.2.2.2. By Component

- 9.3.2.2.3. By Application

- 9.3.2.2.4. By Industry

- 9.3.2.1. Market Size & Forecast

- 9.3.3. Colombia Laser Sensors Market Outlook

- 9.3.3.1. Market Size & Forecast

- 9.3.3.1.1. By Value

- 9.3.3.2. Market Share & Forecast

- 9.3.3.2.1. By Type

- 9.3.3.2.2. By Component

- 9.3.3.2.3. By Application

- 9.3.3.2.4. By Industry

- 9.3.3.1. Market Size & Forecast

- 9.3.1. Brazil Laser Sensors Market Outlook

10. Middle East and Africa Laser Sensors Market Outlook

- 10.1. Market Size & Forecast

- 10.1.1. By Value

- 10.2. Market Share & Forecast

- 10.2.1. By Type

- 10.2.2. By Component

- 10.2.3. By Application

- 10.2.4. By Industry

- 10.2.5. By Country

- 10.3. Middle East and Africa: Country Analysis

- 10.3.1. South Africa Laser Sensors Market Outlook

- 10.3.1.1. Market Size & Forecast

- 10.3.1.1.1. By Value

- 10.3.1.2. Market Share & Forecast

- 10.3.1.2.1. By Type

- 10.3.1.2.2. By Component

- 10.3.1.2.3. By Application

- 10.3.1.2.4. By Industry

- 10.3.1.1. Market Size & Forecast

- 10.3.2. Saudi Arabia Laser Sensors Market Outlook

- 10.3.2.1. Market Size & Forecast

- 10.3.2.1.1. By Value

- 10.3.2.2. Market Share & Forecast

- 10.3.2.2.1. By Type

- 10.3.2.2.2. By Component

- 10.3.2.2.3. By Application

- 10.3.2.2.4. By Industry

- 10.3.2.1. Market Size & Forecast

- 10.3.3. UAE Laser Sensors Market Outlook

- 10.3.3.1. Market Size & Forecast

- 10.3.3.1.1. By Value

- 10.3.3.2. Market Share & Forecast

- 10.3.3.2.1. By Type

- 10.3.3.2.2. By Component

- 10.3.3.2.3. By Application

- 10.3.3.2.4. By Industry

- 10.3.3.1. Market Size & Forecast

- 10.3.4. Kuwait Laser Sensors Market Outlook

- 10.3.4.1. Market Size & Forecast

- 10.3.4.1.1. By Value

- 10.3.4.2. Market Share & Forecast

- 10.3.4.2.1. By Type

- 10.3.4.2.2. By Component

- 10.3.4.2.3. By Application

- 10.3.4.2.4. By Industry

- 10.3.4.1. Market Size & Forecast

- 10.3.5. Turkey Laser Sensors Market Outlook

- 10.3.5.1. Market Size & Forecast

- 10.3.5.1.1. By Value

- 10.3.5.2. Market Share & Forecast

- 10.3.5.2.1. By Type

- 10.3.5.2.2. By Component

- 10.3.5.2.3. By Application

- 10.3.5.2.4. By Industry

- 10.3.5.1. Market Size & Forecast

- 10.3.1. South Africa Laser Sensors Market Outlook

11. Market Dynamics

- 11.1. Drivers

- 11.2. Challenges

12. Market Trends & Developments

13. Company Profiles

- 13.1. SICK AG

- 13.1.1. Business Overview

- 13.1.2. Key Revenue and Financials

- 13.1.3. Recent Developments

- 13.1.4. Key Personnel/Key Contact Person

- 13.1.5. Key Product/Services Offered

- 13.2. Rockwell Automation Inc.

- 13.2.1. Business Overview

- 13.2.2. Key Revenue and Financials

- 13.2.3. Recent Developments

- 13.2.4. Key Personnel/Key Contact Person

- 13.2.5. Key Product/Services Offered

- 13.3. Honeywell International Inc.

- 13.3.1. Business Overview

- 13.3.2. Key Revenue and Financials

- 13.3.3. Recent Developments

- 13.3.4. Key Personnel/Key Contact Person

- 13.3.5. Key Product/Services Offered

- 13.4. OMRON Corporation

- 13.4.1. Business Overview

- 13.4.2. Key Revenue and Financials

- 13.4.3. Recent Developments

- 13.4.4. Key Personnel/Key Contact Person

- 13.4.5. Key Product/Services Offered

- 13.5. Panasonic Corporation

- 13.5.1. Business Overview

- 13.5.2. Key Revenue and Financials

- 13.5.3. Recent Developments

- 13.5.4. Key Personnel/Key Contact Person

- 13.5.5. Key Product/Services Offered

- 13.6. Keyence Corporation

- 13.6.1. Business Overview

- 13.6.2. Key Revenue and Financials

- 13.6.3. Recent Developments

- 13.6.4. Key Personnel/Key Contact Person

- 13.6.5. Key Product/Services Offered

- 13.7. Baumer Holding AG

- 13.7.1. Business Overview

- 13.7.2. Key Revenue and Financials

- 13.7.3. Recent Developments

- 13.7.4. Key Personnel/Key Contact Person

- 13.7.5. Key Product/Services Offered

- 13.8. Pepperl+Fuchs SE

- 13.8.1. Business Overview

- 13.8.2. Key Revenue and Financials

- 13.8.3. Recent Developments

- 13.8.4. Key Personnel/Key Contact Person

- 13.8.5. Key Product/Services Offered

- 13.9. TE Connectivity Ltd.

- 13.9.1. Business Overview

- 13.9.2. Key Revenue and Financials

- 13.9.3. Recent Developments

- 13.9.4. Key Personnel/Key Contact Person

- 13.9.5. Key Product/Services Offered

- 13.10. Leuze electronic GmbH + Co. KG

- 13.10.1. Business Overview

- 13.10.2. Key Revenue and Financials

- 13.10.3. Recent Developments

- 13.10.4. Key Personnel/Key Contact Person

- 13.10.5. Key Product/Services Offered