|

|

市場調査レポート

商品コード

1597070

北米のバイオプロセス市場:2031年までの予測 - 地域別分析 - 製品別、事業規模別、プロセス別、用途別、エンドユーザー別North America Bioprocessing Market Forecast to 2031 - Regional Analysis - by Product, Scale of Operation, Process, Application, and End User |

||||||

|

|||||||

|

|||||||

| 北米のバイオプロセス市場:2031年までの予測 - 地域別分析 - 製品別、事業規模別、プロセス別、用途別、エンドユーザー別 |

|

出版日: 2024年10月03日

発行: The Insight Partners

ページ情報: 英文 151 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

北米のバイオプロセス市場は、2023年に124億4,060万米ドルとなり、2031年までには359億5,043万米ドルに達すると予測され、2023年から2031年までのCAGRは14.2%と推定されます。

慢性疾患の増加が北米のバイオプロセス市場を活性化

高齢者の座りがちな生活は、肥満や糖尿病などの生活習慣病の有病率を高めています。また、遺伝的な遺伝子が、心血管疾患(CVDs)、アルツハイマー病、うつ病などの他の健康上の懸念とともに、これらの状態を表すこともあります。National Council on Aging, Inc.によると、成人(65歳以上)の80%が生涯に少なくとも1つの慢性疾患に罹患すると報告されています。米国疾病予防管理センター(CDC)によると、2020年には米国では10人中約6人が少なくとも1つの深刻な病気にかかり、10人中4人が2つ以上の慢性疾患を抱えています。WHOによると、2020年には、60歳以上の成人の数が5歳未満の子どもの数を上回るといいます。世界人口に占める60歳以上の割合は、2015年から2050年の間に12%から22%へとほぼ倍増します。認知症、変形性関節症、がん、脳卒中、心血管疾患など、数多くの慢性疾患が加齢と関連していることが知られています。狭心症、アテローム性動脈硬化症、多忙なライフスタイルが原因の急性心筋梗塞などのCVDは、世界中で死亡率の大きな原因のひとつとなっています。世界心臓財団によると、CVDによる死亡率は過去30年間(1990年~2020年)で60%も急増しています。2021年にはCVDが原因で2,050万人の死亡が記録されました。糖尿病は、生命を脅かす慢性疾患のひとつであり、機能的な治療法はありません。あらゆるタイプの糖尿病は、身体の様々な部位に様々な合併症を引き起こし、それによって全体的な死亡リスクを増大させます。国際糖尿病連合によると、北米の糖尿病患者数は2017年の4,600万人から2045年には6,200万人に増加すると予測されています。さらに、2017年には4億2,500万人が糖尿病を患っていましたが、2045年には全世界で6億2,900万人に達すると予測されており、これは約35%の増加です。2020年に発表されたGlobal Cancer Observatory(GLOBOCAN)の推計によると、世界中で1,930万人のがん患者が報告されています。症例数は米国、中国、インドで著しく高くなりました。同様に、2022年2月に発表された世界保健機関のデータでは、世界中で1,000万人以上ががんで死亡しています。がん罹患率の増加は、革新的ながん治療の必要性を示しています。モノクローナル抗体は、がん細胞の活動を抑制し、がん細胞を排除する免疫系の自然な能力を高める、標的抗がん剤の有望なクラスです。抗体薬物複合体(ADC)もまた、がん治療において有望な結果を示しています。専門医、患者、プライマリ・ケアの臨床医、その他のヘルスケア専門家によって、バイオシミラーが効率的で安全であると認識されていることが、その需要を後押ししています。バイオシミラーは何百万人もの患者の生活の質を改善することが証明されています。バイオシミラー医薬品は、慢性皮膚疾患(乾癬やアトピー性皮膚炎など)、腸疾患(クローン病、過敏性腸症候群、大腸炎など)、糖尿病、自己免疫疾患、がん、腎臓疾患、関節炎など、多くの疾患の治療に有効であり、費用対効果も高いです。バイオシミラー医薬品の開発企業は、より低い製造コストを実現するために高度なバイオプロセス技術を採用しており、これは最終的な消費者価格を決定する重要な要素となっています。ほぼすべてのバイオシミラー開発企業は、最新の最先端バイオプロセス技術を使用しています。そのため、慢性疾患の蔓延に伴い、生命を脅かす病気を治療するバイオシミラーの需要が急増しており、バイオプロセスの需要を促進しています。

北米のバイオプロセス市場概要

遺伝性疾患や細胞性疾患の増加により、細胞治療の需要が増加しています。米国製薬研究製造者協会(PhRMA)の細胞・遺伝子治療パイプラインに関する報告書(2020年発行)によると、米国ではがんから遺伝性疾患、神経疾患まで、さまざまな疾患や病態をターゲットとした細胞・遺伝子治療が400種類も開発中であることが明らかになりました。2023年4月、Cytivaはシングルユース製品で上流のバイオプロセス業務を簡素化するX-platformバイオリアクターを発売しました。当初、これらのバイオリアクターは50Lと200Lのサイズで利用可能でした。X-Platformバイオリアクターは現在、Figurate自動化ソリューション・ソフトウェアを搭載しており、人間工学的な改善、生産能力、サプライチェーン業務の簡素化を通じて、プロセス効率を向上させることができます。

主に技術の進歩、柔軟性の向上、運用コストの低下によるバイオ医薬品分野の成長は、米国のバイオプロセス市場にも利益をもたらしています。国際貿易局(ITA)によると、米国はバイオ医薬品の最大市場であり、研究開発の世界的リーダーです。PhRMAによると、米国企業は世界のバイオ医薬品研究開発業務の50%近くを占めており、知的財産権を保有する多くの新薬の開発に成功しています。このように、臨床試験の成果を向上させ、患者の安全性を確保するために、米国を拠点とするバイオ医薬品・バイオテクノロジー企業による研究開発投資が増加していること、また、米国政府による投資の増加に伴い、精密医療への牽引力が高まっていることが、米国のバイオプロセス市場の成長に寄与しています。

北米のバイオプロセス市場の収益と2031年までの予測(金額)

北米のバイオプロセス市場のセグメンテーション

北米のバイオプロセス市場は、製品、事業規模、プロセス、用途、エンドユーザー、国に分類されます。

製品別では、北米のバイオプロセス市場は機器と消耗品・アクセサリーに二分されます。2023年の市場シェアは機器セグメントが大きいです。さらに、機器セグメントは、ろ過装置、バイオリアクター、クロマトグラフィーシステム、遠心分離機、乾燥装置、その他にサブセグメント化されます。さらに、バイオリアクターのサブセグメントは、パイロットスケール、フルスケール、ラボスケールに分類されます。さらに、クロマトグラフィーシステムのサブセグメントは、液体クロマトグラフィー、ガスクロマトグラフィー、その他に分類されます。さらに、消耗品・アクセサリーセグメントは、試薬、細胞培養メデューム、クロマトグラフィー樹脂、その他にサブセグメント化されています。

事業規模の観点から、北米のバイオプロセス市場は商業事業と臨床事業に二分されます。2023年の市場シェアは、商業オペレーション分野が大きくなりました。

プロセス別では、北米のバイオプロセス市場は下流バイオプロセスと上流バイオプロセスに二分されます。2023年には下流バイオプロセス分野がより大きな市場シェアを占めています。

用途別では、北米のバイオプロセス市場はモノクローナル抗体、ワクチン、組み換えタンパク質、細胞・遺伝子治療、その他に分類されます。モノクローナル抗体セグメントは2023年に最大の市場シェアを占めました。

エンドユーザー別では、北米のバイオプロセス市場はバイオ製薬企業、受託製造機関、その他に分類されます。バイオ製薬会社セグメントが2023年に最大の市場シェアを占めました。

国別では、北米のバイオプロセス市場は米国、カナダ、メキシコに区分されます。2023年の北米のバイオプロセス市場シェアは米国が独占しました。

Getinge AB、Thermo Fisher Scientific Inc、Sartorius AG、Corning Inc、Bio-Rad Laboratories Inc、Merck KGaA、3M Co、Eppendorf SE、Repligen Corp、Entegris Inc、Agilent Technologies Inc、Cytiva US LLC.は、北米のバイオプロセス市場で事業を展開する主要企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要な洞察

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 北米のバイオプロセス市場情勢

- エコシステム分析

- バリューチェーンのベンダー一覧

第5章 北米のバイオプロセス市場:主要市場力学

- 市場促進要因

- 慢性疾患の増加

- バイオ医薬品産業の成長

- 市場抑制要因

- バイオプロセスに関連する厳しい規制政策と制限

- 市場機会

- 個別化医療への需要の高まり

- 今後の動向

- 細胞治療製造の自動化へのシフト

- 促進要因と抑制要因の影響

第6章 バイオプロセス市場:北米分析

- バイオプロセス市場の収益、2021年~2031年

第7章 北米のバイオプロセス市場分析:製品別

- 機器

- 消耗品・アクセサリー

第8章 北米のバイオプロセス市場分析:事業規模別

- 商業業務

- 臨床業務

第9章 北米のバイオプロセス市場分析:プロセス別

- 下流バイオプロセス

- 上流バイオプロセス

第10章 北米のバイオプロセス市場分析:用途別

- モノクローナル抗体

- ワクチン

- 組み換えタンパク質

- 細胞・遺伝子治療

- その他

第11章 北米のバイオプロセス市場分析:エンドユーザー別

- バイオ医薬品企業

- 製造受託機関

- その他

第12章 北米のバイオプロセス市場:国別分析

- 北米

- 米国

- カナダ

- メキシコ

第13章 業界情勢

- バイオプロセス市場における成長戦略

- 無機的成長戦略

- 有機的成長戦略

第14章 企業プロファイル

- Getinge AB

- Thermo Fisher Scientific Inc

- Sartorius AG

- Corning Inc

- Bio-Rad Laboratories Inc

- Merck KGaA

- 3M Co

- Eppendorf SE

- Repligen Corp

- Entegris Inc

- Agilent Technologies Inc

- Cytiva US LLC

第15章 付録

List Of Tables

- Table 1. North America Bioprocessing Market Segmentation

- Table 2. List of Vendors

- Table 3. Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - By Instruments

- Table 4. Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - By Bioreactors

- Table 5. Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - By Chromatography Systems

- Table 6. Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - By Consumables & Accessories

- Table 7. United States: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Product

- Table 8. United States: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Instruments

- Table 9. United States: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Bioreactors

- Table 10. United States: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Chromatography Systems

- Table 11. United States: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Consumables & Accessories

- Table 12. United States: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Scale of Operation

- Table 13. United States: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Process

- Table 14. United States: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Application

- Table 15. United States: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by End User

- Table 16. Canada: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Product

- Table 17. Canada: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Instruments

- Table 18. Canada: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Bioreactors

- Table 19. Canada: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Chromatography Systems

- Table 20. Canada: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Consumables & Accessories

- Table 21. Canada: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Scale of Operation

- Table 22. Canada: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Process

- Table 23. Canada: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Application

- Table 24. Canada: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by End User

- Table 25. Mexico: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Product

- Table 26. Mexico: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Instruments

- Table 27. Mexico: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Bioreactors

- Table 28. Mexico: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Chromatography Systems

- Table 29. Mexico: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Consumables & Accessories

- Table 30. Mexico: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Scale of Operation

- Table 31. Mexico: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Process

- Table 32. Mexico: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by Application

- Table 33. Mexico: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - by End User

- Table 34. Recent Inorganic Growth Strategies in the Bioprocessing Market

- Table 35. Recent Organic Growth Strategies in the Bioprocessing Market

- Table 36. Glossary of Terms, Bioprocessing Market

List Of Figures

- Figure 1. North America Bioprocessing Market Segmentation, by Country

- Figure 2. Bioprocessing Market - Key Market Dynamics

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Bioprocessing Market Revenue (US$ Million), 2021-2031

- Figure 5. Bioprocessing Market Share (%) - by Product (2023 and 2031)

- Figure 6. Instruments: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 7. Consumables & Accessories: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 8. Bioprocessing Market Share (%) - by Scale of Operation (2023 and 2031)

- Figure 9. Commercial Operations: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 10. Clinical Operations: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 11. Bioprocessing Market Share (%) - by Process (2023 and 2031)

- Figure 12. Downstream Bioprocess: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 13. Upstream Bioprocess: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 14. Bioprocessing Market Share (%) - by Application (2023 and 2031)

- Figure 15. Monoclonal Antibodies: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 16. Vaccines: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 17. Recombinant Protein: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

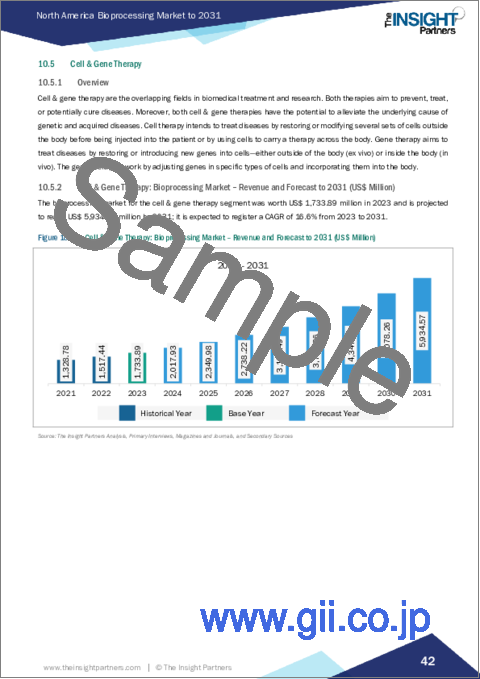

- Figure 18. Cell & Gene Therapy: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 19. Others: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 20. Bioprocessing Market Share (%) - by End User (2023 and 2031)

- Figure 21. Biopharmaceutical Companies: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 22. Contract Manufacturing Organization: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 23. Others: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 24. North America: Bioprocessing Market, by Key Country - Revenue (2023) (US$ Million)

- Figure 25. North America: Bioprocessing Market Breakdown, by Key Countries, 2023 and 2031 (%)

- Figure 26. United States: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 27. Canada: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 28. Mexico: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 29. Growth Strategies in the Bioprocessing Market

The North America bioprocessing market was valued at US$ 12,440.60 million in 2023 and is expected to reach US$ 35,950.43 million by 2031; it is estimated to register a CAGR of 14.2% from 2023 to 2031.

Increasing Prevalence of Chronic Diseases Fuels North America Bioprocessing Market

The sedentary life of older people has boosted the prevalence of lifestyle disorders, such as obesity and diabetes. Inherited genes can also express these conditions along with other health concerns such as cardiovascular disease (CVDs), Alzheimer's disease, and depression. As per the National Council on Aging, Inc., 80% of adults (aged 65 and more) are reported to suffer from at least one chronic condition in their lifetime. According to the Centers for Disease Control and Prevention (CDC), approximately 6 of 10 people in the US suffered from at least one serious disease, and 4 of 10 people had two or more chronic conditions in 2020. According to WHO, in 2020, there were more adults over 60 than children under five. The percentage of the global population over 60 will almost double from 12% to 22% between 2015 and 2050. Numerous chronic disorders, such as dementia, osteoarthritis, cancer, stroke, and cardiovascular disease, are known to be associated with aging. CVDs, such as angina pectoris, atherosclerosis, and acute myocardial infarction caused because of hectic lifestyles, are among the significant causes of mortality across the world. As per the World Heart Foundation, mortality caused due to CVD has surged by 60% over the past 30 years (1990-2020). 20.5 million deaths were recorded in 2021 due to CVDs. Diabetes is one of the life-threatening chronic diseases with no functional cure. Diabetes of all types can cause various complications in different body parts, thereby increasing the overall risk of death. According to the International Diabetes Federation, the number of diabetic cases in North America is anticipated to grow from 46 million in 2017 to 62 million by 2045. Additionally, 425 million people had diabetes in 2017, and the number is anticipated to reach 629 million by 2045 worldwide, which is an increase of about 35%. As per the Global Cancer Observatory (GLOBOCAN) estimates published in 2020, 19.3 million cancer cases were reported across the world. The number of cases was significantly high in the US, China, and India. Similarly, as per the World Health Organization data published in February 2022, ~10 million people across the world have succumbed to death due to cancer. An upsurge in the incidence of cancer indicates the need for innovative cancer treatments. Monoclonal antibodies represent a promising class of targeted anticancer agents that enhance the natural ability of immune systems to suppress cancer cell activity and eliminate cancer cells. Antibody-drug conjugates (ADCs) have also shown promising results in cancer treatment. The recognition of biosimilars as efficient and safe by specialists, patients, primary care clinicians, and other healthcare professionals is propelling its demand. Biosimilars have been proven to improve the quality of life for millions of patients. They are impactful and cost-effective options for treating many diseases, including chronic skin conditions (such as psoriasis and atopic dermatitis), bowel diseases (such as Crohn's disease, irritable bowel syndrome, and colitis), diabetes, autoimmune disease, cancer, kidney conditions, and arthritis. Biosimilar developers are adopting advanced bioprocessing technologies to achieve lower manufacturing costs, which is an important factor in determining the final consumer prices. Nearly all biosimilar developers are using modern, cutting-edge bioprocessing techniques. Therefore, with the growing prevalence of chronic diseases, the demand for biosimilars to treat life-threatening illnesses is spurring, thereby propelling the demand for bioprocessing.

North America Bioprocessing Market Overview

Growing incidences of genetic and cellular disorders are leading to increasing demand for cell therapies. The Pharmaceutical Research and Manufacturers Association (PhRMA)'s report on the cell & gene therapy pipeline (published in 2020), revealed that there are 400 cell and gene therapies in development for targeting a variety of diseases and conditions from cancer to genetic disorders to neurologic conditions in the US. In April 2023, Cytiva launched X-platform bioreactors to simplify upstream bioprocessing operations with single-use products. Initially, these bioreactors were available in the sizes of 50 L and 200 L. The X-Platform bioreactors are now equipped with Figurate automation solution software, and they can increase process efficiency through ergonomic improvements, production capacity, and simplified supply chain operations.

The growth of the biopharmaceutical sector, mainly due to technological advancements, increasing flexibility, and low operational costs, also benefits the bioprocessing market in the US. As per the International Trade Administration (ITA), the US is the largest market for biopharmaceuticals and the global leader in R&D. According to the PhRMA, companies in the US account for nearly 50% of the global biopharmaceutical R&D work, and they have succeeded in developing many novel medicines for which they hold intellectual property rights. Thus, the increasing R&D investments by US-based biopharmaceutical and biotechnology companies to improve outcomes of clinical trials and ensure patient safety, and the growing traction toward precision medicine with rising investments by the US government contribute to the growth of the bioprocessing market in the US.

North America Bioprocessing Market Revenue and Forecast to 2031 (US$ Million)

North America Bioprocessing Market Segmentation

The North America bioprocessing market is categorized into product, scale of operation, process, application, end user, and country.

Based on product, the North America bioprocessing market is bifurcated into instruments and consumables & accessories. The instruments segment held a larger market share in 2023. Furthermore, the instruments segment is sub segmented into filtration devices, bioreactors, chromatography systems, centrifuge, drying devices, and others. Additionally, the bioreactors subsegment is categorized into pilot scale, full scale, and laboratory scale. Furthermore, the sub segment chromatography systems is segmented into liquid chromatography, gas chromatography, and others. Additionally, the consumables & accessories segment is sub segmented into reagents, cell culture media, chromatography resins, and others.

In terms of scale of operation, the North America bioprocessing market is bifurcated into commercial operations and clinical operations. The commercial operations segment held a larger market share in 2023.

By process, the North America bioprocessing market is bifurcated into downstream bioprocess and upstream bioprocess. The downstream bioprocess segment held a larger market share in 2023.

Based on application, the North America bioprocessing market is categorized into monoclonal antibodies, vaccines, recombinant protein, cell & gene therapy, and others. The monoclonal antibodies segment held the largest market share in 2023.

In terms of end user, the North America bioprocessing market is categorized into biopharmaceutical companies, contract manufacturing organization, and others. The biopharmaceutical companies segment held the largest market share in 2023.

By country, the North America bioprocessing market is segmented into the US, Canada, and Mexico. The US dominated the North America bioprocessing market share in 2023.

Getinge AB, Thermo Fisher Scientific Inc, Sartorius AG, Corning Inc, Bio-Rad Laboratories Inc, Merck KGaA, 3M Co, Eppendorf SE, Repligen Corp, Entegris Inc, Agilent Technologies Inc, and Cytiva US LLC. are some of the leading companies operating in the North America bioprocessing market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. North America Bioprocessing Market Landscape

- 4.1 Ecosystem Analysis

- 4.1.1 List of Vendors in the Value Chain

5. North America Bioprocessing Market - Key Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Increasing Prevalence of Chronic Diseases

- 5.1.2 Growing Biopharmaceutical Industry

- 5.2 Market Restraints

- 5.2.1 Stringent Regulatory Policies and Limitations Associated with Bioprocessing

- 5.3 Market Opportunities

- 5.3.1 Proliferating Demand for Personalized Medicine

- 5.4 Future Trends

- 5.4.1 Shift Toward Automated Cell Therapy Manufacturing

- 5.5 Impact of Drivers and Restraints:

6. Bioprocessing Market - North America Analysis

- 6.1 Bioprocessing Market Revenue (US$ Million), 2021-2031

7. North America Bioprocessing Market Analysis - by Product

- 7.1 Overview

- 7.2 Instruments

- 7.2.1 Overview

- 7.2.2 Instruments: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 7.2.2.1 Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - By Instruments

- 7.2.2.1.1 Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - By Bioreactors

- 7.2.2.1.2 Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - By Chromatography Systems

- 7.2.2.1 Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - By Instruments

- 7.3 Consumables & Accessories

- 7.3.1 Overview

- 7.3.2 Consumables & Accessories: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 7.3.2.1 Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million) - By Consumables & Accessories

8. North America Bioprocessing Market Analysis - by Scale of Operation

- 8.1 Overview

- 8.2 Commercial Operations

- 8.2.1 Overview

- 8.2.2 Commercial Operations: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 8.3 Clinical Operations

- 8.3.1 Overview

- 8.3.2 Clinical Operations: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

9. North America Bioprocessing Market Analysis - by Process

- 9.1 Overview

- 9.2 Downstream Bioprocess

- 9.2.1 Overview

- 9.2.2 Downstream Bioprocess: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 9.3 Upstream Bioprocess

- 9.3.1 Overview

- 9.3.2 Upstream Bioprocess: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

10. North America Bioprocessing Market Analysis - by Application

- 10.1 Overview

- 10.2 Monoclonal Antibodies

- 10.2.1 Overview

- 10.2.2 Monoclonal Antibodies: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 10.3 Vaccines

- 10.3.1 Overview

- 10.3.2 Vaccines: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 10.4 Recombinant Protein

- 10.4.1 Overview

- 10.4.2 Recombinant Protein: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 10.5 Cell & Gene Therapy

- 10.5.1 Overview

- 10.5.2 Cell & Gene Therapy: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 10.6 Others

- 10.6.1 Overview

- 10.6.2 Others: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

11. North America Bioprocessing Market Analysis - by End User

- 11.1 Overview

- 11.2 Biopharmaceutical Companies

- 11.2.1 Overview

- 11.2.2 Biopharmaceutical Companies: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 11.3 Contract Manufacturing Organization

- 11.3.1 Overview

- 11.3.2 Contract Manufacturing Organization: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 11.4 Others

- 11.4.1 Overview

- 11.4.2 Others: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

12. North America Bioprocessing Market - Country Analysis

- 12.1 North America: Bioprocessing Market Overview

- 12.1.1 North America: Bioprocessing Market - Revenue and Forecast Analysis - by Country

- 12.1.1.1 United States: Bioprocessing Market- Revenue and Forecast to 2031 (US$ Million)

- 12.1.1.2 Overview

- 12.1.1.3 United States: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 12.1.1.3.1 United States: Bioprocessing Market Breakdown, by Product

- 12.1.1.3.1.1 United States: Bioprocessing Market Breakdown, by Instruments

- 12.1.1.3.1.1.1 United States: Bioprocessing Market Breakdown, by Bioreactors

- 12.1.1.3.1.1.2 United States: Bioprocessing Market Breakdown, by Chromatography Systems

- 12.1.1.3.1.2 United States: Bioprocessing Market Breakdown, by Consumables & Accessories

- 12.1.1.3.2 United States: Bioprocessing Market Breakdown, by Scale of Operation

- 12.1.1.3.3 United States: Bioprocessing Market Breakdown, by Process

- 12.1.1.3.4 United States: Bioprocessing Market Breakdown, by Application

- 12.1.1.3.5 United States: Bioprocessing Market Breakdown, by End User

- 12.1.1.4 Canada: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 12.1.1.4.1 Overview

- 12.1.1.5 Canada: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 12.1.1.5.1 Canada: Bioprocessing Market Breakdown, by Product

- 12.1.1.5.1.1 Canada: Bioprocessing Market Breakdown, by Instruments

- 12.1.1.5.1.1.1 Canada: Bioprocessing Market Breakdown, by Bioreactors

- 12.1.1.5.1.1.2 Canada: Bioprocessing Market Breakdown, by Chromatography Systems

- 12.1.1.5.1.2 Canada: Bioprocessing Market Breakdown, by Consumables & Accessories

- 12.1.1.5.2 Canada: Bioprocessing Market Breakdown, by Scale of Operation

- 12.1.1.5.3 Canada: Bioprocessing Market Breakdown, by Process

- 12.1.1.5.4 Canada: Bioprocessing Market Breakdown, by Application

- 12.1.1.5.5 Canada: Bioprocessing Market Breakdown, by End User

- 12.1.1.6 Mexico: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 12.1.1.6.1 Overview

- 12.1.1.7 Mexico: Bioprocessing Market - Revenue and Forecast to 2031 (US$ Million)

- 12.1.1.7.1 Mexico: Bioprocessing Market Breakdown, by Product

- 12.1.1.7.1.1 Mexico: Bioprocessing Market Breakdown, by Instruments

- 12.1.1.7.1.1.1 Mexico: Bioprocessing Market Breakdown, by Bioreactors

- 12.1.1.7.1.1.2 Mexico: Bioprocessing Market Breakdown, by Chromatography Systems

- 12.1.1.7.1.2 Mexico: Bioprocessing Market Breakdown, by Consumables & Accessories

- 12.1.1.7.2 Mexico: Bioprocessing Market Breakdown, by Scale of Operation

- 12.1.1.7.3 Mexico: Bioprocessing Market Breakdown, by Process

- 12.1.1.7.4 Mexico: Bioprocessing Market Breakdown, by Application

- 12.1.1.7.5 Mexico: Bioprocessing Market Breakdown, by End User

- 12.1.1 North America: Bioprocessing Market - Revenue and Forecast Analysis - by Country

13. Industry Landscape

- 13.1 Overview

- 13.2 Growth Strategies in the Bioprocessing Market

- 13.3 Inorganic Growth Strategies

- 13.3.1 Overview

- 13.4 Organic Growth Strategies

- 13.4.1 Overview

14. Company Profiles

- 14.1 Getinge AB

- 14.1.1 Key Facts

- 14.1.2 Business Description

- 14.1.3 Products and Services

- 14.1.4 Financial Overview

- 14.1.5 SWOT Analysis

- 14.1.6 Key Developments

- 14.2 Thermo Fisher Scientific Inc

- 14.2.1 Key Facts

- 14.2.2 Business Description

- 14.2.3 Products and Services

- 14.2.4 Financial Overview

- 14.2.5 SWOT Analysis

- 14.2.6 Key Developments

- 14.3 Sartorius AG

- 14.3.1 Key Facts

- 14.3.2 Business Description

- 14.3.3 Products and Services

- 14.3.4 Financial Overview

- 14.3.5 SWOT Analysis

- 14.3.6 Key Developments

- 14.4 Corning Inc

- 14.4.1 Key Facts

- 14.4.2 Business Description

- 14.4.3 Products and Services

- 14.4.4 Financial Overview

- 14.4.5 SWOT Analysis

- 14.4.6 Key Developments

- 14.5 Bio-Rad Laboratories Inc

- 14.5.1 Key Facts

- 14.5.2 Business Description

- 14.5.3 Products and Services

- 14.5.4 Financial Overview

- 14.5.5 SWOT Analysis

- 14.5.6 Key Developments

- 14.6 Merck KGaA

- 14.6.1 Key Facts

- 14.6.2 Business Description

- 14.6.3 Products and Services

- 14.6.4 Financial Overview

- 14.6.5 SWOT Analysis

- 14.6.6 Key Developments

- 14.7 3M Co

- 14.7.1 Key Facts

- 14.7.2 Business Description

- 14.7.3 Products and Services

- 14.7.4 Financial Overview

- 14.7.5 SWOT Analysis

- 14.7.6 Key Developments

- 14.8 Eppendorf SE

- 14.8.1 Key Facts

- 14.8.2 Business Description

- 14.8.3 Products and Services

- 14.8.4 Financial Overview

- 14.8.5 SWOT Analysis

- 14.8.6 Key Developments

- 14.9 Repligen Corp

- 14.9.1 Key Facts

- 14.9.2 Business Description

- 14.9.3 Products and Services

- 14.9.4 Financial Overview

- 14.9.5 SWOT Analysis

- 14.9.6 Key Developments

- 14.10 Entegris Inc

- 14.10.1 Key Facts

- 14.10.2 Business Description

- 14.10.3 Products and Services

- 14.10.4 Financial Overview

- 14.10.5 SWOT Analysis

- 14.10.6 Key Developments

- 14.11 Agilent Technologies Inc

- 14.11.1 Key Facts

- 14.11.2 Business Description

- 14.11.3 Products and Services

- 14.11.4 Financial Overview

- 14.11.5 SWOT Analysis

- 14.11.6 Key Developments

- 14.12 Cytiva US LLC

- 14.12.1 Key Facts

- 14.12.2 Business Description

- 14.12.3 Products and Services

- 14.12.4 Financial Overview

- 14.12.5 SWOT Analysis

- 14.12.6 Key Developments

15. Appendix

- 15.1 About The Insight Partners

- 15.2 Glossary of Terms