|

|

市場調査レポート

商品コード

1761168

高速ケーブルの市場規模と予測、2021年~2031年、世界と地域のシェア、動向、成長機会分析レポート:タイプ別、用途別、地域別High Speed Cables Market Size and Forecast 2021 - 2031, Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type, Application, and Geography |

||||||

|

|||||||

|

|||||||

| 高速ケーブルの市場規模と予測、2021年~2031年、世界と地域のシェア、動向、成長機会分析レポート:タイプ別、用途別、地域別 |

|

出版日: 2025年05月30日

発行: The Insight Partners

ページ情報: 英文 187 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

高速ケーブル市場規模は、2024年の129億米ドルから2031年には249億9,000万米ドルに達すると予測され、2025年から2031年までの推定CAGRは10.2%です。

地域別では、高速ケーブル市場は北米、欧州、アジア太平洋、中東・アフリカ、中南米に区分されます。2024年には、欧州が市場で大きなシェアを占めています。Data Center Mapによると、西欧には現在、24カ国に2,273のデータセンターがあり、この地域の高度なデジタルインフラと成熟したコロケーション市場が浮き彫りになっています。この広範なネットワークは幅広い産業を支えており、特にフランクフルト(ドイツ)、ロンドン(英国)、アムステルダム(オランダ)、パリ(フランス)といった金融・経済の主要拠点にデータセンターが集中しています。これらの都市は西欧におけるデータセンターサービスの主要市場であり、その主な理由は金融都市としての役割と、世界のインターネットトラフィックのルーティングにおける戦略的重要性にあります。これらの都市の高密度コロケーション施設は、フランクフルトのDE-CIX、アムステルダムのAMS-IX、ロンドンのLINXといった主要なインターネット・エクスチェンジ・ポイント(IXP)を通じて処理される大量のデータ交換を支えています。これらの取引所は世界で最も利用者の多い取引所のひとつであり、商業および消費者向けデジタルサービスに不可欠な低遅延、広帯域幅の接続を促進しています。

西欧におけるデータセンターの拡大は、光ファイバーや先進的な銅線ケーブルシステムなど、高速ケーブルソリューションの需要を大きく促進しています。高速ケーブルはデータセンターの性能と信頼性を維持するために不可欠であり、サーバー、ストレージシステム、ネットワークコンポーネント間の迅速なデータ転送を可能にします。さらに、クラウド・コンピューティング、AI、エッジ・コンピューティングなどの先端技術は、堅牢でスケーラブルな大容量のケーブル配線インフラの必要性をさらに高めています。西欧のデジタル経済が進化を続ける中、高速ケーブルへの投資も並行して増加し、同地域は世界の高速ケーブル市場の主要貢献地域として位置づけられると予想されます。高密度データセンター、重要なIXP、産業全体のデジタル変革の融合は、このエコシステム内で事業を展開するケーブルメーカーやサービスプロバイダーにとって、強い見通しを強調しています。

高速ケーブル市場の分析は、以下のセグメントを考慮して実施されています:タイプ別と用途別です。

タイプ別では、ダイレクトアタッチ銅(DAC)ケーブル、アクティブ光ケーブル(AOC)、アクティブ銅ケーブル(ACC)、PCIeケーブル、アクティブ電気ケーブル(AEC)、SASケーブルに区分されます。高速ダイレクト・アタッチ・ケーブル(DAC)は銅ベースで、データセンター内のサーバー、スイッチ、ストレージシステムなどのデバイス間の短距離高速データ転送に使用されます。さまざまなフォームファクターと速度があり、10Gから800Gまでの幅があります。DACは400Gbps以上のデータ転送速度に対応できるため、ハイパフォーマンス・コンピューティング・アプリケーションに最適です。DACは光ケーブルよりも消費電力が少ないため、エネルギー効率が高いです。DACは通常、特に短い距離では光接続よりも安価です。費用対効果が高く、直付け銅線ケーブルの入手が容易であることが、DACの需要が大きい2つの重要な要因です。これらのケーブルは、光トランシーバーや光ファイバーケーブルよりもおよそ2倍から3倍安価です。また、DACケーブルは非常に信頼性が高く、ポートに接続するとケーブルが強力に接続されるため、途切れることなく常に信号が流れます。この信頼性の高さも、ケーブルの需要を高める要因のひとつです。ケーブルの需要が高まるもう一つの要因は、信頼性の高さです。この要因は、高速ケーブル市場におけるダイレクトアタッチ銅線ケーブルの市場を牽引しています。

さらに、データセンターの展開が拡大していることも、高速ケーブル市場の成長を後押ししています。また、スマートシティの出現は、今後数年間に新たな高速ケーブル市場動向をもたらすと予想されています。

アプリケーション別に見ると、市場はスイッチ間相互接続、スイッチ・サーバー間相互接続、サーバー・ストレージ間相互接続に区分されます。SASはSerial-attached SCSIとして知られ、ソリッド・ステート・ドライブ、ハード・ディスク・ドライブ、CD-ROMドライブなどのコンピュータ・ストレージ・デバイスとのデータ転送に使用される技術です。SASケーブルの物理リンクは、2つの差動信号ペアとして利用される4本のワイヤーに設定されています。一方のペアは一方向にデータを伝送し、もう一方は逆方向に伝送します。スマートフォンの販売台数の増加に伴い、コンピュータデバイスの採用が増加しているため、デジタルデータ量が増加しており、世界中のデータセンターの展開が拡大しているため、SASケーブルの採用が増加しています。さらに、エンドユーザーによるハードディスクドライブよりもソリッドステートドライブの使用が増加していることも、市場の成長に寄与している要因の1つです。市場には、ミニSASとミニSAS高密度という2種類のSASケーブルがあります。ミニ SAS高密度ケーブルは、6Gb/秒のSASをサポートする能力があるため、大企業が主に購入しています。高密度ミニ SASケーブルの需要は、エンドユーザーの大半がデータフローの増加を経験しているため、今後数年間で増加すると予想されます。高速ケーブル市場におけるSASケーブルの市場を理解し予測するために、この要因を分析します。

Amphenol Corporation、Axon Cable SAS、Molex LLC、Volex PLC、NVIDIA CORPORATION、Samtec INC、Shenzhen Sopto Technology Co.Ltd、TE Connectivity Corporation、Edge Optical Solutions、JPC Connectivityなどが、高速ケーブル市場レポートで紹介されている主要企業です。

高速ケーブル市場推計・予測は、主要企業の出版物、協会データ、データベースなど、さまざまな2次調査と1次調査に基づいています。徹底的な二次調査は、高速ケーブル市場の成長に関連する質的・量的情報を得るために、社内外の情報源を用いて実施しました。このプロセスは、すべての市場セグメントに関する市場の概要と予測を得るのにも役立ちます。また、データを検証し、分析的洞察を得るために、業界関係者に複数の一次インタビューを実施しました。このプロセスには、副社長、市場開拓マネージャー、マーケットインテリジェンスマネージャー、国内営業マネージャーなどの業界専門家と、高速ケーブル市場を専門とする評価専門家、研究アナリスト、キーオピニオンリーダーなどの外部コンサルタントが参加しています。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- アナリスト市場の展望

- 市場の魅力

第3章 調査手法

- 2次調査

- 1次調査

- 仮説の策定

- マクロ経済要因分析

- ファンデーション数値の開発

- データの三角測量

- 国レベルのデータ

第4章 高速ケーブル市場情勢

- PEST分析

- エコシステム分析

- バリューチェーンのベンダー一覧

第5章 高速ケーブル市場 - 主な市場力学

- 高速ケーブル市場 - 主要市場力学

- 市場促進要因

- データセンター展開の拡大

- 企業ITインフラへの投資の増加

- 市場抑制要因

- 先端光ケーブルとアクティブケーブルの高コスト

- 市場機会

- 5Gネットワークサービスへの展開

- 今後の動向

- スマートシティの出現

- 促進要因と抑制要因の影響

第6章 高速ケーブル市場:世界市場分析

- 高速ケーブル市場の収益、2021~2031年

- 高速ケーブル市場予測分析

第7章 章 市場分析:タイプ別

- ダイレクトアタッチ銅(DAC)ケーブル

- アクティブ光ケーブル(AOC)

- アクティブ銅ケーブル

- PCIeケーブル

- アクティブ電気ケーブル(AEC)

- SASケーブル

第8章 市場分析:用途別

- スイッチ間相互接続

- スイッチからサーバーへの相互接続

- サーバーからストレージへの相互接続

第9章 地域別分析

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- アジア太平洋地域のその他諸国

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- 中南米

- ブラジル

- アルゼンチン

- その他中南米

第10章 競合情勢

- 主要プレーヤー別ヒートマップ分析

- 企業シェア分析、2024年

第11章 業界情勢

- 市場イニシアティブ

- 製品ニュース・企業ニュース

- コラボレーションとM&A

第12章 企業プロファイル

- Amphenol Corporation

- Axon Cable SAS

- Molex LLC

- Volex Plc

- NVIDIA Corp

- Samtec Inc

- Shenzhen Sopto Technology Co., Ltd.

- TE Connectivity Ltd

- JPC Connectivity

- EDGE Optical Solutions

第13章 付録

List Of Tables

- Table 1. High Speed Cable Market Segmentation

- Table 2. High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million)

- Table 3. High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million)

- Table 4. High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 5. High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 6. High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 7. High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 8. North America: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Type

- Table 9. North America: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 10. North America: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Application

- Table 11. North America: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 12. North America: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Country

- Table 13. North America: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Country

- Table 14. United States: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 15. United States: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 16. United States: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 17. United States: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 18. Canada: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 19. Canada: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 20. Canada: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 21. Canada: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 22. Mexico: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 23. Mexico: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 24. Mexico: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 25. Mexico: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 26. Europe: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Type

- Table 27. Europe: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 28. Europe: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Application

- Table 29. Europe: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 30. Europe: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Country

- Table 31. Europe: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Country

- Table 32. Germany: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 33. Germany: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 34. Germany: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 35. Germany: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 36. United Kingdom: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 37. United Kingdom: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 38. United Kingdom: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 39. United Kingdom: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 40. France: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 41. France: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 42. France: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 43. France: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 44. Italy: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 45. Italy: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 46. Italy: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 47. Italy: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 48. Russia: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 49. Russia: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 50. Russia: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 51. Russia: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 52. Rest of Europe: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 53. Rest of Europe: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 54. Rest of Europe: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 55. Rest of Europe: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 56. Asia Pacific: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Type

- Table 57. Asia Pacific: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 58. Asia Pacific: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Application

- Table 59. Asia Pacific: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 60. Asia Pacific: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Country

- Table 61. Asia Pacific: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Country

- Table 62. China: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 63. China: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 64. China: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 65. China: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 66. Japan: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 67. Japan: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 68. Japan: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 69. Japan: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 70. India: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 71. India: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 72. India: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 73. India: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 74. South Korea: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 75. South Korea: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 76. South Korea: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 77. South Korea: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 78. Australia: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 79. Australia: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 80. Australia: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 81. Australia: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 82. Rest of APAC: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 83. Rest of APAC: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 84. Rest of APAC: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 85. Rest of APAC: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 86. Middle East and Africa: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Type

- Table 87. Middle East and Africa: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 88. Middle East and Africa: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Application

- Table 89. Middle East and Africa: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 90. Middle East and Africa: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Country

- Table 91. Middle East and Africa: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Country

- Table 92. United Arab Emirates: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 93. United Arab Emirates: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 94. United Arab Emirates: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 95. United Arab Emirates: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 96. Saudi Arabia: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 97. Saudi Arabia: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 98. Saudi Arabia: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 99. Saudi Arabia: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 100. South Africa: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 101. South Africa: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 102. South Africa: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 103. South Africa: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 104. Rest of Middle East and Africa: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 105. Rest of Middle East and Africa: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 106. Rest of Middle East and Africa: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 107. Rest of Middle East and Africa: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 108. South and Central America: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Type

- Table 109. South and Central America: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 110. South and Central America: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Application

- Table 111. South and Central America: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 112. South and Central America: High Speed Cable Market - Revenue, 2021 - 2024 (US$ Million) - by Country

- Table 113. South and Central America: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Country

- Table 114. Brazil: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 115. Brazil: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 116. Brazil: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 117. Brazil: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 118. Argentina: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 119. Argentina: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 120. Argentina: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 121. Argentina: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

- Table 122. Rest of South and Central America: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Type

- Table 123. Rest of South and Central America: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Type

- Table 124. Rest of South and Central America: High Speed Cable Market - Revenue, 2021 - 2024(US$ Million) - by Application

- Table 125. Rest of South and Central America: High Speed Cable Market - Revenue, 2025 - 2031 (US$ Million) - by Application

List Of Figures

- Figure 1. High Speed Cable Market Segmentation, by Geography

- Figure 2. PEST Analysis

- Figure 3. Ecosystem: High Speed Cable Market

- Figure 4. Impact Analysis of Drivers and Restraints

- Figure 5. High Speed Cable Market Breakdown by Geography, 2024 and 2031 (%)

- Figure 6. High Speed Cable Market Revenue (US$ Million), 2021-2031

- Figure 7. High Speed Cable Market Share (%) - by Type (2024 and 2031)

- Figure 8. Direct Attach Copper (DAC) Cable: High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 9. Active Optical Cables (AOC): High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 10. Active Copper Cables: High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 11. PCIe Cable: High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 12. Active Electric Cable (AEC): High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 13. SAS Cable: High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 14. High Speed Cable Market Share (%) - by Application (2024 and 2031)

- Figure 15. Switch to Switch Interconnect: High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 16. Switch to Server: High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 17. Server to Storage Interconnect: High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 18. High Speed Cable Market Breakdown by Region, 2024 and 2031 (%)

- Figure 19. North America: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 20. North America: High Speed Cable Market Breakdown, by Type (2024 and 2031)

- Figure 21. North America: High Speed Cable Market Breakdown, by Application (2024 and 2031)

- Figure 22. North America: High Speed Cable Market Breakdown, by Key Countries, 2024 and 2031 (%)

- Figure 23. United States: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 24. Canada: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 25. Mexico: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 26. Europe: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 27. Europe: High Speed Cable Market Breakdown, by Type (2024 and 2031)

- Figure 28. Europe: High Speed Cable Market Breakdown, by Application (2024 and 2031)

- Figure 29. Europe: High Speed Cable Market Breakdown, by Key Countries, 2024 and 2031 (%)

- Figure 30. Germany: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 31. United Kingdom: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 32. France: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 33. Italy: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 34. Russia: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 35. Rest of Europe: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 36. Asia Pacific: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 37. Asia Pacific: High Speed Cable Market Breakdown, by Type (2024 and 2031)

- Figure 38. Asia Pacific: High Speed Cable Market Breakdown, by Application (2024 and 2031)

- Figure 39. Asia Pacific: High Speed Cable Market Breakdown, by Key Countries, 2024 and 2031 (%)

- Figure 40. China: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 41. Japan: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 42. India: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 43. South Korea: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 44. Australia: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 45. Rest of APAC: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 46. Middle East and Africa: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 47. Middle East and Africa: High Speed Cable Market Breakdown, by Type (2024 and 2031)

- Figure 48. Middle East and Africa: High Speed Cable Market Breakdown, by Application (2024 and 2031)

- Figure 49. Middle East and Africa: High Speed Cable Market Breakdown, by Key Countries, 2024 and 2031 (%)

- Figure 50. United Arab Emirates: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 51. Saudi Arabia: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 52. South Africa: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 53. Rest of Middle East and Africa: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 54. South and Central America: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 55. South and Central America: High Speed Cable Market Breakdown, by Type (2024 and 2031)

- Figure 56. South and Central America: High Speed Cable Market Breakdown, by Application (2024 and 2031)

- Figure 57. South and Central America: High Speed Cable Market Breakdown, by Key Countries, 2024 and 2031 (%)

- Figure 58. Brazil: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 59. Argentina: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 60. Rest of South and Central America: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- Figure 61. Heat Map Analysis by Key Players

- Figure 62. Company Market Share Analysis, 2024

The high speed cables market size is expected to reach US$ 24.99 billion by 2031 from 12.90 billion in 2024, at an estimated CAGR of 10.2% from 2025 to 2031.

By Geography the high speed cables market is segmented into North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. In 2024, Europe held a significant share in the market. According to Data Center Map, Western Europe currently hosts 2,273 data centers across 24 countries, highlighting the region's advanced digital infrastructure and mature colocation market. This extensive network supports a broad range of industries, with a particular concentration of data centers in key financial and economic hubs such as Frankfurt (Germany), London (United Kingdom), Amsterdam (The Netherlands), and Paris (France). These cities represent the primary markets for data center services in Western Europe, largely due to their roles as financial capitals and their strategic importance in global internet traffic routing. High-density colocation facilities in these locations support massive volumes of data exchange, much of which is handled through major internet exchange points (IXPs) such as DE-CIX in Frankfurt, AMS-IX in Amsterdam, and LINX in London. These exchanges are among the busiest in the world, facilitating low-latency, high-bandwidth connections that are vital to both commercial and consumer digital services.

The expansion of data centers in Western Europe is significantly driving demand for high-speed cable solutions, including fiber optics and advanced copper cabling systems. High-speed cables are essential for maintaining the performance and reliability of data centers, enabling rapid data transmission between servers, storage systems, and network components. Additionally, advanced technologies such as cloud computing, AI, and edge computing are further intensifying the need for robust, scalable, and high-capacity cabling infrastructure. As Western Europe's digital economy continues to evolve, investment in high-speed cabling is expected to rise in parallel, positioning the region as a major contributor to the global high-speed cable market. The convergence of high-density data centers, critical IXPs, and digital transformation across industries underscores a strong outlook for cable manufacturers and service providers operating within this ecosystem.

The High Speed Cables market analysis has been carried out by considering the following segments: Type and Application.

Based on the type, the market is segmented into direct attach copper (DAC) cable, active optical cable (AOC), active copper cable (ACC), PCIe cable, active electrical cable (AEC), and SAS cable. High-Speed Direct Attach Cables (DACs) are copper-based and are used for short-distance, high-speed data transfer between devices such as servers, switches, and storage systems in data centers. They are available in various form factors and speeds, ranging from 10G to 800G. DACs are perfect for high-performance computing applications since they can handle data transmission speeds of 400 Gbps and more. DACs are more energy-efficient than optical cables as they use less power. DACs are typically less expensive than optical connections, particularly at shorter distances. Cost effectiveness and easy availability of direct attach copper cables are the two crucial factors behind the significant demand for the same. These cables are approximately 2 to 3 times less expensive than optical transceivers or fiber optic cables. Also, the DAC cables are extremely dependable as when attached to the port, the cables make strong connection, thereby ensuring constant flow of signals without interruption. The dependable factor is also another parameter for higher demand of the cables. This factor also drives the market for direct attach copper cables in the high speed cables market.

Moreover, factor such as growing deployment of data centers propel the high speed cables market growth. Also, emergence of smart cities is expected to bring new High Speed Cables market trends in the coming years.

Based on application, the market is segmented into switch to switch interconnect, switch to server, and server to storage interconnect. SAS, known as Serial-attached SCSI, is technology used for transferring data from and to computer storage devices such as solid-state drives, hard disk drive, and CD-ROM drives. The SAS cable physical links are set for four wires utilized as two differential signal pairs. One pair transmit data in one direction and the other transmits in the opposite direction. With the growing amount of digital data owing to the increasing adoption of computer devices along increasing sales of smartphones has resulted in growing deployment of data centers across the globe, the adoption of SAS cable is on the higher side. Moreover, the growing use solid-state drives over hard disk drives by end users is among another factor contributing to the growth of the market. There are two types of SAS cables available in the market namely; mini SAS and mini SAS high density. The mini SAS high density cables are majorly procured by the larger enterprises owing to the ability of these cables to support 6Gb/sec SAS. The demand for the high density mini SAS cables is expected to rise over the years, as majority of the end users are experiencing rise in data flow. This factor is analyzed to understand and forecast the market of SAS cable in the high speed cable market.

Amphenol Corporation, Axon Cable SAS, Molex LLC, Volex PLC, NVIDIA CORPORATION, Samtec INC, Shenzhen Sopto Technology Co., Ltd., TE Connectivity Corporation, Edge Optical Solutions, and JPC Connectivity are among the key players profiled in the high speed cables market report.

The high speed cables market forecast is estimated on the basis of various secondary and primary research findings such as key company publications, association data, and databases. Exhaustive secondary research has been conducted using internal and external sources to obtain qualitative and quantitative information related to the high speed cables market growth. The process also helps obtain an overview and forecast of the market with respect to all the market segments. Also, multiple primary interviews have been conducted with industry participants to validate the data and gain analytical insights. This process includes industry experts such as VPs, business development managers, market intelligence managers, and national sales managers, along with external consultants such as valuation experts, research analysts, and key opinion leaders, specializing in the high speed cables market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Analyst Market Outlook

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Secondary Research

- 3.2 Primary Research

- 3.2.1 Hypothesis formulation:

- 3.2.2 Macro-economic factor analysis:

- 3.2.3 Developing base number:

- 3.2.4 Data Triangulation:

- 3.2.5 Country level data:

4. High Speed Cable Market Landscape

- 4.1 Overview

- 4.2 PEST Analysis

- 4.3 Ecosystem Analysis

- 4.3.1 List of Vendors in Value Chain

5. High Speed Cable Market - Key Market Dynamics

- 5.1 High Speed Cable Market - Key Market Dynamics

- 5.2 Market Drivers

- 5.2.1 Growing Deployment of Data Centers

- 5.2.2 Rising Investments in Enterprise IT Infrastructure

- 5.3 Market Restraints

- 5.3.1 High Cost of Advanced Optical and Active Cables

- 5.4 Market Opportunities

- 5.4.1 Deployment in 5G Network Services

- 5.5 Future Trends

- 5.5.1 Emergence of Smart Cities

- 5.6 Impact of Drivers and Restraints:

6. High Speed Cable Market - Global Market Analysis

- 6.1 High Speed Cable Market Revenue (US$ Million), 2021-2031

- 6.2 High Speed Cable Market Forecast Analysis

7. High Speed Cable Market Analysis - by Type

- 7.1 Direct Attach Copper (DAC) Cable

- 7.1.1 Overview

- 7.1.2 Direct Attach Copper (DAC) Cable: High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- 7.2 Active Optical Cables (AOC)

- 7.2.1 Overview

- 7.2.2 Active Optical Cables (AOC): High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- 7.3 Active Copper Cables

- 7.3.1 Overview

- 7.3.2 Active Copper Cables: High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- 7.4 PCIe Cable

- 7.4.1 Overview

- 7.4.2 PCIe Cable: High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- 7.5 Active Electric Cable (AEC)

- 7.5.1 Overview

- 7.5.2 Active Electric Cable (AEC): High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- 7.6 SAS Cable

- 7.6.1 Overview

- 7.6.2 SAS Cable: High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

8. High Speed Cable Market Analysis - by Application

- 8.1 Switch to Switch Interconnect

- 8.1.1 Overview

- 8.1.2 Switch to Switch Interconnect: High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- 8.2 Switch to Server

- 8.2.1 Overview

- 8.2.2 Switch to Server: High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

- 8.3 Server to Storage Interconnect

- 8.3.1 Overview

- 8.3.2 Server to Storage Interconnect: High Speed Cable Market - Revenue and Forecast to 2031 (US$ Million)

9. High Speed Cable Market - Geographical Analysis

- 9.1 Overview

- 9.2 North America

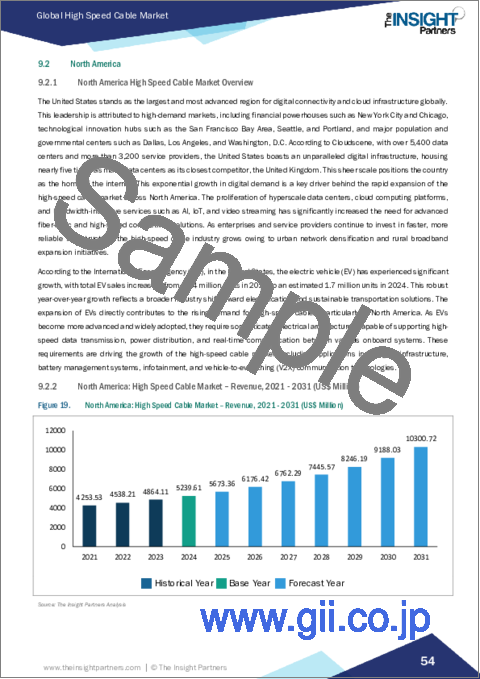

- 9.2.1 North America High Speed Cable Market Overview

- 9.2.2 North America: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.2.3 North America: High Speed Cable Market Breakdown, by Type

- 9.2.3.1 North America: High Speed Cable Market - Revenue and Forecast Analysis - by Type

- 9.2.4 North America: High Speed Cable Market Breakdown, by Application

- 9.2.4.1 North America: High Speed Cable Market - Revenue and Forecast Analysis - by Application

- 9.2.5 North America: High Speed Cable Market - Revenue and Forecast Analysis - by Country

- 9.2.5.1 North America: High Speed Cable Market - Revenue and Forecast Analysis - by Country

- 9.2.5.2 United States: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.2.5.2.1 United States: High Speed Cable Market Breakdown, by Type

- 9.2.5.2.2 United States: High Speed Cable Market Breakdown, by Application

- 9.2.5.3 Canada: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.2.5.3.1 Canada: High Speed Cable Market Breakdown, by Type

- 9.2.5.3.2 Canada: High Speed Cable Market Breakdown, by Application

- 9.2.5.4 Mexico: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.2.5.4.1 Mexico: High Speed Cable Market Breakdown, by Type

- 9.2.5.4.2 Mexico: High Speed Cable Market Breakdown, by Application

- 9.3 Europe

- 9.3.1 Europe High Speed Cable Market Overview

- 9.3.2 Europe: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.3.3 Europe: High Speed Cable Market Breakdown, by Type

- 9.3.3.1 Europe: High Speed Cable Market - Revenue and Forecast Analysis - by Type

- 9.3.4 Europe: High Speed Cable Market Breakdown, by Application

- 9.3.4.1 Europe: High Speed Cable Market - Revenue and Forecast Analysis - by Application

- 9.3.5 Europe: High Speed Cable Market - Revenue and Forecast Analysis - by Country

- 9.3.5.1 Europe: High Speed Cable Market - Revenue and Forecast Analysis - by Country

- 9.3.5.2 Germany: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.3.5.2.1 Germany: High Speed Cable Market Breakdown, by Type

- 9.3.5.2.2 Germany: High Speed Cable Market Breakdown, by Application

- 9.3.5.3 United Kingdom: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.3.5.3.1 United Kingdom: High Speed Cable Market Breakdown, by Type

- 9.3.5.3.2 United Kingdom: High Speed Cable Market Breakdown, by Application

- 9.3.5.4 France: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.3.5.4.1 France: High Speed Cable Market Breakdown, by Type

- 9.3.5.4.2 France: High Speed Cable Market Breakdown, by Application

- 9.3.5.5 Italy: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.3.5.5.1 Italy: High Speed Cable Market Breakdown, by Type

- 9.3.5.5.2 Italy: High Speed Cable Market Breakdown, by Application

- 9.3.5.6 Russia: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.3.5.6.1 Russia: High Speed Cable Market Breakdown, by Type

- 9.3.5.6.2 Russia: High Speed Cable Market Breakdown, by Application

- 9.3.5.7 Rest of Europe: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.3.5.7.1 Rest of Europe: High Speed Cable Market Breakdown, by Type

- 9.3.5.7.2 Rest of Europe: High Speed Cable Market Breakdown, by Application

- 9.4 Asia Pacific

- 9.4.1 Asia Pacific High Speed Cable Market Overview

- 9.4.2 Asia Pacific: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.4.3 Asia Pacific: High Speed Cable Market Breakdown, by Type

- 9.4.3.1 Asia Pacific: High Speed Cable Market - Revenue and Forecast Analysis - by Type

- 9.4.4 Asia Pacific: High Speed Cable Market Breakdown, by Application

- 9.4.4.1 Asia Pacific: High Speed Cable Market - Revenue and Forecast Analysis - by Application

- 9.4.5 Asia Pacific: High Speed Cable Market - Revenue and Forecast Analysis - by Country

- 9.4.5.1 Asia Pacific: High Speed Cable Market - Revenue and Forecast Analysis - by Country

- 9.4.5.2 China: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.4.5.2.1 China: High Speed Cable Market Breakdown, by Type

- 9.4.5.2.2 China: High Speed Cable Market Breakdown, by Application

- 9.4.5.3 Japan: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.4.5.3.1 Japan: High Speed Cable Market Breakdown, by Type

- 9.4.5.3.2 Japan: High Speed Cable Market Breakdown, by Application

- 9.4.5.4 India: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.4.5.4.1 India: High Speed Cable Market Breakdown, by Type

- 9.4.5.4.2 India: High Speed Cable Market Breakdown, by Application

- 9.4.5.5 South Korea: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.4.5.5.1 South Korea: High Speed Cable Market Breakdown, by Type

- 9.4.5.5.2 South Korea: High Speed Cable Market Breakdown, by Application

- 9.4.5.6 Australia: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.4.5.6.1 Australia: High Speed Cable Market Breakdown, by Type

- 9.4.5.6.2 Australia: High Speed Cable Market Breakdown, by Application

- 9.4.5.7 Rest of APAC: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.4.5.7.1 Rest of APAC: High Speed Cable Market Breakdown, by Type

- 9.4.5.7.2 Rest of APAC: High Speed Cable Market Breakdown, by Application

- 9.5 Middle East and Africa

- 9.5.1 Middle East and Africa High Speed Cable Market Overview

- 9.5.2 Middle East and Africa: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.5.3 Middle East and Africa: High Speed Cable Market Breakdown, by Type

- 9.5.3.1 Middle East and Africa: High Speed Cable Market - Revenue and Forecast Analysis - by Type

- 9.5.4 Middle East and Africa: High Speed Cable Market Breakdown, by Application

- 9.5.4.1 Middle East and Africa: High Speed Cable Market - Revenue and Forecast Analysis - by Application

- 9.5.5 Middle East and Africa: High Speed Cable Market - Revenue and Forecast Analysis - by Country

- 9.5.5.1 Middle East and Africa: High Speed Cable Market - Revenue and Forecast Analysis - by Country

- 9.5.5.2 United Arab Emirates: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.5.5.2.1 United Arab Emirates: High Speed Cable Market Breakdown, by Type

- 9.5.5.2.2 United Arab Emirates: High Speed Cable Market Breakdown, by Application

- 9.5.5.3 Saudi Arabia: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.5.5.3.1 Saudi Arabia: High Speed Cable Market Breakdown, by Type

- 9.5.5.3.2 Saudi Arabia: High Speed Cable Market Breakdown, by Application

- 9.5.5.4 South Africa: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.5.5.4.1 South Africa: High Speed Cable Market Breakdown, by Type

- 9.5.5.4.2 South Africa: High Speed Cable Market Breakdown, by Application

- 9.5.5.5 Rest of Middle East and Africa: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.5.5.5.1 Rest of Middle East and Africa: High Speed Cable Market Breakdown, by Type

- 9.5.5.5.2 Rest of Middle East and Africa: High Speed Cable Market Breakdown, by Application

- 9.6 South and Central America

- 9.6.1 South and Central America High Speed Cable Market Overview

- 9.6.2 South and Central America: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.6.3 South and Central America: High Speed Cable Market Breakdown, by Type

- 9.6.3.1 South and Central America: High Speed Cable Market - Revenue and Forecast Analysis - by Type

- 9.6.4 South and Central America: High Speed Cable Market Breakdown, by Application

- 9.6.4.1 South and Central America: High Speed Cable Market - Revenue and Forecast Analysis - by Application

- 9.6.5 South and Central America: High Speed Cable Market - Revenue and Forecast Analysis - by Country

- 9.6.5.1 South and Central America: High Speed Cable Market - Revenue and Forecast Analysis - by Country

- 9.6.5.2 Brazil: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.6.5.2.1 Brazil: High Speed Cable Market Breakdown, by Type

- 9.6.5.2.2 Brazil: High Speed Cable Market Breakdown, by Application

- 9.6.5.3 Argentina: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.6.5.3.1 Argentina: High Speed Cable Market Breakdown, by Type

- 9.6.5.3.2 Argentina: High Speed Cable Market Breakdown, by Application

- 9.6.5.4 Rest of South and Central America: High Speed Cable Market - Revenue, 2021 - 2031 (US$ Million)

- 9.6.5.4.1 Rest of South and Central America: High Speed Cable Market Breakdown, by Type

- 9.6.5.4.2 Rest of South and Central America: High Speed Cable Market Breakdown, by Application

10. Competitive Landscape

- 10.1 Heat Map Analysis by Key Players

- 10.2 Company Market Share Analysis, 2024

11. Industry Landscape

- 11.1 Overview

- 11.2 Market Initiative

- 11.3 Product News & Company News

- 11.4 Collaboration and Mergers & Acquisitions

12. Company Profiles

- 12.1 Amphenol Corporation

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Axon Cable SAS

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 Molex LLC

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Volex Plc

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 NVIDIA Corp

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 Samtec Inc

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 Shenzhen Sopto Technology Co., Ltd.

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 TE Connectivity Ltd

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 JPC Connectivity

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

- 12.10 EDGE Optical Solutions

- 12.10.1 Key Facts

- 12.10.2 Business Description

- 12.10.3 Products and Services

- 12.10.4 Financial Overview

- 12.10.5 SWOT Analysis

- 12.10.6 Key Developments

13. Appendix

- 13.1 About The Insight Partners